|

|

市場調査レポート

商品コード

1663765

C型肝炎治療薬の世界市場:競合情勢Hepatitis C Therapeutics: Competitive Landscape |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| C型肝炎治療薬の世界市場:競合情勢 |

|

出版日: 2024年12月13日

発行: GlobalData

ページ情報: 英文 84 Pages

納期: 即納可能

|

全表示

- 概要

- 目次

2024年のC型肝炎(HCV)感染者数は推定2,516万人であり、2029年までに2,584万人に微増すると予測されています。

HCV治療には革命的な変化の波が押し寄せており、現在では直接作用型抗ウイルス薬(DAA)が主流となっています。

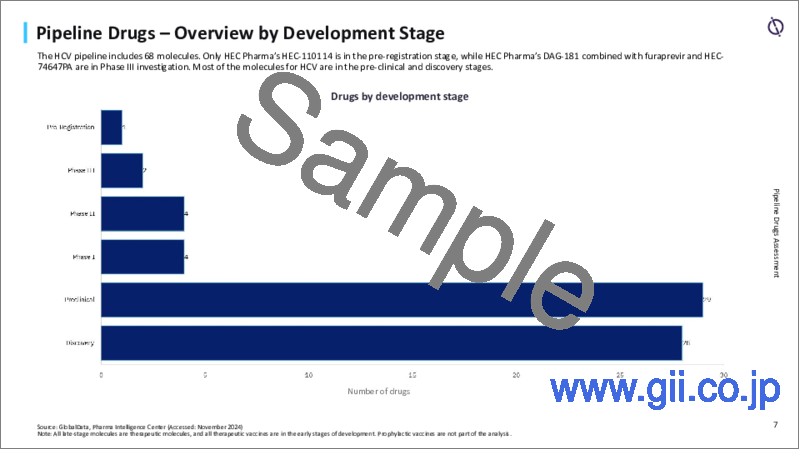

HCVのパイプラインには68の分子があり、1つが登録前、2つがフェーズ3開発中、4つがフェーズII開発中です。

過去10年間で、HCVの臨床試験は866件実施されました。もっとも多くの試験が開始されたのは2014年の196件で、次いで2015年の183件でした。

過去10年間、北米ではパートナーシップが主な取引のタイプでしたが、欧州では買収が最多でした。アジア太平洋と中南米では、ライセンス契約がもっとも一般的でした。

当レポートでは、世界のC型肝炎治療薬市場について調査分析し、疾患情勢、上市済み薬品とパイプライン薬品の評価、現在と将来の競合情勢などを提供しています。

目次

第1章 序文

第2章 主な調査結果

第3章 疾患情勢

- 疾患の概要

- 疫学の概要

- 治療の概要

第4章 上市済み薬品の評価

- 主な上市済み薬品

- 概要:作用機序別

- 概要:分子タイプ別

- 製品プロファイル、売上予測

第5章 価格設定と償還の評価

- 年間治療費

- 価格設定と償還までの時間

第6章 パイプライン薬品の評価

- 中期~後期のパイプライン薬品

- 概要:開発段階別

- 概要:作用機序別

- 概要:分子タイプ別

- 薬品固有のフェーズ移行成功率(PTSR)と承認可能性(LoA)

- 治療領域と適応症固有のPTSRとLoA

第7章 臨床試験の評価

- 過去の概要

- 概要:フェーズ別

- 概要:ステータス別

- 概要:フェーズ別(進行中/計画済みの試験)

- 仮想コンポーネントによる試験

- 試験の概要:地域別

- 単一国/多国間試験:地域別

- スポンサー上位20社と内訳:フェーズ別

- スポンサー上位20社と内訳:ステータス別

- 概要:エンドポイントステータス別

- 概要:人種/民族別

- 登録データ

- 試験施設の上位20ヶ国

- 世界の上位20施設

- 実現可能性分析 - 地理的概要

- 実現可能性分析 - ベンチマークモデル

第8章 取引情勢

- 合併、買収、戦略的提携:地域別

- 近年の合併、買収、戦略的提携

第9章 商業的評価

- 主要市場企業

第10章 将来の市場カタリスト

第11章 付録

This reports provides a data-driven overview of the current and future competitive landscape in Hepatitis C Therapeutics .

GlobalData epidemiologists estimate that there will be 25.16 million diagnosed prevalent cases of Hepatitis C (HCV) infection in 2024, which is expected to increase slightly to 25.84 million diagnosed prevalent cases by 2029.

The HCV treatment landscape has experienced successive waves of revolutionary change and is now dominated by direct-acting antivirals (DAAs).

The HCV pipeline holds 68 molecules, with one asset in the pre-registration stage, two in Phase III development, and four assets in Phase II development.

Over the past decade, 866 clinical trials have been conducted in HCV. The highest number of studies were initiated in 2014 with 196 trials, followed by 2015 with 183 trials.

Over the past decade, partnerships were the primary deal type in North America, whereas acquisitions were most frequent in Europe. In Asia-Pacific (APAC) and South and Central America, licensing agreements were the most common.

Scope

GlobalData's Hepatitis C Therapeutics: Competitive Landscape combines data from the Pharma Intelligence Center with in-house analyst expertise to provide a competitive assessment of the disease marketplace.

Components of the report include -

- Disease Landscape

- Disease Overview

- Epidemiology Overview

- Treatment Overview

- Marketed Products Assessment

- Breakdown by Mechanism of Action, Route of Administration

- Product Profiles with Sales Forecast

- Pricing and Reimbursement Assessment

- Annual Therapy Cost

- Time to Pricing and Time to Reimbursement

- Pipeline Assessment

- Breakdown by Development Stage, Mechanism of Action, Molecule Type, Route of Administration

- Product Profiles with Sales Forecast

- Late-to-mid-stage Pipeline Drugs

- Phase Transition Success Rate and Likelihood of Approval

- Clinical Trials Assessment

- Breakdown of Trials by Phase, Status, Virtual Components, Sponsors, Geography, and Endpoint Status

- Enrolment Analytics, Site Analytics, Feasibility Analysis

- Deals Landscape

- Mergers, Acquisitions, and Strategic Alliances by Region

- Overview of Recent Deals

- Commercial Assessment

- Key Market Players

- Future Market Catalysts

Reasons to Buy

- Develop and design your in-licensing and out-licensing strategies through a review of pipeline products and technologies, and by identifying the companies with the most robust pipeline.

- Develop business strategies by understanding the trends shaping and driving the Hepatitis C Therapeutics market.

- Drive revenues by understanding the key trends, innovative products and technologies, and companies likely to impact the global Hepatitis C Therapeutics market in the future.

- Formulate effective sales and marketing strategies by understanding the competitive landscape and analyzing the performance of various competitors.

- Identify emerging players with potentially strong product portfolios and create effective counter-strategies to gain a competitive advantage.

- Organize your sales and marketing efforts by identifying the market categories that present the maximum opportunities for consolidations, investments, and strategic partnerships.

Table of Contents

1 Table of Contents

1 Preface

- 1.1 Contents

- 1.2 Report Scope

- 1.3 List of Tables and Figures

- 1.4 Abbreviations

2 Key Findings

3 Disease Landscape

- 3.1 Disease Overview

- 3.2 Epidemiology Overview

- 3.3 Treatment Overview

4 Marketed Drugs Assessment

- 4.1 Leading Marketed Drugs

- 4.2 Overview by Mechanism of Action

- 4.3 Overview by Molecule Type

- 4.4 Product Profiles and Sales Forecast

5 Pricing and Reimbursement Assessment

- 5.1 Annual Cost of Therapy

- 5.2 Time to Pricing and Reimbursement

6 Pipeline Drugs Assessment

- 6.1 Mid-to-late-stage Pipeline Drugs

- 6.2 Overview by Development Stage

- 6.3 Overview by Mechanism of Action

- 6.4 Overview by Molecule Type

- 6.5 Drug Specific Phase Transition Success Rate (PTSR) and Likelihood of Approval (LoA)

- 6.6 Therapy Area and Indication-specific PTSR and LoA

7 Clinical Trials Assessment

- 7.1 Historical Overview

- 7.2 Overview by Phase

- 7.3 Overview by Status

- 7.4 Overview by Phase for Ongoing and Planned Trials

- 7.5 Trials with Virtual Components

- 7.6 Overview of Trials by Geography

- 7.7 Single-Country and Multinational Trials by Region

- 7.8 Top 20 Sponsors with Breakdown by Phase

- 7.9 Top 20 Sponsors with Breakdown by Status

- 7.10 Overview by Endpoint Status

- 7.11 Overview by Race and Ethnicity

- 7.12 Enrollment Data

- 7.13 Top 20 countries for Trial Sites

- 7.14 Top 20 Sites Globally

- 7.15 Feasibility Analysis - Geographic Overview

- 7.16 Feasibility Analysis - Benchmark Models

8 Deals Landscape

- 8.1 Mergers, Acquisitions, and Strategic Alliances by Region

- 8.2 Recent Mergers, Acquisitions, and Strategic Alliances

9 Commercial Assessment

- 9.1 Key Market Players

10 Future Market Catalysts

11 Appendix

- 11.1 Methodology

- 11.2 Methodology - Sales Forecast

- 11.3 Methodology - Pricing and Reimbursement

- 11.4 Methodology - PTSR and LoA Analysis

- 11.5 About the Authors

- 11.6 Contact Us

- 11.7 Disclaimer