|

|

市場調査レポート

商品コード

1524904

診断における質量分析とクロマトグラフィ市場- 世界および地域別分析:製品タイプ別、応用タイプ別、サンプルタイプ別、検査タイプ別、地域別 - 分析と予測(2024年~2033年)Mass Spectrometry and Chromatography in Diagnostics Market - A Global and Regional Analysis: Focus on Product Type, Application Type, Sample Type, Testing Type, and Region - Analysis and Forecast, 2024-2033 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 診断における質量分析とクロマトグラフィ市場- 世界および地域別分析:製品タイプ別、応用タイプ別、サンプルタイプ別、検査タイプ別、地域別 - 分析と予測(2024年~2033年) |

|

出版日: 2024年08月02日

発行: BIS Research

ページ情報: 英文 199 Pages

納期: 1~5営業日

|

全表示

- 概要

- 図表

- 目次

世界の診断における質量分析とクロマトグラフィの市場規模は、2023年に7億4,310万米ドルとなりました。

同市場は、2024年から2033年の間に9.92%のCAGRで拡大し、2033年には18億6,380万米ドルに達すると予測されています。質量分析(MS)とクロマトグラフィの両市場は、より広範な分析・ライフサイエンス機器分野の重要な構成要素です。両技術は、化学物質や生物学的物質の分離、同定、定量のための洗練された手法を提供し、医薬品、環境モニタリング、診断、食品安全など、さまざまな分野の進歩の原動力となっています。診断用途では、これらの技術は単独で使用されることはほとんどなく、ワークフローに統合されます。例えば、液体クロマトグラフィ質量分析計は、液体クロマトグラフィの分離能力と質量分析計の質量分析能力を組み合わせたものです。この統合は、質量や構造を決定する前に成分を分離する必要がある複雑なサンプル分析において特に効果的です。このようなハイブリッドシステムは、患者サンプルのハイスループット分析において臨床現場で不可欠であり、診断と治療の指針となる包括的な理解を提供します。診断における質量分析とクロマトグラフィの主な用途には、ビタミンプロファイリングやホルモンプロファイリングなどがあります。

| 主要市場統計 | |

|---|---|

| 予測期間 | 2024年~2033年 |

| 2024年評価 | 7億9,590万米ドル |

| 2033年予測 | 18億6,380万米ドル |

| CAGR | 9.92% |

診断における質量分析とクロマトグラフィ市場は、従来のイムノアッセイと比較してこれらの技術が提供する複数の利点が原動力となって急成長を遂げており、これらの技術における継続的な技術進歩が採用をさらに促進しています。しかし、装置の取得コストが高いこと、熟練した専門家が少ないことが、同市場の成長を妨げると予想されます。

さらに、診断における標準的な技術として液体クロマトグラフィ・タンデム質量分析(LC-MS/MS)の利用へとシフトしています。診断におけるLC-MS/MSへの嗜好の高まりは、卓越した特異性、感度、複雑な診断タスクに不可欠なマルチプレックス検査の実施能力など、その比類ない分析上の優位性によるものです。これに加えて、質量分析ベースの診断における自動サンプル調製システムの統合は、臨床検査業務の極めて重要な進歩です。この動向は、より迅速で正確な診断検査に対する要求の高まりと、現在進行中の技術の進歩によって、今後も拡大し続けるとみられています。

当レポートでは、世界の診断における質量分析とクロマトグラフィ市場について調査し、市場の概要とともに、製品タイプ別、応用タイプ別、サンプルタイプ別、検査タイプ別、地域別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

エグゼクティブサマリー

第1章 世界の診断における質量分析とクロマトグラフィ市場:業界の見通し

- 市場概要

- 主な動向

- 主要動向の機会評価

- 製品ベンチマーク

- 規制状況

第2章 世界の診断における質量分析とクロマトグラフィ市場:市場力学

- 影響分析

- 市場促進要因

- 市場抑制要因

- 市場機会

第3章 世界の診断における質量分析とクロマトグラフィ市場(製品タイプ別)

- 製品タイプの概要

- 成長シェアマトリックス

- サンプル調製

- 質量分析とクロマトグラフィ

第4章 世界の診断における質量分析とクロマトグラフィ市場(応用タイプ別)

- 用途タイプの概要

- 成長シェアマトリックス

- 治療薬モニタリング

- ビタミン

- ホルモン

- メチルマロン酸(MMA)

- 免疫抑制剤

- その他

第5章 世界の診断における質量分析とクロマトグラフィ市場(サンプルタイプ別)

- サンプルタイプの概要

- 成長シェアマトリックス

- 血

- 尿

- 血清

- プラズマ

- 唾液

第6章 世界の診断における質量分析とクロマトグラフィ市場(検査タイプ別)

- 検査タイプの概要

- 成長シェアマトリックス

- 臨床検査

- 商業用アッセイ

第7章 世界の診断における質量分析とクロマトグラフィ市場(地域別)

- 地域別概要

- 促進要因と抑制要因

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第8章 世界の診断における質量分析とクロマトグラフィ市場:競合ベンチマーキングと企業プロファイル

- 競合情勢

- パートナーシップ、提携、事業拡大

- 新しいサービス

- 合併と買収

- 規制当局の承認

- 主要戦略と開発

- 企業競合マトリックス

- 企業シェア分析

- 企業プロファイル

- Agilent Technologies, Inc.

- Thermo Fisher Scientific, Inc.

- Waters Corporation

- Tecan Group Ltd.

- Danaher Corporation

- Shimadzu Corporation

- Merck KGaA

- Bio-Rad Laboratories, Inc.

- PerkinElmer Inc.

- Promega Corporation

- Restek Corporation

- GERSTEL GmbH & Co. KG

- Bruker Corporation

- New England Biolabs

- Hamilton Company

- Avantor, Inc. (VWR International, LLC.)

- Chromsystems Instruments & Chemicals GmbH.

- RECIPE Chemicals + Instruments GmbH

- Zivak

- SENTINEL CH. SpA

第9章 調査手法

List of Figures

- Figure 1: Global Mass Spectrometry and Chromatography in Diagnostics Market, $Million, 2024, 2028, and 2033

- Figure 2: Global Mass Spectrometry and Chromatography in Diagnostics Market (by Region), $Million, 2023, 2027, and 2033

- Figure 3: Global Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), $Million, 2023, 2027, and 2033

- Figure 4: Global Mass Spectrometry and Chromatography in Diagnostics Market (by Application), $Million, 2023, 2027, and 2033

- Figure 5: Global Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Type), $Million, 2023, 2027, and 2033

- Figure 6: Global Mass Spectrometry and Chromatography in Diagnostics Market (by Testing Type), $Million, 2023, 2027, and 2033

- Figure 7: Product Benchmarking (Mass Spectrometry and Chromatography (by Instruments))

- Figure 8: Regulatory Framework, U.S. FDA

- Figure 9: EU IVD Regulation

- Figure 10: Impact Analysis of Market Dynamics, 2023-2033

- Figure 11: Growth-Share Analysis for Global Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), 2023-2033

- Figure 12: Growth-Share Analysis for Global Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type), 2023-2033

- Figure 13: Growth-Share Analysis for Global Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Type), 2023-2033

- Figure 14: Growth-Share Analysis for Global Mass Spectrometry and Chromatography in Diagnostics Market (by Testing Type), 2023-2033

- Figure 15: U.S. Mass Spectrometry and Chromatography in Diagnostics Market, $Million, 2023-2033

- Figure 16: Canada Mass Spectrometry and Chromatography in Diagnostics Market, $Million, 2023-2033

- Figure 17: U.K. Mass Spectrometry and Chromatography in Diagnostics Market, $Million, 2023-2033

- Figure 18: Germany Mass Spectrometry and Chromatography in Diagnostics Market, $Million, 2023-2033

- Figure 19: France Mass Spectrometry and Chromatography in Diagnostics Market, $Million, 2023-2033

- Figure 20: Italy Mass Spectrometry and Chromatography in Diagnostics Market, $Million, 2023-2033

- Figure 21: Spain Mass Spectrometry and Chromatography in Diagnostics Market, $Million, 2023-2033

- Figure 22: Rest-of-Europe Mass Spectrometry and Chromatography in Diagnostics Market, $Million, 2023-2033

- Figure 23: Japan Mass Spectrometry and Chromatography in Diagnostics Market, $Million, 2023-2033

- Figure 24: China Mass Spectrometry and Chromatography in Diagnostics Market, $Million, 2023-2033

- Figure 25: India Mass Spectrometry and Chromatography in Diagnostics Market, $Million, 2023-2033

- Figure 26: Rest-of-Asia-Pacific Mass Spectrometry and Chromatography in Diagnostics Market, $Million, 2023-2033

- Figure 27: Brazil Mass Spectrometry and Chromatography in Diagnostics Market, $Million, 2023-2033

- Figure 28: Mexico Mass Spectrometry and Chromatography in Diagnostics Market, $Million, 2023-2033

- Figure 29: Rest-of-Latin America Mass Spectrometry and Chromatography in Diagnostics Market, $Million, 2023-2033

- Figure 30: GCC Countries Mass Spectrometry and Chromatography in Diagnostics Market, $Million, 2023-2033

- Figure 31: South Africa Mass Spectrometry and Chromatography in Diagnostics Market, $Million, 2023-2033

- Figure 32: Rest-of-Middle East and Africa Mass Spectrometry and Chromatography in Diagnostics Market, $Million, 2023-2033

- Figure 33: Partnerships, Alliances, and Business Expansions, January 2015- June 2024

- Figure 34: New Offerings, January 2015- June 2024

- Figure 35: Mergers and Acquisitions, January 2015- June 2024

- Figure 36: New Offerings, January 2015- June 2024

- Figure 37: Global Mass Spectrometry and Chromatography in Diagnostics Market, Company Competition Matrix

- Figure 38: Global Mass Spectrometry and Chromatography in Diagnostics Market, % Share, 2023

- Figure 39: Data Triangulation

- Figure 40: Assumptions and Limitations

List of Tables

- Table 1: Market Snapshot

- Table 2: Current State and Future Potential of Key Trends in the Global Mass Spectrometry and Chromatography in Diagnostics Market

- Table 3: Immunoassays vs. Mass spectrometry and Chromatography-Based Methods

- Table 4: Cost Breakdown for the Acquisition of a Mass Spectrometer System

- Table 5: Global Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), $Million, 2023-2033

- Table 6: Global Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Preparation), $Million, 2023-2033

- Table 7: Global Mass Spectrometry and Chromatography in Diagnostics Market, Sample Preparation (by Instruments), $Million, 2023-2033

- Table 8: Global Mass Spectrometry and Chromatography in Diagnostics Market, Sample Preparation (by Reagents and Kits), $Million, 2023-2033

- Table 9: Global Mass Spectrometry and Chromatography in Diagnostics Market (by Mass Spectrometry and Chromatography), $Million, 2023-2033

- Table 10: Global Mass Spectrometry and Chromatography in Diagnostics Market, Mass Spectrometry and Chromatography, (by Consumables), $Million, 2023-2033

- Table 11: Global Mass Spectrometry and Chromatography in Diagnostics Market, Mass Spectrometry and Chromatography, (by Instruments), $Million, 2023-2033

- Table 12: Global Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type), $Million, 2023-2033

- Table 13: Global Mass Spectrometry and Chromatography in Diagnostics Market (by Vitamins), $Million, 2023-2033

- Table 14: Global Mass Spectrometry and Chromatography in Diagnostics Market (by Hormones), $Million, 2023-2033

- Table 15: Global Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Type), $Million, 2023-2033

- Table 16: Global Mass Spectrometry and Chromatography in Diagnostics Market (by Testing Type), $Million, 2023-2033

- Table 17: Global Mass Spectrometry and Chromatography in Diagnostics Market (by Region), $Million, 2023-2033

- Table 18: North America Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), $Million, 2023-2033

- Table 19: North America Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Preparation), $Million, 2023-2033

- Table 20: North America Mass Spectrometry and Chromatography in Diagnostics Market (by Mass Spectrometry and Chromatography), $Million, 2023-2033

- Table 21: North America Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type), $Million, 2023-2033

- Table 22: North America Mass Spectrometry and Chromatography in Diagnostics Market (by Vitamins), $Million, 2023-2033

- Table 23: North America Mass Spectrometry and Chromatography in Diagnostics Market (by Hormones), $Million, 2023-2033

- Table 24: U.S. Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), $Million, 2023-2033

- Table 25: U.S. Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Preparation), $Million, 2023-2033

- Table 26: U.S. Mass Spectrometry and Chromatography in Diagnostics Market (by Mass Spectrometry and Chromatography), $Million, 2023-2033

- Table 27: U.S. Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type), $Million, 2023-2033

- Table 28: U.S. Mass Spectrometry and Chromatography in Diagnostics Market (by Vitamins), $Million, 2023-2033

- Table 29: U.S. Mass Spectrometry and Chromatography in Diagnostics Market (by Hormones), $Million, 2023-2033

- Table 30: Canada Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), $Million, 2023-2033

- Table 31: Canada Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Preparation), $Million, 2023-2033

- Table 32: Canada Mass Spectrometry and Chromatography in Diagnostics Market (by Mass Spectrometry and Chromatography), $Million, 2023-2033

- Table 33: Canada Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type), $Million, 2023-2033

- Table 34: Canada Mass Spectrometry and Chromatography in Diagnostics Market (by Vitamins), $Million, 2023-2033

- Table 35: Canada Mass Spectrometry and Chromatography in Diagnostics Market (by Hormones), $Million, 2023-2033

- Table 36: Europe Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), $Million, 2023-2033

- Table 37: Europe Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Preparation), $Million, 2023-2033

- Table 38: Europe Mass Spectrometry and Chromatography in Diagnostics Market (by Mass Spectrometry and Chromatography), $Million, 2023-2033

- Table 39: Europe Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type), $Million, 2023-2033

- Table 40: Europe Mass Spectrometry and Chromatography in Diagnostics Market (by Vitamins), $Million, 2023-2033

- Table 41: Europe Mass Spectrometry and Chromatography in Diagnostics Market (by Hormones), $Million, 2023-2033

- Table 42: U.K. Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), $Million, 2023-2033

- Table 43: U.K. Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Preparation), $Million, 2023-2033

- Table 44: U.K. Mass Spectrometry and Chromatography in Diagnostics Market (by Mass Spectrometry and Chromatography), $Million, 2023-2033

- Table 45: U.K. Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type), $Million, 2023-2033

- Table 46: U.K. Mass Spectrometry and Chromatography in Diagnostics Market (by Vitamins), $Million, 2023-2033

- Table 47: U.K. Mass Spectrometry and Chromatography in Diagnostics Market (by Hormones), $Million, 2023-2033

- Table 48: Germany Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), $Million, 2023-2033

- Table 49: Germany Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Preparation), $Million, 2023-2033

- Table 50: Germany Mass Spectrometry and Chromatography in Diagnostics Market (by Mass Spectrometry and Chromatography), $Million, 2023-2033

- Table 51: Germany Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type), $Million, 2023-2033

- Table 52: Germany Mass Spectrometry and Chromatography in Diagnostics Market (by Vitamins), $Million, 2023-2033

- Table 53: Germany Mass Spectrometry and Chromatography in Diagnostics Market (by Hormones), $Million, 2023-2033

- Table 54: France Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), $Million, 2023-2033

- Table 55: France Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Preparation), $Million, 2023-2033

- Table 56: France Mass Spectrometry and Chromatography in Diagnostics Market (by Mass Spectrometry and Chromatography), $Million, 2023-2033

- Table 57: France Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type), $Million, 2023-2033

- Table 58: France Mass Spectrometry and Chromatography in Diagnostics Market (by Vitamins), $Million, 2023-2033

- Table 59: France Mass Spectrometry and Chromatography in Diagnostics Market (by Hormones), $Million, 2023-2033

- Table 60: Italy Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), $Million, 2023-2033

- Table 61: Italy Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Preparation), $Million, 2023-2033

- Table 62: Italy Mass Spectrometry and Chromatography in Diagnostics Market (by Mass Spectrometry and Chromatography), $Million, 2023-2033

- Table 63: Italy Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type), $Million, 2023-2033

- Table 64: Italy Mass Spectrometry and Chromatography in Diagnostics Market (by Vitamins), $Million, 2023-2033

- Table 65: Italy Mass Spectrometry and Chromatography in Diagnostics Market (by Hormones), $Million, 2023-2033

- Table 66: Spain Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), $Million, 2023-2033

- Table 67: Spain Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Preparation), $Million, 2023-2033

- Table 68: Spain Mass Spectrometry and Chromatography in Diagnostics Market (by Mass Spectrometry and Chromatography), $Million, 2023-2033

- Table 69: Spain Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type), $Million, 2023-2033

- Table 70: Spain Mass Spectrometry and Chromatography in Diagnostics Market (by Vitamins), $Million, 2023-2033

- Table 71: Spain Mass Spectrometry and Chromatography in Diagnostics Market (by Hormones), $Million, 2023-2033

- Table 72: Rest-of-Europe Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), $Million, 2023-2033

- Table 73: Rest-of-Europe Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Preparation), $Million, 2023-2033

- Table 74: Rest-of-Europe Mass Spectrometry and Chromatography in Diagnostics Market (by Mass Spectrometry and Chromatography), $Million, 2023-2033

- Table 75: Rest-of-Europe Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type), $Million, 2023-2033

- Table 76: Rest-of-Europe Mass Spectrometry and Chromatography in Diagnostics Market (by Vitamins), $Million, 2023-2033

- Table 77: Rest-of-Europe Mass Spectrometry and Chromatography in Diagnostics Market (by Hormones), $Million, 2023-2033

- Table 78: Asia-Pacific Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), $Million, 2023-2033

- Table 79: Asia-Pacific Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Preparation), $Million, 2023-2033

- Table 80: Asia-Pacific Mass Spectrometry and Chromatography in Diagnostics Market (by Mass Spectrometry and Chromatography), $Million, 2023-2033

- Table 81: Asia-Pacific Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type), $Million, 2023-2033

- Table 82: Asia-Pacific Mass Spectrometry and Chromatography in Diagnostics Market (by Vitamins), $Million, 2023-2033

- Table 83: Asia-Pacific Mass Spectrometry and Chromatography in Diagnostics Market (by Hormones), $Million, 2023-2033

- Table 84: Japan Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), $Million, 2023-2033

- Table 85: Japan Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Preparation), $Million, 2023-2033

- Table 86: Japan Mass Spectrometry and Chromatography in Diagnostics Market (by Mass Spectrometry and Chromatography), $Million, 2023-2033

- Table 87: Japan Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type), $Million, 2023-2033

- Table 88: Japan Mass Spectrometry and Chromatography in Diagnostics Market (by Vitamins), $Million, 2023-2033

- Table 89: Japan Mass Spectrometry and Chromatography in Diagnostics Market (by Hormones), $Million, 2023-2033

- Table 90: China Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), $Million, 2023-2033

- Table 91: China Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Preparation), $Million, 2023-2033

- Table 92: China Mass Spectrometry and Chromatography in Diagnostics Market (by Mass Spectrometry and Chromatography), $Million, 2023-2033

- Table 93: China Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type), $Million, 2023-2033

- Table 94: China Mass Spectrometry and Chromatography in Diagnostics Market (by Vitamins), $Million, 2023-2033

- Table 95: China Mass Spectrometry and Chromatography in Diagnostics Market (by Hormones), $Million, 2023-2033

- Table 96: India Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), $Million, 2023-2033

- Table 97: India Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Preparation), $Million, 2023-2033

- Table 98: India Mass Spectrometry and Chromatography in Diagnostics Market (by Mass Spectrometry and Chromatography), $Million, 2023-2033

- Table 99: India Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type), $Million, 2023-2033

- Table 100: India Mass Spectrometry and Chromatography in Diagnostics Market (by Vitamins), $Million, 2023-2033

- Table 101: India Mass Spectrometry and Chromatography in Diagnostics Market (by Hormones), $Million, 2023-2033

- Table 102: Rest-of-Asia-Pacific Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), $Million, 2023-2033

- Table 103: Rest-of-Asia-Pacific Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Preparation), $Million, 2023-2033

- Table 104: Rest-of-Asia-Pacific Mass Spectrometry and Chromatography in Diagnostics Market (by Mass Spectrometry and Chromatography), $Million, 2023-2033

- Table 105: Rest-of-Asia-Pacific Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type), $Million, 2023-2033

- Table 106: Rest-of-Asia-Pacific Mass Spectrometry and Chromatography in Diagnostics Market (by Vitamins), $Million, 2023-2033

- Table 107: Rest-of-Asia-Pacific Mass Spectrometry and Chromatography in Diagnostics Market (by Hormones), $Million, 2023-2033

- Table 108: Latin America Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), $Million, 2023-2033

- Table 109: Latin America Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Preparation), $Million, 2023-2033

- Table 110: Latin America Mass Spectrometry and Chromatography in Diagnostics Market (by Mass Spectrometry and Chromatography), $Million, 2023-2033

- Table 111: Latin America Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type), $Million, 2023-2033

- Table 112: Latin America Mass Spectrometry and Chromatography in Diagnostics Market (by Vitamins), $Million, 2023-2033

- Table 113: Latin America Mass Spectrometry and Chromatography in Diagnostics Market (by Hormones), $Million, 2023-2033

- Table 114: Brazil Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), $Million, 2023-2033

- Table 115: Brazil Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Preparation), $Million, 2023-2033

- Table 116: Brazil Mass Spectrometry and Chromatography in Diagnostics Market (by Mass Spectrometry and Chromatography), $Million, 2023-2033

- Table 117: Brazil Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type), $Million, 2023-2033

- Table 118: Brazil Mass Spectrometry and Chromatography in Diagnostics Market (by Vitamins), $Million, 2023-2033

- Table 119: Brazil Mass Spectrometry and Chromatography in Diagnostics Market (by Hormones), $Million, 2023-2033

- Table 120: Mexico Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), $Million, 2023-2033

- Table 121: Mexico Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Preparation), $Million, 2023-2033

- Table 122: Mexico Mass Spectrometry and Chromatography in Diagnostics Market (by Mass Spectrometry and Chromatography), $Million, 2023-2033

- Table 123: Mexico Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type), $Million, 2023-2033

- Table 124: Mexico Mass Spectrometry and Chromatography in Diagnostics Market (by Vitamins), $Million, 2023-2033

- Table 125: Mexico Mass Spectrometry and Chromatography in Diagnostics Market (by Hormones), $Million, 2023-2033

- Table 126: Rest-of-Latin America Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), $Million, 2023-2033

- Table 127: Rest-of-Latin America Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Preparation), $Million, 2023-2033

- Table 128: Rest-of-Latin America Mass Spectrometry and Chromatography in Diagnostics Market (by Mass Spectrometry and Chromatography), $Million, 2023-2033

- Table 129: Rest-of-Latin America Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type), $Million, 2023-2033

- Table 130: Rest-of-Latin America Mass Spectrometry and Chromatography in Diagnostics Market (by Vitamins), $Million, 2023-2033

- Table 131: Rest-of-Latin America Mass Spectrometry and Chromatography in Diagnostics Market (by Hormones), $Million, 2023-2033

- Table 132: Middle East and Africa Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), $Million, 2023-2033

- Table 133: Middle East and Africa Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Preparation), $Million, 2023-2033

- Table 134: Middle East and Africa Mass Spectrometry and Chromatography in Diagnostics Market (by Mass Spectrometry and Chromatography), $Million, 2023-2033

- Table 135: Middle East and Africa Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type), $Million, 2023-2033

- Table 136: Middle East and Africa Mass Spectrometry and Chromatography in Diagnostics Market (by Vitamins), $Million, 2023-2033

- Table 137: Middle East and Africa Mass Spectrometry and Chromatography in Diagnostics Market (by Hormones), $Million, 2023-2033

- Table 138: GCC Countries Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), $Million, 2023-2033

- Table 139: GCC Countries Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Preparation), $Million, 2023-2033

- Table 140: GCC Countries Mass Spectrometry and Chromatography in Diagnostics Market (by Mass Spectrometry and Chromatography), $Million, 2023-2033

- Table 141: GCC Countries Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type), $Million, 2023-2033

- Table 142: GCC Countries Mass Spectrometry and Chromatography in Diagnostics Market (by Vitamins), $Million, 2023-2033

- Table 143: GCC Countries Mass Spectrometry and Chromatography in Diagnostics Market (by Hormones), $Million, 2023-2033

- Table 144: South Africa Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), $Million, 2023-2033

- Table 145: South Africa Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Preparation), $Million, 2023-2033

- Table 146: South Africa Mass Spectrometry and Chromatography in Diagnostics Market (by Mass Spectrometry and Chromatography), $Million, 2023-2033

- Table 147: South Africa Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type), $Million, 2023-2033

- Table 148: South Africa Mass Spectrometry and Chromatography in Diagnostics Market (by Vitamins), $Million, 2023-2033

- Table 149: South Africa Mass Spectrometry and Chromatography in Diagnostics Market (by Hormones), $Million, 2023-2033

- Table 150: Rest-of-Middle East and Africa Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type), $Million, 2023-2033

- Table 151: Rest-of-Middle East and Africa Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Preparation), $Million, 2023-2033

- Table 152: Rest-of-Middle East and Africa Mass Spectrometry and Chromatography in Diagnostics Market (by Mass Spectrometry and Chromatography), $Million, 2023-2033

- Table 153: Rest-of-Middle East and Africa Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type), $Million, 2023-2033

- Table 154: Rest-of-Middle East and Africa Mass Spectrometry and Chromatography in Diagnostics Market (by Vitamins), $Million, 2023-2033

- Table 155: Rest-of-Middle East and Africa Mass Spectrometry and Chromatography in Diagnostics Market (by Hormones), $Million, 2023-2033

- Table 156: Global Mass Spectrometry and Chromatography in Diagnostics Market, Key Development Analysis, January 2015-June 2024

Global Mass Spectrometry and Chromatography in Diagnostics Market Industry Overview

The global mass spectrometry and chromatography in diagnostics market was valued at $743.1 million in 2023 and is expected to reach $1,863.8 million by 2033, growing at a CAGR of 9.92% between 2024 and 2033. The mass spectrometry (MS) and chromatography markets are critical components of the broader analytical and life sciences instrumentation sector. Both technologies offer sophisticated methods for the separation, identification, and quantification of chemical and biological substances and have been instrumental in driving advances across a variety of fields, including pharmaceuticals, environmental monitoring, diagnostics, and food safety, among others. For diagnostics applications, these technologies are mostly not used in isolation but are integrated into workflows. For instance, liquid chromatography-mass spectrometry combines the separation capabilities of liquid chromatography with the mass analysis power of mass spectrometry. This integration is particularly effective in complex sample analysis, where components need to be separated before their mass and structure can be determined. Such hybrid systems are critical in clinical settings for the high-throughput analysis of patient samples, offering a comprehensive understanding that guides diagnosis and treatment. The key applications of mass spectrometry and chromatography in diagnostics include vitamin profiling and hormone profiling, among others.

Market Introduction

| KEY MARKET STATISTICS | |

|---|---|

| Forecast Period | 2024 - 2033 |

| 2024 Evaluation | $795.9 Million |

| 2033 Forecast | $1,863.8 Million |

| CAGR | 9.92% |

The mass spectrometry and chromatography in diagnostics market is experiencing rapid growth, driven by multiple benefits offered by the technologies as compared to the traditional immunoassays, and continuous technological advancements in these technologies are further advancing their adoption. However, the high cost of acquisition of instrumentations, as well as the dearth of skilled professionals, is expected to hinder the growth of the global mass spectrometry and chromatography in diagnostics market.

Furthermore, there has been a shift toward the utilization of liquid chromatography-tandem mass spectrometry (LC-MS/MS) as a standard technique in diagnostics. The growing preference for LC-MS/MS in diagnostics is driven by its unparalleled analytical advantages, which include exceptional specificity, sensitivity, and the ability to conduct multiplex testing, qualities that are indispensable for complex diagnostic tasks. In addition to this, the integration of automated sample preparation systems in mass spectrometry-based diagnostics marks a pivotal advancement in clinical laboratory operations. This trend will continue to expand, driven by the increasing demands for faster, more accurate diagnostic testing and the ongoing advancements in technology.

Industrial Impact

This technology has a pivotal role in diagnostics applications such as therapeutic drug monitoring, vitamin analysis, hormone profiling, newborn screening, and infectious diseases, among others.

Market Segmentation:

Segmentation 1: by Product Type

- Sample Preparation

- Mass Spectrometry and Chromatography

Mass Spectrometry and Chromatography Segment to Dominate the Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type)

The mass spectrometry and chromatography segment is poised to dominate the mass spectrometry and chromatography in diagnostics market based on product type. This dominance has been driven by the high cost of the instrumentations of mass spectrometry and chromatography and the recurring use of consumables in diagnostics.

Segmentation 2: by Application Type

- Therapeutic Drug Monitoring

- Vitamins

- Hormones

- Methylmalonic Acid

- Immunosuppressants

- Others

Others Segment to Dominate the Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type)

The others segment is positioned to dominate the mass spectrometry and chromatography in diagnostics market by application type. This predominance is largely due to the fact that newborn screening was one of the earliest applications of mass spectrometry and chromatography in diagnostics. These technologies have been integral to this field for a long time, making a significant contribution to the market.

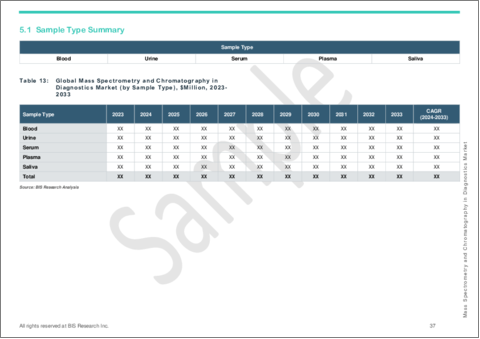

Segmentation 3: by Sample Type

- Blood

- Urine

- Serum

- Plasma

- Saliva

Serum to Dominate the Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Type)

The serum segment is positioned to dominate the mass spectrometry and chromatography in diagnostics market based on sample type due to its suitability for a broad spectrum of applications, from hormone profiling to vitamin analysis. This makes serum an ideal sample type for precise and comprehensive diagnostic tests.

Segmentation 4: by Testing Type

- Laboratory-Developed Tests

- Commercial Assays

Laboratory-Developed Tests to Dominate the Mass Spectrometry and Chromatography in Diagnostics Market (by Testing Type)

The laboratory-developed tests segment is positioned to dominate the mass spectrometry and chromatography in diagnostics market by testing type. On the other hand, the commercial assay segment is expected to be the fastest-growing segment, with a CAGR of 10.40% in the forecast period 2024-2033.

Segmentation 5: by Region

- North America

- U.S.

- Canada

- Europe

- Germany

- U.K.

- Spain

- Italy

- France

- Rest-of-Europe

- Asia-Pacific

- China

- Japan

- India

- Rest-of-Asia-Pacific

- Latin America

- Brazil

- Mexico

- Rest-of-Latin America

- Middle East and Africa

- GCC Countries

- South Africa

- Rest-of-Middle East and Africa

The global mass spectrometry and chromatography in diagnostics market (by region) has been dominated by North America, which held 45.10% of the market share in 2023 and is anticipated to retain its position in the market during the forecast period. The region boasts an advanced healthcare infrastructure, particularly in the U.S., which facilitates the adoption of cutting-edge medical technologies, including mass spectrometry and chromatography. Additionally, North America is the hub to many leading companies in the mass spectrometry and chromatography in diagnostics market, such as Agilent Technologies, Inc., Thermo Fisher Scientific Inc., and SCIEX (Danaher Corporation), among others whose strong presence and continuous innovation drive growth of the mass spectrometry and chromatography in diagnostics market.

Recent Developments in the Mass Spectrometry and Chromatography in Diagnostics Market

- In June 2024, Shimadzu Corporation introduced the new LCMS RX series of triple quadrupole mass spectrometry instruments.

- In October 2023, Revvity, Inc. announced a value-added distribution agreement with SCIEX. This strategic agreement was aimed at enhancing Revvity's newborn screening products by integrating SCIEX's innovative mass spectrometry solutions, leveraging expertise and resources from both companies.

- In August 2023, Thermo Fisher Scientific commercially launched the EXENT Solution upon receiving IVDR certification. This fully automated, integrated mass spectrometry system is designed to revolutionize the diagnosis and evaluation of patients suffering from monoclonal gammopathies, including multiple myeloma.

- In April 2023, Waters Corporation unveiled its next-generation Xevo TQ Absolute IVD mass spectrometer, expanding its MassTrak IVD LC-MS/MS Systems family for clinical diagnostic applications.

- In June 2022, PerkinElmer launched the GC 2400 Platform, an advanced, automated gas chromatography (GC), headspace sampler, and GC/mass spectrometry (GC/MS) solution designed to help lab teams simplify lab operations, drive precise results, and perform more flexible monitoring.

Demand - Drivers, Challenges, and Opportunities

Market Demand Drivers:

Shift from Traditional Methods to Mass Spectrometry and Chromatography in Clinical Diagnostics: The growing shift toward mass spectrometry and chromatography in clinical diagnostics represents a significant growth opportunity for the global mass spectrometry and chromatography in diagnostics market. As laboratories increasingly recognize the limitations of traditional immunoassays, the demand for more precise and efficient diagnostic technologies such as LC-MS/MS is expected to expand even more. This trend has been supported by the technology's ability to deliver accurate, robust, and cost-efficient results, which is crucial for improving patient outcomes and operational efficiency in clinical settings.

Market Challenges:

High Initial Set-Up Cost: The substantial upfront and recurring costs associated with mass spectrometry and chromatography systems present a formidable challenge for their broader adoption in clinical diagnostics. These financial barriers are particularly impactful for smaller laboratories and healthcare facilities with tight budgets, limiting their ability to invest in advanced diagnostic technologies.

Market Opportunities:

Focus on Emerging Markets for Expansion of Mass Spectrometry and Chromatography in Diagnostics: The global mass spectrometry and chromatography in diagnostics market presents substantial opportunities for growth in emerging countries, particularly through strategic focus on market expansion, growth opportunities in emerging economies, and the development of customized solutions. By focusing on affordability and accessibility, developing local partnerships and training programs, navigating regulatory requirements, and creating integrated diagnostic solutions, companies can unlock significant growth opportunities in the untapped markets of emerging countries.

How can this Report add Value to an Organization?

Product/Innovation Strategy: The global mass spectrometry and chromatography in diagnostics market has been segmented based on various categories, such as by product type, application type, sample type, testing type, and region.

Growth/Marketing Strategy: Partnerships, alliances, fundings, new offerings, and business expansions together accounted for the maximum number of key developments of the total developments in the mass spectrometry and chromatography in diagnostics market between January 2015 and June 2024.

Competitive Strategy: The global mass spectrometry and chromatography market consists of various public and few private companies. Key players in the mass spectrometry and chromatography in diagnostics market analyzed and profiled in the study involve established players that offer various kinds of products.

Methodology

Key Considerations and Assumptions in Market Engineering and Validation

- The base year considered for the calculation of the market size is 2023. A historical year analysis has been done for the period FY2018-FY2022. The market size has been estimated for FY2023 and projected for the period FY2024-FY2033.

- The scope of this report has been carefully derived based on interactions with experts in different companies across the world. This report provides a market study of mass spectrometry and chromatography in diagnostics.

- The market contribution of mass spectrometry and chromatography in diagnostics anticipated to be launched in the future has been calculated based on the historical analysis of the solutions.

- Revenues of the companies have been referenced from their annual reports FY2018-FY2023.

- The market has been mapped based on the available mass spectrometry and chromatography in diagnostics products. All the key companies with significant offerings in this field have been considered and profiled in this report.

Primary Research:

The primary sources involve industry experts in mass spectrometry and chromatography in diagnostics. Key opinion leaders (KOLs) such as CEOs, vice presidents, marketing directors, and technology and innovation directors have been interviewed to obtain and verify both qualitative and quantitative aspects of this research study.

The key data points taken from the primary sources include:

- validation and triangulation of all the numbers and graphs

- validation of the report's segmentation and key qualitative findings

- understanding the competitive landscape and business model

- current and proposed production values of a product by market players

- validation of the numbers of the different segments of the market in focus

- percentage split of individual markets for regional analysis

Secondary Research:

Open Sources

- Certified publications, articles from recognized authors, white papers, directories, and major databases, among others

- Annual reports, SEC filings, and investor presentations of the leading market players

- Company websites and detailed study of their product portfolio

- Gold standard magazines, journals, white papers, press releases, and news articles

- Paid databases

The key data points taken from the secondary sources include:

- segmentations and percentage shares

- data for market value

- key industry trends of the top players of the market

- qualitative insights into various aspects of the market, key trends, and emerging areas of innovation

- quantitative data for mathematical and statistical calculations

Key Market Players and Competition Synopsis

The companies profiled have been selected based on inputs gathered from primary experts and analyzing company coverage, product portfolio, and market penetration.

The mass spectrometry and chromatography in diagnostics market (by product type) dominates by mass spectrometry and chromatography segment, securing a share of 85.34% in 2023. Sample preparation, on the other hand, accounted for approximately 14.66% of the market share in 2023.

Some prominent names established in this market are:

- Agilent Technologies, Inc.

- Thermo Fisher Scientific Inc.

- Waters Corporation

- Tecan Group Ltd.

- Danaher Corporation

- Shimadzu Corporation

- Merck KGaA

- Bio-Rad Laboratories, Inc.

- PerkinElmer Inc.

- Promega Corporation

- Restek Corporation

- Gerstel GmbH & Co. KG

- Phenomenex Inc. (Danaher Corporation)

- Bruker Corporation

- New England Biolabs

- Hamilton Company

- Avantor, Inc. (VWR International, LLC.)

- Chromsystems Instruments & Chemicals GmbH

- RECIPE Chemicals + Instruments GmbH

- Zivak

- SENTINEL CH. SpA

Table of Contents

Executive Summary

Scope and Definition

1 Global Mass Spectrometry and Chromatography in Diagnostics Market: Industry Outlook

- 1.1 Market Overview

- 1.2 Key Trends

- 1.2.1 Shift toward Utilization of Liquid Chromatography-Tandem Mass Spectrometry (LC-MS/MS) as Standard Technique in Diagnostics

- 1.2.2 Utilization of Automated Sample Preparation Technologies

- 1.3 Opportunity Assessment of Key Trends

- 1.4 Product Benchmarking

- 1.5 Regulatory Landscape

- 1.5.1 Regulatory Framework in the U.S.

- 1.5.1.1 Recommendations for Diagnostic Approval

- 1.5.2 Regulatory Framework in Europe

- 1.5.2.1 Recommendations for Diagnostic Approval

- 1.5.3 Regulatory Framework in Asia-Pacific

- 1.5.3.1 China

- 1.5.1 Regulatory Framework in the U.S.

2 Global Mass Spectrometry and Chromatography in Diagnostics Market: Market Dynamics

- 2.1 Impact Analysis

- 2.2 Market Drivers

- 2.2.1 Continuous Technological Advancements in Mass Spectrometry and Chromatography Instruments

- 2.2.2 Shift from Traditional Methods to Mass Spectrometry and Chromatography in Clinical Diagnostics

- 2.3 Market Restraints

- 2.3.1 High Initial Set-Up Cost

- 2.3.2 Skill Gap and Dearth Skilled Professionals

- 2.4 Market Opportunities

- 2.4.1 Focus on Emerging Markets for Expansion of Mass Spectrometry and Chromatography in Diagnostics

3 Global Mass Spectrometry and Chromatography in Diagnostics Market (by Product Type)

- 3.1 Product Type Summary

- 3.2 Growth-Share Matrix

- 3.3 Sample Preparation

- 3.3.1 Instruments

- 3.3.1.1 Manual Sample Preparation Instrument

- 3.3.1.2 Automated Sample Preparation Instrument

- 3.3.1.3 Integrated Sample Preparation Instrument

- 3.3.2 Reagents and Kits

- 3.3.2.1 Sample Lysis and Extraction Kits

- 3.3.2.2 Depletion and Enrichment Kits

- 3.3.2.3 Clean-Up Kits

- 3.3.2.4 Digestion Kits

- 3.3.2.5 Accessories

- 3.3.1 Instruments

- 3.4 Mass Spectrometry and Chromatography

- 3.4.1 Consumables

- 3.4.1.1 Kits

- 3.4.1.2 Calibration Solutions

- 3.4.1.3 Controls and Standards

- 3.4.1.4 Solvents

- 3.4.1.5 Columns

- 3.4.1.6 Vials

- 3.4.2 Instruments

- 3.4.2.1 Mass Spectrometry

- 3.4.2.2 Liquid Chromatography

- 3.4.2.3 Gas Chromatography

- 3.4.2.4 Hybrid Mass Spectrometry

- 3.4.3 Data Analysis Software

- 3.4.1 Consumables

4 Global Mass Spectrometry and Chromatography in Diagnostics Market (by Application Type)

- 4.1 Application Type Summary

- 4.2 Growth-Share Matrix

- 4.3 Therapeutic Drug Monitoring

- 4.4 Vitamins

- 4.4.1 Vitamin-A

- 4.4.2 Vitamin-B1

- 4.4.3 Vitamin-B6

- 4.4.4 Vitamin-E

- 4.4.5 Others

- 4.5 Hormones

- 4.5.1 Metanephrines

- 4.5.2 Catecholamines

- 4.5.3 Steroids

- 4.5.4 Others

- 4.6 Methylmalonic Acid (MMA)

- 4.7 Immunosuppressants

- 4.8 Others

5 Global Mass Spectrometry and Chromatography in Diagnostics Market (by Sample Type)

- 5.1 Sample Type Summary

- 5.2 Growth-Share Matrix

- 5.3 Blood

- 5.4 Urine

- 5.5 Serum

- 5.6 Plasma

- 5.7 Saliva

6 Global Mass Spectrometry and Chromatography in Diagnostics Market (by Testing Type)

- 6.1 Testing Type Summary

- 6.2 Growth-Share Matrix

- 6.3 Laboratory-Developed Tests

- 6.4 Commercial Assays

7 Global Mass Spectrometry and Chromatography in Diagnostics Market (by Region)

- 7.1 Regional Summary

- 7.2 Drivers and Restraints

- 7.3 North America

- 7.3.1 Regional Overview

- 7.3.2 Driving Factors for Market Growth

- 7.3.3 Factors Challenging the Market

- 7.3.4 By Product Type

- 7.3.5 By Application Type

- 7.3.6 U.S.

- 7.3.6.1 By Product Type

- 7.3.6.2 By Application Type

- 7.3.7 Canada

- 7.3.7.1 By Product Type

- 7.3.7.2 By Application Type

- 7.4 Europe

- 7.4.1 Regional Overview

- 7.4.2 Driving Factors for Market Growth

- 7.4.3 Factors Challenging the Market

- 7.4.4 By Product Type

- 7.4.5 By Application Type

- 7.4.6 U.K.

- 7.4.6.1 By Product Type

- 7.4.6.2 By Application Type

- 7.4.7 Germany

- 7.4.7.1 By Product Type

- 7.4.7.2 By Application Type

- 7.4.8 France

- 7.4.8.1 By Product Type

- 7.4.8.2 By Application Type

- 7.4.9 Italy

- 7.4.9.1 By Product Type

- 7.4.9.2 By Application Type

- 7.4.10 Spain

- 7.4.10.1 By Product Type

- 7.4.10.2 By Application Type

- 7.4.11 Rest-of-Europe

- 7.4.11.1 By Product Type

- 7.4.11.2 By Application Type

- 7.5 Asia-Pacific

- 7.5.1 Regional Overview

- 7.5.2 Driving Factors for Market Growth

- 7.5.3 Factors Challenging the Market

- 7.5.4 By Product Type

- 7.5.5 By Application Type

- 7.5.6 Japan

- 7.5.6.1 By Product Type

- 7.5.6.2 By Application Type

- 7.5.7 China

- 7.5.7.1 By Product Type

- 7.5.7.2 By Application Type

- 7.5.8 India

- 7.5.8.1 By Product Type

- 7.5.8.2 By Application Type

- 7.5.9 Rest-of-Asia-Pacific

- 7.5.9.1 By Product Type

- 7.5.9.2 By Application Type

- 7.6 Latin America

- 7.6.1 Regional Overview

- 7.6.2 Driving Factors for Market Growth

- 7.6.3 Factors Challenging the Market

- 7.6.4 By Product Type

- 7.6.5 By Application Type

- 7.6.6 Brazil

- 7.6.6.1 By Product Type

- 7.6.6.2 By Application Type

- 7.6.7 Mexico

- 7.6.7.1 By Product Type

- 7.6.7.2 By Application Type

- 7.6.8 Rest-of-Latin America

- 7.6.8.1 By Product Type

- 7.6.8.2 By Application Type

- 7.7 Middle East and Africa

- 7.7.1 Regional Overview

- 7.7.2 Driving Factors for Market Growth

- 7.7.3 Factors Challenging the Market

- 7.7.4 By Product Type

- 7.7.5 By Application Type

- 7.7.6 GCC Countries

- 7.7.6.1 By Product Type

- 7.7.6.2 By Application Type

- 7.7.7 South Africa

- 7.7.7.1 By Product Type

- 7.7.7.2 By Application Type

- 7.7.8 Rest-of-Middle East and Africa

- 7.7.8.1 By Product Type

- 7.7.8.2 By Application Type

8 Global Mass Spectrometry and Chromatography in Diagnostics Market: Competitive Benchmarking and Company Profile

- 8.1 Competitive Landscape

- 8.1.1 Partnerships, Alliances, and Business Expansions

- 8.1.2 New Offerings

- 8.1.3 Mergers and Acquisitions

- 8.1.4 Regulatory Approvals

- 8.2 Key Strategies and Development

- 8.3 Company Competition Matrix

- 8.4 Company Share Analysis

- 8.5 Company Profiles

- 8.5.1 Agilent Technologies, Inc.

- 8.5.1.1 Overview

- 8.5.1.2 Top Products

- 8.5.1.3 Top Competitors

- 8.5.1.4 Top Customers

- 8.5.1.5 Key Personnel

- 8.5.1.6 Analyst View

- 8.5.2 Thermo Fisher Scientific, Inc.

- 8.5.2.1 Overview

- 8.5.2.2 Top Products

- 8.5.2.3 Top Competitors

- 8.5.2.4 Top Customers

- 8.5.2.5 Key Personnel

- 8.5.2.6 Analyst View

- 8.5.3 Waters Corporation

- 8.5.3.1 Overview

- 8.5.3.2 Top Products

- 8.5.3.3 Top Competitors

- 8.5.3.4 Top Customers

- 8.5.3.5 Key Personnel

- 8.5.3.6 Analyst View

- 8.5.4 Tecan Group Ltd.

- 8.5.4.1 Overview

- 8.5.4.2 Top Products

- 8.5.4.3 Top Competitors

- 8.5.4.4 Top Customers

- 8.5.4.5 Key Personnel

- 8.5.4.6 Analyst View

- 8.5.5 Danaher Corporation

- 8.5.5.1 Overview

- 8.5.5.2 Top Products

- 8.5.5.3 Top Competitors

- 8.5.5.4 Top Customers

- 8.5.5.5 Key Personnel

- 8.5.5.6 Analyst View

- 8.5.6 Shimadzu Corporation

- 8.5.6.1 Overview

- 8.5.6.2 Top Products

- 8.5.6.3 Top Competitors

- 8.5.6.4 Top Customers

- 8.5.6.5 Key Personnel

- 8.5.6.6 Analyst View

- 8.5.7 Merck KGaA

- 8.5.7.1 Overview

- 8.5.7.2 Top Products

- 8.5.7.3 Top Competitors

- 8.5.7.4 Top Customers

- 8.5.7.5 Key Personnel

- 8.5.7.6 Analyst View

- 8.5.8 Bio-Rad Laboratories, Inc.

- 8.5.8.1 Overview

- 8.5.8.2 Top Products

- 8.5.8.3 Top Competitors

- 8.5.8.4 Top Customers

- 8.5.8.5 Key Personnel

- 8.5.8.6 Analyst View

- 8.5.9 PerkinElmer Inc.

- 8.5.9.1 Overview

- 8.5.9.2 Top Products

- 8.5.9.3 Top Competitors

- 8.5.9.4 Top Customers

- 8.5.9.5 Key Personnel

- 8.5.9.6 Analyst View

- 8.5.10 Promega Corporation

- 8.5.10.1 Overview

- 8.5.10.2 Top Products

- 8.5.10.3 Top Competitors

- 8.5.10.4 Top Customers

- 8.5.10.5 Key Personnel

- 8.5.10.6 Analyst View

- 8.5.11 Restek Corporation

- 8.5.11.1 Overview

- 8.5.11.2 Top Products

- 8.5.11.3 Top Competitors

- 8.5.11.4 Top Customers

- 8.5.11.5 Key Personnel

- 8.5.11.6 Analyst View

- 8.5.12 GERSTEL GmbH & Co. KG

- 8.5.12.1 Overview

- 8.5.12.2 Top Products

- 8.5.12.3 Top Competitors

- 8.5.12.4 Top Customers

- 8.5.12.5 Key Personnel

- 8.5.12.6 Analyst View

- 8.5.13 Bruker Corporation

- 8.5.13.1 Overview

- 8.5.13.2 Top Products

- 8.5.13.3 Top Competitors

- 8.5.13.4 Top Customers

- 8.5.13.5 Key Personnel

- 8.5.13.6 Analyst View

- 8.5.14 New England Biolabs

- 8.5.14.1 Overview

- 8.5.14.2 Top Products

- 8.5.14.3 Top Competitors

- 8.5.14.4 Top Customers

- 8.5.14.5 Key Personnel

- 8.5.14.6 Analyst View

- 8.5.15 Hamilton Company

- 8.5.15.1 Overview

- 8.5.15.2 Top Products

- 8.5.15.3 Top Competitors

- 8.5.15.4 Top Customers

- 8.5.15.5 Key Personnel

- 8.5.15.6 Analyst View

- 8.5.16 Avantor, Inc. (VWR International, LLC.)

- 8.5.16.1 Overview

- 8.5.16.2 Top Products

- 8.5.16.3 Top Competitors

- 8.5.16.4 Top Customers

- 8.5.16.5 Key Personnel

- 8.5.16.6 Analyst View

- 8.5.17 Chromsystems Instruments & Chemicals GmbH.

- 8.5.17.1 Overview

- 8.5.17.2 Top Products

- 8.5.17.3 Top Competitors

- 8.5.17.4 Top Customers

- 8.5.17.5 Key Personnel

- 8.5.17.6 Analyst View

- 8.5.18 RECIPE Chemicals + Instruments GmbH

- 8.5.18.1 Overview

- 8.5.18.2 Top Products

- 8.5.18.3 Top Competitors

- 8.5.18.4 Top Customers

- 8.5.18.5 Key Personnel

- 8.5.18.6 Analyst View

- 8.5.19 Zivak

- 8.5.19.1 Overview

- 8.5.19.2 Top Products

- 8.5.19.3 Top Competitors

- 8.5.19.4 Top Customers

- 8.5.19.5 Key Personnel

- 8.5.19.6 Analyst View

- 8.5.20 SENTINEL CH. SpA

- 8.5.20.1 Overview

- 8.5.20.2 Top Products

- 8.5.20.3 Top Competitors

- 8.5.20.4 Top Customers

- 8.5.20.5 Key Personnel

- 8.5.20.6 Analyst View

- 8.5.1 Agilent Technologies, Inc.

9 Research Methodology

- 9.1 Data Sources

- 9.1.1 Primary Data Sources

- 9.1.2 Secondary Data Sources

- 9.1.3 Data Triangulation