|

|

市場調査レポート

商品コード

1757390

難治性てんかん治療市場 - 世界および地域別分析:治療タイプ別、患者タイプ別、発作タイプ別、流通チャネル別、地域別 - 分析と予測(2025年~2035年)Refractory Epilepsy Treatment Market - A Global and Regional Analysis: Focus on Treatment Type, Patient Type, Seizure Type, Distribution Channel, and Regional Analysis - Analysis and Forecast, 2025-2035 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 難治性てんかん治療市場 - 世界および地域別分析:治療タイプ別、患者タイプ別、発作タイプ別、流通チャネル別、地域別 - 分析と予測(2025年~2035年) |

|

出版日: 2025年06月27日

発行: BIS Research

ページ情報: 英文 147 Pages

納期: 1~5営業日

|

全表示

- 概要

- 図表

- 目次

難治性てんかん治療は、がん、遺伝性疾患、その他の複雑な疾患の診断、治療、予防に役立てるため、個人の臨床的、分子的、生活習慣的データを活用します。

難治性てんかん治療は、従来の画一的なアプローチから、よりテーラーメイドで的を絞った治療戦略へと移行する、ヘルスケアにおける変革的な転換を意味します。ゲノミクス、分子診断学、データ解析の進歩を活用することで、難治性てんかん治療は、ヘルスケアプロバイダーが個人の遺伝的、環境的、ライフスタイル的要因に基づいた個別化された治療計画を立てることを可能にします。このアプローチは、治療効果の向上を約束するだけでなく、不必要な試行錯誤を減らし、患者の転帰の改善とヘルスケアコストの削減につながります。この分野が進化を続ける中、大規模な集団研究と最先端技術により、より正確な疾患予測、早期診断、最適化された治療介入への道が開かれつつあります。

| 主要市場統計 | |

|---|---|

| 予測期間 | 2025年~2035年 |

| 2025年の評価 | 49億240万米ドル |

| 2035年予測 | 94億7,260万米ドル |

| CAGR | 6.71% |

市場イントロダクション

世界の難治性てんかん治療の市場規模は大幅な成長が見込まれ、2035年には94億7,260万米ドルに達すると予測されています。世界の難治性てんかん治療市場は、てんかんの有病率の増加と、患者の約30~40%で発作を抑制できない従来の抗てんかん薬の限界を背景に、一貫した成長を遂げています。この重大なアンメット・クリニカル・ニーズは、神経刺激療法(VNS、RNS、DBSを含む)、外科的介入、カンナビジオールや次世代抗てんかん薬のような革新的治療薬のような高度な治療オプションへの需要を喚起し、市場の状況を一変させています。さらに、新興市場における認知度の向上、診断能力の強化、幅広いヘルスケアアクセスも成長を支えています。とはいえ、高額な治療費、複雑な規制要件、専門医療へのアクセスの不均等といった障壁が、依然として普及の妨げとなっています。難治性てんかん治療市場は、より個別化され、デバイスが統合され、高精度の標的を絞ったソリューションへと移行する中で、緊急の臨床ニーズと進化する商業的可能性の最前線に位置しています。

薬剤抵抗性てんかん(DRE)とも呼ばれる難治性てんかんは、全てんかん患者の約30%が罹患しており、少なくとも2種類の抗てんかん薬(ASM)で十分な効果が得られていません。この疾患はアンメットニーズが高く、医薬品と医療機器のイノベーションを牽引しています。難治性てんかんは、世界のてんかん患者の約30%が罹患しており、大きなアンメット・メディカル・ニーズとなっています。このような患者層は、2種類以上の抗てんかん薬(ASM)を使用しても発作のコントロールが得られないため、革新的な治療法の需要が高まっています。競合情勢は、医薬品、デバイス、新興の遺伝子治療分野にまたがり、多様かつ急速に進化しています。UCB PharmaのブリバラセタムやSKライフサイエンスのセノバメートのような伝統的なASMは、有効性と忍容性の向上に重点を置いて進歩を続けており、セノバメートの臨床試験が顕著な発作フリー率を示していることがその例です。一方、LivaNovaの迷走神経刺激やNeuroPace社の応答性神経刺激システムのような神経調節装置は、特に手術が適応とならない焦点性てんかん患者に対して、神経回路を標的とした代替的アプローチを提供しています。

さらに、細胞治療や遺伝子治療は、まだ初期段階にあるもの、精密医療へのシフトを反映し、Dravet症候群のような稀な遺伝性てんかんに対する変革の可能性が期待されています。市場の成長は、規制当局のインセンティブと、特にこれらの先進的治療法の長期的な有用性が実臨床データで検証されるにつれて増加する支払者の受容によって支えられています。全体として、難治性てんかんの治療状況は、困難な地形を進む複数の交通機関のようです。従来型の薬剤は幅広い患者群に使用されているが有効性は限定的であり、神経調節療法は高コストではあるがより正確なコントロールを提供し、新たな遺伝子治療は特定の患者を対象とした根治的な治療法として期待されています。

産業への影響

難治性てんかん治療は、患者の予後を大幅に改善する個別化治療を可能にすることで、ヘルスケア産業を再構築しています。例えば、腫瘍学における遺伝子プロファイリングの利用は、HER2陽性腫瘍の患者を治療するために特別に設計された乳がん用ハーセプチンのような標的治療の開発につながっています。難治性てんかん治療は、個々の患者の治療を向上させるだけでなく、特に創薬や臨床試験において、ヘルスケアのエコシステム全体に革新を促しています。製薬業界は、白血病のCAR-T療法である画期的な新薬Kymriahの開発に見られるように、新薬ターゲットを発見するためにゲノミクスを活用しています。NovartisやPfizerのような企業は、患者集団を層別化し、臨床試験の効率を向上させるためにゲノムデータを使用しています。さらに、難治性てんかん治療の集団健康管理への統合は、Geisinger Health SystemのMyCode Community Health Initiativeのような取り組みに顕著であり、予防医療と疾患の早期発見を改善するために患者にゲノムシーケンスを提供しています。難治性てんかん治療へのこのような応用の広がりは、個々の治療成績を向上させるだけでなく、ヘルスケア提供システムの最適化、コスト削減、新治療法の開発加速にも役立っています。

市場セグメンテーション

セグメンテーション1:治療タイプ別

- 薬理学的

- 薬剤クラス別

第一世代医薬品

第二世代医薬品

新薬・新興医薬品

配合剤

- 非医薬品

- 外科・神経刺激装置

切除手術用機器

レーザー間質性温熱療法(LiTT)

定位脳波

脳深部刺激療法(DBS)

迷走神経刺激(VNS)

- 消耗品

電極/リード

バッテリーとパルスジェネレーター

手術器具およびキット

外部アクセサリー

難治性てんかん治療の第一選択薬として抗てんかん薬(AED)が広く使用されていることから、薬物治療が引き続き主要セグメントとなっています。2024年の市場シェアは90.60%、予測期間の2025年~2035年のCAGRは6.87%です。薬剤製剤の継続的な進歩に加え、有効性が向上し副作用の少ない次世代AEDの入手可能性が高まっていることが、2035年までこのセグメントの成長を牽引すると予想されます。

セグメンテーション2:患者タイプ別

- 成人

- 小児

患者タイプ別にみると、世界の難治性てんかん治療市場は小児領域が牽引し、2024年のシェアは59.6%でした。小児は成人と比較しててんかん有病率が高いことから、難治性てんかん治療市場を独占すると予測されます。また、診断率の向上、高齢化の進展、成人におけるヘルスケア意識の高まりが、効果的な治療ソリューションに対する需要の高まりに寄与しています。

セグメンテーション3:発作タイプ別

- 局所性

- 全身性

発作タイプ別にみると、世界の難治性てんかん治療市場は局所性てんかんが牽引し、2024年のシェアは61.4%でした。局所てんかんは、難治性てんかんの症例に占める割合が高いことから、同市場を牽引することが予想されます。てんかんの症状は複雑かつ多様であるため、標準治療に対する抵抗性が高く、新しい薬理学的選択肢や神経調節技術を含む高度な治療アプローチが必要とされています。

セグメンテーション4:流通チャネル別

- 病院薬局

- 小売薬局

- オンライン薬局

流通チャネル別にみると、世界の難治性てんかん治療市場は病院薬局が牽引しており、2024年のシェアは45.7%でした。病院薬局は、専門的な薬剤や高度な治療インフラを利用できることから、流通チャネルを支配すると予測されています。病院ベースの治療プロトコルの増加や、難治性てんかんの重症例における入院治療の選好が、このセグメントの成長をさらに後押ししています。

セグメンテーション5:地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他

- アジア太平洋

- 日本

- インド

- 中国

- オーストラリア

- 韓国

- その他

- ラテンアメリカ

- ブラジル

- メキシコ

- その他

- 中東・アフリカ

- エジプト

- 南アフリカ

- その他

北米地域の難治性てんかん治療市場は、高い疾病負担、高度なヘルスケアインフラ、イノベーションへの強い注力を背景に、予測期間中に大きな成長率を示すと予想されます。同市場は、研究開発投資の増加、患者意識の高まり、診断能力の向上により、今後5年間で顕著な成長が見込まれます。最近の主な開発動向としては、治療抵抗性発作に有効であることを示したSK Life Science社のCenobamateのFDA承認や、Xenon Pharmaceuticals社のXEN1101のような有望候補の後期開発が進行中であることなどが挙げられます。主要企業は、有効性を向上させ副作用を最小限に抑えるために、新規作用機序や個別化医療のアプローチを積極的に追求しています。さらに、患者支援プログラムの拡充や官民の研究協力といった戦略的な取り組みにより、アクセスの向上と技術革新の加速が期待されています。

難治性てんかん治療市場における最近の動向

- 2024年6月、英国を拠点とするバイオテクノロジー企業EpilepsyGTxは、UCL Technology Fundが主導し、Health Technology Holdingも参加するシード資金として1,000万米ドルを確保しました。この資金は、前臨床試験の最終化と、焦点性難治性てんかんの治療を目的としたリード遺伝子治療候補薬EPY201のヒト初となる第1/2a相臨床試験の準備に充てられます。

- 2023年10月、NeuroPaceはてんかん治療の合理化を目的としたRNSシステムの大幅な機能強化を発表しました。これらのアップデートには、データレビューを改善するためのアップグレードされたnSightプラットフォーム、クリニックのワークフローを迅速化するための「Simple Set Programming」、シームレスな患者データ伝送のためのワイヤレス接続機能を備えた、新たにFDA承認されたポータブルタブレットリモートモニターなどが含まれます。

- 2023年6月、SK Biopharmaceuticalsは、同社のパートナーであるPaladin Labsが、従来の治療で十分なコントロールが得られない成人てんかん患者の部分発作を管理するための補助療法として、XCOPRI(セノバメート錠)の販売・流通承認をカナダ保健省から取得したと発表しました。Paladin Labs社は、患者さんのアクセスを確保するためにカナダの医療機関と協力しながら、2023年12月にXCOPRIをカナダで商業的に発売する予定です。

- 2023年2月、LivaNovaは、薬剤抵抗性てんかん患者に迷走神経刺激(VNS)療法を行うために設計されたデュアルピンヘッダーを特徴とする植込み型パルスジェネレーター(IPG)であるSenTiva DUOを発表しました。この進歩により、従来のデュアルピンシステムを使用している患者は、リードの交換を必要とせずに最新のVNS技術にアップグレードすることができ、発作制御を強化するためのカスタマイズ可能で自動化された治療オプションを提供することができます。

需要-促進要因、課題、機会

市場需要促進要因:

薬剤耐性てんかんの増加、新規治療薬のパイプラインの拡大 - 難治性てんかんとは、国際抗てんかん連盟(International League Against Epilepsy, ILAE)により、少なくとも2種類の抗てんかん薬(AED)を適切に選択し、忍容性を確認した上で十分な試験を行ったにもかかわらず、てんかん発作の持続的な消失が得られないてんかんと定義されています。このようなてんかん患者は、健康合併症、傷害や突然死(SUDEP)のリスクが高く、QOLが著しく低下します。このてんかんの有病率の増加は、ヘルスケアシステムの負担をさらに増大させています。

UChicago Medicineによると、世界中で推定6,500万人がてんかんを患っており、そのうちの30~40%、約2,000万~2,600万人が薬剤抵抗性または内科的難治性てんかんです。米国だけでも200万人以上の難治性てんかん患者がおり、1,000万~1,200万人のてんかん患者を抱えるインドでは、約30~40%(300万~400万人)が薬剤耐性であると推定され、世界的に治療格差が拡大しています。

アフリカ全域で薬物治療抵抗性てんかんと診断される患者数が増加していることが、この地域および世界の難治性てんかん治療市場の主要な促進要因となっています。2024年に出版された「アフリカにおける薬物治療抵抗性てんかんの手術 "A Review of Seizure Freedom Outcomes"」では、アフリカ全域のてんかん手術プログラムを体系的にレビューしています。このレビューでは、7つの患者コホートを対象とした8つの研究を分析し、QOLの改善やうつ病の重症度の低下とともに、60~100%の患者が術後1年以内に発作の消失を達成していることを明らかにしました。これらの転帰は、高所得地域で報告されている転帰に匹敵するものであり、アフリカにおける難治性てんかん手術プログラムの確立の可能性と有効性を示しています。ここに示したのは、アフリカで薬物治療抵抗性てんかんに対して様々な外科手術を受けた患者数のグラフです。CAHはcorticoamygdalohippocampectomy、SAHはselective amygdalohippocampectomyです。

市場の課題

患者アクセスに対する経済的制約:特に、難治性てんかん患者の多くは、新しい薬剤や高度な外科的治療、あるいは迷走神経刺激療法(VNS)や反応性神経刺激療法(RNS)のような機器を含む、複数の治療法の併用を必要とすることが多いため、患者アクセスの経済的制約は難治性てんかん治療市場にとって大きな課題です。これらの治療は法外に高価であるため、患者にとって経済的な障壁となり、市場の成長を制限しています。AED、特に近年難治性てんかんの治療薬として承認されたAEDは、高価格であることが多いです。AEDは発作を効果的に抑制することができますが、特に発展途上国や保険適用が限られている地域では、そのコストはヘルスケアシステムと患者の双方にとって負担となります。

市場成長を阻むその他の課題には、以下のようなものがある:

- 薬剤耐性てんかん(DRE)の基準を満たす患者の過小診断

市場機会:

難治性てんかん治療における神経調節デバイスの進歩 - 神経調節は、薬剤耐性てんかん(DRE)を管理するための革新的なアプローチとして登場し、従来の抗てんかん薬に反応しない患者に希望をもたらしています。最近の侵襲的・非侵襲的神経調節技術の進歩により、てんかん発作の制御が著しく向上し、患者の転帰が改善し、治療の選択肢が広がっています。これらの進歩は患者の予後を改善するだけでなく、治療法の展望を広げ、神経調節を難治性てんかん治療の中心的な要素と位置づけています。最先端技術と個別化された治療アプローチの統合は、市場のダイナミックな進化と薬剤耐性てんかんの複雑性への対応への取り組みを強調するものです。

市場動向:

診断と治療を強化するための高度画像診断の統合 - 難治性てんかん治療の動向は、先進イメージング技術、ゲノミクス、AIを活用したソリューションの統合により、高品質で個別化された治療を提供する方向にシフトしています。このアプローチは、がんなどの疾患を多面的に理解することで、診断や治療計画の正確性と有効性を高めます。ラジオミクスとAIは、医療画像から実用的な洞察を提供し、腫瘍の不均一性と患者固有の要因をより深く理解できるようにすることで、臨床の意思決定を変革しています。さらに、クラウドベースのプラットフォームと生物物理学的モデリングにより、リアルタイムの分析と個別化治療のシミュレーションが可能になり、臨床転帰がさらに改善されつつあります。これらの技術が進化するにつれて、従来の方法よりも優れた結果を提供する、高品質でオーダーメイドの治療に対する需要が高まると予想されます。

市場のその他の新たな動向には、以下のようなものがあります:

- 難治性てんかん治療における新たな標的療法

製品/イノベーション戦略:当レポートは、難治性てんかん治療における最新技術の進歩に関する深い洞察を提供し、企業がイノベーションを推進し、市場ニーズに合わせた最先端の製品を開発することを可能にします。

成長/マーケティング戦略:包括的な市場分析を提供し、主要な成長機会を特定することで、企業は的を絞ったマーケティング戦略を立案し、市場でのプレゼンスを効果的に拡大するための知識を得ることができます。

競合戦略:競合情勢の徹底的な分析により、競合企業の強みと弱みを把握し、市場における競争優位性を獲得するための効果的な戦略立案を支援します。

規制とコンプライアンス戦略:難治性てんかん治療薬の市場参入を加速させ、コンプライアンスを維持するために、進化する規制の枠組み、承認、業界ガイドラインに関する最新情報を提供します。

投資および事業拡大戦略:市場動向、資金調達パターン、提携機会を分析することで、企業が十分な情報に基づいた投資決定を下し、事業成長のための潜在的なM&A機会を特定できるよう支援します。

主要市場参入企業と競合情勢

企業プロファイルは、一次専門家から収集したインプットと、企業カバレッジ、製品ポートフォリオ、市場浸透度の分析に基づいて選定しています。

難治性てんかん治療市場の主要企業には、カルバマゼピンやフェニトインといった伝統的な薬剤から、セノバメート(Xcopri)やクロバザム(Onfi)といった新薬まで、さまざまな抗てんかん薬(AED)を提供する世界の大手製薬企業が含まれます。専門企業は、Dravet症候群やLennox-Gastaut症候群のような症候群を含む、稀で重篤なてんかんに焦点を当てています。バイオテクノロジー企業は、発作活動に関与するイオンチャネルを標的とする新規化合物の開発に取り組んでいます。低分子治療薬は、急性発作発生時により良い介入を行うために開発されています。てんかん症候群の調査では、光やその他の誘因に対して特異的な感受性を示す疾患について有望な結果が得られています。また、GABA-A受容体モジュレーターやその他の革新的な創薬標的を開発し、てんかん治療の改善に取り組んでいる企業もあります。難治性疾患に重点を置く企業は、てんかん重積状態や関連合併症を標的とした治療にも取り組んでいます。

当レポートでは、世界の難治性てんかん治療市場について調査し、市場の概要とともに、治療タイプ別、患者タイプ別、発作タイプ別、流通チャネル別、地域別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

エグゼクティブサマリー

第1章 市場:業界展望

- 主要なトレンド

- 難治性てんかん治療市場の動向

- 難治性てんかん治療のための新たな標的療法

- ビジネス戦略

- 企業戦略

- 市場機会

- スタートアップの情勢

- パイプライン薬、難治性てんかん治療

- 動向

- 難治性てんかん治療のための新たな標的療法

- 市場力学

第2章 治療タイプ別

- 治療の種類

- 薬理学的

- 非薬理学的

第3章 患者のタイプ別

- 患者タイプ

- 難治性てんかん治療市場(患者タイプ別)

- 成人

- 小児

第4章 発作タイプ別

- 発作の種類

- 難治性てんかん治療市場(発作型別)

- 局所性

- 全身性

第5章 流通チャネル

- 流通チャネル

- 病院薬局

- 小売薬局

- オンライン薬局

第6章 地域

- 地域のサマリー

- 北米

- 地域概要

- 市場成長促進要因

- 市場成長抑制要因

- 米国

- カナダ

- 欧州

- 地域概要

- 市場成長促進要因

- 市場成長抑制要因

- ドイツ

- フランス

- イタリア

- スペイン

- 英国

- その他

- アジア太平洋

- 地域概要

- 市場成長促進要因

- 市場成長抑制要因

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他

- ラテンアメリカ

- 地域概要

- 市場成長促進要因

- 市場成長抑制要因

- ブラジル

- メキシコ

- その他

- 中東・アフリカ

- 地域概要

- 市場成長促進要因

- エジプト

- サウジアラビア

- その他

第7章 市場-競合ベンチマーキングと企業プロファイル

- Biocodex-SP

- Eisai, Inc.

- GSK plc.

- LivaNova PLC

- NeuroPace, Inc.

- Novartis AG

- Teva Pharmaceutical Industries Ltd.

- UCB SA

- SK Biopharmaceuticals

- Janssen Global Services, LLC

第8章 調査手法

List of Figures

- Figure 1: Refractory Epilepsy Treatment Market (by Scenario), $Million, 2024, 2028, and 2035

- Figure 2: Global Refractory Epilepsy Treatment Market, 2024-2035

- Figure 3: Top 10 Countries, Global Refractory Epilepsy Treatment Market, $Million, 2024

- Figure 4: Timeline of Drugs Launched for Refractory Epilepsy Treatment

- Figure 5: Global Refractory Epilepsy Treatment Market Snapshot

- Figure 6: Global Refractory Epilepsy Treatment Market, $Million, 2024 and 2035

- Figure 7: Refractory Epilepsy Treatment Market (by Treatment Type), $Million, 2024, 2028, and 2035

- Figure 8: Refractory Epilepsy Treatment Market (by Patient Type), $Million, 2023, 2028, and 2035

- Figure 9: Refractory Epilepsy Treatment Market (by Seizure Type), $Million, 2024, 2028, and 2035

- Figure 10: Refractory Epilepsy Treatment Market (by Distribution Channel), $Million, 2024, 2028, and 2035

- Figure 11: Refractory Epilepsy Treatment Market Segmentation

- Figure 12: Surgical Procedures Performed on Patients with Medication-Resistant Epilepsy Treatment in Africa

- Figure 13: Global Refractory Epilepsy Treatment Market, By Treatment Type, 2023, 2028, and 2035

- Figure 14: Major Drugs for Refractory Epilepsy Treatment

- Figure 15: Pharmacological Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 16: Global Refractory Epilepsy Treatment Market, By Drug Class, 2023, 2028, and 2035

- Figure 17: First-Generation Drugs Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 18: Valporic Acid Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 19: Topiramate Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 20: Carbamazepine Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 21: Clobazam Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 22: Other First-Generation Drugs Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 23: Second-Generation Drugs Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 24: Zonisamide Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 25: Oxcarbazepine Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 26: Tigabine Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 27: Rufinamide Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 28: Other Drugs Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 29: Global Refractory Epilepsy Treatment Market, by New and Emerging Drugs, $Million, 2023, 2028, and 2035

- Figure 30: Cenobamate Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 31: Ganaxalone Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 32: Other New and Emerging Drugs Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 33: Combination Drugs Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 34: Global Refractory Epilepsy Treatment Market, by Surgical and Neurostimulation Devices Market, $Million, 2023, 2028, and 2035

- Figure 35: Surgical and Neurostimulation Devices Market, $Million, 2023-2035

- Figure 36: Resective Surgery Devices Market, $Million, 2023-2035

- Figure 37: LiTT Market, $Million, 2023-2035

- Figure 38: SEEG Market, $Million, 2023-2035

- Figure 39: VNS and RNS System Market, $Million, 2023-2035

- Figure 40: DBS System Market, $Million, 2023-2035

- Figure 41: Global Refractory Epilepsy Treatment Market, by Consumables, 2023, 2028, and 2035

- Figure 42: Electrodes/Leads Market, $Million, 2023-2035

- Figure 43: Batteries and Pulse Generators Market, $Million, 2023-2035

- Figure 44: Surgical Tools and Kits Market, $Million, 2023-2035

- Figure 45: External Accessories Market, $Million, 2023-2035

- Figure 46: Global Refractory Epilepsy Treatment Market, by Patient Type, 2023, 2028, and 2035

- Figure 47: Global Refractory Epilepsy Treatment Market, by Adults, $Million, 2023-2035

- Figure 48: Global Refractory Epilepsy Treatment Market, by Paediatrics , $Million, 2023-2035

- Figure 49: Global Refractory Epilepsy Treatment Market, by Seizure Type, 2023, 2028, and 2035

- Figure 50: Global Refractory Epilepsy Treatment Market, by Focal Type , $Million, 2023-2035

- Figure 51: Global Refractory Epilepsy Treatment Market, by Generalised Type , $Million, 2023-2035

- Figure 52: Global Refractory Epilepsy Treatment Market,by Distribution Channel, 2023, 2028, and 2035

- Figure 53: Global Refractory Epilepsy Treatment Market, by Hospital Pharmacy , $Million, 2023-2035

- Figure 54: Global Refractory Epilepsy Treatment Market, by Retail Pharmacy , $Million, 2023-2035

- Figure 55: Global Refractory Epilepsy Treatment Market, by Online Pharmacy , $Million, 2023-2035

- Figure 56: North America Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 57: U.S. Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 58: Canada Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 59: Europe Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 60: Germany Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 61: France Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 62: Italy Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 63: Spain Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 64: U.K. Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 65: Rest-of-Europe Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 66: Asia-Pacific Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 67: China Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 68: Japan Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 69: India Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 70: South Korea Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 71: Australia Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 72: Rest-of-Asia-Pacific Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 73: Latin America Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 74: Brazil Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 75: Mexico Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 76: Rest-of-Latin-America Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 77: Middle East and Africa Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 78: Egypt Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 79: Saudi Arabia Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 80: Rest-of-MEA Refractory Epilepsy Treatment Market, $Million, 2023-2035

- Figure 81: Inclusion and Exclusion

- Figure 82: Data Triangulation

- Figure 83: Top-Down and Bottom-Up Approach

- Figure 84: Assumptions and Limitations

List of Tables

- Table 1: Market Snapshot

- Table 2: Recent Investments in Refractory Epilepsy Treatment

- Table 3: Key Development in Seizure Management by Key Companies

- Table 4: Start-ups and Investment Landscape

- Table 5: Pipeline Drugs and its Clinical Trial Phase

- Table 6: Recent Investments in Refractory Epilepsy Treatment

- Table 7: Major Development in the Refractory Epilepsy Treatment Market

- Table 8: Major Development in Refractory Epilepsy Treatment Market

- Table 9: Major Drugs and Their Indication

- Table 10: Major Devices Used in the Refractory Epilepsy Treatment Market

- Table 11: Refractory Epilepsy Treatment Market (by Regio), $Million, 2023-2035

- Table 12: North America Refractory Epilepsy Treatment Market (By Country), $Million, 2023-2035

- Table 13: Europe Refractory Epilepsy Treatment Market (By Country), $Million, 2023-2035

- Table 14: Asia-Pacific Refractory Epilepsy Treatment Market (By Country), $Million, 2023-2035

- Table 15: LATAM Refractory Epilepsy Treatment Market (By Country), $Million, 2023-2035

- Table 16: Middle East and Africa Refractory Epilepsy Treatment Market (By Country), $Million, 2023-2035

This report can be delivered within 1 working day.

Introduction of Refractory Epilepsy Treatment

Refractory epilepsy treatment utilizes an individual's distinct clinical, molecular, and lifestyle data to inform the diagnosis, treatment, and prevention of cancer, inherited diseases, and other complex conditions. Refractory epilepsy treatment represents a transformative shift in healthcare, moving away from the traditional one-size-fits-all approach to a more tailored and targeted therapeutic strategy. By leveraging advancements in genomics, molecular diagnostics, and data analytics, Refractory epilepsy treatment enables healthcare providers to craft personalized treatment plans based on an individual's genetic, environmental, and lifestyle factors. This approach not only promises to enhance the effectiveness of treatments but also reduces unnecessary trial-and-error, leading to better patient outcomes and reduced healthcare costs. As the field continues to evolve, large-scale population studies and cutting-edge technologies are paving the way for more accurate disease predictions, early diagnoses, and optimized therapeutic interventions.

| KEY MARKET STATISTICS | |

|---|---|

| Forecast Period | 2025 - 2035 |

| 2025 Evaluation | $4,902.4 Million |

| 2035 Forecast | $9,472.6 Million |

| CAGR | 6.71% |

Market Introduction

The global refractory epilepsy treatment market is expected to witness substantial growth, projected to reach $9,472.6 million by 2035. The global refractory epilepsy treatment market is experiencing consistent growth, driven by the increasing prevalence of epilepsy and the limitations of conventional anti-seizure medications, which fail to control seizures in approximately 30-40% of patients. This significant unmet clinical need is transforming the market landscape, spurring demand for advanced treatment options such as neurostimulation therapies (including VNS, RNS, and DBS), surgical interventions, and innovative therapeutics like cannabidiol and next-generation anti-seizure medications. Growth is further supported by rising awareness, enhanced diagnostic capabilities, and broader healthcare access in emerging markets. Nonetheless, barriers such as high treatment costs, complex regulatory requirements, and uneven access to specialized care continue to hinder widespread adoption. As the field moves toward more personalized, device-integrated, and precision-targeted solutions, the refractory epilepsy treatment market stands at the forefront of urgent clinical need and evolving commercial potential.

Refractory epilepsy, also known as drug-resistant epilepsy (DRE), affects approximately 30% of all epilepsy patients, who do not respond adequately to at least two anti-seizure medications (ASMs). This condition represents a high unmet clinical need, driving both pharmaceutical and device innovation. Refractory epilepsy, affects roughly 30% of the global epilepsy population, representing a significant unmet medical need. This subset of patients fails to achieve seizure control despite trials of two or more anti-seizure medications (ASMs), driving demand for innovative therapies. The competitive landscape is diverse and rapidly evolving, spanning pharmaceutical, device, and emerging gene therapy sectors. Traditional ASMs, such as UCB Pharma's brivaracetam and SK Life Science's cenobamate, continue to advance with a focus on improved efficacy and tolerability, exemplified by cenobamate's clinical trials showing notable seizure freedom rates. Meanwhile, neuromodulation devices-like LivaNova's vagus nerve stimulation and NeuroPace's responsive neurostimulation system-offer alternative approaches targeting neural circuits, particularly for patients with focal epilepsy not amenable to surgery.

Additionally, cell and gene therapies, though still in early stages, promise transformative potential for rare genetic epilepsies such as Dravet syndrome, reflecting a shift towards precision medicine. Market growth is supported by regulatory incentives and increasing payer acceptance, particularly as real-world data validate the long-term benefits of these advanced therapies. Overall, the refractory epilepsy treatment landscape resembles a multi-modal transportation system navigating difficult terrain: conventional drugs serve broad populations but with limited efficacy, neuromodulation provides more precise control albeit at higher cost, and emerging genetic therapies hold the promise of a targeted, curative path for select patients.

Industrial Impact

Refractory epilepsy treatment is reshaping the healthcare industry by enabling personalized treatments that significantly improve patient outcomes. For instance, the use of genetic profiling in oncology has led to the development of targeted therapies such as Herceptin for breast cancer, which is specifically designed to treat patients with HER2-positive tumors. In addition to improving individual patient care, Refractory epilepsy treatment is driving innovation across the healthcare ecosystem, particularly in drug discovery and clinical trials. The pharmaceutical industry is leveraging genomics to discover new drug targets, as seen in the development of the breakthrough drug Kymriah, a CAR-T therapy for leukemia, which was developed through the identification of genetic markers specific to the disease. Clinical trials are also becoming more targeted, with companies such as Novartis and Pfizer using genomic data to stratify patient populations and improve trial efficiency. Moreover, the integration of refractory epilepsy treatment into population health management is evident in initiatives such as Geisinger Health System's MyCode Community Health Initiative, which offers genomic sequencing to patients to improve preventive care and early disease detection. This growing application of refractory epilepsy treatment has not only improved individual treatment outcomes but has also helped to optimize healthcare delivery systems, reduce costs, and accelerate the development of new therapies.

Market Segmentation:

Segmentation 1: By Treatment Type

- Pharmacological

- Drug Class

First-Generation Drugs

Second-Generation Drugs

New and Emerging Drugs

Combination Drugs

- Non-Pharmacoogical

- Surgical and Neurostimulation Devices

Resective Surgery Devices

Laser Interstitial Thermal Therapy (LiTT)

Stereotactic EEG

Deep Brain Stimulation (DBS)

Vagus Nerve Stimulation (VNS)

- Consumables

Electrodes/Leads

Batteries and Pulse Generators

Surgical Tools and Kits

External Accessories

Pharmacological treatment remains the leading segment due to the widespread use of anti-epileptic drugs (AEDs) as the first-line approach for managing refractory epilepsy. The segment holds a market share of 90.60% in 2024 with a CAGR of 6.87% during the forecast period 2025-2035. Continuous advancements in drug formulations, coupled with the increasing availability of next-generation AEDs with improved efficacy and fewer side effects, are expected to drive growth in this segment through 2035.

Segmentation 2: By Patient Type

- Adult

- Paediatrics

Based on patient type, the global refractory epilepsy treatment market was led by the paedaitrics segment, which held a 59.6% share in 2024. The paediatric population is projected to dominate the refractory epilepsy treatment market due to a higher prevalence of epilepsy among children compared to adults. Additionally, improved diagnosis rates, a growing aging population, and higher healthcare awareness in adult groups contribute to the rising demand for effective treatment solutions.

Segmentation 3: By Seizure Type

- Focal

- Generalised

Based on seizure ype, the global refractory epilepsy treatment market was led by the focal segment, which held a 61.4% share in 2024. Focal epilepsy is expected to lead the market as it accounts for a significant proportion of refractory epilepsy cases. Its complex and variable presentation often makes it resistant to standard therapies, driving the need for advanced treatment approaches, including newer pharmacological options and neuromodulation techniques

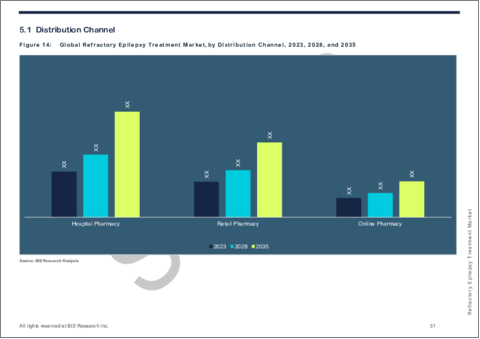

Segmentation 4: By Distribution Channel

- Hospital Pharmacy

- Retail Pharmacy

- Online Pharmacy

Based on distribution channel, the global refractory epilepsy treatment market was led by the hospital pharmacy segment, which held a 45.7% share in 2024. Hospital pharmacies are anticipated to dominate the distribution channel due to their access to specialized medications and advanced treatment infrastructure. The rising number of hospital-based treatment protocols and the preference for inpatient care in severe cases of refractory epilepsy further support this segment's growth.

Segmentation 5: By Region

- North America

- U.S.

- Canada

- Europe

- Germany

- U.K.

- France

- Italy

- Spain

- Rest-of-Europe

- Asia-Pacific

- Japan

- India

- China

- Australia

- South Korea

- Rest-of-Asia-Pacific

- Latin America

- Brazil

- Mexico

- Rest-of-Latin America

- Middle East and Africa

- Egypt

- South Africa

- Rest-of-Middle East and Africa

The refractory epilepsy treatment market in the North America region is expected to witness a significant growth rate during the forecast period, marked by a high disease burden, advanced healthcare infrastructure, and a strong focus on innovation. The market is expected to witness notable growth over the next five years due to increasing R&D investments, rising patient awareness, and improved diagnostic capabilities. Key developments include the FDA's recent approval of Cenobamate by SK Life Science, which has demonstrated effectiveness in treatment-resistant seizures, and the ongoing late-stage development of promising candidates such as XEN1101 by Xenon Pharmaceuticals. Leading companies are actively pursuing novel mechanisms of action and personalized medicine approaches to improve efficacy and minimize side effects. Additionally, strategic initiatives like expanded patient assistance programs and public-private research collaborations are expected to enhance access and accelerate innovation.

Recent Developments in the Refractory Epilepsy Treatment Market

- In June 2024, EpilepsyGTx, a U.K.-based biotechnology company, secured USD 10 million in seed funding led by the UCL Technology Fund, with participation from Health Technology Holding. The funds have been allocated to finalize preclinical studies and prepare for a first-in-human Phase 1/2a clinical trial of their lead gene therapy candidate, EPY201, aimed at treating focal refractory epilepsy.

- In October 2023, NeuroPace introduced significant enhancements to its RNS System aimed at streamlining epilepsy care. These updates include an upgraded nSight Platform for improved data review, 'Simple Set Programming' to expedite clinic workflows, and a newly FDA-approved, portable Tablet Remote Monitor with wireless connectivity for seamless patient data transmission.

- In June 2023, SK Biopharmaceuticals announced that its partner, Paladin Labs, received approval from Health Canada to market and distribute XCOPRI (cenobamate tablets) for adjunctive therapy in managing partial-onset seizures in adults with epilepsy who are not satisfactorily controlled with conventional therapy. Paladin Labs plans to commercially launch XCOPRI in Canada in December 2023, collaborating with Canadian health agencies to ensure patient access.

- In Feb 2023, LivaNova introduced the SenTiva DUO, an implantable pulse generator (IPG) featuring a dual-pin header designed to deliver Vagus Nerve Stimulation (VNS) therapy for individuals with drug-resistant epilepsy. This advancement allows patients with legacy dual-pin systems to upgrade to the latest VNS technology without requiring lead replacement, offering customizable and automated therapy options to enhance seizure control.

Demand -Drivers, Challenges, and Opportunities

Market Demand Drivers:

Increasing prevalence of drug-resistant epilepsy and ever expanding pipeline of novel therapeutics: Refractory epilepsy is defined by the International League Against Epilepsy (ILAE) as the failure to achieve sustained seizure freedom after adequate trials of at least two appropriately chosen and tolerated anti-epileptic drugs (AEDs). Individuals with this form of epilepsy face greater health complications, increased risk of injury or sudden death (SUDEP), and significantly reduced quality of life. The rising prevalence of this epilepsy further amplifies the burden on healthcare systems.

According to UChicago Medicine, an estimated 65 million people worldwide live with epilepsy, and among those, 30-40 percent, roughly 20-26 million individuals, have drug-resistant or medically refractory epilepsy, meaning they fail to achieve sustained seizure control despite trials of two or more appropriate antiseizure medications. In the U.S. alone, there are over 2 million people with refractory epilepsy, and in India, where 10-12 million people have epilepsy, approximately 30-40 percent (3-4 million) are estimated to be drug-resistant, underscoring a substantial and growing treatment gap worldwide.

The increasing number of patients diagnosed with medication-refractory epilepsy across Africa has emerged as a key driver for the regional and global refractory epilepsy treatment market. "Surgery for Medication Refractory Epilepsy in Africa: A Review of Seizure Freedom Outcomes", published in 2024, systematically reviews epilepsy surgery programs across Africa. Analyzing eight studies representing seven unique patient cohorts, the review found that 60-100% of patients achieved seizure freedom within a year post-surgery, alongside improvements in quality of life and reduced depression severity. These outcomes are comparable to those reported in higher-income regions, demonstrating the feasibility and effectiveness of establishing refractory epilepsy surgery programs in Africa. Given here is a graphical representation of the number of patients undergoing various surgical procedures for medication-refractory epilepsy in Africa. CAH, corticoamygdalohippocampectomy; SAH, selective amygdalohippocampectomy.

Some of the other driving factors include:

- Growing Impact of Orphan Drug Development and Role of Addvcacy Group and Awareness Programs

- Emerging Treatment Modalities in Refractory Epilepsy

Note: All of the above factors will be evaluated in detail in the report.

Market Challenges:

Financial Constraints on Patient Access: The financial constraints on patient access are a significant challenge for the refractory epilepsy treatment market, particularly because many patients with refractory epilepsy often require a combination of therapies, including newer medications, advanced surgical options, or devices like Vagus Nerve Stimulation (VNS) or Responsive Neurostimulation (RNS). These treatments can be prohibitively expensive, creating financial barriers for patients and limiting market growth. AEDs, especially those approved in recent years for refractory epilepsy, often come with high price tags. Although they may offer effective seizure control, their cost can be a burden for both healthcare systems and patients, especially in developing countries or where insurance coverage is limited.

Some of the other factors challenging the market growth include:

- Under diagnosis of patients who meet the criteria of drug-resistant epilepsy (DRE)

Note: All of the above factors will be evaluated in detail in the report.

Market Opportunities:

Advances in Neuromodulation Devices in Refractory Epilepsy Treatment Market: Neuromodulation has emerged as a transformative approach for managing drug-resistant epilepsy (DRE), offering hope to patients unresponsive to conventional antiseizure medications. Recent advancements in both invasive and non-invasive neuromodulation technologies have significantly enhanced seizure control, improved patient outcomes, and expanded therapeutic options. These advancements not only enhance patient outcomes but also expand the therapeutic landscape, positioning neuromodulation as a central component in the management of refractory epilepsy. The integration of cutting-edge technologies and personalized treatment approaches underscores the market's dynamic evolution and its commitment to addressing the complexities of drug-resistant epilepsy.

Some of the other factors creating an opportunity for market growth include:

- Shift from neo-adjuvant approaches driven by diagnostic advancements

Note: All of the above factors will be evaluated in detail in the report.

Market Trends:

Integrating Advanced Imaging for Enhanced Diagnostics and Treatment: The trend in Refractory Epilepsy Treatment is shifting toward delivering high-quality, personalized care through the integration of advanced imaging technologies, genomics, and AI-driven solutions. This approach enhances the accuracy and effectiveness of diagnoses and treatment plans by offering a multi-dimensional understanding of diseases such as cancer. Radiomics and AI are transforming clinical decision-making by providing actionable insights from medical images, enabling a deeper understanding of tumor heterogeneity and patient-specific factors. Additionally, cloud-based platforms and biophysical modeling are allowing for real-time analysis and personalized treatment simulations, further improving clinical outcomes. As these technologies evolve, the demand for high-quality, tailored therapies is expected to rise, offering better results than traditional methods.

Some of the other emerging trends in the market include:

- Emerging Targeted Therapy for Refractory Epilepsy Treatment

Note: All of the above trends will be evaluated in detail in the report.

How can this report add value to an organization?

Product/Innovation Strategy: The report offers in-depth insights into the latest technological advancements in refractory epilepsy treatment, enabling organizations to drive innovation and develop cutting-edge products tailored to market needs.

Growth/Marketing Strategy: By providing comprehensive market analysis and identifying key growth opportunities, the report equips organizations with the knowledge to craft targeted marketing strategies and expand their market presence effectively.

Competitive Strategy: The report includes a thorough competitive landscape analysis, helping organizations understand their competitors' strengths and weaknesses and allowing them to strategize effectively to gain a competitive edge in the market.

Regulatory and Compliance Strategy: It provides updates on evolving regulatory frameworks, approvals, and industry guidelines, ensuring organizations stay compliant and accelerate market entry for new Refractory Epilepsy Treatment solutions.

Investment and Business Expansion Strategy: By analyzing market trends, funding patterns, and partnership opportunities, the report assists organizations in making informed investment decisions and identifying potential M&A opportunities for business growth.

Methodology

Key Considerations and Assumptions in Market Engineering and Validation

- The base year considered for the calculation of the market size is 2023. A historical year analysis has been done for the period FY2022-FY2023. The market size has been estimated for FY2024 and projected for the period FY2025-FY2035.

- The scope of this report has been carefully derived based on interactions with experts in different companies across the world. This report provides a market study of applied sciences, precision diagnostics, digital health and information technology, and precision therapeutics products of the refractory epilepsy treatment market.

- The market contribution of the precision therapeutics anticipated to be launched in the future has been calculated based on the historical analysis of the products.

- Revenues of the companies have been referenced from their annual reports for FY2023 and FY2024. For private companies, revenues have been estimated based on factors such as inputs obtained from primary research, funding history, market collaborations, and operational history.

- The market has been mapped based on the available refractory epilepsy treatment solutions. All the key companies with significant offerings in this field have been considered and profiled in this report.

Primary Research:

The primary sources involve industry experts in Refractory Epilepsy Treatment, including the market players offering products and services. Resources such as CEOs, vice presidents, marketing directors, and technology and innovation directors have been interviewed to obtain and verify both qualitative and quantitative aspects of this research study.

The key data points taken from the primary sources include:

- Validation and triangulation of all the numbers and graphs

- Validation of the report's segmentation and key qualitative findings

- Understanding the competitive landscape and business model

- Current and proposed production values of a product by market players

- Validation of the numbers of the different segments of the market in focus

- Percentage split of individual markets for regional analysis

Secondary Research

Open Sources

- Certified publications, articles from recognized authors, white papers, directories, and major databases, among others

- Annual reports, SEC filings, and investor presentations of the leading market players

- Company websites and detailed study of their product portfolio

- Gold standard magazines, journals, white papers, press releases, and news articles

- Paid databases

The key data points taken from the secondary sources include:

- Segmentations and percentage shares

- Data for market value

- Key industry trends of the top players of the market

- Qualitative insights into various aspects of the market, key trends, and emerging areas of innovation

- Quantitative data for mathematical and statistical calculations

Key Market Players and Competition Synopsis

Profiled companies have been selected based on inputs gathered from primary experts, as well as analyzing company coverage, product portfolio, and market penetration.

Key players in the refractory epilepsy treatment market include major global pharmaceutical companies offer a range of antiepileptic drugs (AEDs), including traditional drugs like carbamazepine and phenytoin, as well as newer medications such as cenobamate (Xcopri) and clobazam (Onfi). Specialty companies focus on rare and severe forms of epilepsy, including syndromes like Dravet syndrome and Lennox-Gastaut syndrome. Biotech companies are working on developing novel compounds that target ion channels involved in seizure activity. Small molecule therapies are being developed to offer better intervention during acute seizure events. Research into epilepsy syndromes is yielding promising results for disorders with unique sensitivities to light and other triggers. Other companies are working on GABA-A receptor modulators and other innovative drug targets to improve epilepsy treatment. Companies with a focus on refractory conditions also work on therapies targeting status epilepticus and related complications.

Some prominent names established in this market are:

- Teva Pharmaceuticals Industries Ltd.

- Janssen Global Services, LLC

- SK Biopharmaceuticals

- UCB S.A.

- Novartis AG

- NeuroPace, Inc.

- LivaNova PLC

- GSK plc.

- Eisai, Inc.

- Biocodex-SP

Table of Contents

Executive Summary

Scope and Definition

1 Market: Industry Outlook

- 1.1 Major Trend

- 1.2 Trend in Refractory Epilepsy Treatment Market

- 1.2.1 Emerging Targeted Therapy for Refractory Epilepsy Treatment

- 1.2.2 Business Strategies

- 1.2.2.1 Product Developments

- 1.2.2.2 Market Developments

- 1.2.3 Corporate Strategies

- 1.2.3.1 Partnerships and Joint Ventures

- 1.2.4 Market Opportunities

- 1.2.4.1 Advances in Neuromodulation Devices in the Refractory Epilepsy Treatment Market

- 1.2.4.2 Shift from Neo-Adjuvant Approaches Driven by Diagnostic Advancements

- 1.3 Start-Ups Landscape

- 1.3.1 Key Start-Ups in the Ecosystem

- 1.4 Pipeline Drugs, Refractory Epilepsy Treatment

- 1.5 Trends

- 1.5.1 Emerging Targeted Therapy for Refractory Epilepsy Treatment

- 1.6 Market Dynamics

- 1.6.1 Trends, Drivers, Challenges, and Opportunities: Current and Future Impact Assessment

- 1.6.2 Market Drivers

- 1.6.2.1 Increasing Prevalence of Drug-resistant Epilepsy and Ever-expanding Pipeline of Novel Therapeutics

- 1.6.2.2 Growing Impact of Orphan Drug Development and Role of Advocacy Groups and Awareness Programs

- 1.6.2.3 Emerging Treatment Modalities in Refractory Epilepsy

- 1.6.3 Market Restraints

- 1.6.3.1 Off-Label Medication Practices Hindering the Refractory Epilepsy Treatment Market

- 1.6.3.2 High R&D Cost as a Barrier to New Entry for New and Small-Scale Companies

- 1.6.4 Market Opportunities

- 1.6.4.1 Advances in Neuromodulation Devices in the Refractory Epilepsy Treatment Market

- 1.6.4.2 Shift from Neo-Adjuvant Approaches Driven by Diagnostic Advancements

- 1.6.5 Market Challenges

- 1.6.5.1 Financial Constraints on Patient Access

- 1.6.5.2 Underdiagnosis of Patients who Meet the Criteria for Drug-Resistant Epilepsy (DRE)

2 Treatment Type

- 2.1 Treatment Type

- 2.1.1 Overview

- 2.2 Pharmacological

- 2.2.1 By Drug Class

- 2.2.1.1 First-Generation Drugs

- 2.2.1.1.1 Valporic Acid (Brand: Depakene) or Valporate

- 2.2.1.1.2 Topiramate (Brand: Topamax)

- 2.2.1.1.3 Carbamazepine (Brand: Tegretol, Carbatrol)

- 2.2.1.1.4 Clobazam (Brand: Onfi)

- 2.2.1.1.5 Other Drugs

- 2.2.1.2 Second-Generation Drugs

- 2.2.1.2.1 Zonisamide (Brand: Zonegran)

- 2.2.1.2.2 Oxcarbazepine

- 2.2.1.2.3 Tigabine (Brand: Gabitril)

- 2.2.1.2.4 Rufinamide (Brand: Banzel)

- 2.2.1.2.5 Other Drugs

- 2.2.1.3 New and Emerging Drugs

- 2.2.1.3.1 Cenobamate (Brand: Xcopri)

- 2.2.1.3.1 Ganaxolone

- 2.2.1.3.2 Other New and Emerging Drugs

- 2.2.1.4 Combination Drugs

- 2.2.1.4.1 Valproic acid (VPA) with Lamotrigine

- 2.2.1.4.2 Levetiracetam (LEV) with Carbamazepine (CBZ)

- 2.2.1.1 First-Generation Drugs

- 2.2.1 By Drug Class

- 2.3 Non-Pharmacological

- 2.3.1 Surgical and Neurostimulation Devices

- 2.3.1.1 Surgical and Neurostimulation Devices

- 2.3.1.1.1 Resective Surgery Devices

- 2.3.1.1.2 Laser Interstitial thermal therapy, or LiTT

- 2.3.1.1.3 SEEG (Stereotactic EEG)

- 2.3.1.1.4 Vagus Nerve Stimulation (VNS) & Responsive Neurostimulation (RNS) System

- 2.3.1.1.5 Deep brain stimulation (DBS)

- 2.3.1.2 Consumables

- 2.3.1.2.1 Electrodes/Leads

- 2.3.1.2.2 Batteries and Pulse Generators

- 2.3.1.2.3 Surgical Tools and Kits

- 2.3.1.2.4 External Accessories

- 2.3.1.1 Surgical and Neurostimulation Devices

- 2.3.1 Surgical and Neurostimulation Devices

3 Patient Type

- 3.1 Patient Type

- 3.1.1 Overview

- 3.2 Refractory Epilepsy Treatment Market (by Patient Type)

- 3.2.1 Adults

- 3.2.2 Paediatrics

4 Seizure Type

- 4.1 Seizure Type

- 4.1.1 Overview

- 4.2 Refractory Epilepsy Treatment Market (by Seizure Type)

- 4.2.1 Focal Type

- 4.2.2 Generalized Type

5 Distribution Channel

- 5.1 Distribution Channel

- 5.1.1 Hospital Pharmacy

- 5.1.2 Retail Pharmacy

- 5.1.3 Online Pharmacy

6 Region

- 6.1 Regional Summary

- 6.2 North America

- 6.2.1 Regional Overview

- 6.2.2 Driving Factors for Market Growth

- 6.2.3 Factors Challenging the Market

- 6.2.4 U.S.

- 6.2.5 Canada

- 6.3 Europe

- 6.3.1 Regional Overview

- 6.3.2 Driving Factors for Market Growth

- 6.3.3 Factors Challenging the Market

- 6.3.4 Germany

- 6.3.5 France

- 6.3.6 Italy

- 6.3.7 Spain

- 6.3.8 U.K.

- 6.3.9 Rest-of-Europe

- 6.4 Asia-Pacific

- 6.4.1 Regional Overview

- 6.4.2 Driving Factors for Market Growth

- 6.4.3 Factors Challenging the Market

- 6.4.4 China

- 6.4.5 Japan

- 6.4.6 India

- 6.4.7 South Korea

- 6.4.8 Australia

- 6.4.9 Rest-of-Asia-Pacific

- 6.5 Latin America

- 6.5.1 Regional Overview

- 6.5.2 Driving Factors for Market Growth

- 6.5.3 Factors Challenging the Market

- 6.5.4 Brazil

- 6.5.5 Mexico

- 6.5.6 Rest-of-Latin-America

- 6.6 Middle East and Africa

- 6.6.1 Regional Overview

- 6.6.2 Driving Factors for Market Growth

- 6.6.3 Egypt

- 6.6.4 Saudi Arabia

- 6.6.5 Rest-of-MEA

7 Markets - Competitive Benchmarking & Company Profiles

- 7.1 Biocodex-SP

- 7.1.1 Overview

- 7.1.2 Top Products/Product Portfolio

- 7.1.3 Top Competitors

- 7.1.4 Target Customers

- 7.1.5 Strategic Positioning and Market Impact

- 7.1.6 Analyst View

- 7.1.7 Pipeline and Research Initiatives

- 7.2 Eisai, Inc.

- 7.2.1 Overview

- 7.2.2 Top Products/Product Portfolio

- 7.2.3 Top Competitors

- 7.2.4 Strategic Positioning and Market Impact

- 7.2.5 Key Personal

- 7.2.6 Analyst View

- 7.2.7 Research Initiatives

- 7.3 GSK plc.

- 7.3.1 Overview

- 7.3.2 Top Products/Product Portfolio

- 7.3.3 Top Competitors

- 7.3.4 Target Customers

- 7.3.5 Strategic Positioning and Market Impact

- 7.3.6 Analyst View

- 7.3.7 Research Initiatives

- 7.4 LivaNova PLC

- 7.4.1 Overview

- 7.4.2 Top Products/Product Portfolio

- 7.4.3 Top Competitors

- 7.4.4 Target Customers

- 7.4.5 Strategic Positioning and Market Impact

- 7.4.6 Analyst View

- 7.4.7 Research Initiatives

- 7.5 NeuroPace, Inc.

- 7.5.1 Overview

- 7.5.2 Top Products/Product Portfolio

- 7.5.3 Top Competitors

- 7.5.4 Target Customers

- 7.5.5 Strategic Positioning and Market Impact

- 7.5.6 Analyst View

- 7.5.7 Pipeline and Research Initiatives

- 7.6 Novartis AG

- 7.6.1 Overview

- 7.6.2 Top Products/Product Portfolio

- 7.6.3 Top Competitors

- 7.6.4 Target Customers

- 7.6.5 Strategic Positioning and Market Impact

- 7.6.6 Analyst View

- 7.6.7 Pipeline and Research Initiatives

- 7.7 Teva Pharmaceutical Industries Ltd.

- 7.7.1 Overview

- 7.7.2 Top Products/Product Portfolio

- 7.7.3 Top Competitors

- 7.7.4 Target Customers

- 7.7.5 Strategic Positioning and Market Impact

- 7.7.6 Analyst View

- 7.7.7 Pipeline and Research Initiatives

- 7.8 UCB S.A.

- 7.8.1 Overview

- 7.8.2 Top Products/Product Portfolio

- 7.8.3 Top Competitors

- 7.8.4 Target Customers

- 7.8.5 Strategic Positioning and Market Impact

- 7.8.6 Analyst View

- 7.8.7 Pipeline and Research Initiative

- 7.9 SK Biopharmaceuticals

- 7.9.1 Overview

- 7.9.2 Top Products/Product Portfolio

- 7.9.3 Top Competitors

- 7.9.4 Target Customers

- 7.9.5 Strategic Positioning and Market Impact

- 7.9.6 Analyst View

- 7.9.7 Research Initiatives

- 7.1 Janssen Global Services, LLC

- 7.10.1 Overview

- 7.10.2 Top Products/Product Portfolio

- 7.10.3 Top Competitors

- 7.10.4 Target Customers

- 7.10.5 Strategic Positioning and Market Impact

- 7.10.6 Analyst View

- 7.10.7 Research Initiatives

8 Research Methodology

- 8.1 Data Sources

- 8.1.1 Primary Data Sources

- 8.1.2 Secondary Data Sources

- 8.1.3 Inclusion and Exclusion

- 8.1.4 Data Triangulation

- 8.2 Market Estimation and Forecast