|

市場調査レポート

商品コード

1666657

ソーラーケーブル市場の機会、成長促進要因、産業動向分析、2025~2034年の予測Solar Cable Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ソーラーケーブル市場の機会、成長促進要因、産業動向分析、2025~2034年の予測 |

|

出版日: 2024年12月26日

発行: Global Market Insights Inc.

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

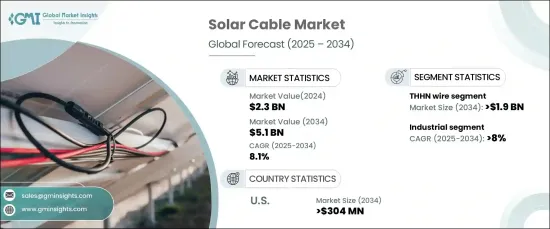

世界のソーラーケーブル市場は、2024年に23億米ドルと評価され、世界の太陽エネルギープロジェクトの急速な拡大に牽引され、2025年から2034年にかけて8.1%のCAGRで堅調に成長する見通しです。

再生可能エネルギーへの投資は、政府の奨励策、持続可能性の義務付け、ネットゼロ排出の追求の高まりを受けて急増しています。ソーラーケーブルは、住宅、商業施設、公共施設規模の太陽光発電設備を接続し、電力を伝送する上で極めて重要な役割を担っており、再生可能エネルギーのインフラにとって不可欠なものとなっています。

技術の進歩により、ソーラーケーブルの効率、耐久性、安全性が大幅に向上しています。耐紫外線性、温度耐性、寿命の向上などの技術革新により、過酷な環境条件下でも最適な性能を発揮します。この技術的進歩は、太陽エネルギー・システムとエネルギー貯蔵ソリューションやスマート・グリッドとの統合が進んでいることと一致しており、より持続可能で信頼性の高いエネルギー・エコシステムへの道を開いています。同市場はまた、再生可能エネルギー目標に対する世界のコミットメントの高まりや、太陽光発電(PV)システムのコスト低下にも後押しされており、アクセシビリティと採用の拡大が続いています。中国とインドにおける大規模な太陽光発電開発のおかげでアジア太平洋地域がこの急成長をリードしているが、北米と欧州も、支持的な政策枠組みと財政的インセンティブに後押しされ、着実な成長を遂げています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 23億米ドル |

| 予測金額 | 51億米ドル |

| CAGR | 8.1% |

THHNワイヤセグメントは、その優れた耐久性、汎用性、費用対効果により、2034年までに19億米ドルを超える見通しです。熱可塑性高耐熱ナイロン被覆(THHN)ワイヤは、その強固な絶縁特性で知られており、電力損失を低減しながら効率的なエネルギートランスミッションを保証します。耐熱性、耐湿性、耐摩耗性に優れているため、屋内外の太陽光発電アプリケーションに最適です。太陽光発電システムの導入が住宅、商業施設、公益事業規模で拡大するにつれて、信頼性が高く高性能なTHHNワイヤーへの需要が増え続けています。

産業分野では、持続可能性目標の達成と運用コストの最小化を目的とした太陽エネルギーの急速な導入に後押しされ、ソーラーケーブル市場は2034年までCAGR 8%を超える成長が予測されています。企業が電気料金の上昇を相殺し、政府の優遇策を活用しようとしているため、大規模な産業用太陽光発電の設置がますます一般的になっています。こうした設置には、一貫したエネルギー・トランスミッションとシステムの信頼性を確保するため、耐久性のあるソーラーケーブルを含む堅牢なインフラが必要です。太陽エネルギーを活用した製造・建設プロセスの強化が、効率的なケーブル・ソリューションの必要性をさらに高めています。

米国のソーラーケーブル市場は、住宅、商業施設、公共施設規模のプロジェクトでソーラーエネルギーシステムの採用が増加していることから、2034年までに3億400万米ドルを超えると予想されています。投資税額控除(ITC)や州レベルの優遇措置といった連邦政府の取り組みが普及に拍車をかけている一方、2050年までに排出量をゼロにするといった野心的な再生可能エネルギー目標が、ソーラーインフラへの継続的な投資に拍車をかけています。高品質のソーラーケーブルは、これらの目標を達成するために不可欠であり、高度な太陽エネルギーシステムの効率的で信頼性の高い運用を保証します。

目次

第1章 調査手法と調査範囲

- 市場の定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 2次データ

- 有償

- 公的

第2章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

第3章 競合情勢

- 戦略ダッシュボード

- イノベーションと持続可能性の展望

第4章 市場規模・予測:タイプ別、2021年~2034年

- 主要動向

- PWワイヤー

- USE-2ワイヤー

- THHNワイヤー

第5章 市場規模・予測:最終用途別、2021年~2034年

- 主要動向

- 住宅用

- 商業用

- 産業用

第6章 市場規模・予測:電流別、2021年~2034年

- 主要動向

- 交流

- 直流

第7章 市場規模・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- アジア太平洋

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- Alpha Wire

- Allied Wire and Cable

- Belden

- Fujikura

- Furukawa Electric

- General Cable

- Havells

- Helukabel

- Hellenic Group

- Kabelwerk Eupen

- KEI Industries

- Lapp Group

- Leoni

- LS Cable and System

- Nexans

- Northwire

- Polycab

- Prysmian Group

- RR Kabel

- Southwire Company

- TE Connectivity

The Global Solar Cable Market, valued at USD 2.3 billion in 2024, is poised to grow at a robust CAGR of 8.1% from 2025 to 2034, driven by the rapid expansion of solar energy projects worldwide. Investments in renewable energy have surged in response to escalating government incentives, sustainability mandates, and the pursuit of net-zero emissions. Solar cables play a pivotal role in connecting and transmitting power across residential, commercial, and utility-scale solar installations, making them indispensable to the renewable energy infrastructure.

Technological advancements are significantly enhancing the efficiency, durability, and safety of solar cables. Innovations such as improved UV resistance, temperature tolerance, and enhanced lifespan ensure optimal performance under harsh environmental conditions. This technological progress aligns with the increasing integration of solar energy systems with energy storage solutions and smart grids, paving the way for a more sustainable and reliable energy ecosystem. The market is also buoyed by a growing global commitment to renewable energy targets and the declining cost of solar photovoltaic (PV) systems, which continue to expand accessibility and adoption. While the Asia Pacific region leads this surge, thanks to large-scale solar developments in China and India, North America and Europe are also experiencing steady growth, driven by supportive policy frameworks and financial incentives.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.3 Billion |

| Forecast Value | $5.1 Billion |

| CAGR | 8.1% |

The THHN wire segment is poised to exceed USD 1.9 billion by 2034 due to its exceptional durability, versatility, and cost-effectiveness. Thermoplastic High Heat-Resistant Nylon-coated (THHN) wires are renowned for their robust insulation properties, which ensure efficient energy transmission while reducing power losses. Their superior resistance to heat, moisture, and abrasion makes them ideal for both indoor and outdoor solar applications. As the deployment of solar PV systems expands across residential, commercial, and utility-scale projects, the demand for reliable and high-performance THHN wires continues to rise.

In the industrial sector, the solar cable market is projected to grow at a CAGR exceeding 8% through 2034, fueled by the rapid adoption of solar energy to achieve sustainability goals and minimize operational expenses. Large-scale industrial solar installations are becoming increasingly common as businesses seek to offset rising electricity costs and capitalize on government incentives. These installations require robust infrastructure, including durable solar cables, to ensure consistent energy transmission and system reliability. Enhanced manufacturing and construction processes leveraging solar energy further drive the need for efficient cable solutions.

The U.S. solar cable market is expected to surpass USD 304 million by 2034, driven by the growing adoption of solar energy systems across residential, commercial, and utility-scale projects. Federal initiatives such as the Investment Tax Credit (ITC) and state-level incentives are spurring widespread installations, while ambitious renewable energy targets, including net-zero emissions by 2050, fuel ongoing investments in solar infrastructure. High-quality solar cables are integral to achieving these goals, ensuring the efficient and reliable operation of advanced solar energy systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Industry Insights

- 2.1 Industry ecosystem analysis

- 2.2 Regulatory landscape

- 2.3 Industry impact forces

- 2.3.1 Growth drivers

- 2.3.2 Industry pitfalls & challenges

- 2.4 Growth potential analysis

- 2.5 Porter's analysis

- 2.5.1 Bargaining power of suppliers

- 2.5.2 Bargaining power of buyers

- 2.5.3 Threat of new entrants

- 2.5.4 Threat of substitutes

- 2.6 PESTEL analysis

Chapter 3 Competitive landscape, 2024

- 3.1 Strategic dashboard

- 3.2 Innovation & sustainability landscape

Chapter 4 Market Size and Forecast, By Type, 2021 – 2034 (USD Million, ‘000 Tonnes)

- 4.1 Key trends

- 4.2 PW wire

- 4.3 USE-2 wire

- 4.4 THHN wire

Chapter 5 Market Size and Forecast, By End Use, 2021 – 2034 (USD Million, ‘000 Tonnes)

- 5.1 Key trends

- 5.2 Residential

- 5.3 Commercial

- 5.4 Industrial

Chapter 6 Market Size and Forecast, By Current, 2021 – 2034 (USD Million, ‘000 Tonnes)

- 6.1 Key trends

- 6.2 AC

- 6.3 DC

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (USD Million, ‘000 Tonnes)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 France

- 7.3.3 Germany

- 7.3.4 Italy

- 7.3.5 Russia

- 7.3.6 Spain

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Turkey

- 7.5.4 South Africa

- 7.5.5 Egypt

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 Alpha Wire

- 8.2 Allied Wire and Cable

- 8.3 Belden

- 8.4 Fujikura

- 8.5 Furukawa Electric

- 8.6 General Cable

- 8.7 Havells

- 8.8 Helukabel

- 8.9 Hellenic Group

- 8.10 Kabelwerk Eupen

- 8.11 KEI Industries

- 8.12 Lapp Group

- 8.13 Leoni

- 8.14 LS Cable and System

- 8.15 Nexans

- 8.16 Northwire

- 8.17 Polycab

- 8.18 Prysmian Group

- 8.19 RR Kabel

- 8.20 Southwire Company

- 8.21 TE Connectivity