|

市場調査レポート

商品コード

1721517

電気自動車用バスバー市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測Electric Vehicle Busbar Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 電気自動車用バスバー市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月02日

発行: Global Market Insights Inc.

ページ情報: 英文 127 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

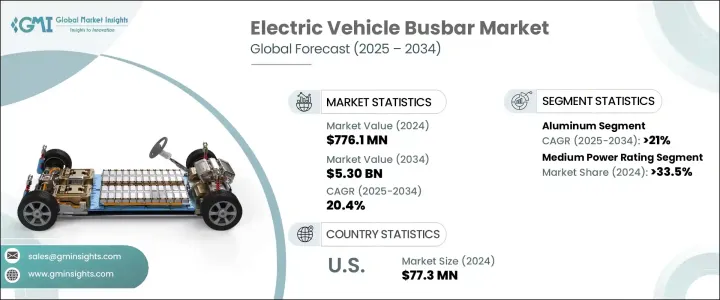

電気自動車用バスバーの世界市場規模は、2024年に7億7,610万米ドルとなり、CAGR 20.4%で成長し、2034年には53億米ドルに達すると予測されています。

電気自動車の急速な普及により、効率的な配電システムへの需要が高まっており、バスバーはこの移行における重要なコンポーネントとして浮上しています。自動車セクターが電動化へとシフトする中、バスバーは、合理的な電力伝達と最適なエネルギー効率を確保する能力から、EVバッテリー・システムに不可欠なものとなりつつあります。環境規制、燃費目標、カーボンニュートラルへのコミットメントに後押しされ、EVが世界的に勢いを増す中、自動車メーカーは高性能バスバーを必要とするより高度な電気システムを統合しつつあります。また、バッテリーアーキテクチャや車両設計の急速な技術進歩や、EV製造の規模拡大に向けた継続的な取り組みにより、市場の牽引力が高まっています。さらに、EVインフラ、特に急速充電ネットワークの拡大により、高電圧と極端な温度に耐える高度なバスバー・ソリューションの需要が引き続き高まっています。

EV充電ステーションの設置が世界的に増加していることが、電気自動車用バスバー市場の拡大に重要な役割を果たしています。これらの部品は、特に現在需要が高まっている超高速充電システムにおいて、高電圧送電を管理するために不可欠です。EVの普及が進むにつれて、高速で信頼性が高く効率的な充電セットアップへの要求も高まっており、エネルギー損失を最小限に抑えながら電流の流れを強化する堅牢なバスバー技術の必要性がさらに高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 7億7,610万米ドル |

| 予測金額 | 53億米ドル |

| CAGR | 20.4% |

市場は素材別に、主に銅とアルミニウムに区分されます。アルミ製バスバーは軽量でコスト面で有利なため、重量と価格が重要な小型EVモデルに最適であり、2034年までのCAGRは21%と予想されます。一方、銅バスバーはその優れた導電性と熱性能により、高級車や高性能のEVでは優位を保っています。このような特性から、銅は電力密度とエネルギー効率が最重要視される用途では不可欠な素材なのです。

市場セグメンテーションは定格電力で区分され、低、中、高のカテゴリーがあります。急速な加速、急速な充電、信頼性の高いエネルギー供給を必要とする電気スポーツカーや高級車の需要の高まりが原動力となっています。バッテリー設計の革新とプレミアムEVに対する消費者の関心の高まりにより、このセグメントは安定した成長を遂げる見通しです。

米国の電気自動車用バスバー市場は、2024年に7,730万米ドルを創出しました。この成長の主な要因はインフレ削減法(IRA)であり、バスバーなどの国産部品を使用した自動車に対する税制優遇措置を通じてEV需要を促進しています。この政策により、メーカーは米国内で製造された先進的で高効率のバスバーシステムに投資するようになり、世界のEVサプライチェーンにおける米国の役割はさらに高まっています。

世界のEVバスバー市場の主要プレーヤーには、シーメンス、シュナイダーエレクトリック、TEコネクティビティ、メルセンSA、インフィニオン・テクノロジーズAG、ルグラン、リテルヒューズ、アンフェノール・コーポレーション、三菱電機株式会社、Weidmuller Interface GmbH &Co.KG、EAE Group、EG Electronics、EMS Group、Rogers Corporationです。これらの企業は、次世代電気自動車に合わせた高性能バスバーシステムを提供するため、研究開発への投資、生産規模の拡大、戦略的パートナーシップの形成に積極的に取り組んでいます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的ダッシュボード

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:材料別、2021-2034

- 主要動向

- 銅

- アルミニウム

第6章 市場規模・予測:出力別、2021-2034

- 主要動向

- 低

- 中

- 高

第7章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ノルウェー

- ドイツ

- フランス

- オランダ

- 英国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- シンガポール

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- Amphenol Corporation

- Brar Elettromeccanica SpA

- EAE Group

- EG Electronics

- EMS Group

- Infineon Technologies AG

- Legrand

- Littelfuse、Inc.

- Mersen SA

- Mitsubishi Electric Corporation

- Rogers Corporation

- Schneider Electric

- Siemens

- TE Connectivity

- Weidmuller Interface GmbH &Co. KG

The Global Electric Vehicle Busbar Market was valued at USD 776.1 million in 2024 and is estimated to grow at a CAGR of 20.4% to reach USD 5.3 billion by 2034. The rapid acceleration in electric vehicle adoption is fueling a robust demand for efficient power distribution systems, and busbars are emerging as a critical component in this transition. As the automotive sector shifts toward electrification, busbars are becoming indispensable in EV battery systems for their ability to ensure streamlined power transfer and optimal energy efficiency. With EVs gaining momentum globally-driven by environmental regulations, fuel economy goals, and carbon neutrality commitments-automakers are integrating more advanced electrical systems that require high-performance busbars. The market is also witnessing increased traction due to rapid technological advancements in battery architecture and vehicle design, as well as ongoing efforts to scale EV manufacturing. Furthermore, the expansion of EV infrastructure, particularly in fast-charging networks, continues to boost demand for advanced busbar solutions that can withstand high voltage and extreme temperatures.

The rising installation of EV charging stations globally plays a key role in expanding the electric vehicle busbar market. These components are vital for managing high-voltage power transfers, especially in ultra-fast charging systems, which are now in high demand. As EV adoption grows, so does the requirement for fast, reliable, and efficient charging setups-further elevating the need for robust busbar technologies that enhance current flow while minimizing energy losses.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $776.1 Million |

| Forecast Value | $5.3 Billion |

| CAGR | 20.4% |

The market is segmented by material, primarily into copper and aluminum. Aluminum busbars are expected to witness a CAGR of 21% through 2034, owing to their lightweight nature and cost benefits, making them ideal for compact EV models where weight and affordability are critical. Meanwhile, copper busbars maintain dominance in luxury and high-performance EVs due to their superior conductivity and thermal performance. These attributes make copper an essential material in applications where power density and energy efficiency are paramount.

Segmented by power rating, the market includes low, medium, and high categories. The medium power rating segment held a 33.5% share in 2024, driven by rising demand for electric sports cars and high-end vehicles that require rapid acceleration, fast charging, and reliable energy delivery. With innovations in battery design and increasing consumer interest in premium EVs, this segment is poised to witness steady growth.

The U.S. Electric Vehicle Busbar Market generated USD 77.3 million in 2024. A key contributor to this growth is the Inflation Reduction Act (IRA), which has propelled EV demand through tax incentives for vehicles using domestically produced components like busbars. This policy is pushing manufacturers to invest in advanced, high-efficiency busbar systems made within the U.S., further enhancing the nation's role in the global EV supply chain.

Key players in the global EV busbar market include Siemens, Schneider Electric, TE Connectivity, Mersen SA, Infineon Technologies AG, Legrand, Littelfuse, Inc., Amphenol Corporation, Mitsubishi Electric Corporation, Weidmuller Interface GmbH & Co. KG, EAE Group, EG Electronics, EMS Group, and Rogers Corporation. These companies are heavily investing in R&D, scaling up production, and forming strategic partnerships to deliver high-performance busbar systems tailored to next-generation electric vehicles.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Material, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Copper

- 5.3 Aluminum

Chapter 6 Market Size and Forecast, By Power Rating, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Low

- 6.3 Medium

- 6.4 High

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Norway

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Netherlands

- 7.3.5 UK

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Singapore

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 Amphenol Corporation

- 8.2 Brar Elettromeccanica SpA

- 8.3 EAE Group

- 8.4 EG Electronics

- 8.5 EMS Group

- 8.6 Infineon Technologies AG

- 8.7 Legrand

- 8.8 Littelfuse, Inc.

- 8.9 Mersen SA

- 8.10 Mitsubishi Electric Corporation

- 8.11 Rogers Corporation

- 8.12 Schneider Electric

- 8.13 Siemens

- 8.14 TE Connectivity

- 8.15 Weidmuller Interface GmbH & Co. KG