|

市場調査レポート

商品コード

1766329

電力・蒸気発生廃熱回収システムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Electricity and Steam Generation Waste Heat Recovery Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 電力・蒸気発生廃熱回収システムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月10日

発行: Global Market Insights Inc.

ページ情報: 英文 138 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

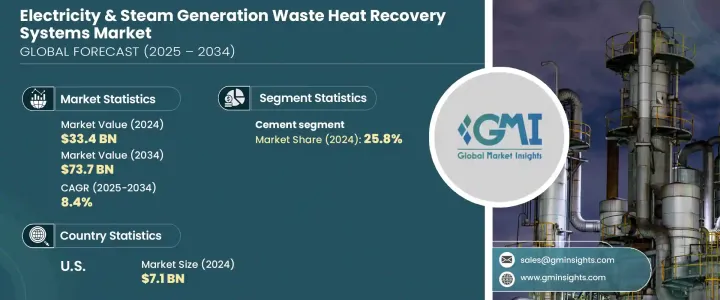

世界の電力・蒸気発生廃熱回収システム市場は、2024年に334億米ドルと評価され、CAGR 8.4%で成長し、2034年には737億米ドルに達すると推定されています。

この急成長は、世界のエネルギー効率重視の政策転換と環境コンプライアンスの厳格化に大きく支えられています。政府の支援は、廃熱回収技術の展開に有利な条件を作り出すのに役立っていることが証明されています。企業が全体的なエネルギー性能を向上させながら運転経費の削減を目指しているため、産業事業全体での採用が拡大し続けています。支持的な規制は、エネルギーコストの上昇と相まって、持続可能なソリューションとして回収システムの統合を業界に促しています。

地域暖房インフラに電力を供給する廃熱回収の役割は、ますます重要になってきています。これらのシステムは、生産プロセスや発電の際に使用されないはずの残留熱エネルギーを利用します。このエネルギーを集中暖房グリッドに振り向けることで、従来の燃料への依存度を大幅に減らし、排出量を削減することができます。都市がより環境に優しいエネルギー枠組みの導入を模索する中、こうしたソリューションは、循環的な資源利用と、よりスマートなエネルギー計画への道筋を提供します。これらの利点は、無駄の削減とシステム全体のパフォーマンス向上に重点を置くエネルギー計画担当者にアピールすることで、市場の潜在力を強化します。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 334億米ドル |

| 予測金額 | 737億米ドル |

| CAGR | 8.4% |

蒸気ランキンサイクルは、ガラス、鉄鋼、セメントなどの高温製造部門から熱を回収するための基礎となっています。産業用炭素集約度の低減に向けた規制の高まりが、こうしたシステムの近代化を加速させています。さらに、有機ランキンサイクルは、公共投資に支えられ、低温から中温の環境に適しているため、人気を集めています。カリーナ・サイクルのシェアは小さいが、高い熱効率を必要とする選択的な用途のために、引き続き資金援助を受けています。これらのサイクルを総合すると、持続可能性を高めるためによりクリーンなエネルギー変換技術を導入しようという国際的な機運が高まっていることがわかる。

2024年、セメント分野のシェアは25.8%でした。最もエネルギー集約的な産業の一つとして知られるセメントメーカーは、排出目標を達成するために廃熱回収システムの採用を増やしています。各地域の奨励金制度や再生可能電力義務(RPO)が、企業がWHRSに投資する強い動機となっています。一部の管轄区域では、これらのシステムを通じて生成されたエネルギーは再生可能エネルギーとして認定され、生産者にさらなるコンプライアンスと経済的利益をもたらしています。

米国の電気・蒸気発電廃熱回収システム市場は、2024年に71億米ドルに達し、北米が21.3%のシェアを占めました。エネルギー政策改革への注力と再生可能技術の統合が、この地域全体の廃熱回収ソリューションの需要拡大に極めて重要な役割を果たしています。よりクリーンなエネルギーを求める動きは、産業用エネルギー需要の増加と相まって、発電および蒸気生成アプリケーションにおけるこれらのシステムの採用を引き続き後押ししています。

電力・蒸気発電廃熱回収システム市場を形成する主要企業には、シーメンス・エナジー、クライミオン、三菱重工業、サーマックス・リミテッド、Bosch Industriekessel GmbH、フォータム、IHIコーポレーション、フォーブス・マーシャル、ゼネラル・エレクトリック、オーマット、HRS、アウラ、ヴィースマン、プロメック・エンジニアリング、エクセルギー・インターナショナルSRL、BIHL、レンテック・ボイラー、ソフインターS.p.A、ダール・グループ、コクランなどがあります。

電力・蒸気発電廃熱回収システム市場の企業は、市場での存在感を確固たるものにするため、技術のアップグレードと統合ソリューションに注力しています。多くの企業が研究開発に投資し、高温と低温の両方の産業プロセスに対応する、よりコンパクトで効率的なシステムを開発しています。鉄鋼、セメント、石油化学などのエネルギー多消費セクターとの戦略的提携により、顧客の要求に合わせたカスタマイズ設置が可能になっています。企業はまた、特に産業基盤が成長している地域において、合併、買収、提携を通じて地理的な足跡を拡大しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 戦略的ダッシュボード

- 戦略的取り組み

- 競合ベンチマーキング

- イノベーションとテクノロジーの情勢

第5章 市場規模・予測:タイプ別、2021年~2034年

- 主要動向

- 蒸気ランキンサイクル

- 有機ランキンサイクル

- カリーナサイクル

第6章 市場規模・予測:温度別、2021年~2034年

- 主要動向

- 230℃

- 230℃~650℃

- 650℃以上

第7章 市場規模・予測:最終用途別、2021年~2034年

- 主要動向

- 石油精製

- セメント

- 重金属製造

- 化学薬品

- パルプ・紙

- 食品・飲料

- ガラス

- その他

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第9章 企業プロファイル

- AURA

- BIHL

- Bosch Industriekessel GmbH

- Climeon

- Cochran

- Durr Group

- Exergy International SRL

- Forbes Marshall

- Fortum

- General Electric

- HRS

- IHI Corporation

- Mitsubishi Heavy Industries Ltd.

- Ormat

- Promec Engineering

- Rentech Boilers

- Siemens Energy

- Sofinter S.p.a

- Thermax Limited

- Viessman

The Global Electricity and Steam Generation Waste Heat Recovery Systems Market was valued at USD 33.4 billion in 2024 and is estimated to grow at a CAGR of 8.4% to reach USD 73.7 billion by 2034. This surge is largely supported by policy shifts emphasizing energy efficiency and stricter environmental compliance worldwide. Government support has proven instrumental in creating favorable conditions for the deployment of waste heat recovery technologies. Adoption across industrial operations continues to grow as businesses aim to cut operational expenses while improving overall energy performance. Supportive regulations, coupled with rising energy costs, are prompting industry to integrate recovery systems as a sustainable solution.

Waste heat recovery's role in powering district heating infrastructure is becoming increasingly relevant. These systems make use of residual thermal energy that would otherwise go unused during production processes or power generation. When redirected to centralized heating grids, this energy significantly reduces reliance on conventional fuels, thus lowering emissions. As cities seek to implement greener energy frameworks, these solutions offer a pathway to circular resource use and smarter energy planning. These benefits strengthen the market potential by appealing to energy planners focused on reducing waste and boosting system-wide performance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $33.4 Billion |

| Forecast Value | $73.7 Billion |

| CAGR | 8.4% |

The steam Rankine cycle remains the cornerstone for recovering heat from high-temperature manufacturing sectors like glass, steel, and cement. Growing regulatory focus on lowering industrial carbon intensity is accelerating the modernization of these systems. Additionally, the Organic Rankine Cycle is gaining traction due to its suitability in low- to medium-temperature settings, supported by public investment. Although the Kalina Cycle holds a smaller share, it continues to receive funding for selective applications that require high thermal efficiency. Altogether, these cycles point to a broader international momentum around implementing cleaner energy conversion technologies for enhanced sustainability.

In 2024, the cement segment generated a 25.8% share. Known for being one of the most energy-intensive industries, cement producers are increasingly adopting waste heat recovery systems to meet emission goals. Incentive programs and renewable power obligations (RPOs) across various regions have provided strong motivation for companies to invest in WHRS. In some jurisdictions, energy generated through these systems qualifies as renewable, giving producers additional compliance and economic benefits.

United States Electricity & Steam Generation Waste Heat Recovery Systems Market reached USD 7.1 billion in 2024, with North America capturing a 21.3% share. A focus on energy policy reform, combined with the integration of renewable technologies, has played a pivotal role in increasing demand for waste heat recovery solutions across the region. The push for cleaner energy, coupled with rising industrial energy demand, continues to drive the adoption of these systems in electricity and steam generation applications.

Key players shaping the Electricity & Steam Generation Waste Heat Recovery Systems Market include Siemens Energy, Climeon, Mitsubishi Heavy Industries Ltd., Thermax Limited, Bosch Industriekessel GmbH, Fortum, IHI Corporation, Forbes Marshall, General Electric, Ormat, HRS, AURA, Viessman, Promec Engineering, Exergy International SRL, BIHL, Rentech Boilers, Sofinter S.p.A, Durr Group, and Cochran.

Companies in the electricity & steam generation waste heat recovery systems market are focusing on technology upgrades and integrated solutions to solidify their market presence. Many are investing in R&D to develop more compact, efficient systems that cater to both high- and low-temperature industrial processes. Strategic collaborations with energy-intensive sectors such as steel, cement, and petrochemicals are enabling customized installations tailored to client requirements. Firms are also expanding their geographic footprint through mergers, acquisitions, and partnerships, especially in regions with growing industrial bases.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic dashboard

- 4.4 Strategic initiative

- 4.5 Competitive benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Type, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Steam rankine cycle

- 5.3 Organic rankine cycle

- 5.4 Kalina cycle

Chapter 6 Market Size and Forecast, By Temperature, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 230 °C

- 6.3 230 °C - 650 °C

- 6.4 > 650 °C

Chapter 7 Market Size and Forecast, By End Use, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 Petroleum refining

- 7.3 Cement

- 7.4 Heavy metal manufacturing

- 7.5 Chemical

- 7.6 Pulp & paper

- 7.7 Food & beverage

- 7.8 Glass

- 7.9 Others

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Australia

- 8.4.3 India

- 8.4.4 Japan

- 8.4.5 South Korea

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 AURA

- 9.2 BIHL

- 9.3 Bosch Industriekessel GmbH

- 9.4 Climeon

- 9.5 Cochran

- 9.6 Durr Group

- 9.7 Exergy International SRL

- 9.8 Forbes Marshall

- 9.9 Fortum

- 9.10 General Electric

- 9.11 HRS

- 9.12 IHI Corporation

- 9.13 Mitsubishi Heavy Industries Ltd.

- 9.14 Ormat

- 9.15 Promec Engineering

- 9.16 Rentech Boilers

- 9.17 Siemens Energy

- 9.18 Sofinter S.p.a

- 9.19 Thermax Limited

- 9.20 Viessman