|

市場調査レポート

商品コード

1740994

PVC電線管市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測PVC Electrical Conduit Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| PVC電線管市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月16日

発行: Global Market Insights Inc.

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

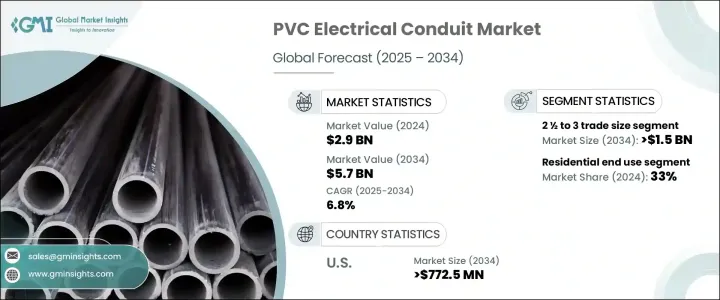

世界のPVC電線管市場は2024年に29億米ドルと評価され、CAGR 6.8%で成長し、2034年には57億米ドルに達すると推定されています。

より安全で耐久性に優れ、費用対効果の高い電気配線保護ソリューションへの需要が加速する中、PVC電線管は住宅、商業、工業の各分野で広く採用され続けています。軽量構造で耐食性に優れ、施工が容易なPVC電線管は、世界中の建設業者や建築業者の間で好まれています。現代の建設現場では、エネルギー効率、スマートビルディングの統合、持続可能性がますます優先されるようになっており、進化する安全基準と期待性能を満たすことができる信頼性の高い電線管ソリューションへの需要が高まっています。

急速な都市化、インフラ投資の増加、新興国での住宅プロジェクトの拡大が、市場の展望を再構築しています。主要地域の各国政府は、電力インフラのアップグレードと電力へのアクセス拡大に多額の投資を行っており、これが電線管使用の直接の推進力となっています。さらに、産業がオートメーションやスマートテクノロジーに移行する中、高性能でメンテナンスが容易な配線システムの必要性が重要になってきています。電線管材料、製造自動化、環境に優しい製品イノベーションの技術的進歩により、PVC電線管は将来対応可能な建築プロジェクトに不可欠な要素として位置付けられています。しかし、業界は、原料価格の変動やPVCベース製品の環境への影響に対する監視の高まりといった課題を克服し続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 29億米ドル |

| 予測金額 | 57億米ドル |

| CAGR | 6.8% |

継続的な都市開発と人口増加が、特に新興地域におけるスマートホームとアップグレードされた電気システムへの需要増加に拍車をかけています。同市場はまた、進化する製造技術や、アクセシビリティとリーチを向上させる流通網の強化からも恩恵を受けています。原材料コストの変動や環境問題をめぐる懸念はあるもの、インフラ整備や電化プロジェクトに重点を置いた政府の積極的な取り組みは、強力な成長触媒になると期待されています。

21/2インチから3インチの間の取引サイズカテゴリーが支配的なセグメントとして台頭しており、2034年までに15億米ドルに達すると予測されています。これらの電線管サイズは、商業用や工業用設備に理想的で、扱いやすさと設置効率を維持しながら、大容量の電線を通すための十分なスペースを提供します。大規模な回路システムや高度な電気ネットワークを必要とするプロジェクトでの採用が増加しており、その重要性が高まっています。

最終用途別では、2024年に住宅セクターのシェアが33%を占め、2034年までCAGR 7%で成長すると予測されています。スマート住宅に対する需要の増加、急速な都市化、集合住宅プロジェクトの急増が、この成長を促進する主な要因です。建設業者は、その手頃な価格、柔軟性、グリーンビルディング基準への適合性からPVCコンジットを支持しています。また、商業部門も依然として主要な消費者であり、製品の安全性、信頼性、低メンテナンス性に信頼を寄せています。

米国のPVC電線管市場は、2024年には4億3,560万米ドルと評価され、2034年には7億7,250万米ドルに達すると予測されています。再生可能エネルギー導入の増加と、商業ビルと住宅の両方におけるスマートシステムの統合が、引き続き需要を牽引しています。環境問題は市場力学に影響を与えるが、PVC導管の長持ちする性能と最新のエネルギーシステムとの適合性は、その支配的地位を確保しています。

ABB、Anamet Electrical、CANTEX、Schneider Electric、Legrand、Atkore、HellermannTyton、Astral、Bahra Electric、Vinidex、Electri-Flex、Wienerberger、Sundeep Electricals、Hubbell、Toyo Industry Lao Factory、Iplex Pipelines、Guangdong Ctube Industry、Champion Fiberglassなどの企業は、柔軟で環境に配慮した設計の製品ポートフォリオを積極的に拡大しています。これらの企業は、主要地域の流通チャネルを強化し、製造の自動化に投資し、建設会社と戦略的パートナーシップを結んでいます。進化する建築基準法に合わせて技術のアップグレードを取り入れることは、市場で競争力を維持するための重要な戦略であり続けています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 戦略的ダッシュボード

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:取引規模別、2021-2034

- 主要動向

- ½から1

- 1 ¼から2

- 2 ½~3

- 3~4

- 5~6

- その他

第6章 市場規模・予測:最終用途別、2021-2034

- 主要動向

- 住宅用

- 商業用

- 産業

- ユーティリティ

第7章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- フランス

- ドイツ

- イタリア

- 英国

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- ABB

- Anamet Electrical

- ASTRAL

- Atkore

- Bahra Electric

- CANTEX

- Champion Fiberglass

- Electri-Flex

- Guangdong Ctube Industry

- HellermannTyton

- Hubbell

- Iplex Pipelines

- Legrand

- Schneider Electric

- Sundeep Electricals

- Toyo Industry Lao Factory

- Vinidex

- Wienerberger

The Global PVC Electrical Conduit Market was valued at USD 2.9 billion in 2024 and is estimated to grow at a CAGR of 6.8% to reach USD 5.7 billion by 2034. As the demand for safer, more durable, and cost-effective solutions for electrical wiring protection accelerates, PVC electrical conduits continue to gain widespread adoption across residential, commercial, and industrial sectors. Their lightweight construction, superior corrosion resistance, and ease of installation make them a preferred choice among contractors and builders worldwide. Modern construction practices increasingly prioritize energy efficiency, smart building integration, and sustainability, driving the demand for reliable conduit solutions that can meet evolving safety standards and performance expectations.

Rapid urbanization, rising infrastructure investments, and expanding residential projects in emerging economies are reshaping the market landscape. Governments across major regions are heavily investing in upgrading power infrastructure and expanding access to electricity, which directly propels conduit usage. Moreover, with industries moving toward automation and smart technologies, the need for high-performance, easily maintainable wiring systems is becoming critical. Technological advancements in conduit materials, manufacturing automation, and eco-friendly product innovations are positioning PVC conduits as an indispensable element in future-ready building projects. However, the industry continues to navigate challenges such as raw material price volatility and increasing scrutiny over the environmental impact of PVC-based products.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.9 Billion |

| Forecast Value | $5.7 Billion |

| CAGR | 6.8% |

Continued urban development and population growth are fueling higher demand for smart homes and upgraded electrical systems, especially in emerging regions. The market also benefits from evolving manufacturing technologies and stronger distribution networks that enhance accessibility and reach. Despite concerns surrounding fluctuating raw material costs and environmental issues, proactive governmental initiatives focused on infrastructure development and electrification projects are expected to be strong growth catalysts.

The trade size category between 21/2 and 3 inches is emerging as a dominant segment, forecasted to reach USD 1.5 billion by 2034. These conduit sizes are ideal for commercial and industrial installations, offering ample space for high-capacity wire runs while maintaining ease of handling and installation efficiency. Their rising adoption across projects requiring extensive circuit systems and advanced electrical networks highlights their growing importance.

Based on end use, the residential sector accounted for a 33% share in 2024 and is projected to grow at a CAGR of 7% through 2034. Increasing demand for smart housing, rapid urbanization, and a surge in multi-unit residential projects are major factors driving this growth. Builders are favoring PVC conduits for their affordability, flexibility, and compliance with green building standards. The commercial sector also remains a major consumer, relying on the product's safety, reliability, and low-maintenance characteristics.

The United States PVC Electrical Conduit Market was valued at USD 435.6 million in 2024 and is expected to reach USD 772.5 million by 2034. Rising renewable energy installations and the integration of smart systems in both commercial and residential buildings continue to drive demand. Although environmental concerns influence market dynamics, the long-lasting performance and compatibility of PVC conduits with modern energy systems secure their dominant position.

Companies like ABB, Anamet Electrical, CANTEX, Schneider Electric, Legrand, Atkore, HellermannTyton, Astral, Bahra Electric, Vinidex, Electri-Flex, Wienerberger, Sundeep Electricals, Hubbell, Toyo Industry Lao Factory, Iplex Pipelines, Guangdong Ctube Industry, and Champion Fiberglass are actively expanding their product portfolios with flexible and eco-conscious designs. They are strengthening distribution channels across key regions, investing in manufacturing automation, and forging strategic partnerships with construction firms. Embracing technology upgrades to align with evolving building codes continues to be a critical strategy for maintaining a competitive edge in the market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Trade Size, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 ½ to 1

- 5.3 1 ¼ to 2

- 5.4 2 ½ to 3

- 5.5 3 to 4

- 5.6 5 to 6

- 5.7 Others

Chapter 6 Market Size and Forecast, By End Use, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

- 6.4 Industrial

- 6.5 Utility

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 France

- 7.3.2 Germany

- 7.3.3 Italy

- 7.3.4 UK

- 7.3.5 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Anamet Electrical

- 8.3 ASTRAL

- 8.4 Atkore

- 8.5 Bahra Electric

- 8.6 CANTEX

- 8.7 Champion Fiberglass

- 8.8 Electri-Flex

- 8.9 Guangdong Ctube Industry

- 8.10 HellermannTyton

- 8.11 Hubbell

- 8.12 Iplex Pipelines

- 8.13 Legrand

- 8.14 Schneider Electric

- 8.15 Sundeep Electricals

- 8.16 Toyo Industry Lao Factory

- 8.17 Vinidex

- 8.18 Wienerberger