|

|

市場調査レポート

商品コード

1804854

北米および欧州の低電圧インバータ市場:機械タイプ・電圧・タイプ・定格電力・地域別の分析・予測 (2025-2035年)North America and Europe Low-Voltage Inverters Market - A Regional Analysis: Focus on Market by Machine Type, Voltage, Type, Power Rating, and Region - Analysis and Forecast, 2025-2035 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 北米および欧州の低電圧インバータ市場:機械タイプ・電圧・タイプ・定格電力・地域別の分析・予測 (2025-2035年) |

|

出版日: 2025年09月05日

発行: BIS Research

ページ情報: 英文 230 Pages

納期: 1~5営業日

|

全表示

- 概要

- 図表

- 目次

北米および欧州の低電圧インバータの市場規模は、2025年の31億8,090万米ドルから、CAGR 9.30%で推移し、2035年には77億4,000万米ドルへと成長すると予測されています。

この成長を牽引する要因は、太陽光発電とエネルギー貯蔵の統合、EVおよびEモビリティの普及、分散型再生可能エネルギーやマイクログリッドの拡大、インダストリー4.0や予知保全イニシアティブの進展です。

北米における需要は住宅用および商業用システムが中心ですが、欧州では住宅・産業・ユーティリティ分野の需要がバランスよく分布しています。単相インバータが依然として市場を支配していますが、商業用途やマイクログリッドで三相システムの導入が進みつつあります。北米市場は主に小規模ユニット (10kW未満) に牽引されていますが、欧州市場では中規模インバータ (10~100kW) へのシフトが見られます。

市場機会としては、送電網の近代化、再エネ貯蔵との統合、高度なインバータ機能 (特に産業用やマイクログリッド用途の中~高電圧システム) にあります。一方で、市場の課題としては、高い初期コスト、規格の断片化、規制の遅れ、進化する系統コード、サプライチェーンの混乱、そして総所有コストに関する問題が挙げられます。

| 主要市場統計 | |

|---|---|

| 予測期間 | 2025-2035年 |

| 2025年評価 | 31億8,090万米ドル |

| 2035年予測 | 77億4,000万米ドル |

| CAGR | 9.3% |

市場セグメンテーション

セグメンテーション1:電圧別

- 48V

- 72V

- 96V~120V

- 電圧別では、96V~120Vセグメントが支配的

北米および欧州の低電圧インバータ市場は、再生可能エネルギーの導入、電化の進展、エネルギー貯蔵技術の進歩によって急速に拡大しています。特に96V~120Vセグメントが市場を牽引し、2024年の21億5,000万米ドルから2035年には60億9,000万米ドル超へと成長する見込みです。この成長は、効率的な電力変換を必要とする産業用および大容量エネルギーシステムにおける需要の高まりに支えられています。

また、住宅用ソーラーや小規模エネルギー貯蔵で好まれる48Vセグメントも拡大しており、5億9,200万米ドルから12億7,000万米ドルへと成長する見通しです。さらに72Vセグメントは、EV充電、自動化、バックアップ電源用途に支えられ、1億8,000万米ドルから3億7,400万米ドルへと着実に拡大します。

政策支援、EVインフラの拡充、分散型エネルギーの需要拡大が市場の追い風となる一方で、高コスト、統合の複雑さ、競争激化といった課題も存在します。それでも、半導体材料やパワーエレクトロニクスの革新が進むことで、より効率的で小型かつ信頼性の高いインバータシステムの実現が期待されています。

戦略的な協業や継続的な投資を通じて、低電圧インバータは地域における分散型で持続可能なエネルギーネットワーク推進の重要な基盤となる見込みです。

セグメンテーション2:タイプ別

- 単相

- 三相

タイプ別では、三相が優位を維持

最新の市場データによると、三相低電圧インバータは北米および欧州の低電圧インバータ市場を支配し、2035年まで最大シェアを維持すると予測されています。このセグメントは2025年に22億4,980万米ドルと評価されており、2035年には60億9,320万米ドルに達し、CAGRは10.48%に達する見込みです。

この成長は、産業用モータードライブ、再生可能エネルギーシステム、高効率、高信頼性、大負荷への対応能力が重要な分野で広く使用されていることです。三相インバータは、特に大規模な太陽光発電やバックアップシステムにおいて、送電網統合、エネルギー自立、クリーンエネルギーへの移行を支える役割から高く評価されています。さらに、パワーエレクトロニクスや自動化の進展、産業の脱炭素化に向けた政府の支援策も需要を後押ししています。

一方で、単相低電圧インバータは主に住宅用や小規模商業用途で使用されており、堅調な成長を続けています。市場規模は2025年の9億3,110万米ドルから、2035年には16億4,680万米ドルへ拡大し、CAGRは5.87%と予測されています。この成長は、住宅用太陽光発電の普及、エネルギー効率改善、バックアップ電源ニーズの高まりによって推進されています。

住宅における屋上太陽光発電の導入拡大、無停電電源装置 (UPS) システムへの需要、家庭での省エネ重視の高まりが単相インバータ市場をさらに支えています。しかし、産業分野や商業用マイクログリッド、再生可能エネルギー設備といった、より強力かつ拡張性の高い電力変換ソリューションを必要とする分野からの需要拡大により、三相システムが引き続き優位を維持すると見込まれます。

セグメンテーション3:電力定格別

- 1 kW未満

- 1-10 kW

- 10-100 kW

- 100 kW以上

セグメンテーション4:地域別

- 北米:米国・カナダ

- 欧州:ドイツ・フランス・英国・イタリア・オランダ・スペイン・その他

北米および欧州の低電圧インバータ市場においては、北米が強い地位を維持すると見込まれており、市場規模は2025年の16億3,120万米ドルから、2035年には36億4,400万米ドルへと拡大し、CAGRは8.37%となる予測です。この成長は、堅調な産業需要、エネルギー貯蔵システムの導入拡大、分散型再生可能エネルギーの幅広い普及によって支えられています。さらに、政府の有利なインセンティブや、輸送・製造といった分野での電化の進展が地域の成長を一層後押ししています。

一方で欧州は、総市場シェアではやや遅れを取るものの、より速い成長が予想されており、2025年の15億4,980万米ドルから、2035年には40億9,600万米ドルへ拡大し、CAGRは10.21%に達すると見込まれます。欧州の成長は、積極的な脱炭素目標、マイクログリッドインフラの拡充、再生可能エネルギー統合やエネルギー自立に対する強力な政策支援によって推進されています。北米と欧州は合わせて、2035年にかけて効率的な低電圧インバータ技術への世界的な移行を牽引していくことが期待されています。

主要企業:

- DANA TM4 INC.

- Enphase Energy

- ZAPI GROUP

- Schneider Electric

当レポートでは、北米および欧州の低電圧インバータの市場を調査し、主要動向、市場影響因子の分析、法規制環境、技術・特許の分析、市場規模の推移・予測、各種区分・地域/主要国別の詳細分析、競合情勢、主要企業のプロファイルなどをまとめています。

目次

エグゼクティブサマリー

範囲と定義

第1章 市場:業界展望

- 動向:現状と将来への影響評価

- ワイドバンドギャップ (WBG) 半導体の採用 (SiC、GaN)

- デジタル化とIoT接続

- 組み込みストレージとハイブリッドアーキテクチャ

- 高度な熱管理とパッケージング

- サプライチェーンの概要

- サプライチェーンの主要企業

- バリューチェーン分析

- 特許分析

- 国別の特許出願動向

- 特許出願動向 (企業別)

- 規制状況

- 技術分析

- パワー半導体の進化

- 制御と通信 (組み込みIoT、エッジ分析)

- パッケージングおよび熱管理ソリューション

- 安全性と信頼性の機能 (アクティブフォールトプロテクション、自己診断)

- バッテリー化学の動向と新たなストレージ

- 油圧ポンプと電動ポンプ

- 市場力学の概要

- 市場促進要因

- 市場抑制要因

- 市場機会

第2章 用途

- 用途のサマリー

- 電化普及率

- ユーティリティビークル、ゴルフカート、UTV

- 二輪車 (電動自転車・モペット)

- 電動空港地上支援設備

- 電動オフハイウェイ車両

- 無人搬送車 (AGV)

- 北米・欧州の低電圧インバータ市場:機械タイプ別

- Eモビリティ

- 産業用ドライブ

- 再生可能エネルギー

- UPSと通信バックアップ

- その他の用途 (海洋、医療、航空宇宙など)

- 北米・欧州の低電圧インバータ市場:機械タイプ・電圧タイプ別

- Eモビリティ

- 産業用ドライブ

- 再生可能エネルギー

- UPSと通信バックアップ

- その他の用途 (海洋、医療、航空宇宙など)

第3章 製品

- 製品セグメントのサマリー

- 北米・欧州の低電圧インバータ市場:電圧別

- 48V

- 72V

- 96V~120V

- 北米・欧州の低電圧インバータ市場:タイプ別

- 単相

- 三相

- 北米・欧州の低電圧インバータ市場:電力定格別

- 最大1kW

- 1~10kW

- 10~100kW

- 100kW以上

第4章 地域

- 地域サマリー

- 北米

- 地域概要

- 市場成長の原動力

- 市場課題

- 米国

- カナダ

- 欧州

- 地域概要

- 市場成長の原動力

- 市場課題

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- オランダ

- その他

第5章 市場:競合ベンチマーキングと企業プロファイル

- 次のフロンティア

- 主要製品ポートフォリオ分析

- 地理的評価

- 競合ベンチマーキング

- 主要企業の分析

- 北米

- 欧州

第6章 調査手法

List of Figures

- Figure 1: North America and Europe Low-Voltage Inverters Market (by Scenario), $Million, 2025, 2030, and 2035

- Figure 2: North America and Europe Low-Voltage Inverters Market, 2024-2035

- Figure 3: Global Market with North America and Europe Low-Voltage Inverters Market Snapshot, 2024

- Figure 4: North America and Europe Low-Voltage Inverters Market, $Million, 2024 and 2035

- Figure 5: North America and Europe Low-Voltage Inverters Market (by Machine Type), $Million, 2024, 2030, and 2035

- Figure 6: North America and Europe Low-Voltage Inverters Market (by Voltage Type), $Million, 2024, 2030, and 2035

- Figure 7: North America and Europe Low-Voltage Inverters Market (by Type), $Million, 2024, 2030, and 2035

- Figure 8: North America and Europe Low-Voltage Inverters Market (by Power Rating), $Million, 2024, 2030, and 2035

- Figure 9: North America and Europe Low-Voltage Inverters Market Segmentation

- Figure 10: Trends, Drivers, Challenges, and Opportunities: Current and Future Impact Assessment

- Figure 11: Key Players in the Supply Chain

- Figure 12: Patent Filing Trend by Country (January 2022-June 2025)

- Figure 13: Patent Filing Trend by Company (January 2022-June 2025)

- Figure 14: Electric Vehicles Stock, Millions, 2019-2023

- Figure 15: North America and Europe Low-Voltage Inverters Market, by Machine Type, Value, $Million, 2024, 2030, and 2035

- Figure 16: North America and Europe Low-Voltage Inverters Market, by Machine Type, Volume, Thousand Units, 2024, 2030, and 2035

- Figure 17: North America and Europe Low-Voltage Inverters Market, E-Mobility (by Value), $Million, 2024-2035

- Figure 18: North America and Europe Low-Voltage Inverters Market, E-Mobility (by Volume), Thousand Units, 2024-2035

- Figure 19: North America and Europe Low-Voltage Inverters Market, Industrial Drives (by Value), $Million, 2024-2035

- Figure 20: North America and Europe Low-Voltage Inverters Market, Industrial Drives (by Volume), Thousand Units, 2024-2035

- Figure 21: North America and Europe Low-Voltage Inverters Market, Renewable Energy (by Value), $Million, 2024-2035

- Figure 22: North America and Europe Low-Voltage Inverters Market, Renewable Energy (by Volume), Thousand Units, 2024-2035

- Figure 23: North America and Europe Low-Voltage Inverters Market, UPS and Telecom Backup (by Value), $Million, 2024-2035

- Figure 24: North America and Europe Low-Voltage Inverters Market, UPS and Telecom Backup (by Volume), Thousand Units, 2024-2035

- Figure 25: North America and Europe Low-Voltage Inverters Market, Other Applications (Marine, Medical, and Aerospace, among others), by Value, $Million, 2024-2035

- Figure 26: North America and Europe Low-Voltage Inverters Market, Other Applications (Marine, Medical, and Aerospace, among others), by Volume, Thousand Units, 2024-2035

- Figure 27: North America and Europe Low-Voltage Inverters Market, E-Mobility, (by Machine Type (by Voltage)), (by Value), $Million, 2024-2035

- Figure 28: North America and Europe Low-Voltage Inverters Market, E-Mobility, (by Machine Type (by Voltage)), (by Volume), Thousand Units, 2024-2035

- Figure 29: North America and Europe Low-Voltage Inverters Market, Industrial Drives, (by Machine Type (by Voltage)), (by Value), $Million, 2024-2035

- Figure 30: North America and Europe Low-Voltage Inverters Market, Industrial Drives, (by Machine Type (by Voltage)), (by Volume), Thousand Units, 2024-2035

- Figure 31: North America and Europe Low-Voltage Inverters Market, Renewable Energy, (by Machine Type (by Voltage)), (by Value), $Million, 2024-2035

- Figure 32: North America and Europe Low-Voltage Inverters Market, Renewable Energy, (by Machine Type (by Voltage)), (by Volume), Thousand Units, 2024-2035

- Figure 33: North America and Europe Low-Voltage Inverters Market, UPS & Telecom Backup, (by Machine Type (by Voltage)), (by Value), $Million, 2024-2035

- Figure 34: North America and Europe Low-Voltage Inverters Market, UPS & Telecom Backup, (by Machine Type (by Voltage)), (by Volume), Thousand Units, 2024-2035

- Figure 35: North America and Europe Low-Voltage Inverters Market, Other Applications, (by Machine Type (by Voltage)), (by Value), $Million, 2024-2035

- Figure 36: North America and Europe Low-Voltage Inverters Market, Other Applications, (by Machine Type (by Voltage)), (by Volume), Thousand Units, 2024-2035

- Figure 37: North America and Europe Low Voltage-Inverters Market (by Voltage), Value, $Million, 2024, 2030, and 2035

- Figure 38: North America and Europe Low Voltage-Inverters Market (by Voltage), Volume, Thousand Units, 2024, 2030, and 2035

- Figure 39: North America and Europe Low-Voltage Inverters Market (by Type), Value, $Million, 2024, 2030, and 2035

- Figure 40: North America and Europe Low-Voltage Inverters Market (by Type), Volume, Thousand Units, 2024, 2030, and 2035

- Figure 41: North America and Europe Low-Voltage Inverters Market (by Power-Rating), Value, $Million, 2024, 2030, and 2035

- Figure 42: North America and Europe Low-Voltage Inverters Market (by Power-Rating), Volume, Thousand Units, 2024, 2030, and 2035

- Figure 43: North America and Europe Low Voltage-Inverters Market (by Voltage), Value, $Million, 2024-2035

- Figure 44: North America and Europe Low Voltage-Inverters Market (by Voltage), Volume, Thousand Units, 2024-2035

- Figure 45: North America and Europe Low Voltage-Inverters Market (by Voltage), Value, $Million, 2024-2035

- Figure 46: North America and Europe Low Voltage-Inverters Market (by Voltage), Volume, Thousand Units, $Million, 2024-2035

- Figure 47: North America and Europe Low Voltage-Inverters Market (by Voltage), Value, $Million, 2024-2035

- Figure 48: North America and Europe Low Voltage-Inverters Market (by Voltage), Volume, Thousand Units, $Million, 2024-2035

- Figure 49: North America and Europe Low Voltage-Inverters Market (by Type), Value, $Million, 2024-2035

- Figure 50: North America and Europe Low Voltage-Inverters Market (by Type), Volume, Thousand Units, 2024-2035

- Figure 51: North America and Europe Low Voltage-Inverters Market (by Type), Value, $Million, 2024-2035

- Figure 52: North America and Europe Low Voltage-Inverters Market (by Type), Volume, Thousand Units, 2024-2035

- Figure 53: North America and Europe Low Voltage-Inverters Market (by Power Rating), Value, $Million, 2024-2035

- Figure 54: North America and Europe Low Voltage-Inverters Market (by Power Rating), Volume, Thousand Units, 2024-2035

- Figure 55: North America and Europe Low Voltage-Inverters Market (by Power Rating), Value, $Million, 2024-2035

- Figure 56: North America and Europe Low Voltage-Inverters Market (by Power Rating), Volume, Thousand Units, 2024-2035

- Figure 57: North America and Europe Low Voltage-Inverters Market (by Power Rating), Value, $Million, 2024-2035

- Figure 58: North America and Europe Low Voltage-Inverters Market (by Power Rating), Volume, Thousand Units, 2024-2035

- Figure 59: North America and Europe Low Voltage-Inverters Market (by Power Rating), Value, $Million, 2024-2035

- Figure 60: North America and Europe Low Voltage-Inverters Market (by Power Rating), Volume, Thousand Units, 2024-2035

- Figure 61: U.S. Low-Voltage Inverters Market, $Million, 2024-2035

- Figure 62: Canada Low-Voltage Inverters Market, $Million, 2024-2035

- Figure 63: Germany Low-Voltage Inverters Market, $Million, 2024-2035

- Figure 64: France Low-Voltage Inverters Market, $Million, 2024-2035

- Figure 65: U.K. Low-Voltage Inverters Market, $Million, 2024-2035

- Figure 66: Italy Low-Voltage Inverters Market, $Million, 2024-2035

- Figure 67: Spain Low-Voltage Inverters Market, $Million, 2024-2035

- Figure 68: Netherlands Low-Voltage Inverters Market, $Million, 2024-2035

- Figure 69: Rest-of-Europe Low-Voltage Inverters Market, $Million, 2024-2035

- Figure 70: Strategic Initiatives, January 2022-April 2025

- Figure 71: Competitive Benchmarking for North America

- Figure 72: Competitive Benchmarking for Europe

- Figure 73: Data Triangulation

- Figure 74: Top-Down and Bottom-Up Approach

- Figure 75: Assumptions and Limitations

List of Tables

- Table 1: Market Snapshot

- Table 2: Competitive Landscape Snapshot

- Table 3: Illustrative Examples of Digital Integration:

- Table 4: Recent Developments (2023-2025)

- Table 5: Latest Techniques for Thermal Management

- Table 6: Latest Amendments in the CE Marking of Low-Voltage Devices

- Table 7: Amendments in UL 1741 standards

- Table 8: Latest Rules and Regulations Under IEEE 1547

- Table 9: Recent Amendments

- Table 10: OpenADR Mandates in the U.S. Now in Force

- Table 11: EU Fit for 55 Legislation that Applies to 48-96V Low-Voltage Inverters

- Table 12: The Clauses in IRA that Single-Out Inverters

- Table 13: Mandatory Rules that Low-Voltage-Inverter Manufacturers must Follow

- Table 14: Cybersecurity Requirements

- Table 15: Recent Product Launches of Semiconductors in North America and Europe

- Table 16: Technical Advantages

- Table 17: Latest Technologies Introduced in North America and Europe for Packaging and Thermal Management Solutions of Low-Voltage Inverters of Range 48V-96V

- Table 18: Latest Technological Innovations Occurred in North America and Europe (Aimed at 48V Nets):

- Table 19: Battery-Chemistry Trends Followed for Low-Voltage Inverters Below 90V

- Table 20: Storage System Design Shifts Enabled by New Chemistries:

- Table 21: Why is it preferred?

- Table 22: Latest Developments

- Table 23: Recent Illustrative Examples of Deployment of PdM Services in European Industrial Sector:

- Table 24: Examples of the Deployment of 48V Battery Backup Units in the Telecom Sectors and Data Centers:

- Table 25: Applications and Regional Fit Analysis of Sub-1kW Inverters

- Table 26: Applications and Regional Fit Analysis of Sub-1kW Inverters

- Table 27: Applications and Regional Fit Analysis of Sub-1kW Inverters

- Table 28: Company Strategic Initiatives and Relevance to >100kW Low-Voltage Inverter Market (2024)

- Table 29: North America and Europe Low-Voltage Inverters Market (by Region), by Value, $Million, 2024-2035

- Table 30: North America and Europe Low-Voltage Inverters Market (by Region), by Volume, Thousand Units, 2024-2035

- Table 31: North America and Europe Low-Voltage Inverters Market (by Machine Type), Value, $Million, 2024-2035

- Table 32: North America and Europe Low-Voltage Inverters Market (by Machine Type), Volume, Thousand Units, 2024-2035

- Table 33: North America and Europe Low-Voltage Inverters Market, by Machine Type (by Voltage), Value, $Million, 2024-2035

- Table 34: North America and Europe Low-Voltage Inverters Market, by Machine Type (by Voltage), Volume, Thousand Units, 2024-2035

- Table 35: North America and Europe Low-Voltage Inverters Market, by Voltage, Value, $Million, 2024-2035

- Table 36: North America and Europe Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 37: North America and Europe Low-Voltage Inverters Market, by Type, Value, $Million, 2024-2035

- Table 38: North America and Europe Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 39: North America and Europe Low-Voltage Inverters Market, by Voltage, Value, $Million, 2024-2035

- Table 40: North America and Europe Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 41: U.S. Low-Voltage Inverters Market (by Machine Type), Value, $Million, 2024-2035

- Table 42: U.S. Low-Voltage Inverters Market (by Machine Type), Volume, Thousand Units, 2024-2035

- Table 43: U.S. Low-Voltage Inverters Market, by Machine Type (by Voltage), Value, $Million, 2024-2035

- Table 44: U.S. Low-Voltage Inverters Market, by Machine Type (by Voltage), Volume, Thousand Units, 2024-2035

- Table 45: U.S. Low-Voltage Inverters Market, by Voltage, Value, $Million, 2024-2035

- Table 46: U.S. Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 47: U.S. Low-Voltage Inverters Market, by Type, Value, $Million, 2024-2035

- Table 48: U.S. Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 49: U.S. Low-Voltage Inverters Market, by Voltage, Value, $Million, 2024-2035

- Table 50: U.S. Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 51: Canada Low-Voltage Inverters Market (by Machine Type), Value, $Million, 2024-2035

- Table 52: Canada Low-Voltage Inverters Market (by Machine Type), Volume, Thousand Units, 2024-2035

- Table 53: Canada Low-Voltage Inverters Market, by Machine Type (by Voltage), Value, $Million, 2024-2035

- Table 54: Canada Low-Voltage Inverters Market, by Machine Type (by Voltage), Volume, Thousand Units, 2024-2035

- Table 55: Canada Low-Voltage Inverters Market, by Voltage, Value, $Million, 2024-2035

- Table 56: Canada Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 57: Canada Low-Voltage Inverters Market, by Type, Value, $Million, 2024-2035

- Table 58: Canada Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 59: Canada Low-Voltage Inverters Market, by Voltage, Value, $Million, 2024-2035

- Table 60: Canada Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 61: Europe Low-Voltage Inverters Market (by Machine Type), Value, $Million, 2024-2035

- Table 62: Europe Low-Voltage Inverters Market (by Machine Type), Volume, Thousand Units, 2024-2035

- Table 63: Europe Low-Voltage Inverters Market, by Machine Type (by Voltage), Value, $Million, 2024-2035

- Table 64: Europe Low-Voltage Inverters Market, by Machine Type (by Voltage), Volume, Thousand Units, 2024-2035

- Table 65: Europe Low-Voltage Inverters Market, by Voltage, Value, $Million, 2024-2035

- Table 66: Europe Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 67: Europe Low-Voltage Inverters Market, by Type, Value, $Million, 2024-2035

- Table 68: Europe Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 69: Europe Low-Voltage Inverters Market, by Voltage, Value, $Million, 2024-2035

- Table 70: Europe Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 71: Germany Low-Voltage Inverters Market (by Machine Type), Value, $Million, 2024-2035

- Table 72: Germany Low-Voltage Inverters Market (by Machine Type), Volume, Thousand Units, 2024-2035

- Table 73: Germany Low-Voltage Inverters Market, by Machine Type (by Voltage), Value, $Million, 2024-2035

- Table 74: Germany Low-Voltage Inverters Market, by Machine Type (by Voltage), Volume, Thousand Units, 2024-2035

- Table 75: Germany Low-Voltage Inverters Market, by Voltage, Value, $Million, 2024-2035

- Table 76: Germany Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 77: Germany Low-Voltage Inverters Market, by Type, Value, $Million, 2024-2035

- Table 78: Germany Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 79: Germany Low-Voltage Inverters Market, by Voltage, Value, $Million, 2024-2035

- Table 80: Germany Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 81: France Low-Voltage Inverters Market (by Machine Type), Value, $Million, 2024-2035

- Table 82: France Low-Voltage Inverters Market (by Machine Type), Volume, Thousand Units, 2024-2035

- Table 83: France Low-Voltage Inverters Market, by Machine Type (by Voltage), Value, $Million, 2024-2035

- Table 84: France Low-Voltage Inverters Market, by Machine Type (by Voltage), Volume, Thousand Units, 2024-2035

- Table 85: France Low-Voltage Inverters Market, by Voltage, Value, $Million, 2024-2035

- Table 86: France Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 87: France Low-Voltage Inverters Market, by Type, Value, $Million, 2024-2035

- Table 88: France Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 89: France Low-Voltage Inverters Market, by Voltage, Value, $Million, 2024-2035

- Table 90: France Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 91: U.K. Low-Voltage Inverters Market (by Machine Type), Value, $Million, 2024-2035

- Table 92: U.K. Low-Voltage Inverters Market (by Machine Type), Volume, Thousand Units, 2024-2035

- Table 93: U.K. Low-Voltage Inverters Market, by Machine Type (by Voltage), Value, $Million, 2024-2035

- Table 94: U.K. Low-Voltage Inverters Market, by Machine Type (by Voltage), Volume, Thousand Units, 2024-2035

- Table 95: U.K. Low-Voltage Inverters Market, by Voltage, Value, $Million, 2024-2035

- Table 96: U.K. Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 97: U.K. Low-Voltage Inverters Market, by Type, Value, $Million, 2024-2035

- Table 98: U.K. Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 99: U.K. Low-Voltage Inverters Market, by Voltage, Value, $Million, 2024-2035

- Table 100: U.K. Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 101: Italy Low-Voltage Inverters Market (by Machine Type), Value, $Million, 2024-2035

- Table 102: Italy Low-Voltage Inverters Market (by Machine Type), Volume, Thousand Units, 2024-2035

- Table 103: Italy Low-Voltage Inverters Market, by Machine Type (by Voltage), Value, $Million, 2024-2035

- Table 104: Italy Low-Voltage Inverters Market, by Machine Type (by Voltage), Volume, Thousand Units, 2024-2035

- Table 105: Italy Low-Voltage Inverters Market, by Voltage, Value, $Million, 2024-2035

- Table 106: Italy Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 107: Italy Low-Voltage Inverters Market, by Type, Value, $Million, 2024-2035

- Table 108: Italy Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 109: Italy Low-Voltage Inverters Market, by Voltage, Value, $Million, 2024-2035

- Table 110: Italy Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 111: Spain Low-Voltage Inverters Market (by Machine Type), Value, $Million, 2024-2035

- Table 112: Spain Low-Voltage Inverters Market (by Machine Type), Volume, Thousand Units, 2024-2035

- Table 113: Spain Low-Voltage Inverters Market, by Machine Type (by Voltage), Value, $Million, 2024-2035

- Table 114: Spain Low-Voltage Inverters Market, by Machine Type (by Voltage), Volume, Thousand Units, 2024-2035

- Table 115: Spain Low-Voltage Inverters Market, by Voltage, Value, $Million, 2024-2035

- Table 116: Spain Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 117: Spain Low-Voltage Inverters Market, by Type, Value, $Million, 2024-2035

- Table 118: Spain Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 119: Spain Low-Voltage Inverters Market, by Voltage, Value, $Million, 2024-2035

- Table 120: Spain Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 121: Netherlands Low-Voltage Inverters Market (by Machine Type), Value, $Million, 2024-2035

- Table 122: Netherlands Low-Voltage Inverters Market (by Machine Type), Volume, Thousand Units, 2024-2035

- Table 123: Netherlands Low-Voltage Inverters Market, by Machine Type (by Voltage), Value, $Million, 2024-2035

- Table 124: Netherlands Low-Voltage Inverters Market, by Machine Type (by Voltage), Volume, Thousand Units, 2024-2035

- Table 125: Netherlands Low-Voltage Inverters Market, by Voltage, Value, $Million, 2024-2035

- Table 126: Netherlands Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 127: Netherlands Low-Voltage Inverters Market, by Type, Value, $Million, 2024-2035

- Table 128: Netherlands Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 129: Netherlands Low-Voltage Inverters Market, by Voltage, Value, $Million, 2024-2035

- Table 130: Netherlands Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 131: Rest-of-Europe Low-Voltage Inverters Market (by Machine Type), Value, $Million, 2024-2035

- Table 132: Rest-of-Europe Low-Voltage Inverters Market (by Machine Type), Volume, Thousand Units, 2024-2035

- Table 133: Rest-of-Europe Low-Voltage Inverters Market, by Machine Type (by Voltage), Value, $Million, 2024-2035

- Table 134: Rest-of-Europe Low-Voltage Inverters Market, by Machine Type (by Voltage), Volume, Thousand Units, 2024-2035

- Table 135: Rest-of-Europe Low-Voltage Inverters Market, by Voltage, Value, $Million, 2024-2035

- Table 136: Rest-of-Europe Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 137: Rest-of-Europe Low-Voltage Inverters Market, by Type, Value, $Million, 2024-2035

- Table 138: Rest-of-Europe Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 139: Rest-of-Europe Low-Voltage Inverters Market, by Voltage, Value, $Million, 2024-2035

- Table 140: Rest-of-Europe Low-Voltage Inverters Market, by Voltage, Volume, Thousand Units, 2024-2035

- Table 141: Feature Analysis of Low-Voltage Inverters

- Table 142: Global Market Share, 2024

- Table 143: Startup Landscape in the Market

This report can be delivered within 1 working day.

North America and Europe Low-Voltage Inverters Market Overview

The North America and Europe low-voltage inverters market is projected to grow from $3,180.9 million in 2025 to $7,740.0 million by 2035, at a CAGR of 9.30%. This growth is driven by solar PV and energy storage integration, the rise of EVs and e?mobility, expansion of distributed renewables and microgrids, and Industry?4.0/predictive maintenance initiatives. North American demand is led by residential and commercial systems, while Europe sees a more balanced split across residential, industrial, and utility segments. Single-phase inverters dominate, but three-phase systems are gaining ground in commercial and microgrid use. North America is led by small-scale units (<10?kW), whereas Europe is shifting toward medium-power inverters (10-100?kW). Opportunities lie in grid modernization, renewables storage integration, and advanced inverter functions, especially in industrial and microgrid applications, and medium- to higher-voltage systems. Key challenges include high upfront costs, fragmented standards, regulatory delays, evolving grid codes, supply chain disruptions, and total cost of ownership issues.

| KEY MARKET STATISTICS | |

|---|---|

| Forecast Period | 2025 - 2035 |

| 2025 Evaluation | $3,180.9 Million |

| 2035 Forecast | $7,740.0 Million |

| CAGR | 9.3% |

Introduction of North America and Europe Low-Voltage Inverters Market

The study conducted by BIS Research identifies the North America and Europe low-voltage inverters market as a pivotal enabler of clean-energy and electrification infrastructure. These inverter platforms are rapidly evolving into multifunctional assets capable of delivering efficient power conversion, grid stabilization, and intelligent energy management across residential, commercial, industrial, and utility domains. Their role is rising amid accelerating renewable deployment, EV integration, distributed microgrids, and Industry?4.0 initiatives that demand real-time responsiveness and predictive control. With advances in AI-driven controls, smart inverter functionalities, and compact power electronics, these systems are becoming increasingly autonomous, agile, and adaptable. Modular and scalable designs support rapid customization for applications like rooftop solar, energy storage, EV charging, microgrids, and industrial systems. As utilities and policymakers embrace distributed, network-centric energy models, these inverter ecosystems offer a competitive edge through enhanced grid support, bidirectional communication, and swift deployment. Supported by evolving regulatory frameworks and ongoing technology innovation, the market in North America and Europe is well-positioned for continued expansion.

Market Introduction

The North America and Europe low-voltage inverters market is becoming a cornerstone of modern clean energy and electrification infrastructure, driven by the increasing demand for efficient power conversion, grid stabilization, and intelligent energy management across residential, commercial, industrial, and utility domains. As renewable energy adoption accelerates and electrification expands, low-voltage inverters, from residential microinverters to industrial-grade string and central inverters, deliver essential power conversion and grid support across diverse applications. Advancements in AI-driven controls, smart inverter functionalities, and compact power electronics are enhancing autonomy and adaptability, while the integration of energy storage systems, electric vehicle charging infrastructure, and smart grid technologies is expanding operational reach. Amid rising energy demands and the need for sustainable solutions, governments and industries are accelerating investments in low-voltage inverter technologies. With continued innovation, low-voltage inverters are set to play a vital role in the future of decentralized, networked energy systems.

Industrial Impact

The North America and Europe low-voltage inverters market is transforming the energy and industrial sectors through rapid advancements in clean energy integration, electrification, and intelligent power management technologies. Low-voltage inverters, ranging from residential microinverters to industrial-grade string and central inverters, enable efficient power conversion, grid stabilization, and energy management across renewables, e-mobility, and industrial drives.

The market growth is driven by the surge in EV and e-mobility adoption, expansion of distributed renewables and micro-grids, and the rise of Industrial 4.0 predictive maintenance. These factors are fueling demand for modular, AI-enabled inverter systems that enhance efficiency and grid resilience. Meanwhile, high upfront costs of wide-bandgap devices and fragmented standards pose challenges to market adoption.

As governments and industries invest in sustainable and intelligent energy solutions, the North America and Europe low-voltage inverters market is poised to play a vital role in the region's transition toward decentralized and smart energy systems.

Market Segmentation:

Segmentation 1: by Voltage

- 48V

- 72V

- 96V to 120V

- 96V to 120V Segment to Dominate the North America and Europe Low-Voltage Inverters Market (by Voltage)

The North America and Europe low-voltage inverters market is expanding rapidly, driven by renewable energy adoption, electrification, and advancements in energy storage. The 96V-120V segment is set to lead, growing from $2.15 billion in 2024 to over $6.09 billion by 2035, propelled by demand in industrial and high-capacity energy systems that require efficient power conversion.

The 48V segment, favored in residential solar and small-scale energy storage, is also on the rise, from $592 million to $1.27 billion. Meanwhile, the 72V segment will grow steadily from $180 million to $374 million, supported by applications in EV charging, automation, and backup power solutions.

Policy support, expanding EV infrastructure, and distributed energy needs are driving momentum, though challenges like high costs, integration complexity, and competition remain. Still, innovations in semiconductor materials and power electronics are paving the way for more efficient, compact, and reliable inverter systems.

With strategic collaborations and continued investment, low-voltage inverters are poised to become a key building block in the region's push toward decentralized, sustainable energy networks.

Segmentation 2: by Type

- Single-Phase

- Three-Phase

Three-Phase to Maintain Dominance in the North America and Europe Low-Voltage Inverters Market (by Type)

According to recent market data, three-phase low-voltage inverters are projected to dominate the North America and Europe low-voltage inverters market, maintaining the largest share through 2035. Valued at $2,249.8 million in 2025, the segment is expected to reach $6,093.2 million by 2035, growing at a CAGR of 10.48%. This growth is driven by their widespread use in industrial motor drives, renewable energy systems, and commercial infrastructure, where high efficiency, reliability, and the capacity to handle large loads are critical. These inverters are favored for their role in supporting grid integration, energy independence, and the shift to clean energy, particularly in large-scale solar and backup systems. Demand is further reinforced by advancements in power electronics, automation, and government incentives for industrial decarbonization.

In contrast, single-phase low-voltage inverters, primarily used in residential and small commercial applications, are also witnessing steady growth, from $931.1 million in 2025 to $1,646.8 million by 2035, at a CAGR of 5.87%, fueled by rising solar adoption, energy efficiency upgrades, and backup power needs.

Growing adoption of rooftop solar, demand for uninterruptible power supply (UPS) systems, and emphasis on energy efficiency in homes further support the segment. However, three-phase systems are expected to maintain their lead, driven by accelerating demand from industrial sectors, commercial microgrids, and renewable energy installations that require more robust and scalable power conversion solutions.

Segmentation 3: by Power Rating

- Upto 1 kW

- 1-10 kW

- 10-100 kW

- Above 100 kW

Segmentation 4: by Region

- North America: U.S. and Canada

- Europe: Germany, France, U.K., Italy, Netherlands, Spain, and Rest-of-Europe

North America is projected to maintain a strong position in the North America and Europe low-voltage inverters market, with its market value rising from $1,631.2 million in 2025 to $3,644.0 million by 2035, reflecting a CAGR of 8.37%. This growth is driven by robust industrial demand, increasing deployment of energy storage systems, and widespread adoption of distributed renewable energy solutions. Favorable government incentives and ongoing electrification of sectors such as transport and manufacturing are further reinforcing regional momentum.

Europe, while slightly behind in total market share, is set to grow even faster, from $1,549.8 million in 2025 to $4,096.0 million by 2035, at a CAGR of 10.21%. The region's growth is being fueled by aggressive decarbonization goals, expansion of microgrid infrastructure, and strong policy support for renewable integration and energy independence. Together, North America and Europe are expected to drive the global transition toward efficient, low-voltage inverter technologies through 2035.

Demand - Drivers, Limitations, and Opportunities

Market Demand Drivers: Surge in E-Mobility, Distributed Renewables, and Industry 4.0

The North America and Europe low-voltage inverters market is witnessing robust demand growth, fueled by structural changes in energy use, electrification, and industrial modernization. A primary driver is the surge in electric vehicles (EVs) and e-mobility adoption, which is significantly increasing the demand for compact, efficient, and scalable inverter systems to support vehicle electrification, charging infrastructure, and related energy management needs.

At the same time, the rapid growth of distributed renewable energy systems, including rooftop solar, community microgrids, and localized wind installations, is creating a heightened need for low-voltage inverters capable of grid integration and bidirectional power conversion. These systems play a critical role in ensuring the smooth and efficient transfer of power between decentralized generation assets and the grid, particularly in residential, commercial, and small industrial applications.

Another key driver is the widespread adoption of Industrial 4.0 and predictive maintenance technologies, which require advanced power control solutions and real-time system monitoring. Low-voltage inverters support this shift by enabling flexible, reliable, and intelligent energy distribution across digitally connected manufacturing and industrial operations.

Together, these trends are transforming the energy and industrial landscape of North America and Europe, positioning low-voltage inverters as a foundational technology in the transition toward clean energy, e-mobility, and intelligent infrastructure.

Market Challenges: High Costs, Regulatory Fragmentation, and Supply Chain Pressure

The North America and Europe low-voltage inverters market faces several critical challenges that may slow its growth trajectory despite strong underlying demand. One of the most pressing issues is the high upfront cost of wide-bandgap (WBG) semiconductor devices, such as silicon carbide (SiC) and gallium nitride (GaN), which are essential for enhancing inverter efficiency and thermal performance. These advanced materials, while technologically superior, remain cost-prohibitive for widespread deployment, particularly in price-sensitive residential and small commercial applications.

Additionally, the market contends with fragmented standards and prolonged certification processes across regions, making it difficult for manufacturers to streamline product development and achieve cross-border compliance. This regulatory inconsistency creates delays in time-to-market and limits scalability for both local and international suppliers.

Compounding these challenges is ongoing raw material price inflation, which is driving up manufacturing costs and squeezing profit margins across the value chain. Key materials such as copper, aluminum, and semiconductor components remain volatile in pricing due to geopolitical factors, supply chain constraints, and growing global demand.

Together, these challenges highlight the need for targeted policy support, harmonized regulations, and innovations in cost reduction to ensure that low-voltage inverter adoption can scale effectively across North America and Europe.

Market Opportunities: Legacy Upgrades, Data Center Efficiency, and Recurring Revenue Models

The North America and Europe low-voltage inverters market is well-positioned to capitalize on a range of emerging opportunities that extend beyond traditional applications. One major area of growth is the adoption of 48V DC bus architectures in data centers and telecom infrastructure, aimed at improving energy efficiency and reducing conversion losses. As these sectors scale to meet increasing digital demand, low-voltage inverters will play a critical role in stabilizing power supply and enhancing operational resilience.

In parallel, the retrofitting and upgrading of legacy inverter systems across industrial, commercial, and residential sectors offer a strong pathway for growth. As grid requirements evolve and renewable energy integration deepens, demand is rising for smarter, more efficient inverter solutions that can replace outdated equipment without overhauling entire systems.

Additionally, service and maintenance contracts are emerging as a lucrative, recurring revenue stream, particularly in commercial and industrial segments where reliability and uptime are paramount. By offering ongoing support and predictive maintenance under long-term agreements, manufacturers and service providers can build stable revenue models while delivering added value to end users. Together, these opportunities are expected to significantly boost market penetration, foster innovation, and enhance lifecycle value across the inverter ecosystem in North America and Europe.

How can this report add value to an organization?

Product/Innovation Strategy: The North America and Europe low-voltage inverters market report offers detailed insights into the evolving landscape of the North America and Europe low-voltage inverters market, helping organizations align their product development strategies with emerging trends and application demands. It examines innovations in three-phase inverter systems, 48V DC architectures, and the integration of smart control systems for use in industrial automation, renewable energy, and e-mobility infrastructure. With growing demand for predictive maintenance, high-efficiency inverters, and retrofit-friendly solutions, the report helps R&D teams identify technological opportunities and prioritize modular, scalable designs suited for residential, commercial, and industrial environments.

Growth/Marketing Strategy: Organizations can use the North America and Europe low-voltage inverters market report to build targeted growth strategies across sectors such as distributed renewable energy, industrial motor drives, and EV charging infrastructure. The North America and Europe Low-Voltage Inverters Market report explores key regional drivers, such as policy incentives in Europe and electrification trends in North America, and evaluates high-growth areas including retrofit markets and off-grid energy solutions. Strategies such as geographic expansion, service contract models, and vertical integration are examined to help companies strengthen market share and revenue resilience.

Competitive Strategy: The North America and Europe low-voltage inverters market report provides a comprehensive overview of the competitive landscape, benchmarking key players, and identifying whitespace opportunities in under-served market segments. It analyzes market dynamics by voltage category (single-phase vs. three-phase), application area, and regional demand patterns, allowing organizations to refine their positioning. With an increasing shift toward service-based revenue models and digital monitoring capabilities, companies can leverage the North America and Europe low-voltage inverters market report to enhance value propositions and differentiate in a market shaped by both technological performance and regulatory alignment.

Research Methodology

Factors for Data Prediction and Modelling

- The base currency considered for the North America and Europe Low-Voltage Inverters Market analysis is US$. Currencies other than the US$ have been converted to the US$ for all statistical calculations, considering the average conversion rate for that particular year.

- The currency conversion rate has been taken from the historical exchange rate of the Oanda website.

- Nearly all the recent developments from January 2021 to March 2024 have been considered in this research study.

- The information rendered in the report is a result of in-depth primary interviews, surveys, and secondary analysis.

- Where relevant information was not available, proxy indicators and extrapolation were employed.

- Any economic downturn in the future has not been taken into consideration for the market estimation and forecast.

- Technologies currently used are expected to persist through the forecast with no major technological breakthroughs.

Market Estimation and Forecast

This research study involves the usage of extensive secondary sources, such as certified publications, articles from recognized authors, white papers, annual reports of companies, directories, and major databases to collect useful and effective information for an extensive, technical, market-oriented, and commercial study of the North America and Europe low-voltage inverters market.

The market engineering process involves the calculation of the market statistics, market size estimation, market forecast, market crackdown, and data triangulation (the methodology for such quantitative data processes is explained in further sections). The primary research study has been undertaken to gather information and validate the market numbers for segmentation types and industry trends of the key players in the market.

Primary Research

The primary sources involve industry experts from the North America and Europe low-voltage inverters market and various stakeholders in the ecosystem. Respondents such as CEOs, vice presidents, marketing directors, and technology and innovation directors have been interviewed to obtain and verify both qualitative and quantitative aspects of this research study.

The key data points taken from primary sources include:

- validation and triangulation of all the numbers and graphs

- validation of report segmentation and key qualitative findings

- understanding the competitive landscape

- validation of the numbers of various markets for the market type

- percentage split of individual markets for geographical analysis

Secondary Research

This research study involves the usage of extensive secondary research, directories, company websites, and annual reports. It also makes use of databases, such as Hoovers, Bloomberg, Businessweek, and Factiva, to collect useful and effective information for an extensive, technical, market-oriented, and commercial study of the global market. In addition to the data sources, the study has been undertaken with the help of other data sources and websites, such as the Census Bureau, OICA, and ACEA.

Secondary research was done to obtain crucial information about the industry's value chain, revenue models, the market's monetary chain, the total pool of key players, and the current and potential use cases and applications.

The key data points taken from secondary research include:

- segmentations and percentage shares

- data for market value

- key industry trends of the top players of the market

- qualitative insights into various aspects of the market, key trends, and emerging areas of innovation

- quantitative data for mathematical and statistical calculations

Key Market Players and Competition Synopsis

The companies that are profiled in the North America and Europe low-voltage inverters market have been selected based on inputs gathered from primary experts, who have analyzed company coverage, product portfolio, and market penetration.

Some of the prominent names in the North America and Europe low-voltage inverters market are:

- DANA TM4 INC.

- Enphase Energy

- ZAPI GROUP

- Schneider Electric

Companies that are not a part of the aforementioned pool have been well represented across different sections of the North America and Europe low-voltage inverters market report (wherever applicable).

Table of Contents

Executive Summary

Scope and Definition

1 Market: Industry Outlook

- 1.1 Trends: Current and Future Impact Assessment

- 1.1.1 Wide-Bandgap (WBG) Semiconductor Adoption (SiC, GaN)

- 1.1.2 Digitalization and IoT Connectivity

- 1.1.3 Embedded Storage and Hybrid Architectures

- 1.1.4 Advanced Thermal Management and Packaging

- 1.2 Supply Chain Overview

- 1.2.1 Key Players within the Supply Chain

- 1.2.2 Value Chain Analysis

- 1.3 Patent Analysis

- 1.3.1 Patent Filing Trend by Country

- 1.3.2 Patent Filing Trend (by Company)

- 1.4 Regulatory Landscape

- 1.4.1 Europe (CE Marking, RED and ERP Directives)

- 1.4.2 North America (UL 1741, IEEE 1547, NERC CIP)

- 1.4.3 Emerging Standards (ISO 15118, Open ADR)

- 1.4.4 Impact of Upcoming Legislation (EU fit for 55, U.S. Inflation Reduction Act)

- 1.4.5 Cybersecurity and Functional Safety Standards

- 1.5 Technological Analysis

- 1.5.1 Power-Semiconductor Evolution

- 1.5.2 Control and Communication (Embedded IoT, Edge Analytics)

- 1.5.3 Packaging and Thermal Management Solutions

- 1.5.4 Safety and Reliability Features (Active Fault Protection, Self Diagnostics)

- 1.5.5 Battery-Chemistry Trends and Emerging Storage

- 1.5.6 Hydraulic vs. Electric Pump

- 1.6 Market Dynamics Overview

- 1.6.1 Market Drivers

- 1.6.1.1 Surge in EV and E-mobility Adoption

- 1.6.1.2 Growth of Distributed Renewables and Micro-Grids

- 1.6.1.3 Industrial 4.0 Predictive Maintenance

- 1.6.2 Market Restraints

- 1.6.2.1 High Upfront Costs of Wide-Bandgap Devices

- 1.6.2.2 Fragmented Standards and Certification Delays

- 1.6.2.3 Raw Material Price Inflation

- 1.6.3 Market Opportunities

- 1.6.3.1 48V DC Buses in Data Centers and Telecom

- 1.6.3.2 Retrofit and Upgrade of Legacy Inverter Systems

- 1.6.3.3 Service and Maintenance Contracts as Recurring Revenue

- 1.6.1 Market Drivers

2 Application

- 2.1 Application Summary

- 2.2 Electrification Penetration Rates

- 2.2.1 Utility Vehicles, Golf Carts, and UTVs

- 2.2.2 2-Wheelers (E-bikes and Mopeds)

- 2.2.3 Electric Airport Ground Support Equipment

- 2.2.4 Electric Off-Highway Vehicles

- 2.2.4.1 Electric Agricultural Equipment

- 2.2.4.2 Electric Construction Machinery

- 2.2.5 Automated Guided Vehicles (AGVs)

- 2.3 North America and Europe Low-Voltage Inverters Market (by Machine Type)

- 2.3.1 E-Mobility

- 2.3.1.1 Utility Vehicles, Golf Carts, and UTVs

- 2.3.1.2 2-Wheelers (E-bikes and Mopeds)

- 2.3.1.3 Electric Airport Ground Support Equipment

- 2.3.1.4 Electric Off-Highway Vehicles

- 2.3.1.4.1 Electric Agricultural Equipment

- 2.3.1.4.2 Electric Construction Machinery

- 2.3.1.5 Others

- 2.3.2 Industrial Drives

- 2.3.2.1 Material Handling

- 2.3.2.2 Aerial Platforms

- 2.3.2.3 Automated Guided Vehicles (AGVs)

- 2.3.2.4 Others

- 2.3.3 Renewable Energy

- 2.3.4 UPS and Telecom Backup

- 2.3.5 Other Applications (Marine, Medical, and Aerospace, among Others)

- 2.3.1 E-Mobility

- 2.4 North America and Europe Low-Voltage Inverters Market (by Machine Type (by Voltage Type))

- 2.4.1 E-Mobility

- 2.4.1.1 48 V

- 2.4.1.2 72 V

- 2.4.1.3 96 V to 120 V

- 2.4.2 Industrial Drives

- 2.4.2.1 48 V

- 2.4.2.2 72 V

- 2.4.2.3 96 V to 120 V

- 2.4.3 Renewable Energy

- 2.4.3.1 48 V

- 2.4.3.2 72 V

- 2.4.3.3 96 V to 120 V

- 2.4.4 UPS and Telecom Backup

- 2.4.4.1 48 V

- 2.4.4.2 72 V

- 2.4.4.3 96 V to 120 V

- 2.4.5 Other Applications (Marine, Medical, and Aerospace, among Others)

- 2.4.5.1 48 V

- 2.4.5.2 72 V

- 2.4.5.3 96 V to 120 V

- 2.4.1 E-Mobility

3 Products

- 3.1 Product Segment Summary

- 3.2 North America and Europe Low-Voltage Inverters Market (by Voltage)

- 3.2.1 48V

- 3.2.2 72V

- 3.2.3 96V to 120V

- 3.3 North America and Europe Low-Voltage Inverters Market (by Type)

- 3.3.1 Single-Phase

- 3.3.2 Three-Phase

- 3.4 North America and Europe Low-Voltage Inverters Market (by Power Rating)

- 3.4.1 Upto 1kW

- 3.4.2 1-10kW

- 3.4.3 10-100kW

- 3.4.4 Above 100kW

4 Region

- 4.1 Regional Summary

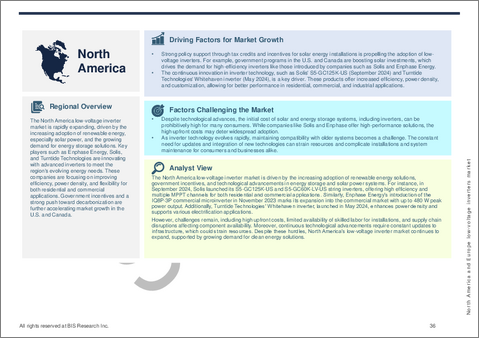

- 4.2 North America

- 4.2.1 Regional Overview

- 4.2.2 Driving Factors for Market Growth

- 4.2.3 Factors Challenging the Market

- 4.2.3.1 Application

- 4.2.3.2 Product

- 4.2.4 U.S.

- 4.2.4.1 Application

- 4.2.4.2 Product

- 4.2.5 Canada

- 4.2.5.1 Application

- 4.2.5.2 Product

- 4.3 Europe

- 4.3.1 Regional Overview

- 4.3.2 Driving Factors for Market Growth

- 4.3.3 Factors Challenging the Market

- 4.3.3.1 Application

- 4.3.3.2 Product

- 4.3.4 Germany

- 4.3.4.1 Application

- 4.3.4.2 Product

- 4.3.5 France

- 4.3.5.1 Application

- 4.3.5.2 Product

- 4.3.6 U.K.

- 4.3.6.1 Application

- 4.3.6.2 Product

- 4.3.7 Italy

- 4.3.7.1 Application

- 4.3.7.2 Product

- 4.3.8 Spain

- 4.3.8.1 Application

- 4.3.8.2 Product

- 4.3.9 Netherlands

- 4.3.9.1 Application

- 4.3.9.2 Product

- 4.3.10 Rest-of-Europe

- 4.3.10.1 Application

- 4.3.10.2 Product

5 Markets - Competitive Benchmarking & Company Profiles

- 5.1 Next Frontiers

- 5.2 Key Product Portfolio Analysis

- 5.2.1 Key Feature Analysis

- 5.3 Geographic Assessment

- 5.3.1 Global Market Share Analysis

- 5.3.2 Strategic Initiatives (Partnerships, Acquisitions, Product Launches)

- 5.4 Competitor Benchmarking

- 5.4.1 Competitive Advantages and Market Differentiators

- 5.4.1.1 North America

- 5.4.1.2 Europe

- 5.4.2 Startup and New Entrants

- 5.4.1 Competitive Advantages and Market Differentiators

- 5.5 Key Player Analysis

- 5.5.1 North America

- 5.5.1.1 Curtis Instruments, Inc.

- 5.5.1.1.1 Overview

- 5.5.1.1.2 Top Products/Product Portfolio

- 5.5.1.1.3 Top Competitors

- 5.5.1.1.4 Target Customers

- 5.5.1.1.5 Key Personal

- 5.5.1.1.6 Analyst View

- 5.5.1.1.7 Market Share, 2024

- 5.5.1.2 Parker Hannifin Corp

- 5.5.1.2.1 Overview

- 5.5.1.2.2 Top Products/Product Portfolio

- 5.5.1.2.3 Top Competitors

- 5.5.1.2.4 Target Customers

- 5.5.1.2.5 Key Personal

- 5.5.1.2.6 Analyst View

- 5.5.1.2.7 Market Share, 2024

- 5.5.1.3 DANA TM4 INC.

- 5.5.1.3.1 Overview

- 5.5.1.3.2 Top Products/Product Portfolio

- 5.5.1.3.3 Top Competitors

- 5.5.1.3.4 Target Customers

- 5.5.1.3.5 Key Personal

- 5.5.1.3.6 Analyst View

- 5.5.1.3.7 Market Share, 2024

- 5.5.1.4 EXELTECH

- 5.5.1.4.1 Overview

- 5.5.1.4.2 Top Products/Product Portfolio

- 5.5.1.4.3 Top Competitors

- 5.5.1.4.4 Target Customers

- 5.5.1.4.5 Key Personal

- 5.5.1.4.6 Analyst View

- 5.5.1.4.7 Market Share, 2024

- 5.5.1.5 Enphase Energy

- 5.5.1.5.1 Overview

- 5.5.1.5.2 Top Products/Product Portfolio

- 5.5.1.5.3 Top Competitors

- 5.5.1.5.4 Target Customers

- 5.5.1.5.5 Key Personal

- 5.5.1.5.6 Analyst View

- 5.5.1.5.7 Market Share, 2024

- 5.5.1.6 Northern Electric Power Technology Inc.

- 5.5.1.6.1 Overview

- 5.5.1.6.2 Top Products/Product Portfolio

- 5.5.1.6.3 Top Competitors

- 5.5.1.6.4 Target Customers

- 5.5.1.6.5 Key Personal

- 5.5.1.6.6 Analyst View

- 5.5.1.6.7 Market Share, 2024

- 5.5.1.7 Turntide

- 5.5.1.7.1 Overview

- 5.5.1.7.2 Top Products/Product Portfolio

- 5.5.1.7.3 Top Competitors

- 5.5.1.7.4 Target Customers

- 5.5.1.7.5 Key Personal

- 5.5.1.7.6 Analyst View

- 5.5.1.7.7 Market Share, 2024

- 5.5.1.1 Curtis Instruments, Inc.

- 5.5.2 Europe

- 5.5.2.1 ZAPI GROUP

- 5.5.2.1.1 Overview

- 5.5.2.1.2 Top Products/Product Portfolio

- 5.5.2.1.3 Top Competitors

- 5.5.2.1.4 Target Customers

- 5.5.2.1.5 Key Personal

- 5.5.2.1.6 Analyst View

- 5.5.2.1.7 Market Share, 2024

- 5.5.2.2 Victron Energy

- 5.5.2.2.1 Overview

- 5.5.2.2.2 Top Products/Product Portfolio

- 5.5.2.2.3 Top Competitors

- 5.5.2.2.4 Target Customers

- 5.5.2.2.5 Key Personal

- 5.5.2.2.6 Analyst View

- 5.5.2.2.7 Market Share, 2024

- 5.5.2.3 Studer Innotec

- 5.5.2.3.1 Overview

- 5.5.2.3.2 Top Products/Product Portfolio

- 5.5.2.3.3 Top Competitors

- 5.5.2.3.4 Target Customers

- 5.5.2.3.5 Key Personal

- 5.5.2.3.6 Analyst View

- 5.5.2.3.7 Market Share, 2024

- 5.5.2.4 Schneider Electric

- 5.5.2.4.1 Overview

- 5.5.2.4.2 Top Products/Product Portfolio

- 5.5.2.4.3 Top Competitors

- 5.5.2.4.4 Target Customers

- 5.5.2.4.5 Key Personal

- 5.5.2.4.6 Analyst View

- 5.5.2.4.7 Market Share, 2024

- 5.5.2.5 CE+T Power

- 5.5.2.5.1 Overview

- 5.5.2.5.2 Top Products/Product Portfolio

- 5.5.2.5.3 Top Competitors

- 5.5.2.5.4 Target Customers

- 5.5.2.5.5 Key Personal

- 5.5.2.5.6 Analyst View

- 5.5.2.5.7 Market Share, 2024

- 5.5.2.6 Mastervolt

- 5.5.2.6.1 Overview

- 5.5.2.6.2 Top Products/Product Portfolio

- 5.5.2.6.3 Top Competitors

- 5.5.2.6.4 Target Customers

- 5.5.2.6.5 Key Personal

- 5.5.2.6.6 Analyst View

- 5.5.2.6.7 Market Share, 2024

- 5.5.2.7 Danfoss

- 5.5.2.7.1 Overview

- 5.5.2.7.2 Top Products/Product Portfolio

- 5.5.2.7.3 Top Competitors

- 5.5.2.7.4 Target Customers

- 5.5.2.7.5 Key Personal

- 5.5.2.7.6 Analyst View

- 5.5.2.7.7 Market Share, 2024

- 5.5.2.8 Valeo

- 5.5.2.8.1 Overview

- 5.5.2.8.2 Top Products/Product Portfolio

- 5.5.2.8.3 Top Competitors

- 5.5.2.8.4 Target Customers

- 5.5.2.8.5 Key Personal

- 5.5.2.8.6 Analyst View

- 5.5.2.8.7 Market Share, 2024

- 5.5.2.1 ZAPI GROUP

- 5.5.1 North America

6 Research Methodology

- 6.1 Data Sources

- 6.1.1 Primary Data Sources

- 6.1.2 Secondary Data Sources

- 6.1.3 Data Triangulation

- 6.2 Market Estimation and Forecast