|

|

市場調査レポート

商品コード

1757395

統合型生体認証シートセンサー市場 - 世界および地域別分析:車両タイプ別、推進力タイプ別、センサータイプ別、販売チャネル別、国別 - 分析と予測(2025年~2035年)Integrated Biometric Seat-Sensor Market - A Global and Regional Analysis: Focus on Vehicle Type, Propulsion Type, Sensor Type, Sales Channel, and Country-Level Analysis - Analysis and Forecast, 2025-2035 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 統合型生体認証シートセンサー市場 - 世界および地域別分析:車両タイプ別、推進力タイプ別、センサータイプ別、販売チャネル別、国別 - 分析と予測(2025年~2035年) |

|

出版日: 2025年06月27日

発行: BIS Research

ページ情報: 英文 140 Pages

納期: 1~5営業日

|

全表示

- 概要

- 図表

- 目次

統合型生体認証シートセンサーシステムは、生理学的および行動学的データを使用して乗員を監視、認証、適応させるために、座席構造内に埋め込まれた高度な車載センサープラットフォームです。

これらのシステムには通常、心拍数、呼吸、姿勢、体温、指紋や顔認識インターフェースなどの生体認証用センサーが含まれます。その目的は、安全性を向上させ、インフォテインメントをパーソナライズし、安全な機能(車内決済など)のためにユーザーを認証し、ドライバーの健康状態や覚醒度をリアルタイムでモニターすることです。この技術は、コネクテッドカーや自律走行車環境における安全性、利便性、パーソナライゼーションの架け橋となります。

統合型生体認証シートセンサーの需要は、主に、衝突軽減にとどまらず、ドライバーの健康状態や注意力を積極的に管理するインテリジェントな車両安全システムに対する消費者の嗜好の高まりが原動力となっています。生体認証シート・センサーは、眠気検出、緊急時の健康モニタリング、認証されたユーザー・プロファイルに基づくパーソナライズされた車内設定などの機能を可能にします。ドライバーの注意力と注意散漫に対する規制の焦点、特にレベル2/3のADAS車両は、OEMの関心を加速させています。さらに、AI主導でパーソナライズされたインフォテインメントに対する消費者の期待の高まりが、座席位置、メディア・コンテンツ、気候の好みをリアルタイムで適応させる組み込み型生体認証ソリューションへの投資を促進しています。

| 主要市場統計 | |

|---|---|

| 予測期間 | 2025年~2035年 |

| 2025年の評価 | 1億1,640万米ドル |

| 2035年の予測 | 3億7,570万米ドル |

| CAGR | 12.44% |

統合型バイオメトリック・シートセンサー市場のもう一つの重要な成長要因は、電気自動車(EV)がますますデジタル・プラットフォームとしての役割を果たすようになり、モビリティの電動化がもう一つの成長エンジンとなっていることです。機械的な注意散漫が少なくなり、キャビンが主要なヒューマン・マシン・インターフェースとなるため、OEMはインテリジェントなセンサー技術をシートのような主要なタッチポイントに組み込むようになっています。同時に、データ収益化モデルも台頭しており、生体認証シートから得られる匿名化された健康状態や行動データが、保険の引き受け、ドライバーのウェルネス・プログラム、サブスクリプション・サービスに活用されています。これらの使用事例は、特にプレミアムEVや将来のモビリティ・アズ・ア・サービス(MaaS)フリートにおいて、生体認証シート統合のROIを強化します。

しかし、強い勢いにもかかわらず、普及にはいくつかの課題があります。第一に、データプライバシーに関する懸念が大きいです。生体情報は非常に機密性が高く、GDPRやCCPAなどの厳しい規制によって管理されています。OEMやサプライヤーは、エンドツーエンドの暗号化、エッジ処理、安全なユーザー同意プロトコルを確保しなければならないです。第2に、マルチモーダル生体センサーを大衆車に組み込むにはコストと複雑さが伴うため、特に価格に敏感な地域では規模の拡大に限界があります。また、他の車両ECUやインフォテインメント・システムとの相互運用性には、標準化されたAPIとテスト・サイクルが必要であり、製品開発スケジュールが長期化することが多いです。

統合型生体認証シートセンサー市場における機会は、特に物流やライドヘイリング・サービス向けのフリート車や商用車への統合型生体認証シートセンサーの拡大です。疲労に起因する事故を防止できるドライバー・モニタリング・システムは、GSR(一般安全規制)2024の下、欧州などの地域で義務付けられています。さらに、車内決済やパーソナライゼーション機能の台頭は、セキュアなログイン、購入認証、ペアレンタル・コントロールなど、バイオメトリクス認証のための自然な経路を提供します。長期的には、これらのセンサーを車内のウェルネス・システムと統合することで、自動車の健康技術や保険と連動したリスク管理といった隣接市場を開拓できる可能性があります。

アジア太平洋の統合型生体認証シート・センサー市場は、中国、日本、韓国の自動車エレクトロニクス・メーカーの存在感の強さから、高成長のハブとして台頭しつつあります。この地域の自動車メーカーは、スマートモビリティ戦略の一環として、次世代ヒューマン・マシン・インターフェースに積極的に投資しています。例えば、NIOやBYDといった中国のOEMは、AIを活用したキャビン体験の一環として、生体認証シートプラットフォームをプレミアムトリムに統合しています。この地域のMEMSセンサー、近接センサー、カーエレクトロニクスの高度なサプライチェーンは、イノベーションサイクルの高速化を支えています。さらに、都市部の人口増加とドライバー監視に関する政府の義務化は、プライベート・モビリティ・モデルと共有モビリティ・モデルの両方への展開を加速させる方向で収束しつつあります。

市場ライフサイクル段階

統合型生体認証シートセンサー市場は現在、成長期から成熟初期段階にあります。特に高級EVやADAS搭載車では、試験的な導入やプレミアムセグメントへの搭載が一般的になりつつあります。しかし、コストと統合の複雑さのため、大衆市場への普及は依然として限定的です。今後5~7年の間に、エッジAIチップ、標準化された生体認証モジュール、規制の明確化が進むにつれて、市場は急速な拡大段階に入ると予想されます。長期的な実現可能性は、より広範な車両エレクトロニクス・アーキテクチャへのシームレスな統合と、ユーザー・データとパーソナライゼーションに関する強固な収益化モデルの開発にかかっています。

生体認証シートセンサーの世界市場セグメンテーション:

セグメンテーション1:車両タイプ別

- 乗用車

- 商用車

- 小型商用車

- 大型商用車

乗用車は、統合型生体認証シートセンサーの世界市場で顕著なアプリケーションセグメントの1つです。

セグメンテーション2:推進力タイプ別

- 内燃機関(ICE)車

- 電気自動車(EV)

セグメンテーション3:センサータイプ別

- 静電容量式センサー

- 心電図(ECG)センサー

- 圧力マッピングセンサー

- 熱センサー

- その他

セグメンテーション4:販売チャネル別

- OEM

- アフターマーケット

セグメンテーション5:地域別

- 北米 - 米国、カナダ、メキシコ

- 欧州 - ドイツ、フランス、英国、イタリア、スペイン、その他

- アジア太平洋 - 中国、日本、韓国、インド、オーストラリア、その他

- その他の地域 - 南米、中東・アフリカ

世界の統合型生体認証シートセンサー市場では、アジア太平洋地域が継続的な成長と主要メーカーの存在により、生産面で牽引力を増すと予想されます。

主要市場参入企業と競合情勢

世界の統合型生体認証シートセンサー市場は、Adient plc、Bosch Mobility、Continental AG、Lear Corporationなどの主要企業が存在感を示し、大きく成長しています。これらの企業は、広範な販売網、広範な研究開発、自動車メーカーとの戦略的パートナーシップを持つ大規模な製造能力を有しています。新興企業は、高性能電気自動車に対する需要の高まりに対応するため、持続可能でコスト効率の高いソリューションに注力しています。同市場は、技術の進歩、規制遵守、自動車生産の増加による激しい競合によって特徴付けられ、自動車のバリューチェーン全体にわたって急速な技術革新と協力をもたらしています。

当レポートでは、世界の統合型生体認証シートセンサー市場について調査し、市場の概要とともに、車両タイプ別、推進力タイプ別、センサータイプ別、販売チャネル別、国別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

エグゼクティブサマリー

範囲と定義

第1章 市場:業界展望

- 動向:現状と将来への影響評価

- 動向:概要

- 乗客快適性ソリューションの需要の高まり

- 電気自動車の需要増加

- サプライチェーンの概要

- バリューチェーン分析

- 市場マップ

- 研究開発レビュー

- 国別・企業別特許出願動向

- 規制状況

- 市場力学の概要

- 市場促進要因

- 市場抑制要因

- 市場機会

第2章 用途

- 用途のセグメンテーション

- 用途のサマリー

- 統合型生体認証シートセンサー市場(車両タイプ別)

- 乗用車

- 商用車

- 統合型生体認証シートセンサー市場(推進力タイプ別)

- 内燃機関(ICE)車

- 電気自動車(EV)

第3章 製品

- 製品のセグメンテーション

- 製品のサマリー

- 統合型生体認証シートセンサー市場(センサータイプ別)

- 静電容量センサー

- 心電図(ECG)センサー

- 圧力マッピングセンサー

- 熱センサー

- その他

- 統合型生体認証シートセンサー市場(販売チャネル別)

- OEM

- アフターマーケット

第4章 地域

- 地域のサマリー

- 促進要因と抑制要因

- 北米

- 地域概要

- 市場成長促進要因

- 市場成長抑制要因

- 用途

- 製品

- 北米の統合型生体認証シートセンサー市場(国別)

- 欧州

- 地域概要

- 市場成長促進要因

- 市場成長抑制要因

- 用途

- 製品

- 欧州の統合型生体認証シートセンサー市場(国別)

- アジア太平洋

- 地域概要

- 市場成長促進要因

- 市場成長抑制要因

- 用途

- 製品

- アジア太平洋の統合型生体認証シートセンサー市場(国別)

- その他の地域

- 地域概要

- 市場成長促進要因

- 市場成長抑制要因

- 用途

- 製品

- その他の地域の統合型生体認証シートセンサー市場(地域別)

第5章 市場-競合情勢と企業プロファイル

- 今後の見通し

- 地理的評価

- 企業プロファイル

- Adient plc

- airbaglightoff limited

- Bosch Mobility

- Continental AG

- Flexpoint Sensor Systems

- Forvia Faurecia

- Gentex

- Lear Corporation

- National Seating (CVG Group)

- Novel GmbH

- Sensor Products Inc.

- Sensing Tex

- TE Connectivity

- Tekscan Inc.

- XSENSOR Tech.

- その他の主要参入企業のリスト

第6章 調査手法

List of Figures

- Figure 1: Integrated Biometric Seat-Sensor Market (by Scenario), $Million, 2025, 2028, and 2035

- Figure 2: Integrated Biometric Seat-Sensor Market (by Region), $Million, 2024, 2027, and 2035

- Figure 3: Integrated Biometric Seat-Sensor Market (by Application), $Million, 2024, 2028, and 2035

- Figure 4: Integrated Biometric Seat-Sensor Market (by Product), $Million, 2024, 2025, and 2035

- Figure 5: Competitive Landscape Snapshot

- Figure 6: Supply Chain Analysis

- Figure 7: Value Chain Analysis

- Figure 8: Patent Analysis (by Country), January 2021-June 2025

- Figure 9: Patent Analysis (by Company), January 2021-June 2025

- Figure 10: Impact Analysis of Market Navigating Factors, 2024-2035

- Figure 11: U.S. Integrated Biometric Seat-Sensor Market, $Million, 2024-2035

- Figure 12: Canada Integrated Biometric Seat-Sensor Market, $Million, 2024-2035

- Figure 13: Mexico Integrated Biometric Seat-Sensor Market, $Million, 2024-2035

- Figure 14: Germany Integrated Biometric Seat-Sensor Market, $Million, 2024-2035

- Figure 15: France Integrated Biometric Seat-Sensor Market, $Million, 2024-2035

- Figure 16: U.K. Integrated Biometric Seat-Sensor Market, $Million, 2024-2035

- Figure 17: Italy Integrated Biometric Seat-Sensor Market, $Million, 2024-2035

- Figure 18: Spain Integrated Biometric Seat-Sensor Market, $Million, 2024-2035

- Figure 19: Rest-of-Europe Integrated Biometric Seat-Sensor Market, $Million, 2024-2035

- Figure 20: China Integrated Biometric Seat-Sensor Market, $Million, 2024-2035

- Figure 21: Japan Integrated Biometric Seat-Sensor Market, $Million, 2024-2035

- Figure 22: South Korea Integrated Biometric Seat-Sensor Market, $Million, 2024-2035

- Figure 23: India Integrated Biometric Seat-Sensor Market, $Million, 2024-2035

- Figure 24: Australia Integrated Biometric Seat-Sensor Market, $Million, 2024-2035

- Figure 25: Rest-of-Asia-Pacific Integrated Biometric Seat-Sensor Market, $Million, 2024-2035

- Figure 26: South America Integrated Biometric Seat-Sensor Market, $Million, 2024-2035

- Figure 27: Middle East and Africa Integrated Biometric Seat-Sensor Market, $Million, 2024-2035

- Figure 28: Strategic Initiatives (by Company), 2021-2025

- Figure 29: Share of Strategic Initiatives, 2021-2025

- Figure 30: Data Triangulation

- Figure 31: Top-Down and Bottom-Up Approach

- Figure 32: Assumptions and Limitations

List of Tables

- Table 1: Market Snapshot

- Table 2: Opportunities across Region

- Table 3: Trends Overview

- Table 4: Integrated Biometric Seat-Sensor Market Pricing Forecast, 2024-2035

- Table 5: Application Summary (by Application)

- Table 6: Product Summary (by Product)

- Table 7: Integrated Biometric Seat-Sensor Market (by Region), $Million, 2024-2035

- Table 8: North America Integrated Biometric Seat-Sensor Market (by Application), $Million, 2024-2035

- Table 9: North America Integrated Biometric Seat-Sensor Market (by Product), $Million, 2024-2035

- Table 10: U.S. Integrated Biometric Seat-Sensor Market (by Application), $Million, 2024-2035

- Table 11: U.S. Integrated Biometric Seat-Sensor Market (by Product), $Million, 2024-2035

- Table 12: Canada Integrated Biometric Seat-Sensor Market (by Application), $Million, 2024-2035

- Table 13: Canada Integrated Biometric Seat-Sensor Market (by Product), $Million, 2024-2035

- Table 14: Mexico Integrated Biometric Seat-Sensor Market (by Application), $Million, 2024-2035

- Table 15: Mexico Integrated Biometric Seat-Sensor Market (by Product), $Million, 2024-2035

- Table 16: Europe Integrated Biometric Seat-Sensor Market (by Application), $Million, 2024-2035

- Table 17: Europe Integrated Biometric Seat-Sensor Market (by Product), $Million, 2024-2035

- Table 18: Germany Integrated Biometric Seat-Sensor Market (by Application), $Million, 2024-2035

- Table 19: Germany Integrated Biometric Seat-Sensor Market (by Product), $Million, 2024-2035

- Table 20: France Integrated Biometric Seat-Sensor Market (by Application), $Million, 2024-2035

- Table 21: France Integrated Biometric Seat-Sensor Market (by Product), $Million, 2024-2035

- Table 22: U.K. Integrated Biometric Seat-Sensor Market (by Application), $Million, 2024-2035

- Table 23: U.K. Integrated Biometric Seat-Sensor Market (by Product), $Million, 2024-2035

- Table 24: Italy Integrated Biometric Seat-Sensor Market (by Application), $Million, 2024-2035

- Table 25: Italy Integrated Biometric Seat-Sensor Market (by Product), $Million, 2024-2035

- Table 26: Spain Integrated Biometric Seat-Sensor Market (by Application), $Million, 2024-2035

- Table 27: Spain Integrated Biometric Seat-Sensor Market (by Product), $Million, 2024-2035

- Table 28: Rest-of-Europe Integrated Biometric Seat-Sensor Market (by Application), $Million, 2024-2035

- Table 29: Rest-of-Europe Integrated Biometric Seat-Sensor Market (by Product), $Million, 2024-2035

- Table 30: Asia-Pacific Integrated Biometric Seat-Sensor Market (by Application), $Million, 2024-2035

- Table 31: Asia-Pacific Integrated Biometric Seat-Sensor Market (by Product), $Million, 2024-2035

- Table 32: China Integrated Biometric Seat-Sensor Market (by Application), $Million, 2024-2035

- Table 33: China Integrated Biometric Seat-Sensor Market (by Product), $Million, 2024-2035

- Table 34: Japan Integrated Biometric Seat-Sensor Market (by Application), $Million, 2024-2035

- Table 35: Japan Integrated Biometric Seat-Sensor Market (by Product), $Million, 2024-2035

- Table 36: South Korea Integrated Biometric Seat-Sensor Market (by Application), $Million, 2024-2035

- Table 37: South Korea Integrated Biometric Seat-Sensor Market (by Product), $Million, 2024-2035

- Table 38: India Integrated Biometric Seat-Sensor Market (by Application), $Million, 2024-2035

- Table 39: India Integrated Biometric Seat-Sensor Market (by Product), $Million, 2024-2035

- Table 40: Australia Integrated Biometric Seat-Sensor Market (by Application), $Million, 2024-2035

- Table 41: Australia Integrated Biometric Seat-Sensor Market (by Product), $Million, 2024-2035

- Table 42: Rest-of-Asia-Pacific Integrated Biometric Seat-Sensor Market (by Application), $Million, 2024-2035

- Table 43: Rest-of-Asia-Pacific Integrated Biometric Seat-Sensor Market (by Product), $Million, 2024-2035

- Table 44: Rest-of-the-World Integrated Biometric Seat-Sensor Market (by Application), $Million, 2024-2035

- Table 45: Rest-of-the-World Integrated Biometric Seat-Sensor Market (by Product), $Million, 2024-2035

- Table 46: South America Integrated Biometric Seat-Sensor Market (by Application), $Million, 2024-2035

- Table 47: South America Integrated Biometric Seat-Sensor Market (by Product), $Million, 2024-2035

- Table 48: Middle East and Africa Integrated Biometric Seat-Sensor Market (by Application), $Million, 2024-2035

- Table 49: Middle East and Africa Integrated Biometric Seat-Sensor Market (by Product), $Million, 2024-2035

- Table 50: Market Share

Global Integrated Biometric Seat-Sensor Market: Industry Overview

Integrated biometric seat-sensor systems are advanced in-vehicle sensor platforms embedded within the seating structure to monitor, authenticate, and adapt to occupants using physiological and behavioral data. These systems typically include sensors for heart rate, respiration, posture, body temperature, and biometric identifiers such as fingerprints or facial recognition interfaces. The goal is to improve safety, personalize infotainment, authenticate users for secure features (e.g., in-car payments), and monitor driver health and alertness in real time. This technology bridges safety, convenience, and personalization in connected and autonomous vehicle environments.

The demand for integrated biometric seat-sensor market is primarily driven by the increasing consumer preference for intelligent vehicle safety systems that go beyond crash mitigation to proactively manage driver health and attention. Biometric seat sensors enable features such as drowsiness detection, emergency health monitoring, and personalized in-cabin settings based on authenticated user profiles. Regulatory focus on driver attention and distraction, particularly for Level 2/3 ADAS vehicles, has accelerated OEM interest. Additionally, rising consumer expectations for AI-driven personalized infotainment are fueling investment in embedded biometric solutions that adapt seat positioning, media content, and climate preferences in real-time.

| KEY MARKET STATISTICS | |

|---|---|

| Forecast Period | 2025 - 2035 |

| 2025 Evaluation | $116.4 Million |

| 2035 Forecast | $375.7 Million |

| CAGR | 12.44% |

Another significant growth driver for the integrated biometric seat-sensor market is the electrification of mobility is another growth engine, as electric vehicles (EVs) increasingly serve as digital platforms. With fewer mechanical distractions, the cabin becomes the main human-machine interface, driving OEMs to embed intelligent sensor technology into key touchpoints like the seat. Simultaneously, data monetization models are emerging-where anonymized health or behavior data from biometric seats is used to inform insurance underwriting, driver wellness programs, or subscription services. These use cases strengthen the ROI for biometric seat integration, particularly in premium EVs and future mobility-as-a-service (MaaS) fleets.

However, despite the strong momentum, several hurdles challenge widespread adoption. First, data privacy concerns are significant-biometric information is highly sensitive and governed by strict regulations such as GDPR and CCPA. OEMs and suppliers must ensure end-to-end encryption, edge processing, and secure user consent protocols. Second, the cost and complexity of integrating multimodal biometric sensors into mass-market vehicles limit scale, especially in price-sensitive regions. Interoperability with other vehicle ECUs and infotainment systems also requires standardized APIs and testing cycles, often prolonging product development timelines.

Opportunities in the integrated biometric seat-sensor market are expanding integrated biometric seat sensors into fleet and commercial vehicles, particularly for logistics and ride-hailing services. Driver monitoring systems that can prevent fatigue-induced accidents are being mandated in regions like Europe under GSR (General Safety Regulation) 2024. Additionally, the rise of in-car payment and personalization features offers a natural pathway for biometric authentication-such as secure logins, purchase verification, or parental controls. Long-term, integrating these sensors with in-cabin wellness systems could open adjacent markets in automotive health tech and insurance-linked risk management.

The Asia-Pacific integrated biometric seat-sensor market is emerging as a high-growth hub ue to the strong presence of automotive electronics manufacturers in China, Japan, and South Korea. Automakers in the region are actively investing in next-gen human-machine interfaces as part of smart mobility strategies. For example, Chinese OEMs like NIO and BYD are integrating biometric seat platforms into premium trims as part of AI-powered cabin experiences. The region's advanced supply chain for MEMS sensors, proximity sensors, and automotive electronics supports faster innovation cycles. Moreover, urban population growth and government mandates on driver monitoring are converging to accelerate deployment in both private and shared mobility models.

Market Lifecycle Stage

The integrated biometric seat-sensor market is currently in a growth-to-early-maturity phase. Pilot deployments and premium segment installations are becoming more common, particularly in luxury EVs and ADAS-equipped vehicles. However, mass-market penetration remains limited due to cost and integration complexity. Over the next five to seven years, as edge AI chips, standardized biometric modules, and regulatory clarity improve, the market is expected to enter a rapid expansion stage. Long-term viability will depend on seamless integration into broader vehicle electronics architecture and the development of robust monetization models around user data and personalization.

Global Integrated Biometric Seat-Sensor Market Segmentation:

Segmentation 1: by Vehicle Type

- Passenger Vehicles

- Commercial Vehicles

- Light Commercial Vehicles

- Heavy Commercial Vehicles

Passenger vehicles is one of the prominent application segments in the global integrated biometric seat-sensor market.

Segmentation 2: by Propulsion Type

- Internal Combustion Engine (ICE) Vehicles

- Electric Vehicles (EV)

Segmentation 3: by Sensor Type

- Capacitive Sensors

- Electrocardiogram (ECG) Sensor

- Pressure Mapping Sensors

- Thermal Sensor

- Others

Segmentation 4: by Sales Channel

- OEM

- Aftermarket

Segmentation 5: by Region

- North America - U.S., Canada, and Mexico

- Europe - Germany, France, U.K., Italy, Spain, and Rest-of-Europe

- Asia-Pacific - China, Japan, South Korea, India, Australia, and Rest-of-Asia-Pacific

- Rest-of-the-World - South America and Middle East and Africa

In the global integrated biometric seat-sensor market, Asia-Pacific is anticipated to gain traction in terms of production, owing to the continuous growth and the presence of key manufacturers in the region.

Key Market Players and Competition Synopsis

The global integrated biometric seat-sensor market is growing considerably with presence key players including Adient plc, Bosch Mobility, Continental AG, and Lear Corporation among others. These companies having wide large manufacturing capacities with wide distribution network, extensive research and development, and strategic partnerships with automakers. Emerging players are focusing on sustainable and cost-effective solutions to meet the growing demand for high-performance electric vehicles. The market is characterized by intense competition driven by technological advancements, regulatory compliance, and increasing vehicle production, leading to rapid innovation and collaboration across the automotive value chain.

Some of the prominent established names in the integrated biometric seat-sensor market are:

- Adient plc

- airbaglightoff limited

- Bosch Mobility

- Continental AG

- Flexpoint Sensor Systems

- Forvia Faurecia

- Gentex

- Lear Corporation

- National Seating (CVG Group)

- Novel GmbH

- Sensor Products Inc.

- Sensing Tex

- TE Connectivity

- Tekscan Inc.

- XSENSOR Tech.

Companies that are not a part of the previously mentioned pool have been well represented across different sections of the report (wherever applicable).

Table of Contents

Executive Summary

Scope and Definition

1. Market: Industry Outlook

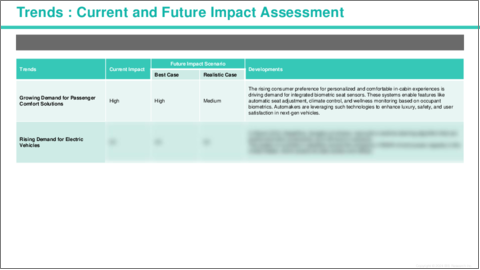

- 1.1 Trends: Current and Future Impact Assessment

- 1.1.1 Trends: Overview

- 1.1.2 Growing Demand for Passenger Comfort Solutions

- 1.1.3 Rising Demand for Electric Vehicles

- 1.2 Supply Chain Overview

- 1.2.1 Value Chain Analysis

- 1.2.2 Market Map

- 1.3 Research and Development Review

- 1.3.1 Patent Filing Trend by Country and by Company

- 1.4 Regulatory Landscape

- 1.5 Market Dynamics Overview

- 1.5.1 Market Drivers

- 1.5.2 Market Restraints

- 1.5.3 Market Opportunities

2. Application

- 2.1 Application Segmentation

- 2.2 Application Summary

- 2.3 Integrated Biometric Seat-Sensor Market (by Vehicle Type)

- 2.3.1 Passenger Vehicles

- 2.3.2 Commercial Vehicles

- 2.3.2.1 Light Commercial Vehicles

- 2.3.2.2 Heavy Commercial Vehicles

- 2.4 Integrated Biometric Seat-Sensor Market (by Propulsion Type)

- 2.4.1 Internal Combustion Engine (ICE) Vehicles

- 2.4.2 Electric Vehicles (EV)

3. Product

- 3.1 Product Segmentation

- 3.2 Product Summary

- 3.3 Integrated Biometric Seat-Sensor Market (by Sensor Type)

- 3.3.1 Capacitive Sensor

- 3.3.2 Electrocardiogram (ECG) Sensor

- 3.3.3 Pressure Mapping Sensor

- 3.3.4 Thermal Sensor

- 3.3.5 Others

- 3.4 Integrated Biometric Seat-Sensor Market (by Sales Channel)

- 3.4.1 OEM

- 3.4.2 Aftermarket

4. Region

- 4.1 Regional Summary

- 4.2 Drivers and Restraints

- 4.3 North America

- 4.3.1 Regional Overview

- 4.3.2 Driving Factors for Market Growth

- 4.3.3 Factors Challenging the Market

- 4.3.4 Application

- 4.3.5 Product

- 4.3.6 North America Integrated Biometric Seat-Sensor Market (by Country)

- 4.3.6.1 U.S.

- 4.3.6.1.1 Market by Application

- 4.3.6.1.2 Market by Product

- 4.3.6.2 Canada

- 4.3.6.2.1 Market by Application

- 4.3.6.2.2 Market by Product

- 4.3.6.3 Mexico

- 4.3.6.3.1 Market by Application

- 4.3.6.3.2 Market by Product

- 4.3.6.1 U.S.

- 4.4 Europe

- 4.4.1 Regional Overview

- 4.4.2 Driving Factors for Market Growth

- 4.4.3 Factors Challenging the Market

- 4.4.4 Application

- 4.4.5 Product

- 4.4.6 Europe Integrated Biometric Seat-Sensor Market (by Country)

- 4.4.6.1 Germany

- 4.4.6.1.1 Market by Application

- 4.4.6.1.2 Market by Product

- 4.4.6.2 France

- 4.4.6.2.1 Market by Application

- 4.4.6.2.2 Market by Product

- 4.4.6.3 U.K.

- 4.4.6.3.1 Market by Application

- 4.4.6.3.2 Market by Product

- 4.4.6.4 Italy

- 4.4.6.4.1 Market by Application

- 4.4.6.4.2 Market by Product

- 4.4.6.5 Spain

- 4.4.6.5.1 Market by Application

- 4.4.6.5.2 Market by Product

- 4.4.6.6 Rest-of-Europe

- 4.4.6.6.1 Market by Application

- 4.4.6.6.2 Market by Product

- 4.4.6.1 Germany

- 4.5 Asia-Pacific

- 4.5.1 Regional Overview

- 4.5.2 Driving Factors for Market Growth

- 4.5.3 Factors Challenging the Market

- 4.5.4 Application

- 4.5.5 Product

- 4.5.6 Asia-Pacific Integrated Biometric Seat-Sensor Market (by Country)

- 4.5.6.1 China

- 4.5.6.1.1 Market by Application

- 4.5.6.1.2 Market by Product

- 4.5.6.2 Japan

- 4.5.6.2.1 Market by Application

- 4.5.6.2.2 Market by Product

- 4.5.6.3 South Korea

- 4.5.6.3.1 Market by Application

- 4.5.6.3.2 Market by Product

- 4.5.6.4 India

- 4.5.6.4.1 Market by Application

- 4.5.6.4.2 Market by Product

- 4.5.6.5 Australia

- 4.5.6.5.1 Market by Application

- 4.5.6.5.2 Market by Product

- 4.5.6.6 Rest-of-Asia-Pacific

- 4.5.6.6.1 Market by Application

- 4.5.6.6.2 Market by Product

- 4.5.6.1 China

- 4.6 Rest-of-the-World

- 4.6.1 Regional Overview

- 4.6.2 Driving Factors for Market Growth

- 4.6.3 Factors Challenging the Market

- 4.6.4 Application

- 4.6.5 Product

- 4.6.6 Rest-of-the-World Integrated Biometric Seat-Sensor Market (by Region)

- 4.6.6.1 South America

- 4.6.6.1.1 Market by Application

- 4.6.6.1.2 Market by Product

- 4.6.6.2 Middle East and Africa

- 4.6.6.2.1 Market by Application

- 4.6.6.2.2 Market by Product

- 4.6.6.1 South America

5. Markets - Competitive Landscape & Company Profiles

- 5.1 Next Frontiers

- 5.2 Geographic Assessment

- 5.3 Company Profiles

- 5.3.1 Adient plc

- 5.3.1.1 Overview

- 5.3.1.2 Top Products / Product Portfolio

- 5.3.1.3 Top Competitors

- 5.3.1.4 Target Customers/End-Users

- 5.3.1.5 Key Personnel

- 5.3.1.6 Analyst View

- 5.3.1.7 Market Share

- 5.3.2 airbaglightoff limited

- 5.3.2.1 Overview

- 5.3.2.2 Top Products / Product Portfolio

- 5.3.2.3 Top Competitors

- 5.3.2.4 Target Customers/End-Users

- 5.3.2.5 Key Personnel

- 5.3.2.6 Analyst View

- 5.3.2.7 Market Share

- 5.3.3 Bosch Mobility

- 5.3.3.1 Overview

- 5.3.3.2 Top Products / Product Portfolio

- 5.3.3.3 Top Competitors

- 5.3.3.4 Target Customers/End-Users

- 5.3.3.5 Key Personnel

- 5.3.3.6 Analyst View

- 5.3.3.7 Market Share

- 5.3.4 Continental AG

- 5.3.4.1 Overview

- 5.3.4.2 Top Products / Product Portfolio

- 5.3.4.3 Top Competitors

- 5.3.4.4 Target Customers/End-Users

- 5.3.4.5 Key Personnel

- 5.3.4.6 Analyst View

- 5.3.4.7 Market Share

- 5.3.5 Flexpoint Sensor Systems

- 5.3.5.1 Overview

- 5.3.5.2 Top Products / Product Portfolio

- 5.3.5.3 Top Competitors

- 5.3.5.4 Target Customers/End-Users

- 5.3.5.5 Key Personnel

- 5.3.5.6 Analyst View

- 5.3.5.7 Market Share

- 5.3.6 Forvia Faurecia

- 5.3.6.1 Overview

- 5.3.6.2 Top Products / Product Portfolio

- 5.3.6.3 Top Competitors

- 5.3.6.4 Target Customers/End-Users

- 5.3.6.5 Key Personnel

- 5.3.6.6 Analyst View

- 5.3.6.7 Market Share

- 5.3.7 Gentex

- 5.3.7.1 Overview

- 5.3.7.2 Top Products / Product Portfolio

- 5.3.7.3 Top Competitors

- 5.3.7.4 Target Customers/End-Users

- 5.3.7.5 Key Personnel

- 5.3.7.6 Analyst View

- 5.3.7.7 Market Share

- 5.3.8 Lear Corporation

- 5.3.8.1 Overview

- 5.3.8.2 Top Products / Product Portfolio

- 5.3.8.3 Top Competitors

- 5.3.8.4 Target Customers/End-Users

- 5.3.8.5 Key Personnel

- 5.3.8.6 Analyst View

- 5.3.8.7 Market Share

- 5.3.9 National Seating (CVG Group)

- 5.3.9.1 Overview

- 5.3.9.2 Top Products / Product Portfolio

- 5.3.9.3 Top Competitors

- 5.3.9.4 Target Customers/End-Users

- 5.3.9.5 Key Personnel

- 5.3.9.6 Analyst View

- 5.3.9.7 Market Share

- 5.3.10 Novel GmbH

- 5.3.10.1 Overview

- 5.3.10.2 Top Products / Product Portfolio

- 5.3.10.3 Top Competitors

- 5.3.10.4 Target Customers/End-Users

- 5.3.10.5 Key Personnel

- 5.3.10.6 Analyst View

- 5.3.10.7 Market Share

- 5.3.11 Sensor Products Inc.

- 5.3.11.1 Overview

- 5.3.11.2 Top Products / Product Portfolio

- 5.3.11.3 Top Competitors

- 5.3.11.4 Target Customers/End-Users

- 5.3.11.5 Key Personnel

- 5.3.11.6 Analyst View

- 5.3.11.7 Market Share

- 5.3.12 Sensing Tex

- 5.3.12.1 Overview

- 5.3.12.2 Top Products / Product Portfolio

- 5.3.12.3 Top Competitors

- 5.3.12.4 Target Customers/End-Users

- 5.3.12.5 Key Personnel

- 5.3.12.6 Analyst View

- 5.3.12.7 Market Share

- 5.3.13 TE Connectivity

- 5.3.13.1 Overview

- 5.3.13.2 Top Products / Product Portfolio

- 5.3.13.3 Top Competitors

- 5.3.13.4 Target Customers/End-Users

- 5.3.13.5 Key Personnel

- 5.3.13.6 Analyst View

- 5.3.13.7 Market Share

- 5.3.14 Tekscan Inc.

- 5.3.14.1 Overview

- 5.3.14.2 Top Products / Product Portfolio

- 5.3.14.3 Top Competitors

- 5.3.14.4 Target Customers/End-Users

- 5.3.14.5 Key Personnel

- 5.3.14.6 Analyst View

- 5.3.14.7 Market Share

- 5.3.15 XSENSOR Tech.

- 5.3.15.1 Overview

- 5.3.15.2 Top Products / Product Portfolio

- 5.3.15.3 Top Competitors

- 5.3.15.4 Target Customers/End-Users

- 5.3.15.5 Key Personnel

- 5.3.15.6 Analyst View

- 5.3.15.7 Market Share

- 5.3.1 Adient plc

- 5.4 List of Other Key Players