|

|

市場調査レポート

商品コード

1322942

世界の抗体薬物複合体(ADC)の成長機会、2028年までの予測Global Antibody Drug Conjugate (ADC) Growth Opportunities, Forecast to 2028 |

||||||

|

|

|||||||

|

|||||||

| 世界の抗体薬物複合体(ADC)の成長機会、2028年までの予測 |

|

出版日: 2023年07月17日

発行: Frost & Sullivan

ページ情報: 英文 55 Pages

納期: 即日から翌営業日

|

- 全表示

- 概要

- 目次

革新的なプラットフォーム開発企業とのコラボレーションが成長の可能性を促進

この調査サービスは、世界のADC市場を概観し、2023年から2028年までの6年間の収益予測を提供しています。ADCは、抗体、コンジュゲーションケミストリー、リンカー、ペイロードなどの複数のコンポーネントから構成されます。多くの企業が各構成要素に取り組んでいる一方、ADCのみを開発している企業もあり、市場競争は激しいです。標準的な抗体を上回る標的デリバリー・ビークルの開発により、これらの薬剤の性能が向上し、新たながん治療への可能性が広がっています。新しい技術は、安定性の低さ、忍容性の低さ、有効性の低さ、治療指数の狭さ、ADC製造の課題など、既存のADC技術の欠点に対処しようとしています。

フロスト&サリバンの分析によると、初期の医薬品開発を研究開発業務受託機関(CDMO)/研究開発業務受託機関(CRO)に依存している中小企業は、新規の抗体治療技術を生み出しています。抗体開発企業の多くは、自社での研究開発努力を減らし、パイプラインを強化するために抗体治療製品ラインのライセンシングや買収を増やしています。主要なCDMOはすべて、次世代のADCをサポートするために新たな投資に踏み切っており、このセグメントの競争力を高めています。バイオ医薬品企業は、選択的な腫瘍抗原に対する標的特異性のメリットを享受するためにADCに注力しています。ADCは過去2年間に7件の承認を取得し、成功率を反映しているため、開発者はペイロードの効力を向上させるために強固なアプローチを用いています。

本レポートに含まれるその他の情報は以下の通り:

- 市場動向

- 主要ディスラプター

- 血液腫瘍と固形腫瘍の成長を促進するADCの市場投入品とパイプライン

- 利害関係者が活用できるこの分野の成長機会

目次

戦略的課題

- なぜ成長が難しくなっているのか?

- The Strategic Imperative 8(TM)

- ADC業界における戦略的重要課題トップ3のインパクト

- Growth Pipeline Engine(TM)を支える成長機会

成長環境

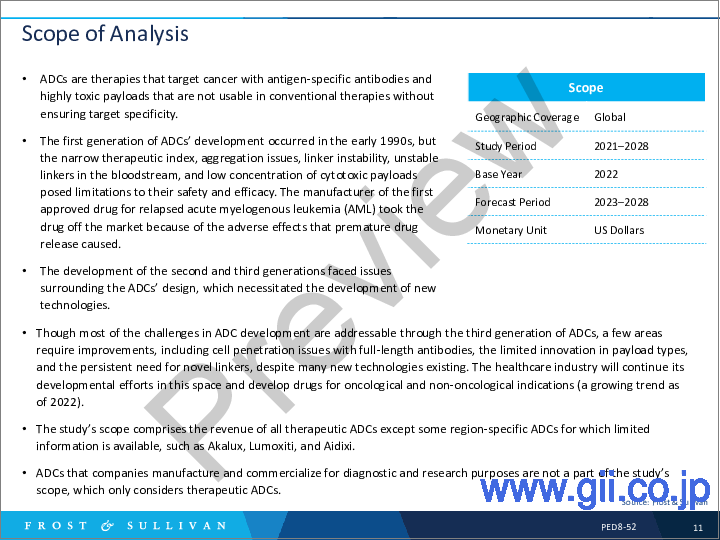

- 分析範囲

- ADC市場ハイライト

- 成長機会:ADC市場

- 成長促進要因

- 成長阻害要因

- 薬物複合体の歴史、進歩、研究段階

- ADC市場の動向

- ADC技術の進化

- ADCのプレシジョン・オンコロジー・アプローチ

- がん領域全体におけるバイオマーカーの応用

- ライフサイクルマネジメント戦略

- ADCの取引と投資見通し

- 注目すべきADCパートナーシップと提携(2022年)

- 注目すべきADCのパートナーシップと提携(2022年および2023年)

- 承認されたADC血液がん

- 承認されたADC固形がん

- 注目すべき後期ADC

収益予測と分析

- 予測の前提条件

- 成長指標

- 収益予測

- 収益予測分析:固形がん(上市済み)

- 収益予測分析:固形がん(パイプライン)

- 収益予測分析:血液がん(上市済み)

- 収益予測分析:血液がん(後期パイプライン)

アクションを起こす企業ADC市場を破壊する企業

- ツブリス幅広い技術プラットフォーム

- LCB:コンジュゲーション技術プラットフォーム

- Synaffix(Lonza):エンド・ツー・エンドのADCサービス

- WuXi Biologics:ADC CRDMO

- メルサナ・セラピューティクス後期ADCパイプラインとプラットフォーム

- イクスダADC開発のためのツールボックス・アプローチ

成長機会ユニバース

- 成長機会1:高精度化学療法のためのADC併用療法

- 成長機会2:CDMOと初期段階のプラットフォームおよびADC開発企業間の戦略的パートナーシップ

- 成長機会3:新規リンカーとコンジュゲーションケミストリー

- 図表一覧

- 免責事項

Collaborations with Innovative Platform Developers will Drive Growth Potential

This research service overviews the global ADC market and provides a 6-year revenue forecast from 2023 to 2028. An ADC comprises multiple components such as the antibody, conjugation chemistry, linker, and payload. Many companies are working on each component while others only develop ADCs, which makes the market highly competitive. The development of targeted delivery vehicles over standard antibodies is improving the performance of these drugs and expanding their potential for treating new cancers. New technologies are trying to address drawbacks of existing ADC technology, such as poor stability, leading to poor tolerability, efficacy, and a narrow therapeutic index and challenging ADC manufacturing.

Frost & Sullivan's analysis shows that small and mid-sized enterprises that rely on contract development and manufacturing organizations (CDMOs)/contract research organizations (CROs) for initial drug development create novel antibody therapeutic technologies. Many antibody developers have been decreasing in-house R&D efforts and increasing in-licensing or acquiring therapeutic antibody product lines to strengthen their pipelines. All major CDMOs are stepping up with new investments to support the next generation of ADC, making the segment more competitive. Biopharmaceutical companies are focusing on ADCs to reap the benefits of target specificity for selective tumor antigens. Developers are using robust approaches to improve payloads' potency as ADCs reflect the success rate in the last two years with seven approvals.

Other information included in the report consists of the following:

- Market trends

- Leading disruptors

- Marketed and pipeline ADC that will drive growth in hematological and solid tumors

- Growth opportunities emerging from this space that stakeholders can leverage

Table of Contents

Strategic Imperatives

- Why Is It Increasingly Difficult to Grow?

- The Strategic Imperative 8™

- The Impact of the Top 3 Strategic Imperatives on the ADC Industry

- Growth Opportunities Fuel the Growth Pipeline Engine™

Growth Environment

- Scope of Analysis

- ADC Market Highlights

- Growth Opportunities: The ADC Market

- Growth Drivers

- Growth Restraints

- Drug Conjugates' History, Progress, and Research Stages

- ADC Market Trends

- ADC Technology Evolution

- Precision Oncology Approaches for ADCs

- Biomarker Application Across the Cancer Continuum

- Life Cycle Management Strategies

- ADC Deals and Investment Outlook

- Notable ADC Partnerships and Collaborations, 2022

- Notable ADC Partnerships and Collaborations, 2022 and 2023

- Approved ADCs: Hematological Cancer

- Approved ADCs: Solid Tumors

- Late-stage ADCs to Watch

Revenue Forecast and Analysis

- Forecast Assumptions

- Growth Metrics

- Revenue Forecast

- Revenue Forecast Analysis: Solid Tumors (Launched)

- Revenue Forecast Analysis: Solid Tumors (Pipeline)

- Revenue Forecast Analysis: Hematological Cancer (Launched)

- Revenue Forecast Analysis: Hematological Cancer (Late-stage Pipeline)

Companies to Action: ADC Market Disruptors

- Tubulis: Broad Spectrum of Technology Platforms

- LCB: Conjugation Technology Platforms

- Synaffix (Lonza): End-to-end ADC Services

- WuXi Biologics: ADC CRDMO

- Mersana Therapeutics: Late-stage ADC Pipeline and Platform

- Iksuda: A Toolbox Approach for ADC Development

Growth Opportunity Universe

- Growth Opportunity 1: ADC Combination Therapies for Precision Chemotherapeutics

- Growth Opportunity 2: Strategic Partnerships between CDMOs and Early-stage Platform and ADC Developers

- Growth Opportunity 3: Novel Linkers and Conjugation Chemistries

- List of Exhibits

- Legal Disclaimer