|

市場調査レポート

商品コード

1833665

血液透析カテーテル市場機会と促進要因、業界動向分析、2025年~2034年予測Hemodialysis Catheters Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 血液透析カテーテル市場機会と促進要因、業界動向分析、2025年~2034年予測 |

|

出版日: 2025年09月09日

発行: Global Market Insights Inc.

ページ情報: 英文 132 Pages

納期: 2~3営業日

|

概要

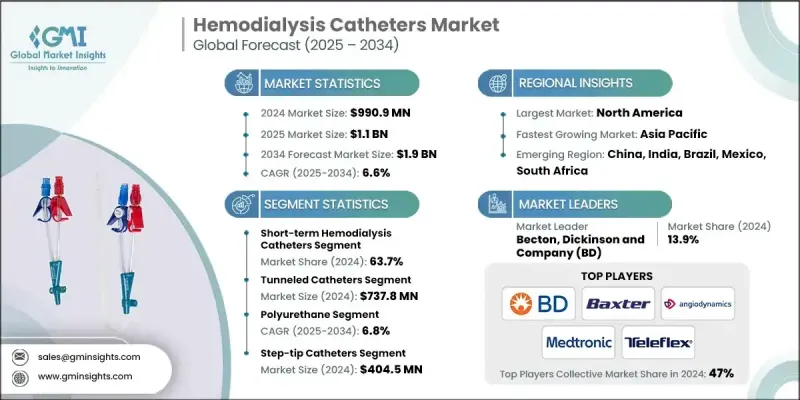

血液透析カテーテルの世界市場は、2024年には9億9,090万米ドルとなり、CAGR 6.6%で成長し、2034年には19億米ドルに達すると予測されています。

同市場の着実な成長は、透析治療への大きな需要を生み出す慢性腎臓病(CKD)および末期腎不全(ESRD)の有病率の増加に大きく関連しています。腎代替療法に対する意識の高まりが、各地域での採用をさらに加速させています。さらに、カテーテル設計の技術進歩や、生体適合性に優れ感染しにくい先進材料の導入が、業界の拡大に拍車をかけています。腎臓関連の合併症を起こしやすい世界人口の急速な高齢化も、患者の裾野を広げ、長期透析アクセスの必要性を高めています。同時に、ヘルスケア支出の増加、透析センターの設立の増加、インフラ強化のための政府支援イニシアティブが、救命治療への幅広いアクセスを可能にしています。ヘルスケア機関は透析サービスへの投資を優先する一方、メーカーはより安全で効率的なカテーテル設計の革新を続けており、予測期間中の持続的成長を支えています。これらの要因に加え、診断プログラムの改善や腎臓の健康に関する啓発キャンペーンが、世界的な普及率の上昇を後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 9億9,090万米ドル |

| 予測金額 | 19億米ドル |

| CAGR | 6.6% |

2024年の短期血液透析カテーテルセグメントのシェアは63.7%で、急性腎障害や緊急時に迅速なバスキュラーアクセスを提供するカテーテルの重要な役割に支えられています。これらのカテーテルは、簡単に挿入でき、コスト効率が高く、すぐに透析を開始できるため、病院やクリティカルケア環境で広く利用されています。外科手術や敗血症、心血管合併症に伴う急性腎不全の発生率が上昇していることから、これらのカテーテルに対する需要は増加の一途をたどっています。

トンネル型カテーテル分野は、2024年に7億3,780万米ドルを生み出し、市場での優位性を確立しました。これらのカテーテルは、透析を継続する患者に信頼性の高い長期的なバスキュラーアクセスを提供するように設計されています。皮下トンネリングにより感染リスクを低減し、優れた安定性を提供する一方、非トンネリング製品に比べ耐久性が向上し、患者の快適性が高まるため、ヘルスケアプロバイダーの間で好まれています。

米国血液透析カテーテル2024年の市場規模は4億3,750万米ドルでした。治療要因としては、糖尿病、高血圧、肥満の急増に加え、早期診断・治療を促す啓発プログラムの改善が挙げられます。先進的な医療インフラ、透析センターの存在感、トンネル型や生体適合設計などの革新的なカテーテルの急速な採用により、同国は引き続き世界的な成長に大きく貢献しています。

血液透析カテーテル業界で活躍する主要企業には、Vygon、Amecath、Cook Medical、Polymed、Mozarc Medical、Delta Med、Teleflex、B. Braun、ST Stone Medical、Merit Medical、Medcomp、AngioDynamics、Becton, Dickinson and Company(BD)、Healthline Medical Products、Baxter、Bain Medical Equipmentなどがあります。市場ポジションを強化するため、血液透析カテーテル分野の企業は技術革新、地理的拡大、戦略的提携を優先しています。メーカー各社は、患者や臨床医のニーズの高まりに対応するため、生体適合性を高め、感染リスクを低減し、フロー性能を向上させた先進的なカテーテル設計に注力しています。ヘルスケアプロバイダーや透析センターとの戦略的提携は、長期供給契約を確保し、製品へのアクセスを改善するために進められています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 慢性腎臓疾患および末期腎疾患の有病率の上昇

- 慢性腎臓病の認知度向上のための促進活動

- 腎代替療法の増加

- 血液透析カテーテルにおける技術の進歩

- 世界の腎臓ドナー不足

- 業界の潜在的リスク&課題

- 腎臓関連疾患に関する認識の低さ

- 血液透析カテーテルに関連する合併症

- 市場機会

- 在宅透析および遠隔患者モニタリングソリューションの拡大

- 抗菌性および生体適合性カテーテル材料の採用増加

- ヘルスケアインフラの整備が進む新興市場における成長の可能性

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 現在の技術動向

- 長期使用のためのトンネル型カフ付きカテーテルへの移行

- 抗菌コーティングおよびヘパリンコーティングカテーテルの進歩

- 低侵襲カテーテル留置技術の採用増加

- 新興技術

- 感染と血栓症を最小限に抑える薬剤溶出カテーテルの開発

- 血流と凝固をリアルタイムで監視するセンサーを内蔵したスマートカテーテル

- 患者固有の解剖学的構造に合わせて設計された3Dプリントのカスタマイズされたカテーテル

- 現在の技術動向

- 将来の市場動向

- カテーテル依存を制限するために永久血管アクセスへの移行

- 在宅透析の利用増加が高度なカテーテルの需要を促進

- 遠隔カテーテルモニタリングのためのデジタルヘルスの統合

- 市場開拓戦略

- 価格分析

- GAP分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- グローバル

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ・中東・アフリカ

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:カテーテルの種類別、2021-2034

- 主要動向

- 短期的な血液透析カテーテル

- 長期的な血液透析カテーテル

第6章 市場推計・予測:製品別、2021-2034

- 主要動向

- トンネル型カテーテル

- カフ付きトンネルカテーテル

- カフなしトンネルカテーテル

- 非トンネル型カテーテル

第7章 市場推計・予測:材料別、2021-2034

- 主要動向

- ポリウレタン

- シリコーン

第8章 市場推計・予測:チップ構成別、2021-2034

- 主要動向

- ステップチップカテーテル

- スプリットチップカテーテル

- 対称カテーテル

- その他のチップ構成

第9章 市場推計・予測:ルーメン, 2021-2034

- 主要動向

- シングルルーメン

- ダブルルーメン

- トリプルルーメン

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Amecath

- AngioDynamics

- B. Braun

- Bain Medical Equipment

- Baxter

- Becton, Dickinson and Company(BD)

- Cook Medical

- Delta Med

- Healthline Medical Products

- Medcomp

- Merit Medical

- Mozarc Medical

- Polymed

- ST Stone Medical

- Teleflex

- Vygon