|

市場調査レポート

商品コード

1928918

衛星モデム市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Satellite Modem Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 衛星モデム市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2026年01月09日

発行: Global Market Insights Inc.

ページ情報: 英文 165 Pages

納期: 2~3営業日

|

概要

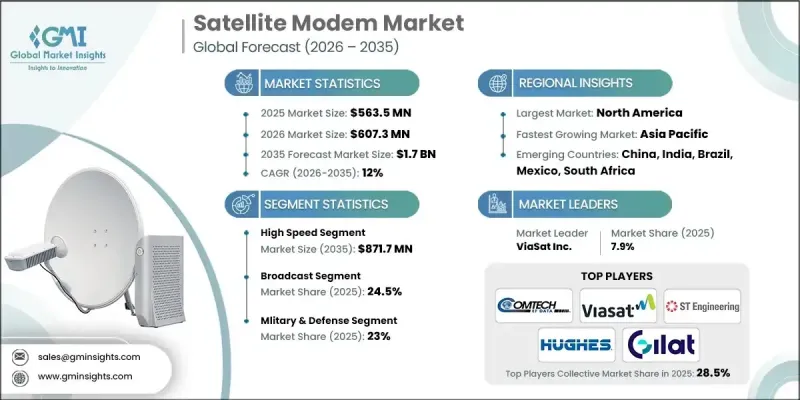

世界の衛星モデム市場は、2025年に5億6,350万米ドルと評価され、2035年までにCAGR 12%で成長し、17億米ドルに達すると予測されています。

市場成長は、世界中の防衛・安全保障活動における衛星通信システムへの依存度の高まりに大きく影響されています。軍事組織が安全で途切れのないデータ交換をより重視するにつれ、厳格な性能・セキュリティ基準を満たす高度な衛星モデムへの需要が高まっています。これらのソリューションは、保護された通信、リアルタイムの作戦可視性、指揮統制の支援において広く認知されており、高度に専門化されたモデム技術の開発を推進してきました。防衛分野以外では、サービスが行き届いていない地域や地理的に孤立した地域における信頼性の高いブロードバンド接続への需要拡大が、市場の普及を加速させています。衛星モデム技術は、従来のインフラが整備できない地域においても安定したインターネットアクセスを実現し、商業・機関・住宅ユーザーにわたる接続ニーズを支えます。衛星通信システムにおいて、これらのモデムはデジタル情報を無線信号に変換して上りリンクで送信し、受信信号を再び利用可能なデジタルデータに変換する機能を果たします。衛星ネットワーク拡張への継続的な投資が、市場の長期的な成長見通しを強化しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 5億6,350万米ドル |

| 予測金額 | 17億米ドル |

| CAGR | 12% |

高速セグメントは、2035年までに8億7,170万米ドルに達すると予測されています。このセグメントは、データ集約型アプリケーションにおける高速データ伝送、低遅延、シームレスなパフォーマンスへの需要が高まるにつれ、注目を集めています。モデム設計の進歩に加え、データ変調および符号化技術の改善により、より高いスループットレートとサービス品質の向上が可能となり、幅広い帯域幅を必要とする使用事例をサポートしています。

放送セグメントは2025年に24.5%のシェアを占めました。デジタルメディア配信における消費パターンの変化が本セグメントを再構築しており、衛星モデムは大規模な動画配信、信号品質の向上、効率的な帯域幅利用に対応するよう最適化が進んでいます。これらの強化により、コンテンツプロバイダーは伝送遅延を抑えつつ、より効果的に番組を配信することが可能となっています。

米国衛星モデム市場は2025年に1億7,380万米ドルに達しました。同国における市場拡大は、遠隔地間通信、防衛ネットワーク、企業ITシステムにおける信頼性の高い通信ニーズの高まりによって支えられています。先進的なバックホールソリューションや接続デバイスエコシステムを含む次世代技術の採用は、高い適応性と性能を提供する柔軟なソフトウェア駆動型モデムプラットフォームの利用を促進しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 遠隔地域における高速インターネットアクセス需要の増加

- 海事・航空分野における衛星通信の採用拡大

- 衛星を利用した放送およびメディアサービスの拡大

- 軍事・防衛用途における衛星ネットワークの展開拡大

- 業界の潜在的リスク&課題

- 大気条件への依存度

- 技術的陳腐化

- 市場機会

- 低軌道(LEO)衛星コンステレーションの成長

- 小型衛星プラットフォームの小型化と電力効率化

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 新興ビジネスモデル

- コンプライアンス要件

- 特許および知的財産分析

- 地政学的・貿易動向

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 主要企業の競合ベンチマーキング

- 財務実績比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオ比較

- 製品ラインの広さ

- 技術

- イノベーション

- 地域別展開比較

- 世界展開分析

- サービスネットワークのカバー率

- 地域別市場浸透率

- 競合ポジショニングマトリックス

- リーダー企業

- 課題者

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績比較

- 主な発展, 2021-2024

- 合併・買収

- 提携および共同事業

- 技術的進歩

- 拡大と投資戦略

- デジタルトランスフォーメーションの取り組み

- 新興/スタートアップ競合の動向

第5章 市場推計・予測:チャネルタイプ別、2022-2035

- シングルチャネル・パー・キャリア(SCPC)モデム

- 多重チャネル・パー・キャリア(MCPC)モデム

第6章 市場推計・予測:データレート別、2022-2035

- 高速

- ミドルレンジ

- エントリーレベル

第7章 市場推計・予測:用途別、2022-2035

- 放送

- 企業向け・ブロードバンド

- 機内接続

- IPトランキング

- モバイル・バックホール

- オフショア通信

- 追跡・監視

- その他

第8章 市場推計・予測:最終用途産業別、2022-2035

- エネルギー・公益事業

- 政府

- 船舶

- メディア・エンターテインメント

- 軍事・防衛

- 鉱業

- 石油・ガス

- 通信

- 運輸・物流

- その他

第9章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- 世界の主要企業

- Comtech EF Data Corporation

- Hughes Network Systems

- Iridium Communications Inc.

- ViaSat Inc.

- 地域別主要企業

- 北米

- Datum Systems Inc.

- ORBCOMM INC.

- Teledyne Paradise Datacom

- 欧州

- ND SATCOM

- Rohde &Schwarz Inradios Gmbh

- WORK Microwave GmbH

- アジア太平洋

- ST Engineering

- Gilat Satellite Networks Ltd.

- Thuraya Telecommunications Company

- 北米

- ニッチプレイヤー/ディスラプター

- Amplus Communication Pvt. Ltd.

- Ayecka Communication Systems Ltd.

- NOVELSAT

- Ntvsat

- SatixFy