|

市場調査レポート

商品コード

1913381

産業用3Dプリンター市場:市場機会、成長促進要因、産業動向分析、将来予測(2026~2035年)Industrial 3D Printer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 産業用3Dプリンター市場:市場機会、成長促進要因、産業動向分析、将来予測(2026~2035年) |

|

出版日: 2025年12月17日

発行: Global Market Insights Inc.

ページ情報: 英文 250 Pages

納期: 2~3営業日

|

概要

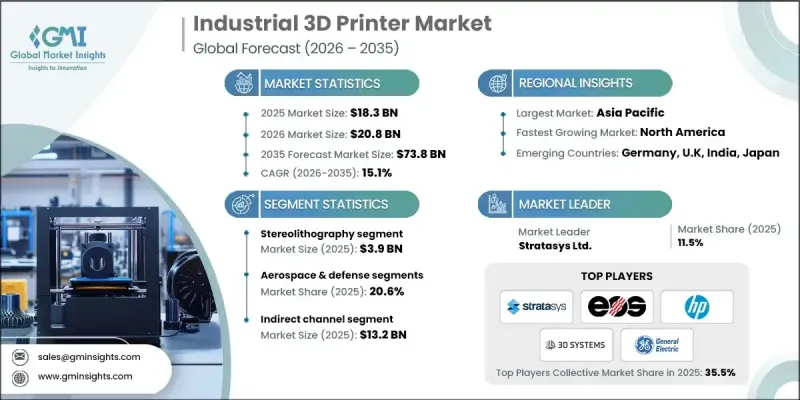

世界の産業用3Dプリンター市場は、2025年に183億米ドルと評価され、2035年までにCAGR 15.1%で成長し、738億米ドルに達すると予測されています。

コスト効率性は市場成長を牽引する主要因であり、製造業者は金型コストを最大80~90%削減可能で、特定の用途では少量生産時でも部品当たり10万米ドル以上の節約につながります。本市場は、高度にカスタマイズされた幾何学的に複雑な部品を製造できる3Dプリント技術から恩恵を受けています。医療分野では、患者特異的なインプラントを提供し、回復成果の向上に貢献しています。材料効率と持続可能性も重要な役割を果たしており、3Dプリンティングは用途に応じて廃棄物を30~95%削減します。金属積層造形やマルチマテリアル印刷などの技術革新は、新たな産業使用事例を可能にすることで市場をさらに拡大しています。政府のイニシアチブや資金援助プログラムは、特に精密性や高度な材料性能を必要とする使用事例において、調査と導入を支援しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026~2035年 |

| 当初の市場規模 | 183億米ドル |

| 市場規模予測 | 738億米ドル |

| CAGR | 15.1% |

ステレオリソグラフィー(SLA)は2025年に39億米ドルの市場規模を生み出しました。SLAは極めて精密な複雑なプロトタイプや機能部品の製造を可能とし、複雑な設計を必要とする産業に最適です。政府の資金援助や施策により産業分野での採用が進み、特殊なSLA樹脂や特定用途における技術革新が促進されています。

航空宇宙・防衛分野は2025年に20.6%のシェアを占めました。軽量化、燃料効率、幾何学的に高度な部品への需要が背景にあります。積層造形技術は、従来技術では実現不可能な格子構造やコンフォーマル冷却チャネルの製造を可能とし、航空宇宙・防衛分野を産業用3Dプリンティングの主要導入分野として確固たる地位に押し上げています。

米国の産業用3Dプリンター市場は2025年に78.1%のシェアを占めました。この成長は、強固な製造基盤と先進技術の急速な導入によって支えられています。ストラタシスや3Dシステムズといった主要企業は、航空宇宙や医療など高精度分野の需要に応えるため製品ラインを拡充し、主要メーカーとの連携により3D生産ラインの規模拡大を推進することで、米国市場の成長を牽引しています。

よくあるご質問

目次

第1章 分析手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界のエコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- ラピッドプロトタイピングの広範な活用

- 製品開発とサプライチェーンの改善

- 3Dプリンティングプロジェクトへの政府投資

- 業界の潜在的リスクと課題

- 材料の制約と品質管理

- 3Dプリント技術による設計の複製し易さ

- 市場機会

- 医療分野およびバイオプリンティングへの展開

- 持続可能性と規制順守ソリューション

- 促進要因

- 成長可能性分析

- 将来の市場動向

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 技術別

- 地域別

- 規制情勢

- 規格およびコンプライアンス要件

- 地域別規制枠組み

- 認証基準

- ギャップ分析

- リスク評価と軽減策

- ポーターのファイブフォース分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業別の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要企業の競合分析

- 競合ポジショニング・マトリックス

- 主な動向

- 企業合併・買収 (M&A)

- 事業提携・協力

- 新製品の発売

- 拡大計画

第5章 市場の推定・予測:技術別(2022~2035年)

- 選択的レーザー焼結法

- ステレオリソグラフィー

- 溶融積層法

- 直接金属レーザー焼結

- インクジェット印刷

- ポリジェット印刷

- 電子ビーム溶解

- 積層物体製造

- デジタル光処理技術

- レーザー金属積層法

- その他

第6章 市場の推定・予測:エンドユーザー別(2022~2035年)

- 自動車

- 航空宇宙・防衛

- 医療

- 民生用電子機器

- 食品・料理

- 電力・エネルギー

- その他

第7章 市場の推定・予測:流通チャネル別(2022~2035年)

- 直接

- 間接

第8章 市場の推定・予測:地域別(2022~2035年)

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- 3D Systems

- Desktop Metal

- EOS

- Formlabs

- General Electric

- HP

- Markforged

- Materialise

- Nano Dimension

- Prodways

- Renishaw

- SLM Solutions

- Stratasys

- Ultimaker

- Velo3D