|

市場調査レポート

商品コード

1716508

データセンター自動化市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Data Center Automation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| データセンター自動化市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月17日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

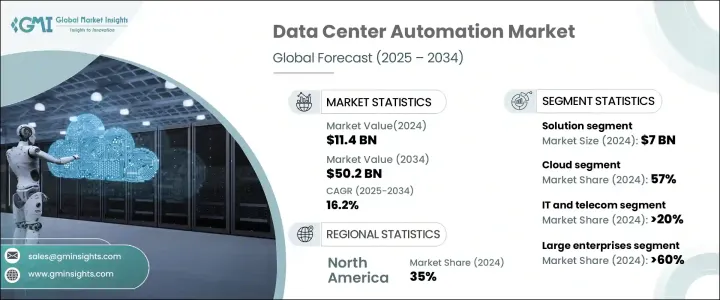

世界のデータセンター自動化市場は、2024年に114億米ドルに達し、2025年から2034年にかけて16.2%のCAGRで堅調に成長すると予測されています。

この顕著な成長は、クラウドサービス、ソーシャルメディアプラットフォーム、ビデオストリーミングの採用が増加し、業界全体でIoTデバイスが普及していることが背景にあります。組織がクラウドベースのインフラやデジタルストレージにシフトするにつれ、データセンター運用の効率化と自動化の必要性が最も高まっています。自動化は運用効率を向上させるだけでなく、人的ミスを減らし、膨大なデータのシームレスな管理を実現します。データの複雑さと量の増加に伴い、企業は機械学習(ML)、人工知能(AI)、クラウド・コンピューティングなどの先進技術に目を向け、スケーラビリティとパフォーマンスを強化しています。

これらのテクノロジーは、システムプロセスを最適化し、ダウンタイムを最小化し、予知保全をサポートすることで、急速に進化するデジタル情勢の中で企業が競争力を維持することを可能にします。さらに、サイバーセキュリティとデータ保護が重視されるようになったことで、企業はデータセンターに自動化を導入し、リアルタイムの脅威検知と安全なデータ処理を実現する必要に迫られています。ハイブリッド環境やマルチクラウド環境を採用する業界が増えるにつれ、データセンター自動化ソリューションの需要は急増し、自動化技術の革新的な進歩への道が開かれると予想されます。デジタルインフラとクラウド技術の導入を推進する政府のイニシアティブが市場をさらに強化し、データセンター自動化が現代のビジネス戦略にとって重要な要素となっています。

| 市場規模 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 114億米ドル |

| 予測金額 | 502億米ドル |

| CAGR | 16.2% |

データセンター自動化市場は、主にソリューションとサービスに区分されます。ソリューションセグメントが60%のシェアを占め、2024年には70億米ドルの市場規模になります。自動化ソフトウェアは、組織がリソース割り当てを最適化し、ルーチンタスクを自動化し、データセンターの稼働時間を増加させ、シームレスな運用を確保するのに役立ちます。企業が運用効率の向上に努める中、リアルタイムのデータ管理とワークロードの自動化を可能にする高度なソリューションへの需要は高まり続けています。一方、自動化システムの導入と保守において、専門家による指導と継続的なサポートを求める企業が増えているため、サービス分野も急成長しています。技術の進歩が加速する中、企業は自動化投資の価値を最大化し、長期的な成功を確実にするために、専門家の洞察と戦略的コンサルティングに依存しています。

導入形態の観点から、データセンター自動化市場はオンプレミスとクラウドベースのソリューションに分けられます。クラウドセグメントは2024年に57%のシェアを占め、リモートアクセス、セキュリティ機能、柔軟性に対する嗜好の高まりがその要因となっています。クラウド・ソリューションは、インターネット接続を通じてどこからでもデータにシームレスにアクセスできるため、遠隔地のチームや複数のデバイスで作業する個人に最適です。データ・セキュリティが最優先事項となる中、クラウド・プロバイダーは暗号化、多要素認証、リアルタイムの脅威監視を提供することでセキュリティ対策を強化し、機密情報の保護に努めています。

北米のデータセンター自動化市場は市場シェア全体の35%を占め、2024年には30億米ドルを生み出します。北米のデータセンター全体でAI、ML、その他の先進技術が急速に採用されていることが、同地域の大きな成長を促進しています。企業は、運用効率の向上、セキュリティの強化、予知保全の実現に向けて、AIを活用した自動化をますます重視するようになっており、データセンター自動化ソリューションの需要急増に寄与しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- ソリューションプロバイダー

- クラウドサービスプロバイダー

- システムインテグレーター

- エンドユース

- 利益率分析

- テクノロジーとイノベーションの展望

- 特許分析

- 主要ニュースとイニシアチブ

- 規制状況

- 影響要因

- 促進要因

- データ量の増加

- クラウド・コンピューティング、機械学習、人工知能の台頭

- 運用コストの削減

- 問題解決によるダウンタイムの最小化

- 業界の潜在的リスク&課題

- 熟練した専門家の不足

- 実装の複雑さ

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ソリューション

- サーバー自動化

- ネットワークの自動化

- ストレージ自動化

- セキュリティオートメーション

- その他

- サービス

第6章 市場推計・予測:展開モード別、2021年~2034年

- 主要動向

- オンプレミス

- クラウド

第7章 市場推計・予測:組織規模別、2021年~2034年

- 主要動向

- 中小企業

- 大企業

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- BFSI

- コロケーション

- エネルギー

- 政府機関

- ヘルスケア

- 製造業

- IT&テレコム

- その他

第9章 市場推計・予測:データセンタータイプ別、2021年~2034年

- 主要動向

- エンタープライズデータセンター

- コロケーションデータセンター

- パブリッククラウドデータセンター

- エッジデータセンター

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- ABB

- Arista Networks

- BMC Software

- Broadcom

- Cisco

- Citrix

- Fujitsu

- HPE

- Huawei Enterprise

- IBM

- Juniper

- Microsoft

- NTT Communications

- Open Text(Micro Focus)

- Progress Chef

- Puppet(Perforce)

- Rockwell Automation

- VMware

The Global Data Center Automation Market reached USD 11.4 billion in 2024 and is projected to grow at a robust CAGR of 16.2% between 2025 and 2034. This remarkable growth is driven by the rising adoption of cloud services, social media platforms, video streaming, and the proliferation of IoT devices across industries. As organizations shift towards cloud-based infrastructure and digital storage, the need for efficient and automated data center operations has become paramount. Automation not only improves operational efficiency but also reduces human errors, ensuring seamless management of vast amounts of data. With increasing data complexity and volume, businesses are turning to advanced technologies like machine learning (ML), artificial intelligence (AI), and cloud computing to enhance scalability and performance.

These technologies optimize system processes, minimize downtime, and support predictive maintenance, allowing companies to stay competitive in a rapidly evolving digital landscape. Moreover, the growing emphasis on cybersecurity and data protection is pushing organizations to implement automation in data centers, ensuring real-time threat detection and secure data handling. As more industries adopt hybrid and multi-cloud environments, the demand for data center automation solutions is expected to surge, paving the way for innovative advancements in automation technologies. Government initiatives promoting the adoption of digital infrastructure and cloud technologies further strengthen the market, making data center automation a critical component of modern business strategies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.4 Billion |

| Forecast Value | $50.2 Billion |

| CAGR | 16.2% |

The data center automation market is primarily segmented into solutions and services. The solution segment dominated the market with a 60% share, generating USD 7 billion in 2024. Automation software helps organizations optimize resource allocation, automate routine tasks, and increase the uptime of data centers, ensuring seamless operations. As businesses strive to enhance operational efficiency, the demand for advanced solutions that enable real-time data management and workload automation continues to rise. Meanwhile, the service segment is growing rapidly as organizations seek expert guidance and ongoing support in implementing and maintaining automated systems. As technological advancements accelerate, companies rely on expert insights and strategic consulting to maximize the value of their automation investments and ensure long-term success.

In terms of deployment mode, the data center automation market is divided into on-premises and cloud-based solutions. The cloud segment held a 57% share in 2024, driven by the growing preference for remote accessibility, security features, and flexibility. Cloud solutions enable seamless access to data from any location through an internet connection, making them ideal for remote teams and individuals working across multiple devices. With data security becoming a top priority, cloud providers are enhancing their security measures by offering encryption, multi-factor authentication, and real-time threat monitoring to protect sensitive information.

North America data center automation market accounted for 35% of the total market share, generating USD 3 billion in 2024. The rapid adoption of AI, ML, and other advanced technologies across data centers in North America is driving significant growth in the region. Businesses are increasingly turning to AI-driven automation to enhance operational efficiency, strengthen security, and enable predictive maintenance, contributing to the surging demand for data center automation solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Solution providers

- 3.2.2 Cloud service providers

- 3.2.3 System integrators

- 3.2.4 End use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rising volumes of data

- 3.8.1.2 The rise of cloud computing, machine learning and artificial intelligence

- 3.8.1.3 Reduction of operational cost

- 3.8.1.4 Resolve issues to minimize the downtime

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Lack of skilled professionals

- 3.8.2.2 Complexity in implementation

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Solution

- 5.2.1 Server automation

- 5.2.2 Network automation

- 5.2.3 Storage automation

- 5.2.4 Security automation

- 5.2.5 Others

- 5.3 Service

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-Premises

- 6.3 Cloud

Chapter 7 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 SME

- 7.3 Large enterprises

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 BFSI

- 8.3 Colocation

- 8.4 Energy

- 8.5 Government

- 8.6 Healthcare

- 8.7 Manufacturing

- 8.8 IT & Telecom

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By Data Center Type, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Enterprise data center

- 9.3 Colocation data center

- 9.4 Public cloud data center

- 9.5 Edge data center

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 ABB

- 11.2 Arista Networks

- 11.3 BMC Software

- 11.4 Broadcom

- 11.5 Cisco

- 11.6 Citrix

- 11.7 Fujitsu

- 11.8 HPE

- 11.9 Huawei Enterprise

- 11.10 IBM

- 11.11 Juniper

- 11.12 Microsoft

- 11.13 NTT Communications

- 11.14 Open Text (Micro Focus)

- 11.15 Progress Chef

- 11.16 Puppet (Perforce)

- 11.17 Rockwell Automation

- 11.18 VMware