|

|

市場調査レポート

商品コード

1441999

デジタルアイソレータ市場:技術別、絶縁材料別、データレート別、最終用途産業別 2024年~2032年予測Digital Isolator Market - By Technology (Magnetic Coupling, Capacitive Coupling, Optical Isolation (Optocouplers), Giant Magnetoresistance (GMR)), By Insulating Material, By Data Rate, By End-Use Industry, Forecast 2024 - 2032 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| デジタルアイソレータ市場:技術別、絶縁材料別、データレート別、最終用途産業別 2024年~2032年予測 |

|

出版日: 2024年01月19日

発行: Global Market Insights Inc.

ページ情報: 英文 200 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

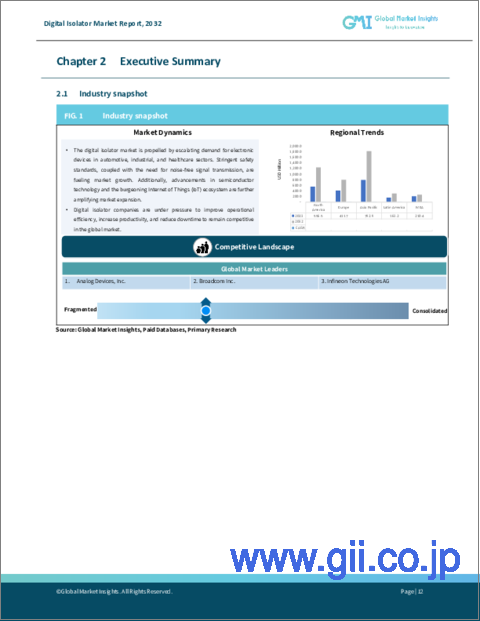

デジタルアイソレータ産業は、継続的な技術の進歩により、2024年から2032年にかけて約8%のCAGRを記録すると予測されています。

産業のデジタル化と自動化が進むにつれ、信頼性が高く高性能な絶縁ソリューションへの需要が高まっています。2023年5月、Toshiba Electronic Devices & Storage Corporationは、100kV/μs(min)の高いコモンモード過渡耐性(CMTI)と150Mbpsの高速データレートを備えた高速2次チャネルであるデジタルアイソレータ「DCL54xx01シリーズ」を発売しました。

さらに、さまざまな用途で電気安全が重視されるようになっています。電気的危険に関連するリスクに対する認識が高まる中、産業界は、繊細な電子部品を保護し、作業員の安全を確保するために、堅牢な絶縁ソリューションの導入を優先しています。デジタルアイソレータは優れた絶縁性能を発揮し、電圧サージ、グラウンド・ループ、電磁干渉を効果的に防止することで、機器とオペレータの両方を保護します。

デジタルアイソレータ産業は、技術、絶縁材料、データ・レート、最終用途、地域によって区分されます。

巨大磁気抵抗分野は、効率と信頼性を向上させた高性能な絶縁ソリューションを提供できることから、予測期間中に顕著な成長を遂げると思われます。GMRベースのアイソレータは、革新的な磁気センシング技術を利用して優れた絶縁性能を実現し、光絶縁や静電容量絶縁といった従来の方法を凌駕します。コンパクトなサイズ、低消費電力、高速データ伝送能力により、これらのアイソレータは車載電子機器、産業オートメーション、医療機器など幅広い用途に適しています。

二酸化ケイ素セグメントは、卓越した性能特性を持つ高度な絶縁材料であるため、2024年から2032年にかけて大きなCAGRが見込まれます。集積回路や半導体デバイスの製造における主要部品として、SiO2は優れた電気絶縁特性を提供し、電子部品間の信頼性の高い絶縁を保証します。さらに、プラズマエンハンスト化学気相成長法(PECVD)や原子層堆積法(ALD)などのSiO2堆積技術の進歩により、絶縁層の厚さと均一性を正確に制御できるようになり、デジタルアイソレータの信頼性と性能が向上しています。

北米のデジタルアイソレータ産業は、2024年から2032年にかけて目覚ましい成長動向を示すと思われます。同地域の堅調な半導体産業と技術革新エコシステムは、先進的なデジタルアイソレータ技術の開発を促進しています。さらに、電気自動車、再生可能エネルギーシステム、IoTデバイスなどの新興用途でデジタルアイソレータの採用が増加していることも、この地域の市場成長をさらに加速させています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 デジタルアイソレーター業界考察

- エコシステム分析

- ベンダーマトリックス

- 利益率分析

- 技術とイノベーションの展望

- 特許分析

- 主要ニュースとイニシアチブ

- パートナーシップ/コラボレーション

- 合併/買収

- 投資

- 製品上市とイノベーション

- 規制状況

- 影響要因

- 促進要因

- ノイズのない信号伝送へのニーズの高まり

- モノのインターネット(IoT)用途の台頭

- カーエレクトロニクスへの普及

- 堅牢な高電圧絶縁に対する需要の高まり

- ヘルスケア・用途における需要の高まり

- 業界の潜在的リスク&課題

- 電力転送能力の制限

- データレートの制限

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 各社の市場シェア

- 主要市場企業の競合分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 デジタルアイソレータ市場推計・予測:技術別 2018年~2032年

- 主要動向

- 磁気カップリング

- 容量性カップリング

- 光絶縁(オプトカプラ)

- 巨大磁気抵抗(GMR)

- その他

第6章 デジタルアイソレータ市場推計・予測:絶縁材料別 2018年~2032年

- 主要動向

- 二酸化ケイ素(SiO2)

- ポリマー系絶縁材料

- その他

第7章 デジタルアイソレータ市場推定・予測:データレート別 2018年~2032年

- 主要動向

- 25Mbps未満

- 25-75 Mbps

- 25Mbps以上

第8章 デジタルアイソレータ市場推計・予測:チャネル別 2018年~2032年

- 主要動向

- 2チャンネル

- 4チャンネル

- 6チャンネル

- 8チャンネル

- その他

第9章 デジタルアイソレータ市場推計・予測:最終用途産業別 2018年~2032年

- 主要動向

- 製造業およびプロセス制御

- 自動車

- ヘルスケア

- 通信

- 家電

- エネルギーおよび公益事業

- 航空宇宙・防衛

- データセンターとIT

第10章 デジタルアイソレータ市場推計・予測:地域別 2018~2032年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ANZ

- シンガポール

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- UAE

- 南アフリカ

- その他のMEA

第11章 企業プロファイル

- Analog Devices, Inc.

- Broadcom Inc.

- Infineon Technologies AG

- Maxim Integrated Products, Inc.

- Murata Manufacturing Co., Ltd.

- NXP Semiconductors

- ON Semiconductor

- Power Integrations

- Renesas Electronics Corporation

- ROHM Semiconductor

- Silicon Labs

- STMicroelectronics

- Texas Instruments, Inc.

- Toshiba Corporation

- Vicor Corporation

Digital Isolator Industry is projected to witness around 8% CAGR from 2024 to 2032, driven by continuous advancements in technology. As industries increasingly shift to digitalization and automation, the demand for reliable and high-performance isolation solutions escalates. In May 2023, Toshiba Electronic Devices & Storage Corporation launched high-speed quadratic-channel digital isolators, known as the "DCL54xx01 Series," which presented 100kV/μs (min) of high common mode transient immunity (CMTI) and a 150Mbps high-speed data rate.

Additionally, there is a growing emphasis on electrical safety in various applications. With the rising awareness of the risks associated with electrical hazards, industries are prioritizing the implementation of robust isolation solutions to protect sensitive electronic components and ensure personnel safety. Digital isolators offer superior isolation performance, effectively preventing voltage surges, ground loops, and electromagnetic interference, thus safeguarding both equipment and operators.

Digital isolator industry is divided on the basis of technology, insulating material, data rate, end use, and region.

Giant magnetoresistance segment is set to witness notable growth in the forecast period, favored by the ability to offer high-performance isolation solutions with enhanced efficiency and reliability. GMR-based isolators utilize innovative magnetic sensing technology to achieve superior isolation performance, surpassing traditional methods such as optical and capacitive isolation. With their compact size, low power consumption, and high-speed data transmission capabilities, these isolators are well-suited for a wide range of applications, including automotive electronics, industrial automation, and medical devices.

Silicon dioxide segment is anticipated to observe a significant CAGR during 2024 and 2032, as it is an advanced insulation material with exceptional performance characteristics. As a key component in the manufacturing of integrated circuits and semiconductor devices, SiO2 provides excellent electrical insulation properties, ensuring reliable isolation between electronic components. Additionally, advancements in SiO2 deposition techniques, such as plasma-enhanced chemical vapor deposition (PECVD) and atomic layer deposition (ALD), enable precise control over insulation layer thickness and uniformity, enhancing the reliability and performance of digital isolators.

North America digital isolator industry will showcase impressive growth trends over 2024-2032, attributed to stringent regulatory standards and industry certifications regarding electrical safety. The region's robust semiconductor industry and technological innovation ecosystem foster the development of advanced digital isolator technologies. Additionally, the increasing adoption of digital isolators in emerging applications such as electric vehicles, renewable energy systems, and IoT devices further accelerates regional market growth. Digital Isolator Industry is projected to witness around 8% CAGR from 2024 to 2032, driven by continuous advancements in technology. As industries increasingly shift to digitalization and automation, the demand for reliable and high-performance isolation solutions escalates. In May 2023, Toshiba Electronic Devices & Storage Corporation launched high-speed quadratic-channel digital isolators, known as the "DCL54xx01 Series," which presented 100kV/μs (min) of high common mode transient immunity (CMTI) and a 150Mbps high-speed data rate.

Additionally, there is a growing emphasis on electrical safety in various applications. With the rising awareness of the risks associated with electrical hazards, industries are prioritizing the implementation of robust isolation solutions to protect sensitive electronic components and ensure personnel safety. Digital isolators offer superior isolation performance, effectively preventing voltage surges, ground loops, and electromagnetic interference, thus safeguarding both equipment and operators.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Digital isolator market 360 degree synopsis, 2018 - 2032

Chapter 3 Digital Isolator Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Vendor matrix

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news and initiatives

- 3.6.1 Partnership/Collaboration

- 3.6.2 Merger/Acquisition

- 3.6.3 Investment

- 3.6.4 Product launch & innovation

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Growing need for noise-free signal transmission

- 3.8.1.2 Emerging internet of things (IoT) applications

- 3.8.1.3 Increased penetration in automotive electronics

- 3.8.1.4 Rising demand for robust high-voltage isolation

- 3.8.1.5 Growing demand in healthcare applications

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Limited power transfer capability

- 3.8.2.2 Data rate limitations

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.10.1 Supplier power

- 3.10.2 Buyer power

- 3.10.3 Threat of new entrants

- 3.10.4 Threat of substitutes

- 3.10.5 Industry rivalry

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

Chapter 5 Digital Isolator Market Estimates & Forecast, By Technology 2018 - 2032 (USD Million)

- 5.1 Key trends

- 5.2 Magnetic coupling

- 5.3 Capacitive coupling

- 5.4 Optical isolation (Optocouplers)

- 5.5 Giant magnetoresistance (GMR)

- 5.6 Others

Chapter 6 Digital Isolator Market Estimates & Forecast, By Insulating Material 2018 - 2032 (USD Million)

- 6.1 Key trends

- 6.2 Silicon dioxide (SiO2)

- 6.3 Polymer-based insulators

- 6.4 Others

Chapter 7 Digital Isolator Market Estimates & Forecast, By Data Rate 2018 - 2032 (USD Milion)

- 7.1 Key trends

- 7.2 Below 25 Mbps

- 7.3 25 - 75 Mbps

- 7.4 Above 25 Mbps

Chapter 8 Digital Isolator Market Estimates & Forecast, By Channel 2018 - 2032 (USD Million)

- 8.1 Key trends

- 8.2 2-Channel

- 8.3 4-Channel

- 8.4 6-Channel

- 8.5 8-Channel

- 8.6 Others

Chapter 9 Digital Isolator Market Estimates & Forecast, By End-Use Industry 2018 - 2032 (USD Million)

- 9.1 Key trends

- 9.2 Manufacturing and process control

- 9.3 Automotive

- 9.4 Healthcare

- 9.5 Telecommunications

- 9.6 Consumer electronics

- 9.7 Energy and utilities

- 9.8 Aerospace and defense

- 9.9 Data centers and IT

Chapter 10 Digital Isolator Market Estimates & Forecast, By Region 2018 - 2032 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Singapore

- 10.4.7 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Rest of Latin America

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

- 10.6.4 Rest of MEA

Chapter 11 Company Profiles

- 11.1 Analog Devices, Inc.

- 11.2 Broadcom Inc.

- 11.3 Infineon Technologies AG

- 11.4 Maxim Integrated Products, Inc.

- 11.5 Murata Manufacturing Co., Ltd.

- 11.6 NXP Semiconductors

- 11.7 ON Semiconductor

- 11.8 Power Integrations

- 11.9 Renesas Electronics Corporation

- 11.10 ROHM Semiconductor

- 11.11 Silicon Labs

- 11.12 STMicroelectronics

- 11.13 Texas Instruments, Inc.

- 11.14 Toshiba Corporation

- 11.15 Vicor Corporation