睡眠時無呼吸症候群治療機器市場のビジネスチャンス、成長要因、業界動向分析、および2026年~2035年の予測

Sleep Apnea Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035- 発行日

- ページ情報

- 英文 176 Pages

- 納期

- 2~3営業日

- 商品コード

- 2038383

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

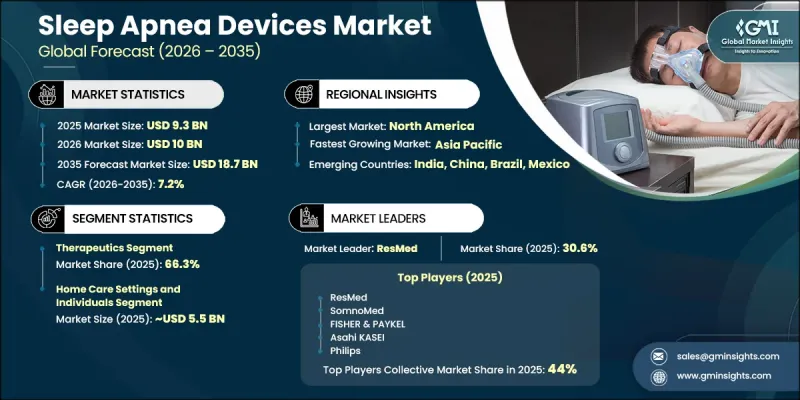

世界の睡眠時無呼吸症候群治療機器市場は、2025年に93億米ドルと評価され、CAGR 7.2%で成長し、2035年までに187億米ドルに達すると予測されています。

睡眠時無呼吸症候群関連機器業界は、睡眠関連呼吸障害の有病率の増加、意識の高まり、そして継続的な技術革新により、着実な拡大を遂げています。コンパクトで効率的かつ高性能な治療ソリューションへの需要の高まりが、市場情勢を一新しています。加齢に伴う疾患が睡眠障害に大きく寄与していることから、高齢人口の増加が導入をさらに加速させています。並行して、医療機関や市場参入企業による啓発活動の増加により、診断率と治療率が向上しています。ワイヤレス接続、クラウドベースのプラットフォーム、モバイル対応モニタリングなどの先進技術の統合により、患者のエンゲージメントが向上し、遠隔治療管理が可能になっています。これらの進歩により、治療の順守状況や有効性をリアルタイムで追跡できるようになり、長期的な治療成果が向上しています。睡眠時無呼吸症候群治療機器は、気道の確保、酸素供給の改善、睡眠の質の向上において重要な役割を果たしており、それによって関連する健康リスクを最小限に抑え、患者の全体的な健康をサポートしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026年~2035年 |

| 開始時の市場規模 | 93億米ドル |

| 予測額 | 187億米ドル |

| CAGR | 7.2% |

治療機器セグメントは、治療の快適性と有効性の向上を目的とした継続的なイノベーションに支えられ、2025年には66.3%のシェアを占めました。先進的な治療機器には、使いやすさの向上や性能の向上が組み込まれており、患者のコンプライアンス向上と長期的な治療の成功に寄与しています。

睡眠検査室および病院セグメントは、CAGR 6.3%で成長し、2035年までに70億米ドルに達すると予測されています。このセグメントの成長は、臨床的に管理された診断および治療ソリューションへの需要の高まりによって牽引されています。正確な診断と体系的な治療経路へのニーズが、医療施設全体での拡大を後押しし続けています。

米国睡眠時無呼吸症候群治療機器市場は、2025年に39億米ドルと評価されました。市場の成長は、有利な償還制度と、利便性の高い診断手法の普及によって支えられています。利用しやすい検査および治療ソリューションへの移行は、患者の参加を促進し、市場全体のリーチを拡大しています。

よくあるご質問

目次

第1章 調査手法

- 調査アプローチ

- 品質に関する取り組み

- GMI AIポリシーおよびデータ完全性への取り組み

- 情報源の一貫性に関するプロトコル

- GMI AIポリシーおよびデータ完全性への取り組み

- 調査の経緯と信頼度スコアリング

- 調査トレイルの構成要素

- スコアリングの構成要素

- データ収集

- 一次情報の一部リスト

- データマイニング情報源

- 有料情報源

- 地域別情報源

- 有料情報源

- 基本推定と算出方法

- 基準年の算出

- 予測モデル

- 定量化された市場影響分析

- 成長パラメータが予測に与える数学的影響

- 定量化された市場影響分析

- 調査の透明性に関する補足

- 情報源の帰属フレームワーク

- 品質保証指標

- 信頼への取り組み

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 睡眠時無呼吸症候群および関連する併存疾患の発生率の増加

- 携帯型で高性能な睡眠時無呼吸症候群ソリューションへの需要の高まり

- 睡眠時無呼吸症候群および睡眠障害に対する認識の高まり

- 高齢化の進展が需要を拡大

- 技術的進歩

- 業界の潜在的リスク&課題

- 睡眠時無呼吸症候群治療の遵守不足

- 製品リコールと安全上の懸念

- 機会

- 新興市場への進出

- AIとデジタルヘルスの統合

- 促進要因

- 成長可能性分析

- 規制状況(1次調査に基づく)

- 北米

- 欧州

- アジア太平洋地域

- 技術およびイノベーションの動向

- 現在の技術動向

- 新興技術

- 将来の市場動向(1次調査に基づく)

- 償還シナリオ

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- SOMNOMED LIMITED

- フィッシャー・アンド・ペイケル・ヘルスケア

- ResMed Inc.

- 企業マトリックス分析

- 企業の市場シェア分析(1次調査に基づく)

- 世界

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ(MEA)

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- パートナーシップおよび提携

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:製品別、2022-2035

- 治療機器

- 陽圧呼吸(PAP)装置

- 持続的気道陽圧(CPAP)装置

- 自動陽圧呼吸(APAP)装置

- 二段階陽圧呼吸(BiPAP)装置

- 口腔内装置

- 下顎前突装置

- 舌保持装置

- 適応型サーボ換気(ASV)装置

- 気道クリアランスシステム

- その他の治療用製品

- 陽圧呼吸(PAP)装置

- 診断機器

- 在宅睡眠検査(HST)装置

- タイプ2

- タイプ3

- タイプ4

- 睡眠ポリソムノグラフィー(PSG)装置

- 臨床用PSG装置

- 携帯型PSG装置

- アクティグラフィシステム

- その他の診断機器

- 在宅睡眠検査(HST)装置

第6章 市場推計・予測:最終用途別、2022-2035

- 在宅ケア施設および個人

- 睡眠検査室および病院

第7章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ(MEA)

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第8章 企業プロファイル

- Apnea Sciences

- Asahi KASEI

- BMC

- Cadwell

- Drive DeVilbiss

- DynaFlex

- FISHER & PAYKEL

- Glidewell

- natus

- NIHON KOHDEN

- Philips

- ResMed

- SomnoMed

- Teleflex

- WEINMANN

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 176 Pages

- 納期

- 2~3営業日