|

市場調査レポート

商品コード

1913460

スマート医療機器市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Smart Medical Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| スマート医療機器市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月18日

発行: Global Market Insights Inc.

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

概要

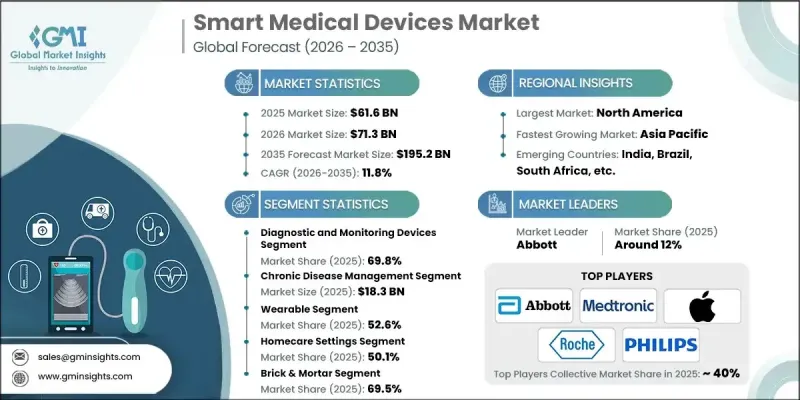

世界のスマート医療機器市場は、2025年に616億米ドルと評価され、2035年までにCAGR 11.8%で成長し、1,952億米ドルに達すると予測されています。

この成長は、糖尿病や喘息などの慢性疾患の有病率の上昇と、在宅医療ソリューションや遠隔患者モニタリング(RPM)デバイスに対する需要の高まりによって促進されています。遠隔医療やデジタルヘルスプラットフォームの拡大、そしてIoT、AI、クラウドベースの統合における技術の進歩が、スマート医療機器の採用を推進しています。ウェアラブルデバイスや小型デバイス、予防医療、在宅医療モデルなどの動向も、市場の需要をさらに押し上げています。アボット、アップル、メドトロニック、ロシュ、フィリップスなどの大手企業は、市場での存在感を強化するため、地理的な拡大、製品の革新、手頃な価格、医療提供者との提携に注力しています。健康意識の高まりと、個別化されたリアルタイムの患者モニタリングへの移行が、業界の成長に大きく貢献しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025 |

| 予測年 | 2026-2035 |

| 開始時価値 | 616億米ドル |

| 予測金額 | 1,952億米ドル |

| CAGR | 11.8% |

診断・モニタリング機器セグメントは2025年に69.8%のシェアを占めました。このセグメントには、持続血糖測定装置(CGM)、ウェアラブル心電図パッチ、スマート血圧計、パルスオキシメーターが含まれます。これらの機器は生理データをリアルタイムで継続的に収集し、接続されたプラットフォームへ送信して分析を行います。技術プロバイダーと医療機関との提携により、患者モニタリングのアクセス性と効率性が向上し、このカテゴリーのさらなる成長が期待されます。

慢性疾患管理セグメントは2025年に183億米ドルに達しました。慢性疾患管理向けスマートデバイスは、ウェアラブルセンサー、在宅モニタリング機器、服薬遵守システムを統合し、バイタルサイン、症状、治療法の使用状況を追跡します。リアルタイムのデータ収集により、臨床医と患者はリスクスコアを評価し、複数の疾患を効果的に管理することが可能となり、長期治療を支援し患者の治療成果を向上させます。

北米スマート医療機器市場は2025年に34.8%のシェアを占めました。地域的な成長は、確立された医療システム、慢性疾患の高い罹患率、デジタルヘルス技術の普及、有利な償還政策によって推進されています。健康保険の普及と先進的な遠隔医療インフラが、同地域におけるスマートデバイスの導入をさらに後押ししており、北米はスマートヘルスケアソリューションの革新と成長における主要市場としての地位を確立しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 糖尿病、喘息その他の疾患の増加傾向

- 急成長する医療機器産業

- インターネット普及率の増加とビッグデータの採用

- 診断と治療におけるリアルタイムデータ駆動型アプローチの重要性が高まっています

- 業界の潜在的リスク&課題

- プライバシーに関する懸念

- 低・中所得国における適切なインフラの不足

- 促進要因

- 成長可能性分析

- 規制情勢

- 償還シナリオ

- 技術的情勢

- 価格分析

- 将来の市場動向

- サプライヤーの情勢

- M&A活動

- ポーター分析

- PESTEL分析

- ギャップ分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品タイプ別、2021-2032

- 診断・モニタリング機器

- 血糖値測定器

- 心拍数モニター

- パルスオキシメーター

- 血圧計

- アルコール検知器

- その他の診断・モニタリング機器

- 治療用機器

- 携帯型酸素濃縮器および人工呼吸器

- インスリンポンプ

- 補聴器

- その他の治療用機器

- その他の製品タイプ

第6章 市場推計・予測:最終用途別、2021-2032

- 病院

- 在宅医療環境

- その他の用途

第7章 市場推計・予測:流通チャネル別、2021-2032

- 実店舗

- 電子商取引

第8章 市場推計・予測:地域別、2021-2032

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Abbott

- Apple

- Biobeat

- Boston Scientific Corporation

- Dexcom

- F Hoffmann-La Roche

- Fitbit

- Medtronic

- NeuroMetrix

- Novo Nordisk

- Omron Corporation

- SAMSUNG

- VitalConnect

- West Pharmaceutical Services