|

|

市場調査レポート

商品コード

1747201

電気自動車用複合材料市場- 世界および地域別分析:繊維タイプ別、樹脂タイプ別、製造プロセス別、用途別、地域別 - 分析と予測(2025年~2034年)Electric Vehicle Composites Market - A Global and Regional Analysis: Focus on Fiber Type, Resin Type, Manufacturing Process, Application, and Regional Analysis - Analysis and Forecast, 2025-2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 電気自動車用複合材料市場- 世界および地域別分析:繊維タイプ別、樹脂タイプ別、製造プロセス別、用途別、地域別 - 分析と予測(2025年~2034年) |

|

出版日: 2025年06月13日

発行: BIS Research

ページ情報: 英文 150 Pages

納期: 1~5営業日

|

全表示

- 概要

- 図表

- 目次

電気自動車用複合材料市場は、自動車材料業界の中でも重要なセグメントであり、複合材料は電気自動車設計の中心となる軽量化戦略において不可欠な役割を果たしています。

繊維の種類、樹脂の配合、製造プロセスにおける技術の進歩により、電気自動車の構造部品および非構造部品に使用される複合材料の強度対重量比、耐久性、持続可能性が改善され続けています。熱・音響管理、バッテリー筐体、ドライブトレイン部品は、厳しい安全基準と効率基準を満たすために、複合材料ソリューションを取り入れることが増えています。電気自動車用複合材料市場は、コスト削減、リサイクル性の向上、樹脂トランスファー成形や積層造形などの自動化製造技術との統合に焦点を当てた研究開発への投資が活発化していることが特典となっています。

電気自動車用複合材料の世界市場ライフサイクルステージ

| 主要市場統計 | |

|---|---|

| 予測期間 | 2025年~2034年 |

| 2025年の評価 | 30億6,000万米ドル |

| 2034年の予測 | 134億2,000万米ドル |

| CAGR | 17.85% |

現在、電気自動車用複合材料市場は、北米、欧州、アジア太平洋を含む主要地域での電気自動車導入の加速に後押しされ、力強い成長段階にあります。市場参入企業の報告によると、複合材料ソリューションがニッチ用途から大衆向け電気自動車に広く採用されるようになり、技術準備レベルが高まっています。クリーンエネルギーと排出削減を促進する政府の政策が市場の勢いを支えています。複合材料メーカー、OEM、研究機関の協力体制は、材料性能と製造効率を向上させるための基本です。電気自動車用複合材料市場は、自動車設計パラダイムの進化と電動化への世界の移行に牽引され、今後10年間は2桁台の成長率を維持すると予想されます。

電気自動車用複合材料の市場セグメンテーション:

セグメンテーション1:繊維タイプ別

- 炭素繊維

- ガラス繊維

- その他

セグメンテーション2:樹脂タイプ別

- 熱硬化性樹脂

- 熱可塑性樹脂

セグメンテーション3:製造プロセス別

- 圧縮成形

- 射出成形

- RTM

セグメンテーション4:用途別

- 構造部品

- 非構造部品

- バッテリー・エンクロージャーとパック

- その他

セグメンテーション5:地域別

- 北米- 米国、カナダ、メキシコ

- 欧州- ドイツ、フランス、イタリア、スペイン、英国、その他

- アジア太平洋地域- 中国、日本、韓国、インド、その他

- その他地域- 南米、中東・アフリカ

需要- 促進要因と抑制要因

電気自動車用複合材料市場の需要促進要因は以下の通りです:

- 電気自動車の走行距離とエネルギー効率を向上させるための軽量材料への需要の高まり

- 自動車の排出ガス削減と持続可能性向上のための規制圧力の高まり

- 複合材料製造技術の進歩別コスト削減と拡張性の向上

電気自動車用複合材料市場は、以下の課題によっていくつかの抑制要因にも直面すると予想されます:

- 高度な複合材料に関連する高い製造コストと原材料コスト

- 複合材料のリサイクルと使用後管理の複雑さ

電気自動車用複合材料市場の主要参入企業と競合の概要

世界の電気自動車用複合材料市場は、既存の自動車材料サプライヤーと新興の複合材料技術革新企業によって形成されたダイナミックで急速に進化する競合情勢を呈しています。Toray Industries、Teijin Limited、Syensqo、Piran Advanced Composites、Rochling SE &Co.KGといった国際的な大手企業が、電気自動車用途に合わせた高性能複合材料ソリューションの推進において極めて重要な役割を果たしています。これらの主な参入企業は、電気自動車の効率、航続距離、安全性を高める軽量で耐久性があり、コスト効率の高い複合材料の開発を重視しています。このような既存企業に加えて、新興企業や専門材料メーカーが相次いで、電気自動車メーカーの多様な需要に対応するため、リサイクル性、熱管理改善、製造拡張性に焦点を当てた革新的な複合材料を提供しています。電気自動車用複合材料市場の競争は、自動車OEMとの戦略的提携、継続的な研究開発、政府の奨励策や環境規制を原動力とする地域的成長によって推進されています。電気自動車用複合材料市場の拡大に伴い、参入企業は次世代の電気自動車アーキテクチャーに適合する、適応性のある高性能複合材料を世界に提供することに注力しています。

当レポートでは、世界の電気自動車用複合材料市場について調査し、市場の概要とともに、繊維タイプ別、樹脂タイプ別、製造プロセス別、用途別、地域別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

エグゼクティブサマリー

第1章 市場:業界展望

- 動向:現状と将来への影響評価

- 市場力学の概要

- 規制と環境政策の影響

- 特許分析

- 技術情勢

- スタートアップの情勢

- 投資情勢と研究開発動向

- バリューチェーン分析

- 業界の魅力

第2章 世界の電気自動車用複合材料市場(繊維タイプ別)

- カーボンファイバー

- ガラス繊維

- その他

第3章 世界の電気自動車用複合材料市場(樹脂タイプ別)

- 熱硬化性樹脂

- 熱可塑性樹脂

第4章 世界の電気自動車用複合材料市場(製造プロセス別)

- 圧縮成形

- 射出成形

- RTM

第5章 世界の電気自動車用複合材料市場(用途別)

- 構造部品

- 非構造部品

- バッテリーエンクロージャとパック

- その他

第6章 世界の電気自動車用複合材料市場(地域別)

- 世界の電気自動車用複合材料市場(地域別)

- 北米

- 欧州

- アジア太平洋

- その他の地域

第7章 市場-競合ベンチマーキングと企業プロファイル

- 今後の見通し

- 地理的評価

- 企業プロファイル

- Toray Industries, Inc.

- Teijin Limited

- Syensqo

- Piran Advanced Composites

- HRC (Hengrui Corporation)

- Envalior

- Exel Composites

- SGL Carbon

- Plastic Omnium

- Rochling SE & Co. KG

- Mar-Bal, Inc.

- ElringKlinger AG

- POLYTEC HOLDING AG

- Faurecia

- KG

- その他の主要企業

第8章 調査手法

List of Figures

- Figure 1: Electric Vehicle Composites Market (by Scenario), $Billion, 2025, 2028, and 2034

- Figure 2: Electric Vehicle Composites Market (by Region), $Billion, 2024, 2027, and 2034

- Figure 3: Electric Vehicle Composites Market (by Fiber Type), $Billion, 2024, 2027, and 2034

- Figure 4: Electric Vehicle Composites Market (by Resin Type), $Billion, 2024, 2027, and 2034

- Figure 5: Electric Vehicle Composites Market (by Manufacturing Process), $Billion, 2024, 2027, and 2034

- Figure 6: Electric Vehicle Composites Market (by Application), $Billion, 2024, 2027, and 2034

- Figure 7: Competitive Landscape Snapshot

- Figure 8: Supply Chain Analysis

- Figure 9: Value Chain Analysis

- Figure 10: Patent Analysis (by Country), January 2021-April 2025

- Figure 11: Patent Analysis (by Company), January 2021-April 2025

- Figure 12: Impact Analysis of Market Navigating Factors, 2024-2034

- Figure 13: U.S. Electric Vehicle Composites Market, $Billion, 2024-2034

- Figure 14: Canada Electric Vehicle Composites Market, $Billion, 2024-2034

- Figure 15: Mexico Electric Vehicle Composites Market, $Billion, 2024-2034

- Figure 16: Germany Electric Vehicle Composites Market, $Billion, 2024-2034

- Figure 17: France Electric Vehicle Composites Market, $Billion, 2024-2034

- Figure 18: Italy Electric Vehicle Composites Market, $Billion, 2024-2034

- Figure 19: Spain Electric Vehicle Composites Market, $Billion, 2024-2034

- Figure 20: U.K. Electric Vehicle Composites Market, $Billion, 2024-2034

- Figure 21: Rest-of-Europe Electric Vehicle Composites Market, $Billion, 2024-2034

- Figure 22: China Electric Vehicle Composites Market, $Billion, 2024-2034

- Figure 23: Japan Electric Vehicle Composites Market, $Billion, 2024-2034

- Figure 24: India Electric Vehicle Composites Market, $Billion, 2024-2034

- Figure 25: South Korea Electric Vehicle Composites Market, $Billion, 2024-2034

- Figure 26: Rest-of-Asia-Pacific Electric Vehicle Composites Market, $Billion, 2024-2034

- Figure 27: South America Electric Vehicle Composites Market, $Billion, 2024-2034

- Figure 28: Middle East and Africa Electric Vehicle Composites Market, $Billion, 2024-2034

- Figure 29: Strategic Initiatives (by Company), 2021-2025

- Figure 30: Share of Strategic Initiatives, 2021-2025

- Figure 31: Data Triangulation

- Figure 32: Top-Down and Bottom-Up Approach

- Figure 33: Assumptions and Limitations

List of Tables

- Table 1: Market Snapshot

- Table 2: Opportunities across Region

- Table 3: Trends Overview

- Table 4: Electric Vehicle Composites Market (by Region), $Billion, 2024-2034

- Table 5: North America Electric Vehicle Composites Market (by Fiber Type), $Billion, 2024-2034

- Table 6: North America Electric Vehicle Composites Market (by Resin Type), $Billion, 2024-2034

- Table 7: North America Electric Vehicle Composites Market (by Manufacturing Process), $Billion, 2024-2034

- Table 8: North America Electric Vehicle Composites Market (by Application), $Billion, 2024-2034

- Table 9: U.S. Electric Vehicle Composites Market (by Fiber Type), $Billion, 2024-2034

- Table 10: U.S. Electric Vehicle Composites Market (by Resin Type), $Billion, 2024-2034

- Table 11: U.S. Electric Vehicle Composites Market (by Manufacturing Process), $Billion, 2024-2034

- Table 12: U.S. Electric Vehicle Composites Market (by Application), $Billion, 2024-2034

- Table 13: Canada Electric Vehicle Composites Market (by Fiber Type), $Billion, 2024-2034

- Table 14: Canada Electric Vehicle Composites Market (by Resin Type), $Billion, 2024-2034

- Table 15: Canada Electric Vehicle Composites Market (by Manufacturing Process), $Billion, 2024-2034

- Table 16: Canada Electric Vehicle Composites Market (by Application), $Billion, 2024-2034

- Table 17: Mexico Electric Vehicle Composites Market (by Fiber Type), $Billion, 2024-2034

- Table 18: Mexico Electric Vehicle Composites Market (by Resin Type), $Billion, 2024-2034

- Table 19: Mexico Electric Vehicle Composites Market (by Manufacturing Process), $Billion, 2024-2034

- Table 20: Mexico Electric Vehicle Composites Market (by Application), $Billion, 2024-2034

- Table 21: Europe Electric Vehicle Composites Market (by Fiber Type), $Billion, 2024-2034

- Table 22: Europe Electric Vehicle Composites Market (by Resin Type), $Billion, 2024-2034

- Table 23: Europe Electric Vehicle Composites Market (by Manufacturing Process), $Billion, 2024-2034

- Table 24: Europe Electric Vehicle Composites Market (by Application), $Billion, 2024-2034

- Table 25: Germany Electric Vehicle Composites Market (by Fiber Type), $Billion, 2024-2034

- Table 26: Germany Electric Vehicle Composites Market (by Resin Type), $Billion, 2024-2034

- Table 27: Germany Electric Vehicle Composites Market (by Manufacturing Process), $Billion, 2024-2034

- Table 28: Germany Electric Vehicle Composites Market (by Application), $Billion, 2024-2034

- Table 29: France Electric Vehicle Composites Market (by Fiber Type), $Billion, 2024-2034

- Table 30: France Electric Vehicle Composites Market (by Resin Type), $Billion, 2024-2034

- Table 31: France Electric Vehicle Composites Market (by Manufacturing Process), $Billion, 2024-2034

- Table 32: France Electric Vehicle Composites Market (by Application), $Billion, 2024-2034

- Table 33: Italy Electric Vehicle Composites Market (by Fiber Type), $Billion, 2024-2034

- Table 34: Italy Electric Vehicle Composites Market (by Resin Type), $Billion, 2024-2034

- Table 35: Italy Electric Vehicle Composites Market (by Manufacturing Process), $Billion, 2024-2034

- Table 36: Italy Electric Vehicle Composites Market (by Application), $Billion, 2024-2034

- Table 37: Spain Electric Vehicle Composites Market (by Fiber Type), $Billion, 2024-2034

- Table 38: Spain Electric Vehicle Composites Market (by Resin Type), $Billion, 2024-2034

- Table 39: Spain Electric Vehicle Composites Market (by Manufacturing Process), $Billion, 2024-2034

- Table 40: Spain Electric Vehicle Composites Market (by Application), $Billion, 2024-2034

- Table 41: U.K. Electric Vehicle Composites Market (by Fiber Type), $Billion, 2024-2034

- Table 42: U.K. Electric Vehicle Composites Market (by Resin Type), $Billion, 2024-2034

- Table 43: U.K. Electric Vehicle Composites Market (by Manufacturing Process), $Billion, 2024-2034

- Table 44: U.K. Electric Vehicle Composites Market (by Application), $Billion, 2024-2034

- Table 45: Rest-of-Europe Electric Vehicle Composites Market (by Fiber Type), $Billion, 2024-2034

- Table 46: Rest-of-Europe Electric Vehicle Composites Market (by Resin Type), $Billion, 2024-2034

- Table 47: Rest-of-Europe Electric Vehicle Composites Market (by Manufacturing Process), $Billion, 2024-2034

- Table 48: Rest-of-Europe Electric Vehicle Composites Market (by Application), $Billion, 2024-2034

- Table 49: China Electric Vehicle Composites Market (by Fiber Type), $Billion, 2024-2034

- Table 50: China Electric Vehicle Composites Market (by Resin Type), $Billion, 2024-2034

- Table 51: China Electric Vehicle Composites Market (by Manufacturing Process), $Billion, 2024-2034

- Table 52: China Electric Vehicle Composites Market (by Application), $Billion, 2024-2034

- Table 53: Japan Electric Vehicle Composites Market (by Fiber Type), $Billion, 2024-2034

- Table 54: Japan Electric Vehicle Composites Market (by Resin Type), $Billion, 2024-2034

- Table 55: Japan Electric Vehicle Composites Market (by Manufacturing Process), $Billion, 2024-2034

- Table 56: Japan Electric Vehicle Composites Market (by Application), $Billion, 2024-2034

- Table 57: India Electric Vehicle Composites Market (by Fiber Type), $Billion, 2024-2034

- Table 58: India Electric Vehicle Composites Market (by Resin Type), $Billion, 2024-2034

- Table 59: India Electric Vehicle Composites Market (by Manufacturing Process), $Billion, 2024-2034

- Table 60: India Electric Vehicle Composites Market (by Application), $Billion, 2024-2034

- Table 61: South Korea Electric Vehicle Composites Market (by Fiber Type), $Billion, 2024-2034

- Table 62: South Korea Electric Vehicle Composites Market (by Resin Type), $Billion, 2024-2034

- Table 63: South Korea Electric Vehicle Composites Market (by Manufacturing Process), $Billion, 2024-2034

- Table 64: South Korea Electric Vehicle Composites Market (by Application), $Billion, 2024-2034

- Table 65: Rest-of-Asia-Pacific Electric Vehicle Composites Market (by Fiber Type), $Billion, 2024-2034

- Table 66: Rest-of-Asia-Pacific Electric Vehicle Composites Market (by Resin Type), $Billion, 2024-2034

- Table 67: Rest-of-Asia-Pacific Electric Vehicle Composites Market (by Manufacturing Process), $Billion, 2024-2034

- Table 68: Rest-of-Asia-Pacific Electric Vehicle Composites Market (by Application), $Billion, 2024-2034

- Table 69: Rest-of-the-World Electric Vehicle Composites Market (by Fiber Type), $Billion, 2024-2034

- Table 70: Rest-of-the-World Electric Vehicle Composites Market (by Resin Type), $Billion, 2024-2034

- Table 71: Rest-of-the-World Electric Vehicle Composites Market (by Manufacturing Process), $Billion, 2024-2034

- Table 72: Rest-of-the-World Electric Vehicle Composites Market (by Application), $Billion, 2024-2034

- Table 73: South America Electric Vehicle Composites Market (by Fiber Type), $Billion, 2024-2034

- Table 74: South America Electric Vehicle Composites Market (by Resin Type), $Billion, 2024-2034

- Table 75: South America Electric Vehicle Composites Market (by Manufacturing Process), $Billion, 2024-2034

- Table 76: South America Electric Vehicle Composites Market (by Application), $Billion, 2024-2034

- Table 77: Middle East and Africa Electric Vehicle Composites Market (by Fiber Type), $Billion, 2024-2034

- Table 78: Middle East and Africa Electric Vehicle Composites Market (by Resin Type), $Billion, 2024-2034

- Table 79: Middle East and Africa Electric Vehicle Composites Market (by Manufacturing Process), $Billion, 2024-2034

- Table 80: Middle East and Africa Electric Vehicle Composites Market (by Application), $Billion, 2024-2034

- Table 81: Market Share

Electric Vehicle Composites Market Industry and Technology Overview

The electric vehicle composites market represents a critical segment within the automotive materials industry, with composite materials playing an indispensable role in the lightweighting strategies central to electric vehicle design. Technological advances in fiber types, resin formulations, and manufacturing processes continue to improve the strength-to-weight ratio, durability, and sustainability of composites used across structural and non-structural components of electric vehicles. Thermal and acoustic management, battery enclosures, and drive train components increasingly incorporate composite solutions to meet stringent safety and efficiency standards. The electric vehicle composites market benefits from heightened investments in R&D focusing on cost reduction, enhanced recyclability, and integration with automated manufacturing techniques such as resin transfer molding and additive manufacturing.

Global Electric Vehicle Composites Market Lifecycle Stage

| KEY MARKET STATISTICS | |

|---|---|

| Forecast Period | 2025 - 2034 |

| 2025 Evaluation | $3.06 Billion |

| 2034 Forecast | $13.42 Billion |

| CAGR | 17.85% |

Currently, the electric vehicle composites market is in a robust growth phase, propelled by accelerating electric vehicle adoption in key regions including North America, Europe, and Asia-Pacific. Market participants report increasing technology readiness levels, with composite solutions transitioning from niche applications to widespread adoption in mass-market electric vehicles. Government policies promoting clean energy and emission reduction support market momentum. Collaborative efforts between composite manufacturers, OEMs, and research institutions are fundamental to advancing material performance and manufacturing efficiencies. The electric vehicle composites market is expected to sustain double-digit growth rates over the next decade, driven by evolving automotive design paradigms and the global transition toward electrification.

Electric Vehicle Composites Market Segmentation:

Segmentation 1: by Fiber Type

- Carbon Fiber

- Glass Fiber

- Others

Segmentation 2: by Resin Type

- Thermoset Resins

- Thermoplastic Resins

Segmentation 3: by Manufacturing Process

- Compression Molding

- Injection Molding

- RTM

Segmentation 4: by Application

- Structural Components

- Vehicle Body Panels

- Chassis and Frame Elements

- Bumpers and Impact Absorbers

- Non-Structural Components

- Interior Parts

- Exterior Trim and Accessories

- Under-the-Hood Components

- Battery Enclosures and Packs

- Battery Housing and Protective Casings

- Thermal Management Components

- Structural Support Elements in Battery Modules

- Others

Segmentation 5: by Region

- North America - U.S., Canada, and Mexico

- Europe - Germany, France, Italy, Spain, U.K., and Rest-of-Europe

- Asia-Pacific - China, Japan, South Korea, India, and Rest-of-Asia-Pacific

- Rest-of-the-World - South America and Middle East and Africa

Demand - Drivers and Limitations

The following are the demand drivers for the electric vehicle composites market:

- Growing demand for lightweight materials to improve EV driving range and energy efficiency

- Increasing regulatory pressure to reduce vehicle emissions and enhance sustainability

- Advancements in composite manufacturing technologies reducing costs and increasing scalability

The electric vehicle composites market is expected to face some limitations as well due to the following challenges:

- High production and raw material costs associated with advanced composites

- Complexity in recycling and end-of-life management of composite materials

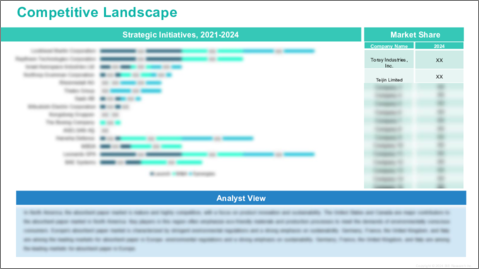

Electric Vehicle Composites Market Key Players and Competition Synopsis

The global electric vehicle composites market presents a dynamic and rapidly evolving competitive landscape shaped by both established automotive material suppliers and emerging composite technology innovators. Leading international companies such as Toray Industries, Teijin Limited, Syensqo, Piran Advanced Composites, and Rochling SE & Co. KG play pivotal roles in advancing high-performance composite solutions tailored for electric vehicle applications. These key players emphasize the development of lightweight, durable, and cost-effective composite materials that enhance electric vehicle efficiency, range, and safety. Alongside these established entities, a wave of startups and specialized material manufacturers are contributing innovative composites focusing on recyclability, improved thermal management, and manufacturing scalability to address the diverse demands of electric vehicle manufacturers. Competition in the electric vehicle composites market is driven by strategic collaborations with automotive OEMs, continuous research and development, and regional growth fueled by government incentives and environmental regulations. As the electric vehicle composites market expands, players concentrate on delivering adaptable, high-performance composite materials compatible with next-generation electric vehicle architectures globally.

Some prominent names established in the electric vehicle composites market are:

- Toray Industries, Inc.

- Teijin Limited

- Syensqo

- Piran Advanced Composites

- HRC (Hengrui Corporation)

- Envalior

- Exel Composites

- SGL Carbon

- Plastic Omnium

- Rochling SE & Co. KG

- Mar-Bal, Inc.

- ElringKlinger AG

- POLYTEC HOLDING AG

- Faurecia

- Kautex Textron GmbH & Co. KG

Companies that are not a part of the previously mentioned pool have been well represented across different sections of the report (wherever applicable).

Table of Contents

Executive Summary

Scope and Definition

Market/Product Definition

Key Questions Answered

Analysis and Forecast Note

1. Markets: Industry Outlook

- 1.1 Trends: Current and Future Impact Assessment

- 1.2 Market Dynamics Overview

- 1.2.1 Market Drivers

- 1.2.2 Market Restraints

- 1.2.3 Market Opportunities

- 1.3 Impact of Regulatory and Environmental Policies

- 1.4 Patent Analysis

- 1.4.1 By Year

- 1.4.2 By Region

- 1.5 Technology Landscape

- 1.6 Start-Up Landscape

- 1.7 Investment Landscape and R&D Trends

- 1.8 Value Chain Analysis

- 1.9 Industry Attractiveness

2. Global Electric Vehicle Composites Market (by Fiber Type)

- 2.1 Carbon Fiber

- 2.2 Glass Fiber

- 2.3 Others

3. Global Electric Vehicle Composites Market (by Resin Type)

- 3.1 Thermoset Resins

- 3.2 Thermoplastic Resins

4. Global Electric Vehicle Composites Market (by Manufacturing Process)

- 4.1 Compression Molding

- 4.2 Injection Molding

- 4.3 RTM

5. Global Electric Vehicle Composites Market (by Application)

- 5.1 Structural Components

- 5.1.1 Vehicle Body Panels

- 5.1.2 Chassis and Frame Elements

- 5.1.3 Bumpers and Impact Absorbers

- 5.2 Non-Structural Components

- 5.2.1 Interior Parts

- 5.2.2 Exterior Trim and Accessories

- 5.2.3 Under-the-Hood Components

- 5.3 Battery Enclosures and Packs

- 5.3.1 Battery Housing and Protective Casings

- 5.3.2 Thermal Management Components

- 5.3.3 Structural Support Elements in Battery Modules

- 5.4 Others

6. Global Electric Vehicle Composites Market (by Region)

- 6.1 Global Electric Vehicle Composites Market (by Region)

- 6.2 North America

- 6.2.1 Regional Overview

- 6.2.2 Driving Factors for Market Growth

- 6.2.3 Factors Challenging the Market

- 6.2.4 Key Companies

- 6.2.5 Fiber Type

- 6.2.6 Resin Type

- 6.2.7 Manufacturing Process

- 6.2.8 Application

- 6.2.9 North America (by Country)

- 6.2.9.1 U.S.

- 6.2.9.1.1 Market by Fiber Type

- 6.2.9.1.2 Market by Resin Type

- 6.2.9.1.3 Market by Manufacturing Process

- 6.2.9.1.4 Market by Application

- 6.2.9.2 Canada

- 6.2.9.2.1 Market by Fiber Type

- 6.2.9.2.2 Market by Resin Type

- 6.2.9.2.3 Market by Manufacturing Process

- 6.2.9.2.4 Market by Application

- 6.2.9.3 Mexico

- 6.2.9.3.1 Market by Fiber Type

- 6.2.9.3.2 Market by Resin Type

- 6.2.9.3.3 Market by Manufacturing Process

- 6.2.9.3.4 Market by Application

- 6.2.9.1 U.S.

- 6.3 Europe

- 6.3.1 Regional Overview

- 6.3.2 Driving Factors for Market Growth

- 6.3.3 Factors Challenging the Market

- 6.3.4 Key Companies

- 6.3.5 Fiber Type

- 6.3.6 Resin Type

- 6.3.7 Manufacturing Process

- 6.3.8 Application

- 6.3.9 Europe (by Country)

- 6.3.9.1 Germany

- 6.3.9.1.1 Market by Fiber Type

- 6.3.9.1.2 Market by Resin Type

- 6.3.9.1.3 Market by Manufacturing Process

- 6.3.9.1.4 Market by Application

- 6.3.9.2 France

- 6.3.9.2.1 Market by Fiber Type

- 6.3.9.2.2 Market by Resin Type

- 6.3.9.2.3 Market by Manufacturing Process

- 6.3.9.2.4 Market by Application

- 6.3.9.3 Italy

- 6.3.9.3.1 Market by Fiber Type

- 6.3.9.3.2 Market by Resin Type

- 6.3.9.3.3 Market by Manufacturing Process

- 6.3.9.3.4 Market by Application

- 6.3.9.4 Spain

- 6.3.9.4.1 Market by Fiber Type

- 6.3.9.4.2 Market by Resin Type

- 6.3.9.4.3 Market by Manufacturing Process

- 6.3.9.4.4 Market by Application

- 6.3.9.5 U.K.

- 6.3.9.5.1 Market by Fiber Type

- 6.3.9.5.2 Market by Resin Type

- 6.3.9.5.3 Market by Manufacturing Process

- 6.3.9.5.4 Market by Application

- 6.3.9.6 Rest-of-Europe

- 6.3.9.6.1 Market by Fiber Type

- 6.3.9.6.2 Market by Resin Type

- 6.3.9.6.3 Market by Manufacturing Process

- 6.3.9.6.4 Market by Application

- 6.3.9.1 Germany

- 6.4 Asia-Pacific

- 6.4.1 Regional Overview

- 6.4.2 Driving Factors for Market Growth

- 6.4.3 Factors Challenging the Market

- 6.4.4 Key Companies

- 6.4.5 Fiber Type

- 6.4.6 Resin Type

- 6.4.7 Manufacturing Process

- 6.4.8 Application

- 6.4.9 Asia-Pacific (by Country)

- 6.4.9.1 China

- 6.4.9.1.1 Market by Fiber Type

- 6.4.9.1.2 Market by Resin Type

- 6.4.9.1.3 Market by Manufacturing Process

- 6.4.9.1.4 Market by Application

- 6.4.9.2 Japan

- 6.4.9.2.1 Market by Fiber Type

- 6.4.9.2.2 Market by Resin Type

- 6.4.9.2.3 Market by Manufacturing Process

- 6.4.9.2.4 Market by Application

- 6.4.9.3 India

- 6.4.9.3.1 Market by Fiber Type

- 6.4.9.3.2 Market by Resin Type

- 6.4.9.3.3 Market by Manufacturing Process

- 6.4.9.3.4 Market by Application

- 6.4.9.4 South Korea

- 6.4.9.4.1 Market by Fiber Type

- 6.4.9.4.2 Market by Resin Type

- 6.4.9.4.3 Market by Manufacturing Process

- 6.4.9.4.4 Market by Application

- 6.4.9.5 Rest-of-Asia-Pacific

- 6.4.9.5.1 Market by Fiber Type

- 6.4.9.5.2 Market by Resin Type

- 6.4.9.5.3 Market by Manufacturing Process

- 6.4.9.5.4 Market by Application

- 6.4.9.1 China

- 6.5 Rest-of-the-World

- 6.5.1 Regional Overview

- 6.5.2 Driving Factors for Market Growth

- 6.5.3 Factors Challenging the Market

- 6.5.4 Key Companies

- 6.5.5 Fiber Type

- 6.5.6 Resin Type

- 6.5.7 Manufacturing Process

- 6.5.8 Application

- 6.5.9 Rest-of-the-World (by Region)

- 6.5.9.1 South America

- 6.5.9.1.1 Market by Fiber Type

- 6.5.9.1.2 Market by Resin Type

- 6.5.9.1.3 Market by Manufacturing Process

- 6.5.9.1.4 Market by Application

- 6.5.9.2 Middle East and Africa

- 6.5.9.2.1 Market by Fiber Type

- 6.5.9.2.2 Market by Resin Type

- 6.5.9.2.3 Market by Manufacturing Process

- 6.5.9.2.4 Market by Application

- 6.5.9.1 South America

7. Markets - Competitive Benchmarking & Company Profiles

- 7.1 Next Frontiers

- 7.2 Geographic Assessment

- 7.3 Company Profiles

- 7.3.1 Toray Industries, Inc.

- 7.3.1.1 Overview

- 7.3.1.2 Top Products/Product Portfolio

- 7.3.1.3 Top Competitors

- 7.3.1.4 Target Customers

- 7.3.1.5 Key Personnel

- 7.3.1.6 Analyst View

- 7.3.1.7 Market Share

- 7.3.2 Teijin Limited

- 7.3.2.1 Overview

- 7.3.2.2 Top Products/Product Portfolio

- 7.3.2.3 Top Competitors

- 7.3.2.4 Target Customers

- 7.3.2.5 Key Personnel

- 7.3.2.6 Analyst View

- 7.3.2.7 Market Share

- 7.3.3 Syensqo

- 7.3.3.1 Overview

- 7.3.3.2 Top Products/Product Portfolio

- 7.3.3.3 Top Competitors

- 7.3.3.4 Target Customers

- 7.3.3.5 Key Personnel

- 7.3.3.6 Analyst View

- 7.3.3.7 Market Share

- 7.3.4 Piran Advanced Composites

- 7.3.4.1 Overview

- 7.3.4.2 Top Products/Product Portfolio

- 7.3.4.3 Top Competitors

- 7.3.4.4 Target Customers

- 7.3.4.5 Key Personnel

- 7.3.4.6 Analyst View

- 7.3.4.7 Market Share

- 7.3.5 HRC (Hengrui Corporation)

- 7.3.5.1 Overview

- 7.3.5.2 Top Products/Product Portfolio

- 7.3.5.3 Top Competitors

- 7.3.5.4 Target Customers

- 7.3.5.5 Key Personnel

- 7.3.5.6 Analyst View

- 7.3.5.7 Market Share

- 7.3.6 Envalior

- 7.3.6.1 Overview

- 7.3.6.2 Top Products/Product Portfolio

- 7.3.6.3 Top Competitors

- 7.3.6.4 Target Customers

- 7.3.6.5 Key Personnel

- 7.3.6.6 Analyst View

- 7.3.6.7 Market Share

- 7.3.7 Exel Composites

- 7.3.7.1 Overview

- 7.3.7.2 Top Products/Product Portfolio

- 7.3.7.3 Top Competitors

- 7.3.7.4 Target Customers

- 7.3.7.5 Key Personnel

- 7.3.7.6 Analyst View

- 7.3.7.7 Market Share

- 7.3.8 SGL Carbon

- 7.3.8.1 Overview

- 7.3.8.2 Top Products/Product Portfolio

- 7.3.8.3 Top Competitors

- 7.3.8.4 Target Customers

- 7.3.8.5 Key Personnel

- 7.3.8.6 Analyst View

- 7.3.8.7 Market Share

- 7.3.9 Plastic Omnium

- 7.3.9.1 Overview

- 7.3.9.2 Top Products/Product Portfolio

- 7.3.9.3 Top Competitors

- 7.3.9.4 Target Customers

- 7.3.9.5 Key Personnel

- 7.3.9.6 Analyst View

- 7.3.9.7 Market Share

- 7.3.10 Rochling SE & Co. KG

- 7.3.10.1 Overview

- 7.3.10.2 Top Products/Product Portfolio

- 7.3.10.3 Top Competitors

- 7.3.10.4 Target Customers

- 7.3.10.5 Key Personnel

- 7.3.10.6 Analyst View

- 7.3.10.7 Market Share

- 7.3.11 Mar-Bal, Inc.

- 7.3.11.1 Overview

- 7.3.11.2 Top Products/Product Portfolio

- 7.3.11.3 Top Competitors

- 7.3.11.4 Target Customers

- 7.3.11.5 Key Personnel

- 7.3.11.6 Analyst View

- 7.3.11.7 Market Share

- 7.3.12 ElringKlinger AG

- 7.3.12.1 Overview

- 7.3.12.2 Top Products/Product Portfolio

- 7.3.12.3 Top Competitors

- 7.3.12.4 Target Customers

- 7.3.12.5 Key Personnel

- 7.3.12.6 Analyst View

- 7.3.12.7 Market Share

- 7.3.13 POLYTEC HOLDING AG

- 7.3.13.1 Overview

- 7.3.13.2 Top Products/Product Portfolio

- 7.3.13.3 Top Competitors

- 7.3.13.4 Target Customers

- 7.3.13.5 Key Personnel

- 7.3.13.6 Analyst View

- 7.3.13.7 Market Share

- 7.3.14 Faurecia

- 7.3.14.1 Overview

- 7.3.14.2 Top Products/Product Portfolio

- 7.3.14.3 Top Competitors

- 7.3.14.4 Target Customers

- 7.3.14.5 Key Personnel

- 7.3.14.6 Analyst View

- 7.3.14.7 Market Share

- 7.3.15 KG

- 7.3.15.1 Overview

- 7.3.15.2 Top Products/Product Portfolio

- 7.3.15.3 Top Competitors

- 7.3.15.4 Target Customers

- 7.3.15.5 Key Personnel

- 7.3.15.6 Analyst View

- 7.3.15.7 Market Share

- 7.3.1 Toray Industries, Inc.

- 7.4 Other Key Companies