|

市場調査レポート

商品コード

1740977

蒸気タービンサービス市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測Steam Turbine Service Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 蒸気タービンサービス市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月17日

発行: Global Market Insights Inc.

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

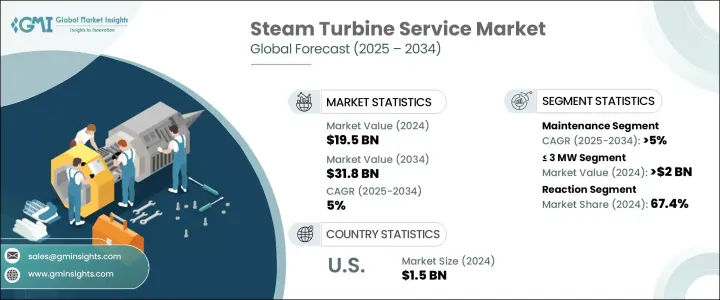

蒸気タービンサービスの世界市場規模は、2024年に195億米ドルとなり、火力発電の需要増加、アップグレードを必要とするタービンの老朽化、運転効率の最適化への注目の高まりなどを背景に、CAGR 5%で成長し、2034年には318億米ドルに達すると予測されています。

蒸気タービンサービスは、発電、石油・ガス、工業製造などの産業において、タービンのライフサイクルと性能を向上させるために設計されたメンテナンス、修理、オーバーホール(MRO)活動を包含します。ダウンタイムの削減とエネルギー出力の向上が重視される中、タービンの機能を最適化するための予知保全、デジタル監視、高度な修理ソリューションへの投資が増加しています。

エネルギー効率と排出基準の厳格化を推進する政府の取り組みが、発電事業者と産業事業者に蒸気タービンの定期的な整備への投資をさらに促しています。老朽化した石炭およびガスベースのプラントの近代化は、熱電併給(CHP)プロジェクトの出現とともに、包括的なサービス・ソリューションの需要に拍車をかけています。サービスプロバイダーはまた、エンドユーザーの進化する運用要件を満たすために、長期サービス契約(LTSA)やパフォーマンスベースの契約を含むカスタマイズされた契約を提供しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 195億米ドル |

| 予測金額 | 318億米ドル |

| CAGR | 5% |

蒸気タービンサービス市場は主に容量別に区分され、定格出力100MW超のタービンが2024年の市場をリードし、144億米ドルを生み出します。大容量タービンは、稼働の信頼性と高効率が重要な公益事業規模の火力発電所、原子力施設、産業用コージェネレーションプラントで主に使用されています。これらの大容量タービンの保守需要は、運転寿命を延ばし、変化する送電網規制や効率基準への適合を維持するための定期的な改修、部品交換、性能アップグレードの必要性によって推進されています。

設計別では、反応蒸気タービン分野が2024年に131億米ドルの評価額でサービス市場を独占しました。反応タービンは、高圧蒸気条件の処理効率が高いことで知られ、大規模な火力発電や原子力発電に広く導入されています。反応タービンの複雑な運転環境では、費用のかかる故障を防ぎ、出力レベルを維持するために、頻繁な検査、精密な修理、高度な診断サービスが必要となります。サービス・プロバイダーは、3Dスキャン、遠隔監視、積層造形などの技術を活用することで、より迅速で正確なメンテナンス・ソリューションを世界のリアクション・タービン・フリートに提供するようになってきています。

サービスの種類別では、修理分野が2024年に最大の市場シェアを占め、82億米ドルを占める。多くの蒸気タービンが設計寿命に達するか、それを超えているため、ブレードの改修、ローターの溶接、ケーシングの修復、効率の改修を含む修理サービスへの需要が高まっています。タイムリーな修理は、大きな故障を防ぐだけでなく、性能を回復し、燃料消費を最適化し、タービン全交換に伴う資本支出を先送りします。サービスプロバイダーは、ダウンタイムを最小限に抑え、顧客サービスを向上させるため、移動式サービスユニット、現場修理、デジタルツインテクノロジーによって修理能力を拡大しています。

2024年の蒸気タービンサービス世界市場は、火力発電所の大規模な設備ベースと堅調な産業活動に支えられ、アジア太平洋地域が96億米ドルを稼ぎ出し、世界をリードしました。中国、インド、日本、韓国などの国々がこの地域の成長を牽引しており、政府や電力会社が、急増する電力需要と持続可能性の目標に対応するため、既存のタービン資産の維持とアップグレードに多額の投資を行っています。送電網の安定化、石炭火力発電インフラの近代化、クリーン・コール・テクノロジーへの投資の増加は、この地域のサービス・プロバイダーに有利な機会を生み出しています。さらに、競争力のある地域密着型サービスを提供する大手OEMやサードパーティ・サービス・プロバイダの存在が、アジア太平洋市場の優位性をさらに強めています。

シーメンス・エナジー、ゼネラル・エレクトリック(GE)、三菱電機、エトスエナジー、スルザー・リミテッドなどの主要企業は、戦略的サービスの提供、デジタル化への取り組み、地域サービスセンターの拡大を通じて市場での地位を強化しています。これらの企業は、ユーティリティ企業や産業用顧客の進化するニーズに対応するため、フィールドサービス、状態監視、アップグレードソリューション、遠隔診断を含む包括的なサービスポートフォリオの提供にますます注力しています。AIを活用した予知保全プラットフォーム、モジュール式修理技術、柔軟なサービス契約などのイノベーションは、世界の蒸気タービンサービス市場の着実な成長を活かそうとする企業にとって極めて重要になってきています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:容量別、2021-2034

- 主要動向

- 3MW未満

- 3MW~100MW以上

- 100MW以上

第6章 市場規模・予測:デザイン別、2021-2034

- 主要動向

- 反応

- インパルス

第7章 市場規模・予測:サービス別、2021-2034

- 主要動向

- メンテナンス

- 修理

- オーバーホール

- その他

第8章 市場規模・予測:最終用途別、2021-2034

- 主要動向

- 産業

- ユーティリティ

第9章 市場規模・予測:サービスプロバイダー別、2021-2034

- 主要動向

- OEM

- 非OEM

第10章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ロシア

- ドイツ

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- 日本

- 韓国

- インド

- オーストラリア

- インドネシア

- マレーシア

- タイ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- イラン

- エジプト

- 南アフリカ

- ナイジェリア

- トルコ

- モロッコ

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

第11章 企業プロファイル

- EthosEnergy

- Fincantieri

- Fortum

- GE Vernova

- Goltens

- Mechanical Dynamics &Analysis

- Metalock Engineering

- Mitsubishi Power

- Power Services Group

- S.T. Cotter Turbine Services

- Siemens Energy

- Soderqvist Engineering Sweden

- Steam Turbine Services

- Sulzer

- Toshiba America Energy Systems

- Trillium Flow Technologies

- Triveni Turbine

- WEG

The Global Steam Turbine Service Market was valued at USD 19.5 billion in 2024 and is estimated to grow at a CAGR of 5% to reach USD 31.8 billion by 2034, driven by the rising demand for thermal power generation, the aging turbine fleet requiring upgrades, and increased focus on optimizing operational efficiency. Steam turbine service encompasses maintenance, repair, and overhaul (MRO) activities designed to enhance the lifecycle and performance of turbines across industries such as power generation, oil and gas, and industrial manufacturing. With a growing emphasis on reducing downtime and improving energy output, companies are increasingly investing in predictive maintenance, digital monitoring, and advanced repair solutions to ensure optimal turbine functionality.

Government initiatives promoting energy efficiency and stricter emission standards are further encouraging power producers and industrial operators to invest in the regular servicing of their steam turbines. Modernization of aging coal- and gas-based plants, along with the emergence of combined heat and power (CHP) projects, is fueling the demand for comprehensive service solutions. Service providers are also offering customized contracts, including long-term service agreements (LTSA) and performance-based contracts, to meet the evolving operational requirements of end-users.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $19.5 Billion |

| Forecast Value | $31.8 Billion |

| CAGR | 5% |

The Steam Turbine Service Market is primarily segmented by capacity, with turbines rated >100 MW leading the market in 2024, generating USD 14.4 billion. Large-capacity turbines are predominantly used in utility-scale thermal power plants, nuclear facilities, and industrial cogeneration plants, where operational reliability and high efficiency are critical. The demand for servicing these high-capacity turbines is being propelled by the need for periodic refurbishment, parts replacement, and performance upgrades to extend operational life and maintain compliance with changing grid regulations and efficiency norms.

By design, the reaction steam turbine segment dominated the service market in 2024 with a valuation of USD 13.1 billion. Reaction turbines, known for their efficiency at handling high-pressure steam conditions, are widely deployed in large-scale thermal and nuclear power generation. The complex operating environments of reaction turbines necessitate frequent inspections, precision repairs, and advanced diagnostic services to prevent costly failures and sustain output levels. Service providers are increasingly leveraging technologies such as 3D scanning, remote monitoring, and additive manufacturing to deliver faster and more precise maintenance solutions for reaction turbine fleets globally.

In terms of service type, the repair segment held the largest market share in 2024, accounting for USD 8.2 billion. As many steam turbines are reaching or surpassing their design lifespans, demand for repair services - including blade refurbishment, rotor welding, casing restoration, and efficiency retrofits - is rising. Timely repairs not only prevent major breakdowns but also restore performance, optimize fuel consumption, and defer the capital expenditure associated with complete turbine replacements. Service providers are expanding their repair capabilities with mobile service units, in-situ repairs, and digital twin technologies to minimize downtime and improve customer service.

Asia Pacific led the global Steam Turbine Service Market in 2024, generating USD 9.6 billion, supported by its large installed base of thermal power plants and robust industrial activity. Countries like China, India, Japan, and South Korea are driving regional growth, as governments and utilities invest heavily in maintaining and upgrading existing turbine assets to meet surging electricity demand and sustainability goals. The push for grid stability, modernization of coal-fired power infrastructure, and rising investments in clean coal technologies are creating lucrative opportunities for service providers across the region. Additionally, the presence of major OEMs and third-party service providers offering competitive, localized services further strengthens Asia Pacific's dominance in the market.

Leading companies such as Siemens Energy, General Electric (GE), Mitsubishi Power, EthosEnergy, and Sulzer Ltd. are reinforcing their market position through strategic service offerings, digitalization initiatives, and regional service center expansions. These players are increasingly focused on providing comprehensive service portfolios - encompassing field services, condition monitoring, upgrade solutions, and remote diagnostics - to cater to the evolving needs of utilities and industrial clients. Innovations such as AI-powered predictive maintenance platforms, modular repair techniques, and flexible service agreements are becoming pivotal for companies seeking to capitalize on the steady growth of the global Steam Turbine Service Market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Capacity, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 ≤ 3 MW

- 5.3 > 3 MW - 100 MW

- 5.4 > 100 MW

Chapter 6 Market Size and Forecast, By Design, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Reaction

- 6.3 Impulse

Chapter 7 Market Size and Forecast, By Service, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Maintenance

- 7.3 Repair

- 7.4 Overhaul

- 7.5 Others

Chapter 8 Market Size and Forecast, By End Use, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Industrial

- 8.3 Utility

Chapter 9 Market Size and Forecast, By Service Provider, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Non-OEM

Chapter 10 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 France

- 10.3.3 Russia

- 10.3.4 Germany

- 10.3.5 Spain

- 10.3.6 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 South Korea

- 10.4.4 India

- 10.4.5 Australia

- 10.4.6 Indonesia

- 10.4.7 Malaysia

- 10.4.8 Thailand

- 10.5 Middle East & Africa

- 10.5.1 Saudi Arabia

- 10.5.2 UAE

- 10.5.3 Iran

- 10.5.4 Egypt

- 10.5.5 South Africa

- 10.5.6 Nigeria

- 10.5.7 Turkey

- 10.5.8 Morocco

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Argentina

- 10.6.3 Chile

Chapter 11 Company Profiles

- 11.1 EthosEnergy

- 11.2 Fincantieri

- 11.3 Fortum

- 11.4 GE Vernova

- 11.5 Goltens

- 11.6 Mechanical Dynamics & Analysis

- 11.7 Metalock Engineering

- 11.8 Mitsubishi Power

- 11.9 Power Services Group

- 11.10 S.T. Cotter Turbine Services

- 11.11 Siemens Energy

- 11.12 Soderqvist Engineering Sweden

- 11.13 Steam Turbine Services

- 11.14 Sulzer

- 11.15 Toshiba America Energy Systems

- 11.16 Trillium Flow Technologies

- 11.17 Triveni Turbine

- 11.18 WEG