|

|

市場調査レポート

商品コード

1667006

金属電線管市場の機会、成長促進要因、産業動向分析、2025~2034年の予測Metal Electrical Conduit Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 金属電線管市場の機会、成長促進要因、産業動向分析、2025~2034年の予測 |

|

出版日: 2024年12月03日

発行: Global Market Insights Inc.

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

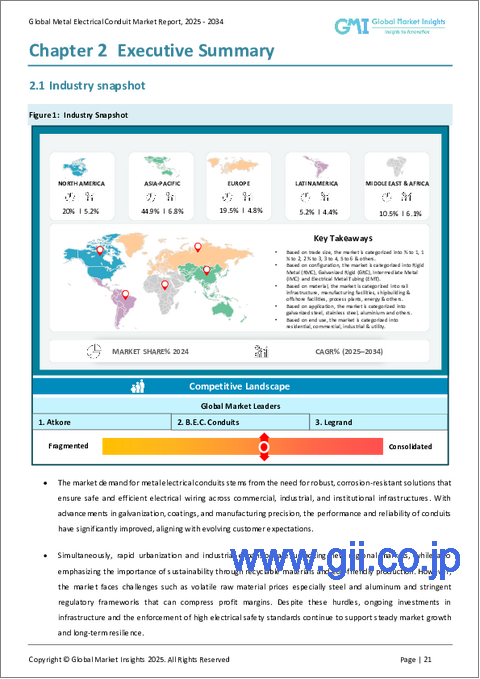

世界の金属電線管市場は、2024年に34億米ドルと評価され、2025年から2034年にかけてCAGR 5.9%で成長する見込みです。 この成長は、建設活動の拡大、急速な工業化、堅牢な電気インフラの必要性によって促進されます。

都市化とエネルギー効率の高い再生可能電力システムへの移行が市場需要をさらに拡大し、インフラ近代化プロジェクトが採用促進に極めて重要な役割を果たしています。

持続可能な素材と競合価格の進歩が、電線管製造の技術革新に拍車をかけています。企業は、サプライチェーンを最適化し、流通網を拡大するために、戦略的パートナーシップや買収に注力しています。このアプローチは、持続可能な建設慣行と厳格な安全基準の遵守を世界的に重視するようになっていることと一致しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 34億米ドル |

| 予測金額 | 62億米ドル |

| CAGR | 5.9% |

中間金属導管(IMC)分野は、その軽量設計、費用対効果、強度により、2034年までに16億米ドルの売上が見込まれています。IMCは、同等の性能を維持しながら、硬質金属導管(RMC)に代わる経済的な選択肢を提供し、産業用および商業用用途にますます支持されています。耐腐食性とコーティングを施した電線管に対する需要の高まりは、進化する顧客要件と規制基準を満たすためにメーカーが技術革新を進めるにつれて、多様化を促進しています。エネルギー効率の高い建築基準が市場力学を再構築するにつれて、カスタマイズと持続可能性が重要な要素になりつつあります。

エネルギー部門は、2034年までのCAGRが4.5%と、大きな成長を遂げる見込みです。太陽光発電や風力発電を含む再生可能エネルギー・プロジェクトでは、電気配線を保護し運用の安全性を確保するため、信頼性が高く耐候性に優れた電線管が必要とされます。スマートグリッドインフラと高度なエネルギー管理システムの拡大は、複雑なネットワークをサポートするように設計された高品質の導管に対する需要をさらに押し上げています。メーカー各社は、環境に配慮した建設の重要性の高まりを反映し、エネルギー部門の持続可能性目標に沿った耐火性・耐腐食性製品を投入しています。

米国の金属電線管市場は、2034年までに8億3,000万米ドルを創出すると予測されています。住宅、商業、工業分野のインフラ開発と都市化が相まって、耐久性、耐火性、長寿命の電線管に対する需要が高まっています。再生可能エネルギー源へのシフトが進む同国では、近代的なエネルギー構想をサポートできる信頼性の高い電気システムの必要性がさらに高まっています。

全体として、金属電線管市場は、技術の進歩、持続可能性の動向、世界のインフラ開発の高まりに支えられ、持続的な成長の態勢を整えています。材料設計の革新と厳格な安全基準を満たすことに重点を置くことで、同市場は多様な産業の進化する需要に対応できる体制を整えています。

目次

第1章 調査手法と調査範囲

- 市場の定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 2次データ

- 有償

- 公的

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

第4章 競合情勢

- 戦略ダッシュボード

- イノベーションと持続可能性の展望

第5章 市場規模・予測:取引規模別、2021年~2034年

- 主要動向

- 1/2~1

- 1 1/4~2

- 2 1/2~3

- 3~4

- 5~6

- その他

第6章 市場規模・予測:構成別、2021年~2034年

- 主要動向

- 硬質金属(RMC)

- 亜鉛めっき硬質(GRC)

- 中間金属(IMC)

- 電気金属管(EMT)

第7章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 鉄道インフラ

- 製造施設

- 造船・海洋施設

- プロセスプラント

- エネルギー

- その他

第8章 市場規模・予測:最終用途別、2021年~2034年

- 主要動向

- 住宅用

- 商業用

- 産業用

- ユーティリティ

第9章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- フランス

- ドイツ

- イタリア

- 英国

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第10章 企業プロファイル

- Anamet Electrical

- American Conduit

- Atkore

- Flexa

- Gibson Stainless &Specialty

- HellermannTyton

- Legrand

- Nucor Tubular Products

- Schneider Electric

- Techno Flex

- United Pipe &Steel

- Weifang East Steel Pipe

- Western Tube

- Wheatland Tube

- Zekelman Industries

The Global Metal Electrical Conduit Market, valued at USD 3.4 billion in 2024, is poised to grow at a CAGR of 5.9% during 2025-2034. This growth is fueled by expanding construction activities, rapid industrialization, and the need for robust electrical infrastructure. Urbanization and the transition to energy-efficient and renewable power systems further amplify market demand, with infrastructure modernization projects playing a pivotal role in driving adoption.

Advancements in sustainable materials and competitive pricing have spurred innovation in conduit manufacturing. Companies are focusing on strategic partnerships and acquisitions to optimize supply chains and broaden distribution networks. This approach aligns with the increasing global emphasis on sustainable construction practices and adherence to stringent safety standards.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.4 Billion |

| Forecast Value | $6.2 Billion |

| CAGR | 5.9% |

The intermediate metal conduit (IMC) segment is expected to generate USD 1.6 billion by 2034, owing to its lightweight design, cost-effectiveness, and strength. IMCs are increasingly favored for industrial and commercial applications, offering an economical alternative to rigid metal conduits (RMC) while maintaining comparable performance. Rising demand for corrosion-resistant and coated conduits is driving diversification as manufacturers innovate to meet evolving customer requirements and regulatory standards. Customization and sustainability are becoming critical factors as energy-efficient building codes reshape market dynamics.

The energy sector is set to experience significant growth, with a CAGR of 4.5% through 2034. Renewable energy projects, including solar and wind installations, require reliable, weather-resistant conduits to protect electrical wiring and ensure operational safety. The expansion of smart grid infrastructure and advanced energy management systems is further boosting demand for high-quality conduits designed to support complex networks. Manufacturers are introducing fire-resistant and corrosion-proof products that align with the energy sector's sustainability goals, reflecting the growing importance of environmentally conscious construction.

U.S. metal electrical conduit market is projected to generate USD 830 million through 2034. Infrastructure development in residential, commercial, and industrial sectors, coupled with urbanization, is driving demand for durable, fire-resistant, and long-lasting conduits. The country's increasing shift toward renewable energy sources has further fueled the need for reliable electrical systems capable of supporting modern energy initiatives.

Overall, the metal electrical conduit market is poised for sustained growth, supported by technological advancements, sustainability trends, and rising global infrastructure development. With innovations in material design and a focus on meeting rigorous safety standards, the market is well-positioned to address the evolving demands of diverse industries.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Trade Size, 2021 – 2034 (USD Million)

- 5.1 Key trends

- 5.2 ½ to 1

- 5.3 1 ¼ to 2

- 5.4 2 ½ to 3

- 5.5 3 to 4

- 5.6 5 to 6

- 5.7 Others

Chapter 6 Market Size and Forecast, By Configuration, 2021 – 2034 (USD Million)

- 6.1 Key trends

- 6.2 Rigid metal (RMC)

- 6.3 Galvanized rigid (GRC)

- 6.4 Intermediate metal (IMC)

- 6.5 Electrical metal tubing (EMT)

Chapter 7 Market Size and Forecast, By Application, 2021 – 2034 (USD Million)

- 7.1 Key trends

- 7.2 Rail infrastructure

- 7.3 Manufacturing facilities

- 7.4 Shipbuilding & offshore facilities

- 7.5 Process plants

- 7.6 Energy

- 7.7 Others

Chapter 8 Market Size and Forecast, By End Use, 2021 – 2034 (USD Million)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.4 Industrial

- 8.5 Utility

Chapter 9 Market Size and Forecast, By Region, 2021 – 2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 France

- 9.3.2 Germany

- 9.3.3 Italy

- 9.3.4 UK

- 9.3.5 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 Qatar

- 9.5.4 South Africa

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Argentina

Chapter 10 Company Profiles

- 10.1 Anamet Electrical

- 10.2 American Conduit

- 10.3 Atkore

- 10.4 Flexa

- 10.5 Gibson Stainless & Specialty

- 10.6 HellermannTyton

- 10.7 Legrand

- 10.8 Nucor Tubular Products

- 10.9 Schneider Electric

- 10.10 Techno Flex

- 10.11 United Pipe & Steel

- 10.12 Weifang East Steel Pipe

- 10.13 Western Tube

- 10.14 Wheatland Tube

- 10.15 Zekelman Industries