|

|

市場調査レポート

商品コード

1560792

2型糖尿病の世界市場:2024年~2031年Global Type 2 Diabetes Market - 2024 - 2031 |

||||||

|

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 2型糖尿病の世界市場:2024年~2031年 |

|

出版日: 2024年09月23日

発行: DataM Intelligence

ページ情報: 英文 184 Pages

納期: 即日から翌営業日

|

- 全表示

- 概要

- 目次

レポート概要

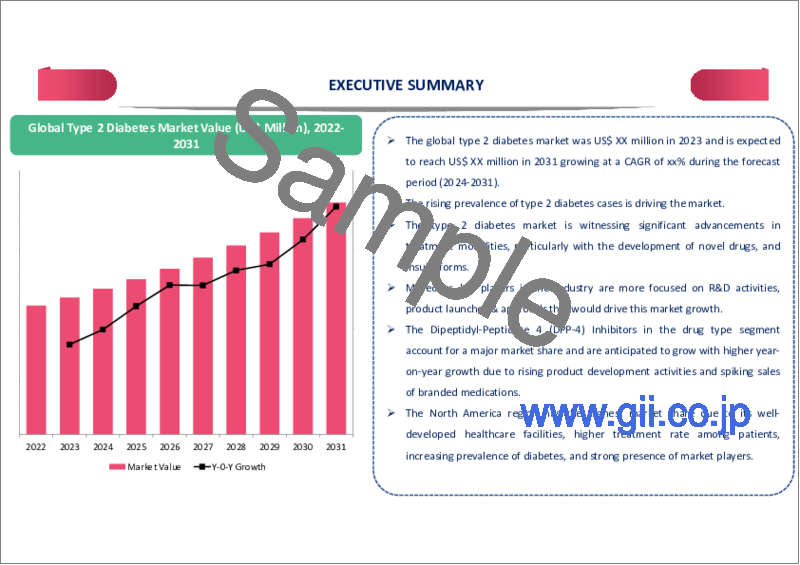

世界の2型糖尿病の市場規模は、2023年に330億7,000万米ドルに達し、2031年には625億9,000万米ドルに達すると予測され、予測期間2024年~2031年のCAGRは8.3%で成長する見込みです。

2型糖尿病は多面的な慢性疾患であり、体内でインスリンが十分に分泌されないか、インスリンを効果的に利用できない場合に発症します。2型糖尿病患者は、インスリンと血糖値を効果的に管理する治療が必要です。

インスリンは膵臓から分泌されるホルモンで、血糖値を調節します。インスリンの量が不足すると、体は摂取した食物からグルコースを吸収するのに苦労します。その結果、血糖値が上昇し、時間の経過とともに血管を傷つけ、体の臓器や神経への酸素や栄養豊富な血液の流れが悪くなります。2型糖尿病患者は、グルコースを処理する体の能力を改善し、長期的な合併症のリスクを軽減するための治療が必要となります。

市場力学:

促進要因

糖尿病有病率の上昇と治療の選択肢の進歩

世界の2型糖尿病市場の需要は、複数の要因によって牽引されています。主な要因の1つは、糖尿病有病率の上昇と治療の選択肢の進歩です。2型糖尿病の発症には、肥満、運動不足、遺伝的素因など、いくつかの要因が関与しています。2型糖尿病に伴う深刻な結果を軽減するためには、早期発見が重要な役割を果たします。糖尿病を早期に発見する最も効果的な方法は、ヘルスケア専門家による定期的な健康診断と血液検査です。

2022年2月のアボットのニュースによると、インドは世界で2番目に糖尿病人口が多く、最近の研究では、この大流行により非伝染性疾患のヘルスケアに大きな混乱が生じていることが示されています。糖尿病患者の最大87%が医療機関への受診回数を減らしており、自宅で血糖測定器を所有しているのは半数以下です。集中的なインスリン治療を受けている成人の2型糖尿病患者の場合、センサー式機器を少なくとも3ヵ月使用することで、平均HbA1c値が8.9%から8%に低下することが調査で示されています。

同様に、2021年、国際糖尿病連合(IDF)は、20歳から79歳の成人の10.5%が糖尿病を患っていると報告しており、これは約5億3,000万人に相当します。この数字は、2045年までに7億8,300万人に増加すると予測されており、成人の約8人に1人に相当し、有病率が46%増加することになります。

さらに、研究開発の継続的な進歩により、SGLT2阻害薬やGLP-1受容体作動薬のような革新的な糖尿病治療薬や投与方法への道が開かれました。これらの新規治療薬は、従来の治療薬に比べて有効性が高く、安全性も改善されています。これらの革新的なソリューションの導入は、患者の転帰を最適化し、2型糖尿病市場の成長を促進すると予想されます。

さらに、業界の主な企業は、2型糖尿病の先進的な治療、臨床試験と製品承認の数の増加、およびこの市場の成長を促進する主要な発展に、より焦点を当てています。例えば、ファイザーは2023年6月、成人の肥満と2型糖尿病(T2DM)の潜在的治療薬として、経口グルカゴン様ペプチド-1受容体作動薬(GLP-1-RA)候補薬ダヌグリプロンの開発を継続すると発表しました。なお、もう一つのGLP-1-RA候補薬であるロチグリプロンについては、臨床開発を中止します。

また、2024年6月、アストラゼネカのファルキシガ(一般名:ダパグリフロジン)は、10歳以上の小児2型糖尿病(T2DM)患者における血糖コントロール強化の目的で、米国食品医薬品局(FDA)より承認を取得しました。今回の承認は、小児の2型糖尿病患者を対象とした第III相臨床試験の良好な成績に基づいています。これまでファルキシガは、成人のT2D患者を対象に、食事療法と運動療法の補助として血糖コントロールの改善に使用することが承認されていました。

抑制要因

高額な治療費、新興国市場における不十分なヘルスケアインフラ、個人の認識不足、規制上の課題などが市場の抑制要因になると予想されます。

市場セグメンテーション

世界の2型糖尿病市場は、薬剤タイプ、ジェンダー、年齢層、投与経路、用途、流通チャネル、地域によって細分化されます。

ジペプチジルペプチダーゼ4(DPP-4)阻害薬セグメントは、世界の2型糖尿病市場シェアの約42.8%を占めています。

予測期間中、ジペプチジルペプチダーゼ4(DPP-4)阻害薬セグメントが最大の市場シェアを占めると予想されます。DPP-4阻害薬はグリプチンとしても知られ、成人の2型糖尿病治療薬としてFDAに承認された経口薬の一種です。FDAが承認したDPP-4阻害薬には、シタグリプチン、サキサグリプチン、リナグリプチン、アログリプチンなどがあります。もう1つのDPP-4阻害薬であるビルダグリプチンは、欧州医薬品庁(EMA)では承認されていますが、FDAでは承認されていません。

これらの薬剤はジペプチジルペプチダーゼ-4(DPP-4)という酵素を阻害することによって作用し、この酵素はインクレチンホルモンのグルカゴン様ペプチド-1(GLP-1)とグルコース依存性インスリン分泌促進ポリペプチド(GIP)を不活性化します。インクレチンホルモンは、経口摂取後のグルコースホメオスタシスを調節する腸内ホルモンです。DPP-4を阻害することにより、これらの薬剤は活性インクレチンのレベルを上昇させ、2型糖尿病における血糖値のコントロールに役立ついくつかの効果をもたらします。

さらに、主要企業の製品上市と承認、糖尿病管理の進歩がこの市場成長の原動力となっています。例えば、2024年1月、Dong-A STは2型糖尿病の治療を目的とした新しい配合剤を発売しましたが、これは糖尿病管理における重要な進歩です。この合剤(FDC)には、テネリグリプチン、ダパグリフロジン、メトホルミンの3つの有効成分が配合されています。この配合剤は、2型糖尿病患者、特にHbA1c値が高く、高血圧や心血管疾患などの合併症を有する患者の血糖コントロールを改善するように設計されています。

同様に2023年10月、ザイダスライフサイエンスは、25mg、50mg、100mgの用量を有するZITUVIO(シタグリプチン)錠の新薬承認申請(NDA)が米国食品医薬品局(FDA)により承認されたと発表しました。ZITUVIOは、ジペプチジルペプチダーゼ-4(DPP-4)阻害薬に分類されるシタグリプチンを含有しています。本剤は、2型糖尿病と診断された成人患者を対象に、食事療法および運動療法と併用して血糖コントロールの改善を図ります。

また、グレンマークは2022年4月、DPP4阻害剤テネリグリプチンとチアゾリジンジオン(TZD)系薬剤ピオグリタゾンの新規合剤(FDC)を発売しました。ジータ・プラス・ピオ」の製品名で販売されているこのFDCは、テネリグリプチン20mgとピオグリタゾン15mgを含有し、1日1回服用します。インドでは、成人におけるコントロール不能な2型糖尿病の治療薬として、DPP4とグリタゾンの配合剤が唯一販売されています。

地域別の市場シェア

北米は、世界の2型糖尿病市場シェアの約44.5%を占める

北米では、2型糖尿病の罹患率が上昇していることが市場成長の主な要因となっており、予測期間中、北米が最大の市場シェアを占めると予想されます。CDCによると、2021年には全年齢で約3,840万人(米国人口の11.6%)が糖尿病と診断されました。18歳以上の成人では、この数字は3,810万人に上り、米国成人の14.7%を占めます。

注目すべきは、この年齢層の870万人の成人が、糖尿病の検査基準を満たしても、自分の状態を知らなかったか、報告しなかったことです。これは、米国成人の3.4%、糖尿病患者の22.8%を占めます。成人の糖尿病有病率は年齢とともに増加し、65歳以上では29.2%に達します。

さらに、肥満率の上昇、技術の進歩、政府の取り組みと支援、研究開発がこの市場開拓の原動力となっています。さらに、多くの主要企業が進出していること、ヘルスケアのインフラが整備されていること、製品の上市と承認がこの地域の市場成長を後押ししています。例えば、2023年6月、米国食品医薬品局は、食事療法と運動療法を含む治療計画の一環として、10歳以上の2型糖尿病の小児への使用について、ジャーディアンス(エンパグリフロジン)とシンジャーディ(エンパグリフロジンと塩酸メトホルミン)を承認しました。これにより、小児の2型糖尿病管理における新しいクラスの経口薬が導入されることになります。

また、2023年1月、セラコスバイオは、経口ナトリウム・グルコース共輸送体2(SGLT2)阻害薬であるBrenzavvy(一般名:ベキサグリフロジン)が米国食品医薬品局(FDA)より承認されたと発表しました。Brenzavvyは、成人の2型糖尿病患者において、血糖コントロールを強化するための食事療法および運動療法の補助薬として適応されます。1型糖尿病の患者や糖尿病性ケトアシドーシスの治療には推奨されません。

加えて、主要企業は2型糖尿病治療により注力しており、革新的な新薬の発売がこの市場の成長を後押ししています。例えば、2023年8月、Dr. Reddy's Laboratoriesは米国市場でSaxagliptin and Metformin Hydrochloride Extended-Release Tabletsを発売しました。この製品は、米国食品医薬品局(USFDA)から承認を受けているコンビグライズXR(サキサグリプチンおよびメトホルミン塩酸塩徐放製剤)錠のジェネリック医薬品です。

サキサグリプチンおよびメトホルミン塩酸塩徐放錠は、サキサグリプチンおよびメトホルミンの併用治療が適切と判断される成人2型糖尿病患者において、食事療法および運動療法の補助として血糖コントロールを強化する適応を有します。錠剤の強さは、2.5mg/1000mgが60錠入り、5mg/500mgが30錠入り、5mg/1000mgが30錠入りです。

同様に、2022年5月、米国食品医薬品局(FDA)は、イーライリリー・アンド・カンパニーのムンジャロ(チルゼパチド)注射剤を、GIP(グルコース依存性インスリン分泌促進ポリペプチド)およびGLP-1(グルカゴン様ペプチド-1)受容体作動薬として作用する週1回投与の治療薬として承認しました。成人の2型糖尿病患者を対象に、食事療法や運動療法と並行して血糖コントロールを強化する目的で使用されます。ただし、膵炎の既往歴のある患者を対象とした試験は行われておらず、糖尿病患者を対象とした承認はされていません。

目次

第1章 調査手法と調査範囲

第2章 定義と概要

第3章 エグゼクティブサマリー

第4章 市場力学

- 影響要因

- 促進要因

- 糖尿病の有病率の上昇と治療法の進歩

- 抑制要因

- 高い治療費

- 機会

- 影響分析

- 促進要因

第5章 産業分析

- ポーターのファイブフォース分析

- サプライチェーン分析

- 価格分析

- 規制分析

第6章 薬剤タイプ別

- ジペプチジルペプチダーゼ4(DPP-4)阻害薬

- サキサグリプチン

- シタグリプチン

- リナグリプチン

- アログリプチン

- α-グルコシダーゼ阻害薬

- アカルボース

- ミグリトール

- グルカゴン様ペプチド-1(GLP-1)受容体作動薬

- デュラグルチド

- エキセナチド

- リラグルチド

- リキセナチド

- セマグルチド

- ナトリウムグルコーストランスポーター2(SGLT2)阻害薬

- カナグリフロジン

- ダパグリフロジン

- エンパグリフロジン

- エルトゥグリフロジン

- メグリチニド

- レパグリニド

- ナテグリニド

- スルホニル尿素

- グリピジド

- グリメピリド

- グリブリド

- チアゾリジン系薬剤

- ロシグリタゾン

- ピオグリタゾン

- ビグアナイド薬(メトホルミン)

- 胆汁酸分泌抑制薬(コレセベラム)

- アミリン模倣薬(プラムリンタイド)

第7章 ジェンダー別

- 男性

- 女性

第8章 年齢層別

- 19歳以下

- 20歳~65歳

- 65歳超

第9章 投与経路別

- 経口

- 非経口

第10章 用途別

- 血糖コントロール

- 心血管安全性

- 低血糖回避

- その他

第11章 流通チャネル別

- 院内薬局

- 小売薬局

- オンライン薬局

第12章 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋

- 中東・アフリカ

第13章 競合情勢

- 競合シナリオ

- 市況/シェア分析

- M&A分析

第14章 企業プロファイル

- Abbott

- 会社概要

- 製品ポートフォリオと説明

- 財務概要

- 主な発展

- Medtronic

- Dexcom, Inc.

- AstraZeneca

- TheracosBio, LLC

- Boehringer Ingelheim International GmbH

- Eli Lilly and Company.

- Novo Nordisk A/S

- Merck & Co., Inc.,

- Pfizer Inc

第15章 付録

Report Overview

The Global Type 2 Diabetes Market reached US$ 33.07 billion in 2023 and is expected to reach US$ 62.59 billion by 2031 growing with a CAGR of 8.3% during the forecast period 2024-2031.

Type 2 diabetes is a multifaceted chronic condition that arises when the body either fails to produce sufficient insulin or cannot utilize it effectively. Individuals with type 2 diabetes require treatment to manage their insulin and blood sugar levels effectively.

Insulin is a hormone produced by the pancreas that regulates blood glucose levels. When there is an insufficient amount of insulin, the body struggles to absorb glucose from the food consumed. This leads to elevated blood glucose levels, which, over time, can harm blood vessels and diminish the flow of oxygen and nutrient-rich blood to the body's organs and nerves. Individuals with type 2 diabetes may require treatment to improve their body's ability to process glucose and to reduce the risk of long-term complications.

Market Dynamics: Drivers

Rising prevalence of diabetes and advancements in treatment options

The demand for the global type 2 diabetes market is driven by multiple factors. One of the primary factors is the rising prevalence of diabetes and advancements in treatment options. Several factors contribute to the development of type 2 diabetes, including obesity, physical inactivity, and genetic predisposition. Early detection plays a crucial role in mitigating the severe consequences associated with type 2 diabetes. The most effective way to identify diabetes at an early stage is through regular health check-ups and blood tests conducted by a healthcare professional.

As per Abbott news in February 2022, India has the second-largest diabetes population globally, with recent studies indicating significant disruptions in healthcare for non-communicable diseases due to the pandemic. Up to 87% of individuals with diabetes have reduced their visits to healthcare providers, and less than half own a blood glucose monitoring device at home. For adults with type 2 diabetes who are on intensive insulin therapy, research has shown that using sensor-based devices for at least three months can lower average HbA1c levels from 8.9% to 8%.

Similarly, in 2021, the International Diabetes Federation (IDF) reported that 10.5% of adults aged 20 to 79 were living with diabetes, which translates to approximately 530 million individuals. This figure is anticipated to rise to 783 million by 2045, equating to about 1 in 8 adults, marking a 46% increase in prevalence.

Furthermore, continuous advancements in research and development have paved the way for innovative diabetes medications and delivery methods, such as SGLT2 inhibitors and GLP-1 receptor agonists. These novel therapies demonstrate enhanced efficacy and improved safety profiles compared to traditional treatments. The introduction of these innovative solutions is anticipated to optimize patient outcomes and propel the growth of the type 2 diabetes market.

Moreover, key players in the industry more focus on the advanced treatments for type 2 diabetes and the rising number of clinical trials & product approvals, and key developments that would drive this market growth. For instance, in June 2023, Pfizer announced that it will continue advancing the development of its oral glucagon-like peptide-1 receptor agonist (GLP-1-RA) candidate, danuglipron for the potential treatment of obesity and type 2 diabetes mellitus (T2DM) in adults. The company will discontinue the clinical development of its other GLP-1-RA candidate, lotiglipron.

Also, in June 2024, AstraZeneca's Farxiga (dapagliflozin) received approval from the U.S. Food and Drug Administration (FDA) to enhance glycemic control in pediatric patients aged 10 years and older with type 2 diabetes (T2D). This approval is based on favorable outcomes from the pediatric T2D now in the Phase III trial. Previously, Farxiga was approved for use in adults with T2D as an adjunct to diet and exercise for improving glycemic control.

Restraints

Factors such as high treatment costs, inadequate healthcare infrastructure in developing countries, lack of awareness among individuals, and regulatory challenges are expected to hamper the market.

Market Segment Analysis

The global type 2 diabetes market is segmented based on drug type, gender, age group, route of administration, application, distribution channels, and region.

The dipeptidyl-peptidase 4 (DPP-4) inhibitors segment accounted for approximately 42.8% of the global type 2 diabetes market share.

The dipeptidyl-peptidase 4 (DPP-4) Inhibitors segment is expected to hold the largest market share over the forecast period. DPP-4 inhibitors, also known as gliptins, are a class of oral medications approved by the FDA for treating type 2 diabetes in adults. The FDA-approved DPP-4 inhibitors include sitagliptin, saxagliptin, linagliptin, and alogliptin. Vildagliptin, another DPP-4 inhibitor, has been approved by the European Medicines Agency (EMA) but not the FDA.

These drugs work by inhibiting the enzyme dipeptidyl peptidase-4 (DPP-4), which inactivates the incretin hormones glucagon-like peptide-1 (GLP-1) and glucose-dependent insulinotropic polypeptide (GIP). Incretin hormones are gut hormones responsible for regulating glucose homeostasis after oral food intake. By inhibiting DPP-4, these drugs increase the levels of active incretins, leading to several effects that help control blood glucose levels in type 2 diabetes.

Moreover, key player's product launches & approvals, and advancements in diabetes management drive this market growth. For instance, in January 2024, Dong-A ST launched a new combination drug aimed at treating type 2 diabetes, which is a significant advancement in diabetes management. This fixed-dose combination (FDC) drug combines three active ingredients: Teneligliptin, Dapagliflozin, and Metformin. This combination is designed to improve glycemic control in patients with type 2 diabetes, particularly those with high HbA1c levels and other co-morbidities such as hypertension or cardiovascular issues.

Similarly, in October 2023, Zydus Lifesciences Limited announced that the U.S. Food and Drug Administration (FDA) has approved its New Drug Application (NDA) for ZITUVIO (Sitagliptin) tablets, available in dosages of 25 mg, 50 mg, and 100 mg. ZITUVIO contains sitagliptin, which is classified as a dipeptidyl peptidase-4 (DPP-4) inhibitor. It is indicated to be used alongside diet and exercise to help improve glycemic control in adults diagnosed with type 2 diabetes mellitus.

Also, in April 2022, Glenmark Pharmaceuticals introduced a novel fixed-dose combination (FDC) of the DPP4 inhibitor Teneligliptin and the thiazolidinedione (TZD) Pioglitazone. This FDC, marketed under the brand name Zita Plus Pio, contains Teneligliptin 20 mg and Pioglitazone 15 mg, to be taken once daily. It is the only available DPP4 and glitazone combination in India for managing uncontrolled type 2 diabetes in adults.

Market Geographical Share

North America accounted for approximately 44.5% of the global type 2 diabetes market share.

North America region is expected to hold the largest market share over the forecast period owing to the rising incidence of type 2 diabetes is a primary driver of market growth in North America. According to the CDC, in 2021, approximately 38.4 million individuals of all ages, representing 11.6% of the U.S. population, were diagnosed with diabetes. Among adults aged 18 and older, this figure rose to 38.1 million, accounting for 14.7% of all U.S. adults.

Notably, 8.7 million adults in this age group met the laboratory criteria for diabetes but were either unaware of their condition or did not report it, which constitutes 3.4% of all U.S. adults and 22.8% of those with diabetes. The prevalence of diabetes among adults increases with age, reaching 29.2% for those aged 65 and older.

Furthermore, rising obesity rates, technological advancements, government initiatives and support, and research and development drive this market growth. Moreover, a major number of key player's presence, well-advanced healthcare infrastructure, and product launches & approvals would drive this market growth in this region. For instance, in June 2023, the U.S. Food and Drug Administration approved Jardiance (empagliflozin) and Synjardy (empagliflozin and metformin hydrochloride) for use in children aged 10 and older with type 2 diabetes, as part of a treatment plan that includes diet and exercise. This marks the introduction of a new class of oral medications for pediatric type 2 diabetes management.

Also, in January 2023, TheracosBio announced that the U.S. Food and Drug Administration (FDA) has approved Brenzavvy (bexagliflozin), an oral sodium-glucose cotransporter 2 (SGLT2) inhibitor. Brenzavvy is indicated as an adjunct to diet and exercise to enhance glycemic control in adults with type 2 diabetes. It is not recommended for individuals with type 1 diabetes mellitus or the treatment of diabetic ketoacidosis.

In addition, key players more focus on the treatment for type-2, and innovative launches help to drive this market growth. For instance, in August 2023, Dr. Reddy's Laboratories launched Saxagliptin and Metformin Hydrochloride Extended-Release Tablets in the U.S. market. This product is a generic equivalent of Kombiglyze XR (saxagliptin and metformin hydrochloride extended-release) tablets, which has received approval from the U.S. Food and Drug Administration (USFDA).

The Saxagliptin and Metformin Hydrochloride Extended-Release Tablets are indicated as an adjunct to diet and exercise to enhance glycemic control in adults with type 2 diabetes mellitus when treatment with both saxagliptin and metformin is deemed appropriate. The tablets are available in the following strengths: 2.5 mg/1000 mg in bottles of 60, 5 mg/500 mg, and 5 mg/1000 mg in bottles of 30 each.

Similarly, in May 2022, the U.S. Food and Drug Administration (FDA) approved Mounjaro (tirzepatide) injection from Eli Lilly and Company as a once-weekly treatment that acts as a GIP (glucose-dependent insulinotropic polypeptide) and GLP-1 (glucagon-like peptide-1) receptor agonist. It is indicated for use alongside diet and exercise to enhance glycemic control in adults with type 2 diabetes. However, Mounjaro has not been tested in individuals with a history of pancreatitis and is not approved for patients with type diabetes mellitus.

Market Segmentation

By Drug Type

Dipeptidyl-Peptidase 4 (DPP-4) Inhibitors

Saxagliptin

Sitagliptin

Linagliptin

Alogliptin

Alpha-glucosidase Inhibitors

Acarbose

Miglitol

Glucagon-Like Peptide-1 (GLP-1) Receptor Agonists)

Dulaglutide

Exenatide

Liraglutide

Lixisenatide

Semaglutide

Sodium-glucose Transporter 2 (SGLT2) Inhibitors

Canagliflozin

Dapagliflozin

Empagliflozin

Ertugliflozin

Meglitinides

Repaglinide

Nateglinide

Sulfonylureas

Glipizide

Glimepiride

Glyburide

Thiazolidinediones

Rosiglitazone

Pioglitazone

Biguanides (Metformin)

Bile Acid sequestrants (Colesevelam)

Amylin Mimetics (Pramlintide)

By Gender

Male

Female

By Age Group

Up to 19 years

20 - 65 years

Above 65 years

By Route of Administration

Oral

Parenteral

By Application

Glycemic Control

Cardiovascular Safety

Hypoglycemia Avoidance

Others

By Distribution Channel

Hospital Pharmacies

Retail Pharmacies

Online Pharmacies

By Region

North America

The U.S.

Canada

Mexico

Europe

Germany

U.K.

France

Spain

Italy

Rest of Europe

South America

Brazil

Argentina

The rest of South America

Asia-Pacific

China

India

Japan

South Korea

Rest of Asia-Pacific

Middle East and Africa

Market Competitive Landscape

The major global players in the type 2 diabetes market include Abbott, Medtronic, Dexcom, Inc., AstraZeneca, TheracosBio, LLC, Boehringer Ingelheim International GmbH, Eli Lilly and Company., Novo Nordisk A/S, Merck & Co., Inc., and Pfizer Inc. among others.

Key Developments

In July 2024, Novo Nordisk announced that the U.S. Food and Drug Administration (FDA) has issued a Complete Response Letter (CRL) regarding the Biologics License Application for once-weekly basal insulin icodec, intended for the treatment of diabetes mellitus. Insulin icodec, marketed as Awiqli is already approved in the EU, Canada, Australia, Japan, and Switzerland for both type 1 and type 2 diabetes, and in China specifically for type 2 diabetes.

In June 2024, Dexcom, Inc. announced a major advancement in product accessibility for individuals managing Type 2 diabetes (T2D) with basal insulin injections. The company, which has been at the forefront of CGM technology for 25 years, has secured access to its Dexcom ONE sensor for approximately 100,000 T2D patients in France. The reimbursement guidelines allow individuals over the age of two who are on non-intensified insulin therapy (fewer than three injections daily) and have inadequate glycemic control (HbA1c >= 8%) to benefit from Dexcom's innovative technology.

Why Purchase the Report?

To visualize the global type 2 diabetes market segmentation based on drug type, gender, age group, route of administration, application, distribution channels, and region and understand key commercial assets and players.

Identify commercial opportunities by analyzing trends and co-development.

Excel data sheet with numerous data points of the type 2 diabetes market with all segments.

PDF report consists of a comprehensive analysis after exhaustive qualitative interviews and an in-depth study.

Product mapping is available in Excel consisting of key products of all the major players.

The global type 2 diabetes market report would provide approximately 82 tables, 91 figures, and 184 pages.

Target Audience 2024

Manufacturers/ Buyers

Industry Investors/Investment Bankers

Research Professionals

Emerging Companies

Table of Contents

1. Methodology and Scope

- 1.1. Research Methodology

- 1.2. Research Objective and Scope of the Report

2. Definition and Overview

3. Executive Summary

- 3.1. Snippet by Drug Type

- 3.2. Snippet by Gender

- 3.3. Snippet by Age Group

- 3.4. Snippet by Route of Administration

- 3.5. Snippet by Application

- 3.6. Snippet by Distribution Channels

- 3.7. Snippet by Region

4. Dynamics

- 4.1. Impacting Factors

- 4.1.1. Drivers

- 4.1.1.1. Rising Prevalence of Diabetes and Advancements in Treatment Options

- 4.1.2. Restraints

- 4.1.2.1. High Treatment Costs

- 4.1.3. Opportunity

- 4.1.4. Impact Analysis

- 4.1.1. Drivers

5. Industry Analysis

- 5.1. Porter's Five Force Analysis

- 5.2. Supply Chain Analysis

- 5.3. Pricing Analysis

- 5.4. Regulatory Analysis

6. By Drug Type

- 6.1. Introduction

- 6.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Drug Type

- 6.1.2. Market Attractiveness Index, By Drug Type

- 6.2. Dipeptidyl-Peptidase 4 (DPP-4) Inhibitors *

- 6.2.1. Introduction

- 6.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

- 6.2.3. Saxagliptin

- 6.2.4. Sitagliptin

- 6.2.5. Linagliptin

- 6.2.6. Alogliptin

- 6.3. Alpha-glucosidase Inhibitors

- 6.3.1. Acarbose

- 6.3.2. Miglitol

- 6.4. Glucagon-Like Peptide-1 (GLP-1) Receptor Agonists)

- 6.4.1. Dulaglutide

- 6.4.2. Exenatide

- 6.4.3. Liraglutide

- 6.4.4. Lixisenatide

- 6.4.5. Semaglutide

- 6.5. Sodium-glucose Transporter 2 (SGLT2) Inhibitors

- 6.5.1. Canagliflozin

- 6.5.2. Dapagliflozin

- 6.5.3. Empagliflozin

- 6.5.4. Ertugliflozin

- 6.6. Meglitinides

- 6.6.1. Repaglinide

- 6.6.2. Nateglinide

- 6.7. Sulfonylureas

- 6.7.1. Glipizide

- 6.7.2. Glimepiride

- 6.7.3. Glyburide

- 6.8. Thiazolidinediones

- 6.8.1. Rosiglitazone

- 6.8.2. Pioglitazone

- 6.9. Biguanides (Metformin)

- 6.10. Bile Acid sequestrants (Colesevelam)

- 6.11. Amylin Mimetics (Pramlintide)

7. By Gender

- 7.1. Introduction

- 7.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Gender

- 7.1.2. Market Attractiveness Index, By Gender

- 7.2. Male *

- 7.2.1. Introduction

- 7.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

- 7.3. Female

8. By Age Group

- 8.1. Introduction

- 8.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Age Group

- 8.1.2. Market Attractiveness Index, By Age Group

- 8.2. Up to 19 years*

- 8.2.1. Introduction

- 8.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

- 8.3. 20 - 65 years

- 8.4. Above 65 years

9. By Route of Administration

- 9.1. Introduction

- 9.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Route of Administration

- 9.1.2. Market Attractiveness Index, By Route of Administration

- 9.2. Oral*

- 9.2.1. Introduction

- 9.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

- 9.3. Parenteral

10. By Application

- 10.1. Introduction

- 10.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

- 10.1.2. Market Attractiveness Index, By Application

- 10.2. Glycemic Control *

- 10.2.1. Introduction

- 10.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

- 10.3. Cardiovascular Safety

- 10.4. Hypoglycemia Avoidance

- 10.5. Others

11. By Distribution Channels

- 11.1. Introduction

- 11.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Distribution Channels

- 11.1.2. Market Attractiveness Index, By Distribution Channels

- 11.2. Hospital Pharmacies *

- 11.2.1. Introduction

- 11.2.2. Market Size Analysis and Y-o-Y Growth Analysis (%)

- 11.3. Retail Pharmacies

- 11.4. Online Pharmacies

12. By Region

- 12.1. Introduction

- 12.1.1. Market Size Analysis and Y-o-Y Growth Analysis (%), By Region

- 12.1.2. Market Attractiveness Index, By Region

- 12.2. North America

- 12.2.1. Introduction

- 12.2.2. Key Region-Specific Dynamics

- 12.2.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Drug Type

- 12.2.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Gender

- 12.2.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Age Group

- 12.2.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Route of Administration

- 12.2.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

- 12.2.8. Market Size Analysis and Y-o-Y Growth Analysis (%), By Distribution Channels

- 12.2.9. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

- 12.2.9.1. The U.S.

- 12.2.9.2. Canada

- 12.2.9.3. Mexico

- 12.3. Europe

- 12.3.1. Introduction

- 12.3.2. Key Region-Specific Dynamics

- 12.3.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Drug Type

- 12.3.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Gender

- 12.3.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Age Group

- 12.3.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Route of Administration

- 12.3.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

- 12.3.8. Market Size Analysis and Y-o-Y Growth Analysis (%), By Distribution Channels

- 12.3.9. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

- 12.3.9.1. Germany

- 12.3.9.2. U.K.

- 12.3.9.3. France

- 12.3.9.4. Spain

- 12.3.9.5. Italy

- 12.3.9.6. Rest of Europe

- 12.4. South America

- 12.4.1. Introduction

- 12.4.2. Key Region-Specific Dynamics

- 12.4.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Drug Type

- 12.4.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Gender

- 12.4.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Age Group

- 12.4.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Route of Administration

- 12.4.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

- 12.4.8. Market Size Analysis and Y-o-Y Growth Analysis (%), By Distribution Channels

- 12.4.9. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

- 12.4.9.1. Brazil

- 12.4.9.2. Argentina

- 12.4.9.3. Rest of South America

- 12.5. Asia-Pacific

- 12.5.1. Introduction

- 12.5.2. Key Region-Specific Dynamics

- 12.5.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Drug Type

- 12.5.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Gender

- 12.5.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Age Group

- 12.5.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Route of Administration

- 12.5.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

- 12.5.8. Market Size Analysis and Y-o-Y Growth Analysis (%), By Distribution Channels

- 12.5.9. Market Size Analysis and Y-o-Y Growth Analysis (%), By Country

- 12.5.9.1. China

- 12.5.9.2. India

- 12.5.9.3. Japan

- 12.5.9.4. South Korea

- 12.5.9.5. Rest of Asia-Pacific

- 12.6. Middle East and Africa

- 12.6.1. Introduction

- 12.6.2. Key Region-Specific Dynamics

- 12.6.3. Market Size Analysis and Y-o-Y Growth Analysis (%), By Drug Type

- 12.6.4. Market Size Analysis and Y-o-Y Growth Analysis (%), By Gender

- 12.6.5. Market Size Analysis and Y-o-Y Growth Analysis (%), By Age Group

- 12.6.6. Market Size Analysis and Y-o-Y Growth Analysis (%), By Route of Administration

- 12.6.7. Market Size Analysis and Y-o-Y Growth Analysis (%), By Application

- 12.6.8. Market Size Analysis and Y-o-Y Growth Analysis (%), By Distribution Channels

13. Competitive Landscape

- 13.1. Competitive Scenario

- 13.2. Market Positioning/Share Analysis

- 13.3. Mergers and Acquisitions Analysis

14. Company Profiles

- 14.1. Abbott *

- 14.1.1. Company Overview

- 14.1.2. Product Portfolio and Description

- 14.1.3. Financial Overview

- 14.1.4. Key Developments

- 14.2. Medtronic

- 14.3. Dexcom, Inc.

- 14.4. AstraZeneca

- 14.5. TheracosBio, LLC

- 14.6. Boehringer Ingelheim International GmbH

- 14.7. Eli Lilly and Company.

- 14.8. Novo Nordisk A/S

- 14.9. Merck & Co., Inc.,

- 14.10. Pfizer Inc (*LIST NOT EXHAUSTIVE)

15. Appendix

- 15.1. About Us and Services

- 15.2. Contact Us