|

市場調査レポート

商品コード

1755329

金融クラウド市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年)Finance Cloud Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 金融クラウド市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年) |

|

出版日: 2025年05月22日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

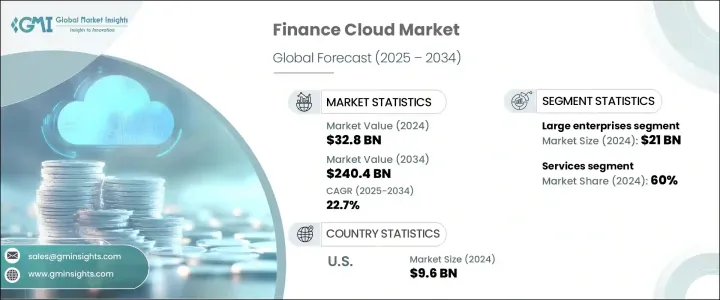

世界の金融クラウドの市場規模は、2024年に328億米ドルとなり、CAGR 22.7%で成長し、2034年には2,404億米ドルに達すると予測されています。

成長の原動力となっているのは、銀行、保険、投資管理、その他の金融分野におけるデジタル変革に対する需要の高まりです。企業は業務効率を高め、規制へのコンプライアンスを維持し、顧客体験を向上させるために、クラウドベースの金融ソリューションにシフトしています。自動化、人工知能(AI)、高度な分析を統合することで、リアルタイムの意思決定とプロアクティブなリスク管理を可能にし、金融ワークフローを変革します。

金融クラウドプラットフォームは、自動化された会計、リアルタイムの財務レポート、企業資源計画(ERP)や顧客関係管理(CRM)システムとのスムーズな接続など、最適化された財務業務の基盤を提供します。暗号化、多要素認証、ブロックチェーン対応トランザクション検証などの強化されたセキュリティプロトコルは、機密性の高い財務情報を保護し、厳しい規制要件を満たすのに役立ちます。キャッシュフロー予測のための予測分析、トランザクション処理のためのロボティック・プロセス・オートメーション(RPA)、対話型ダッシュボードのための拡張現実(AR)などのイノベーションは、市場導入を加速させます。これらの技術的進歩により、企業は財務サービスの差別化を図り、精度を向上させ、競争の激しい環境におけるビジネスの俊敏性を高めることができます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025~2034年 |

| 当初の市場規模 | 328億米ドル |

| 市場規模予測 | 2,404億米ドル |

| CAGR | 22.7% |

大企業セグメントの2024年の市場規模は210億米ドルでした。大企業のリーダーシップは、多額のIT予算と拡張可能で包括的なクラウドインフラを展開する能力に起因しています。これらの企業は、金融クラウドシステムを使用して、世界な財務プロセスを合理化し、規制コンプライアンスを確保し、多様な事業部門にまたがるサービスを統合しています。一元化されたクラウドプラットフォームは、ポリシーの一貫した実施と部門間の効率的な調整を可能にし、地域間で標準化されたプロセスと強固なセキュリティを提供します。

サービス分野は、コンサルティング、導入、サポート、マネージドサービスへのニーズの高まりにより、2024年には60%のシェアを占めています。金融機関がクラウド・ネイティブ・システムに移行する際、円滑な移行、統合、規制基準の遵守を確保するために、専門サービス・プロバイダーに大きく依存しています。これらのサービスは、金融機関がプラットフォームをカスタマイズし、ワークロードを管理し、セキュリティを維持しながら稼働時間を維持できるよう支援することで、クラウドのパフォーマンスを最適化します。継続的なサポートとマネージド・サービスにより、組織は中核機能に集中することができ、インフラ管理は外部に任せることができます。金融規制の複雑化、サイバーセキュリティリスク、デジタル変革の進行により、大企業や中小企業にとって専門的なクラウドサービスの戦略的重要性が高まっています。

米国の金融クラウド市場は2024年に96億米ドルとなり、2034年までCAGR 24%で成長すると予測されています。同国の強固なITインフラ、大手金融機関の存在、クラウド技術の早期導入がこの成長を後押ししています。強力な規制環境とダイナミックなフィンテック・エコシステムが、銀行、保険、投資の各分野でクラウドの採用を加速させています。米国の金融機関は、レガシーシステムの近代化、サイバーセキュリティの強化、シームレスなデジタル体験の提供のためにクラウドプラットフォームを活用しています。グーグルLLC、マイクロソフト、アマゾンなどの大手クラウドサービスプロバイダーとの提携が、この移行を支えています。

世界の金融クラウド業界の主要企業には、Salesforce、IBM、Dell、Oracle、Capgemini、Acumatica、Infosys、Amazon、Microsoft、Google LLCなどがあります。市場での存在感を高めるため、金融クラウド分野の企業は継続的なイノベーションと技術提供の拡大に注力しています。効率性とコンプライアンスを強化するため、AI主導の自動化ソリューションの開発に投資しています。金融機関やクラウドプロバイダーとの戦略的提携やパートナーシップは、導入を加速し、リーチを広げるのに役立ちます。各社は、業界標準を満たすために、セキュリティ機能と規制コンプライアンス機能の強化を優先しています。さらに、多くの企業は地域の規制に対応し、レイテンシーを削減するために、ローカライズされたサービスやデータセンターを通じて世界なフットプリントを拡大しています。

目次

第1章 分析手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 原材料供給者

- 部品供給業者

- メーカー

- 技術プロバイダー

- 流通チャネル分析

- 最終用途

- 利益率分析

- サプライヤーの情勢

- テクノロジーとイノベーションの情勢

- 特許分析

- 規制情勢

- コスト内訳分析

- 主なニュースと取り組み

- 影響要因

- 促進要因

- 顧客データと財務の管理

- 不正行為の検出と防止に対する需要の増加

- ビジネスインテリジェンスと戦略計画の強化の必要性の増大

- 強化された財務計画と分析

- 業界の潜在的リスクと課題

- データのプライバシーとセキュリティに関する懸念

- 既存のレガシーシステムとの統合が複雑になる可能性

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:種類別(2021~2034年)

- 主要動向

- サービス

- ソリューション

第6章 市場推計・予測:企業規模別(2021~2034年)

- 主要動向

- 大企業

- 中小企業

第7章 市場推計・予測:展開方式別(2021~2034年)

- 主要動向

- パブリック

- ハイブリッド

- プライベート

第8章 市場推計・予測:最終用途別(2021~2034年)

- 主要動向

- 銀行業務

- 保険

- 投資管理

- その他

第9章 市場推計・予測:用途別(2021~2034年)

- 主要動向

- 顧客関係管理

- 資産管理

- 資産運用管理

- アカウント管理

- 収益管理

- その他

第10章 市場推計・予測:地域別(2021~2034年)

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- イタリア

- ロシア

- 北欧諸国

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- Acumatica

- Amazon

- Aryaka

- Capgemini

- Cisco

- Dell

- Google LLC

- Hewlett Packard

- IBM

- Infosys

- Microsoft

- Oracle

- Rapidscale

- Sage

- Salesforce

- ServiceNow

- Tata Consultancy

- Unit4

- Wipro

- Workday

- Yardi

The Global Finance Cloud Market was valued at USD 32.8 billion in 2024 and is estimated to grow at a CAGR of 22.7% to reach USD 240.4 billion by 2034. The growth is driven by the rising demand for digital transformation within banking, insurance, investment management, and other financial sectors. Companies shift to cloud-based finance solutions to boost operational efficiency, maintain compliance with regulations, and enhance customer experience. Integrating automation, artificial intelligence (AI), and advanced analytics transform financial workflows by enabling real-time decision-making and proactive risk management.

Finance cloud platforms provide a foundation for optimized financial operations, including automated accounting, real-time financial reporting, and smooth connectivity with enterprise resource planning (ERP) and customer relationship management (CRM) systems. Enhanced security protocols such as encryption, multi-factor authentication, and blockchain-enabled transaction verification protect sensitive financial information and help meet stringent regulatory requirements. Innovations like predictive analytics for cash flow forecasting, robotic process automation (RPA) for transaction handling, and augmented reality (AR) for interactive dashboards accelerate market adoption. These technological advancements allow organizations to differentiate their financial offerings, improve accuracy, and increase business agility in a highly competitive environment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $32.8 Billion |

| Forecast Value | $240.4 Billion |

| CAGR | 22.7% |

The large enterprises segment was valued at USD 21 billion in 2024. Their leadership stems from substantial IT budgets and the ability to deploy scalable, comprehensive cloud infrastructures. These organizations use finance cloud systems to streamline global financial processes, ensure regulatory compliance, and integrate services across diverse business units. Centralized cloud platforms enable consistent enforcement of policies and efficient coordination between departments, delivering standardized processes and robust security across regions.

The services segment held a 60% share in 2024, driven by the increasing need for consulting, implementation, support, and managed services. As financial institutions migrate to cloud-native systems, they depend heavily on specialized service providers to ensure smooth transitions, integration, and adherence to regulatory standards. These services optimize cloud performance by helping institutions customize platforms, manage workloads, and maintain uptime while upholding security. Continuous support and managed services free organizations to focus on core functions while infrastructure management is handled externally. The complexity of financial regulations, cybersecurity risks, and ongoing digital transformation has elevated the strategic importance of specialized cloud services for large corporations and SMEs.

U.S. Finance Cloud Market was valued at USD 9.6 billion in 2024 and is expected to grow at a CAGR of 24% through 2034. The country's robust IT infrastructure, presence of major financial institutions, and early adoption of cloud technologies fuel this growth. A strong regulatory environment along with a dynamic fintech ecosystem accelerates cloud adoption across banking, insurance, and investment sectors. Financial firms in the U.S. leverage cloud platforms to modernize legacy systems, strengthen cybersecurity, and deliver seamless digital experiences. Partnerships with leading cloud service providers like Google LLC, Microsoft, and Amazon support this transition.

Key players in the Global Finance Cloud Industry include Salesforce, IBM, Dell, Oracle, Capgemini, Acumatica, Infosys, Amazon, Microsoft, and Google LLC. To strengthen their market presence, companies in the finance cloud sector focus on continuous innovation and expanding their technology offerings. They invest in developing AI-driven and automation-powered solutions to enhance efficiency and compliance. Strategic alliances and partnerships with financial institutions and cloud providers help accelerate adoption and broaden their reach. Firms prioritize enhancing security features and regulatory compliance capabilities to meet industry standards. Additionally, many are scaling their global footprint through localized services and data centers to cater to regional regulations and reduce latency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 Distribution channel analysis

- 3.1.1.6 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Regulatory landscape

- 3.5 Cost breakdown analysis

- 3.6 Key news & initiatives

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Managing customer data and financials

- 3.7.1.2 Increased demand for fraud detection and prevention

- 3.7.1.3 Rising need to enhance business intelligence and strategic planning

- 3.7.1.4 Enhanced financial planning and analysis

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 Data privacy and security concerns

- 3.7.2.2 Integration with the existing legacy systems can be complex

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Services

- 5.3 Solution

Chapter 6 Market Estimates & Forecast, By Enterprise size, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Large enterprises

- 6.3 SME

Chapter 7 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Public

- 7.3 Hybrid

- 7.4 Private

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Banking

- 8.3 Insurance

- 8.4 Investment management

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Customer relationship management

- 9.3 Wealth management

- 9.4 Asset management

- 9.5 Account management

- 9.6 Revenue management

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 France

- 10.3.3 UK

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Acumatica

- 11.2 Amazon

- 11.3 Aryaka

- 11.4 Capgemini

- 11.5 Cisco

- 11.6 Dell

- 11.7 Google LLC

- 11.8 Hewlett Packard

- 11.9 IBM

- 11.10 Infosys

- 11.11 Microsoft

- 11.12 Oracle

- 11.13 Rapidscale

- 11.14 Sage

- 11.15 Salesforce

- 11.16 ServiceNow

- 11.17 Tata Consultancy

- 11.18 Unit4

- 11.19 Wipro

- 11.20 Workday

- 11.21 Yardi