|

|

市場調査レポート

商品コード

1576912

抗体薬物複合体 (ADC):市場規模、対象人口、競合情勢、市場予測 (2034年)Antibody Drug Conjugates Market Size, Target Population, Competitive Landscape & Market Forecast - 2034 |

||||||

|

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 抗体薬物複合体 (ADC):市場規模、対象人口、競合情勢、市場予測 (2034年) |

|

出版日: 2024年01月01日

発行: DelveInsight

ページ情報: 英文 120 Pages

納期: 2~10営業日

|

- 全表示

- 概要

- 図表

- 目次

抗体薬物複合体 (ADC) 市場

米国FDA (食品医薬品局) は合計13種類のADCを承認しており、最初に承認されたADCはMYLOTARGでした。しかしその後、2017年にMYLOTARGは、その後の確認試験で臨床的有用性が確認できず、早期死亡の多発など安全性の懸念が示されたため、自主的に市場から撤退しました。

抗体薬物複合体市場の発展は世界な取り組みであり、世界中の企業が多大な資源を投入しています。現在、約200種類以上のADCが前臨床・臨床開発のさまざまな段階にあり、この分野への関心の高さと可能性を示しています。

抗体薬物複合体市場には特定の主要企業が存在します。Roche、Takeda、Gilead Sciences、Pfizer、GlaxoSmithKline、Daiichi Sankyo/AstraZenecaなどです。Daiichi Sankyoは抗体薬物複合体の新時代をリードすると期待されています。

最近のASCO2024で、AbbVieは革新的なADCプラットフォームから新しいデータを発表し、3つの異なるADC、すなわち固形がんにおけるABBV-706、テリソツズマブ・ベドチン、ABBV-400のデータを紹介しました。

ASCO2024の後期セッションで、GSKはDREAMM-8試験の注目すべき結果を発表しましたが、これはGSKが2022年末にBLENREPの米国市場からの撤退を決定したことを考慮したものです。新たなデータは、BLENREPの市場再導入を支持する可能性があります。多発性骨髄腫の第二選択治療薬 (セカンドライン) 以上を対象としたDREAMM-7/8試験に基づく米国、EU、日本での規制決定と、多発性骨髄腫を対象としたDREAMM-8試験に基づく承認申請が2025年に予定されています。

当レポートでは、世界の抗体薬物複合体 (ADC) 市場について分析し、過去の推移や現在の競合情勢、世界主要7ヶ国 - 米国、欧州主要4ヶ国 (EU4:ドイツ、フランス、イタリア、スペイン)・英国、日本 - の市場動向などを詳細に調査しています。

当レポートではまた、現在の治療法や新たな薬剤、個々の治療法の市場シェア、2020年から2034年までの主要7ヶ国の過去・将来の市場規模 (2020~2034年) などを調査・予測しています。また、現在のADCの治療法/アルゴリズム、アンメットメディカルニーズも網羅し、最適な治療機会を発掘し、市場の可能性を評価します。

分析対象地域

- 米国

- EU4 (ドイツ、フランス、イタリア、スペイン)、英国

- 日本

- 調査期間:2020年~2034年

目次

第1章 重要な洞察

第2章 分析概要

第3章 抗体薬物複合体 (ADC):エグゼクティブサマリー

第4章 主な出来事

第5章 抗体薬物複合体 (ADC):市場概要

- 抗体薬物複合体 (ADC) の市場シェア:クラス別 (%、2023年)

- 抗体薬物複合体 (ADC) の市場シェア:クラス別 (%、2034年)

第6章 背景と概要

第7章 対象人口

第8章 抗体薬物複合体 (ADC) の上市済み製品

- 主な競合企業

- 製品概要

- 規制のマイルストーン

- その他の開発活動

- 進行中の臨床開発

- 安全性と効能

第9章 抗体薬物複合体 (ADC) の新たな治療法

- 主な競合企業

- 製品説明

- その他の開発活動

- 臨床開発

- 安全性と効能

第10章 抗体薬物複合体 (ADC):主要7ヶ国の分析

- 主な調査結果

- 市場見通し

- 主要な市場予測の前提条件

- 主要7ヶ国における抗体薬物複合体 (ADC) の総市場規模

- 主要7ヶ国における抗体薬物複合体 (ADC) の市場規模:治療薬別

- 主要7ヶ国における抗体薬物複合体 (ADC) の市場規模:適応症別

- 米国市場

- 米国における抗体薬物複合体 (ADC) の総市場規模

- 米国における抗体薬物複合体 (ADC) の市場規模 :治療薬別

- EU4・英国市場

- EU4・英国における抗体薬物複合体 (ADC) の総市場規模

- EU4・英国における抗体薬物複合体 (ADC) の市場規模:治療薬別

- 日本市場

- 日本における抗体薬物複合体 (ADC) の総市場規模

- 日本における抗体薬物複合体 (ADC) の市場規模:治療薬別

第11章 アンメットニーズ

第12章 SWOT分析

第13章 KOLの見解

第14章 市場アクセスと償還

- 米国

- EU4・英国

- ドイツ

- フランス

- イタリア

- スペイン

- 英国

- 日本

第15章 付録

第16章 DelveInsightのサービス内容

第17章 免責事項

第18章 DelveInsightについて

List of Tables

- Table 1: Target Population in the 7MM (2020-2034)

- Table 2: Marketed Drug Key cross

- Table 3: Product 1, Clinical Trial Description, 2024

- Table 4: Product 2, Clinical Trial Description, 2024

- Table 5: Emerging Drug Key cross

- Table 6: Product 1, Clinical Trial Description, 2024

- Table 7: Product 2, Clinical Trial Description, 2024

- Table 8: Total Antibody Drug Conjugates (ADC) Market Size in the 7MM (2020-2034)

- Table 9: Antibody Drug Conjugates (ADC) Market Size by Therapies in the 7MM (2020-2034)

- Table 10: Antibody Drug Conjugates (ADC) Market Size by Indication in the 7MM (2020-2034)

- Table 11: Total Antibody Drug Conjugates (ADC) Market Size in the United States (2020-2034)

- Table 12: Antibody Drug Conjugates (ADC) Market Size by Therapies in the United States (2020-2034)

- Table 13: Total Antibody Drug Conjugates (ADC) Market Size in EU4 and the UK (2020-2034)

- Table 14: Antibody Drug Conjugates (ADC) Market Size by Therapies in EU4 and the UK (2020-2034)

- Table 15: Total Antibody Drug Conjugates (ADC) Market Size in Japan (2020-2034)

- Table 16: Antibody Drug Conjugates (ADC) Market Size by Therapies in Japan (2020-2034)

List of Figures

- Figure 1: Target Population in the 7MM (2020-2034)

- Figure 2: Total Antibody Drug Conjugates (ADC) Market Size in the 7MM (2020-2034)

- Figure 3: Antibody Drug Conjugates (ADC) Market Size by Therapies in the 7MM (2020-2034)

- Figure 4: Antibody Drug Conjugates (ADC) Market Size by Indication in the 7MM (2020-2034)

- Figure 5: Total Antibody Drug Conjugates (ADC) Market Size in the United States (2020-2034)

- Figure 6: Antibody Drug Conjugates (ADC) Market Size by Therapies in the United States (2020-2034)

- Figure 7: Total Antibody Drug Conjugates (ADC) Market Size in EU4 and the UK (2020-2034)

- Figure 8: Antibody Drug Conjugates (ADC) Market Size by Therapies in EU4 and the UK (2020-2034)

- Figure 9: Total Antibody Drug Conjugates (ADC) Market Size in Japan (2020-2034)

- Figure 10: Antibody Drug Conjugates (ADC) Market Size by Therapies in Japan (2020-2034)

Antibody Drug Conjugates Market

The US FDA has approved a total of 13 ADCs and the first ADC to be approved was MYLOTARG. But later in 2017, MYLOTARG was voluntarily withdrawn from the market after subsequent confirmatory trials failed to verify clinical benefit and demonstrated safety concerns, including a high number of early deaths.

The development of Antibody Drug Conjugate market is a global endeavor, with companies across the world investing significant resources. Currently, over ~200 antibody-drug conjugates are in various stages of pre-clinical and clinical development, indicating the widespread interest and potential of this field.

The Antibody Drug Conjugate Market has certain key players. A lot of companies are actively developing antibody drug conjugate in the 7MM, and many of them are large-cap companies actively working in this space, such as Roche, Takeda, Gilead Sciences, Pfizer, GlaxoSmithKline, Daiichi Sankyo/AstraZeneca, and others. Daiichi Sankyo is expected to lead a new era of antibody-drug conjugates.

Recently sat ASCO 2024, AbbVie presented new data from its innovative ADC platform that showcased data across three different ADCs i.e., ABBV-706, telisotuzumab vedotin, and ABBV-400 in solid tumors.

In a late-breaking session at the ASCO 2024, GSK announced noteworthy results in the DREAMM-8 Study, particularly in light of GSK's decision in late 2022 to withdraw BLENREP from the US market. The new data could support a case for the reintroduction of BLENREP to the market. Regulatory decision (US, EU, JP) based on DREAMM-7/8 trial in second line and above multiple myeloma and regulatory submission based on DREAMM-8 trial in multiple myeloma is planned in 2025.

DelveInsight's "Antibody Drug Conjugate Market - Competitive Landscape, and Market Forecast - 2034" report delivers an in-depth understanding of the antibody-drug conjugates, historical and competitive landscape as well as the antibody-drug conjugates market trends in the United States, EU4 (Germany, France, Italy, and Spain) and the United Kingdom, and Japan.

The antibody drug conjugate market report provides current treatment practices, emerging drugs, market share of individual therapies, and current and forecasted 7MM antibody drug conjugate market size from 2020 to 2034. The report also covers current antibody-drug conjugates treatment practices/algorithms and unmet medical needs to curate the best opportunities and assess the market's potential.

Geography Covered:

- The United States

- EU4 (Germany, France, Italy, and Spain), and the UK

- Japan

- Study Period: 2020-2034

Antibody Drug Conjugate Market Understanding

Antibody drug Conjugates (ADCs) Overview

Antibody drug conjugate is a new emerging class of highly potent pharmaceutical drugs, which is a great combination of chemotherapy and immunotherapy. Antibody-drug conjugates empower the selective delivery of highly potent drugs to tumor cells while sparing healthy cells, attenuating the main clinical obstacle of traditional chemotherapy, thus providing a broad therapeutic window. One of the most important aspects of antibody-drug conjugate development for cancer is the identification of the unique antigenic target of the monoclonal antibody component. The selected antigen needs to fulfill several requirements. First, the target antigen needs to have high expression in the tumor and no or low expression in the healthy cell. Second, the target antigen should be displayed on the surface of the tumor cell to be available to the circulated monoclonal antibody. Third, the target antigen should possess internalization properties as it will facilitate the antibody-drug conjugate to transport into the cell, which will in turn enhance the efficacy of the cytotoxic agent.

The 13 US FDA-approved antibody-drug conjugates are KADCYLA, ADCETRIS, BESPONSA, MYLOTARG, LUMOXITI, POLIVY, PADCEV, TRODELVY, ENHERTU, BLENREP, ZYNLONTA, TIVDAK, and ELAHERE.

Antibody drug Conjugates (ADCs) Epidemiology

Antibody Drug Conjugate Qualitative Analysis

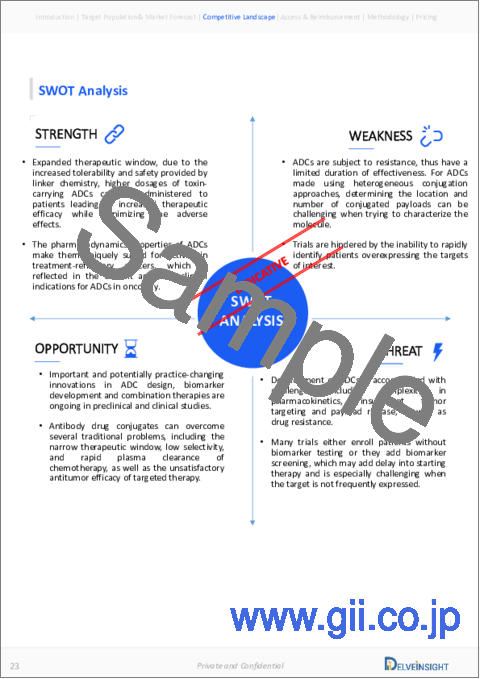

We perform qualitative and market intelligence analysis using various approaches, such as SWOT analysis and Conjoint Analysis. In the SWOT analysis, strengths, weaknesses, opportunities, and threats in terms of gaps in disease diagnosis, patient awareness, physician acceptability, competitive landscape, cost-effectiveness, and geographical accessibility of therapies are provided.

Conjoint Analysis analyses multiple approved and emerging therapies based on relevant attributes such as safety, efficacy, frequency of administration, route of administration, and order of entry. Scoring is given based on these parameters to analyze the effectiveness of therapy.

In efficacy, the trial's primary and secondary outcome measures are evaluated; for instance, in event-free survival, one of the most important primary outcome measures is event-free survival and overall survival.

Further, the therapies' safety is evaluated wherein the acceptability, tolerability, and adverse events are majorly observed, and it sets a clear understanding of the side effects posed by the drug in the trials. In addition, the scoring is also based on the probability of success, and the addressable patient pool for each therapy. According to these parameters, the final weightage score and the ranking of the emerging therapies are decided.

Antibody Drug Conjugate Market Access and Reimbursement

Market Access refers to the ability of all patients to have access to a given product quickly, conveniently, and affordably. Reimbursement is the negotiation of a price between the manufacturer and payer that allows the manufacturer access to that market. It is provided to reduce the high costs and make essential drugs affordable. Reimbursement is the price negotiation between the manufacturer and payer that allows the manufacturer access to that market. It is provided to reduce the high costs and make essential drugs affordable. In the US healthcare system, both Public and Private health insurance coverage are included. In addition, Medicare and Medicaid are the largest government-funded programs in the US. The major healthcare programs, including Medicare, Medicaid, the Children's Health Insurance Program (CHIP), and the state and federal health insurance marketplaces, are overseen by the Centers for Medicare & Medicaid Services (CMS). Other than these, Pharmacy Benefit Managers (PBMs), and third-party organizations that provide services and educational programs to aid patients are also present.

The report further provides detailed insights on the country-wise accessibility and reimbursement scenarios, cost-effectiveness scenario of currently used therapies, programs making accessibility easier and out-of-pocket costs more affordable, insights on patients insured under federal or state government prescription drug programs, etc.

Scope of the Antibody Drug Conjugate Market Report

- The adc market forecast report covers a segment of key events, an executive summary, and a descriptive overview of antibody-drug conjugates, explaining its mechanism, and therapies (current and emerging).

- Comprehensive insight into the competitive landscape, and forecasts, the future growth potential of treatment rate, drug uptake, and drug information have been provided.<

- Additionally, an all-inclusive account of the current and emerging therapies and the elaborative profiles of late-stage and prominent therapies will impact the current landscape.

- A detailed review of the antibody-drug conjugates market, historical and forecasted market size, market share by therapies, detailed assumptions, and rationale behind our approach is included in the report, covering the 7MM drug outreach.

- The adc market forecast report provides an edge while developing business strategies, by understanding trends, through SWOT analysis expert insights/KOL views, and treatment preferences that help shape and drive the 7MM antibody-drug conjugates market.

Table of Contents

1. Key Insights

2. Report Introduction

3. Executive Summary of Antibody Drug Conjugates (ADC)

4. Key Events

5. Antibody Drug Conjugates (ADC) Market Overview At A Glance

- 5.1. Market Share (%) Distribution of Antibody Drug Conjugates (ADC) By Therapy in 2023

- 5.2. Market Share (%) Distribution of Antibody Drug Conjugates (ADC) By Therapy in 2034

6. Background And Overview

7. Target Population

8. Antibody Drug Conjugates (ADC) Marketed Drugs

- 8.1. Key Competitors

- 8.2. Company 1: Product 1

- 8.2.1. Product Description

- 8.2.2. Regulatory Milestones

- 8.2.3. Other Developmental Activities

- 8.2.4. Ongoing Clinical Development

- 8.2.5. Safety and Efficacy

- 8.3. Company 2: Product 2

- 8.3.1. Product Description

- 8.3.2. Regulatory Milestones

- 8.3.3. Other Developmental Activities

- 8.3.4. Ongoing Clinical Development

- 8.3.5. Safety and Efficacy

9. Antibody Drug Conjugates (ADC) Emerging Drugs

- 9.1. Key Competitors

- 9.2. Company 1: Product 1

- 9.2.1. Product Description

- 9.2.2. Other Development Activities

- 9.2.3. Clinical Development

- 9.2.3.1. Clinical Trials Information

- 9.2.4. Safety and Efficacy

- 9.3. Company 2: Product 2

- 9.3.1. Product Description

- 9.3.2. Other Development Activities

- 9.3.3. Clinical Development

- 9.3.3.1. Clinical Trials Information

- 9.3.4. Safety and Efficacy

10. Antibody Drug Conjugates (ADC): The 7MM Analysis

- 10.1. Key Findings

- 10.2. Market Outlook

- 10.3. Key Market Forecast Assumptions

- 10.4. Total Market Size of Antibody Drug Conjugates (ADC) in the 7MM

- 10.4.1. Market Size of Antibody Drug Conjugates (ADC) By Therapies In the 7MM

- 10.4.2. Market Size of Antibody Drug Conjugates (ADC) By Indication In the 7MM

- 10.6. United States Market

- 10.6.1. Total Market Size of Antibody Drug Conjugates (ADC) in the United States

- 10.6.2. Market Size of Antibody Drug Conjugates (ADC) By Therapies in the United States

- 10.7. EU4 and the UK Market

- 10.7.1. Total Market Size of Antibody Drug Conjugates (ADC) in EU4 and the UK

- 10.7.2. Market Size of Antibody Drug Conjugates (ADC) By Therapies in EU4 and the UK

- 10.8. Japan Market

- 10.8.1. Total Market Size of Antibody Drug Conjugates (ADC) in Japan

- 10.8.2. Market Size of Antibody Drug Conjugates (ADC) By Therapies in Japan

11. Unmet Needs

12. SWOT Analysis

13. KOL Views

14. Market Access and Reimbursement

- 14.1. United States

- 14.1.1. Centre for Medicare & Medicaid Services (CMS)

- 14.2. EU4 and the UK

- 14.2.1. Germany

- 14.2.2. France

- 14.2.3. Italy

- 14.2.4. Spain

- 14.2.5. United Kingdom

- 14.3. Japan

- 14.3.1. MHLW

15. Appendix

- 15.1. Bibliography

- 15.2. Report Methodology