|

|

市場調査レポート

商品コード

1445391

米国の製造業向けロボティクス統合市場:市場・用途・技術への焦点、分析と予測 (2024-2029年)U.S. Robotics Integration for the Manufacturing Market - Analysis and Forecast, 2024-2029: Focus on Market, Applications and Technologies |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 米国の製造業向けロボティクス統合市場:市場・用途・技術への焦点、分析と予測 (2024-2029年) |

|

出版日: 2024年03月07日

発行: BIS Research

ページ情報: 英文 97 Pages

納期: 1~5営業日

|

全表示

- 概要

- 図表

- 目次

米国の製造業向けロボティクス統合の市場規模は、2029年には74億8,000万米ドルの規模に達すると予測されています。

米国のロボティクス統合は、自動化、AI、機械学習の進歩によって牽引されており、産業および技術的情勢の変革を示しています。ロボティクス統合は、効率性、生産性、安全性を向上させることで、製造、ヘルスケア、サービスを含むさまざまな産業を再構築しています。この移行は、政策立案者、教育機関、ロボットシステムメーカー、エンドユーザーを巻き込んだ強固なエコシステムによって支えられており、イノベーションと成長を促す環境が整えられています。

| 主要市場統計 | |

|---|---|

| 予測期間 | 2024-2029年 |

| 2024年評価額 | 43億米ドル |

| 2029年予測 | 74億8,000万米ドル |

| CAGR | 11.69% |

米国政府は、ロボティクスの戦略的重要性を認識し、R&D、人材育成、倫理的配備を促進するために、いくつかのプログラムや投資を開始しました。例えば、Advanced Robotics for Manufacturing (ARM) Instituteは、この分野における米国の世界的リーダーシップを強化するための協調的努力を反映しています。さらに、大学と産業界の協働は、ロボット技術の限界を押し広げ、有能な人材の安定した流れを確保し、統合の課題に取り組む上で極めて重要です。

用途別では、自動車部門が市場をリードしています。その主な理由は、大量生産と精密製造という本質的ニーズが、ロボットシステムの能力とシームレスに合致しているためです。自動車業界では、AI、ADAS、V2X (Vehicle-to-Everything) インフラの拡大により、コネクティビティと技術の急速な進化が推進され、この分野は自動運転へと舵を切っています。自動車製造におけるロボティクスの統合は、高度な部品の生産における精度と品質、急増する需要に対応する拡張性、急速に進化する技術への適応性を提供し、この変革に役立っています。製造業向けロボティクスは、最新の自動車に必要な複雑な組立工程を下支えし、自動車業界が最新のAI、ADAS、V2Xシステムを搭載した自動車を効率的に生産できるようにすることで、自動車技術とモビリティの未来を形成します。

当レポートでは、米国の製造業向けロボティクス統合の市場を調査し、市場概要、市場影響因子の分析、市場規模の推移・予測、各種区分別の詳細分析、競合情勢、主要企業の分析、成長機会の分析などをまとめています。

目次

エグゼクティブサマリー

調査範囲

第1章 市場

- 業界の展望

- 製造業向けロボティクス市場:概要

- インダストリー4.0からインダストリー5.0への移行

- ロボット産業を可能にする動向

- ロボットの効率と精度の分析

- 主要業界における従来型および非従来型のユースケース

- 規格と規制

- スタートアップと投資の情勢

- 事業力学

- 事業促進要因

- 事業上の課題

- 事業機会

第2章 用途

- 米国の製造業向けロボティクス統合市場 (用途別)

- 市場概要

- 航空

- スペーステック

- 自動車

- CE製品

- 半導体

- 再生可能エネルギー・電力

- フードテック

- 倉庫保管

- ヘルステック・メッドテック

第3章 製品

- 米国の製造業向けロボティクス統合市場 (タイプ別)

- 市場概要

- 自律移動ロボット (AMR)

- 無人搬送車 (AGV)

- 協働ロボット (コボット)

- その他

第4章 市場:競合ベンチマーキングと企業プロファイル

- 競合ベンチマーキング

- 企業プロファイル

- ACRO Automation Systems, Inc.

- Andrews Cooper

- Bastian Solutions, LLC

- Cleveland Automation Systems

- Dynamic Automation

- enVista, LLC.

- KC Robotics

- Productivity Inc.

- Remtec Automation, LLC.

- Steven Douglas Corp.

- その他の主要参入企業

第5章 成長機会と推奨事項

- 成長機会

- 成長機会1:自動車市場からの需要の拡大

- 成長機会2:倉庫自動化の需要の拡大

第6章 調査手法

List of Figures

- Figure 1: U.S. Robotics Integration for the Manufacturing Market, $Billion, 2023-2029

- Figure 2: U.S. Robotics Integration for the Manufacturing Market, Units, 2023 to 2029

- Figure 3: U.S. Robotics Integration for the Manufacturing Market (by Application), $Billion, 2024-2029

- Figure 4: U.S. Robotics Integration for the Manufacturing Market (by Application), Units, 2024-2029

- Figure 5: U.S. Robotics Integration for the Manufacturing Market (by Type), $Billion, 2024 to 2029

- Figure 6: U.S. Robotics Integration for the Manufacturing Market (by Type), Units, 2024-2029

- Figure 7: U.S. Robotics Integration for the Manufacturing Market Coverage

- Figure 8: U.S. Robotics Integration for the Manufacturing Market, Business Dynamics

- Figure 9: U.S. Robotics Integration for the Manufacturing Market (by Application)

- Figure 10: U.S. Robotics Integration for the Manufacturing Market (by Type)

- Figure 11: U.S. Robotics Integration for the Manufacturing Market: Competitive Benchmarking, 2023

- Figure 12: Research Methodology

- Figure 13: Top-Down and Bottom-Up Approach

- Figure 14: Assumptions and Limitations

List of Tables

- Table 1: Industry 4.0 vs. Industry 5.0

- Table 2: Level of Collaboration Between Humans and Robots

- Table 3: Funding and Investment Comparisons, July 2021-December 2023

- Table 4: U.S. Robotics Integration for the Manufacturing Market (by Application), $Million, 2023-2029

- Table 5: U.S. Robotics Integration for the Manufacturing Market (by Application), Units, 2023-2029

- Table 6: U.S. Robotics Integration for the Manufacturing Market (by Type), $Million, 2023-2029

- Table 7: U.S. Robotics Integration for the Manufacturing Market (by Type), Units, 2023-2029

- Table 8: Bastian Solutions, LLC: Product Portfolio

- Table 9: Bastian Solutions, LLC: Product Developments and Fundings

- Table 10: Bastian Solutions, LLC: Partnerships, Collaborations, Contracts, and Agreements

- Table 11: Productivity, Inc.: Product Portfolio

The U.S. Robotics Integration for the Manufacturing Market Expected to Reach $7.48 Billion by 2029

Introduction of U.S. Robotics Integration for the Manufacturing

Robotics integration in the U.S. signifies a transformative phase in the industrial and technological landscapes, driven by advancements in automation, artificial intelligence, and machine learning. The integration of robotics is reshaping various sectors, including manufacturing, healthcare, and service industries, by enhancing efficiency, productivity, and safety. This transition is supported by a robust ecosystem involving policymakers, educational institutions, manufacturers of robotic systems, and end users, fostering a conducive environment for innovation and growth.

| KEY MARKET STATISTICS | |

|---|---|

| Forecast Period | 2024 - 2029 |

| 2024 Evaluation | $4.30 Billion |

| 2029 Forecast | $7.48 Billion |

| CAGR | 11.69% |

The U.S. government, recognizing the strategic importance of robotics, has initiated several programs and investments to accelerate research and development, workforce training, and ethical deployment of robotics. For instance, the Advanced Robotics for Manufacturing (ARM) Institute reflects a concerted effort to fortify the country's global leadership in this domain. Moreover, collaboration between universities and industry is pivotal in pushing the boundaries of robotics technology, ensuring a steady flow of skilled labor, and addressing the challenges of integration.

Market Introduction

The integration of robotics in the U.S. manufacturing sector marks a significant paradigm shift toward Industry 5.0, which emphasizes a human-centric approach, increased resilience, and focus on sustainability, shifting from a sole focus on efficiency and productivity to a broader vision of industry contributing to society's well-being. Industry 5.0 is value-driven, combining technology with a focus on people and environment. The manufacturing market is increasingly embracing robotics to address challenges such as labor shortages, need for precision and consistency in production, and imperative for sustainable practices. Robotics integration is pivotal in automating repetitive and hazardous tasks, leading to enhanced efficiency and reduced downtime. Advanced robotic systems equipped with sensors and AI capabilities are enabling predictive maintenance, quality control, and customized production, aligning with the just-in-time manufacturing model.

Furthermore, the rise of cobots is a notable trend. Cobots are designed to work alongside humans, enhancing safety and productivity. Cobots are being increasingly adopted for tasks that require precision and flexibility, proving to be cost-effective for small- and medium-sized enterprises. Robotics offers solutions for material handling, packaging, and logistics. Automated guided vehicles (AGVs) and autonomous mobile robots (AMRs) are revolutionizing warehouse operations, ensuring timely and accurate fulfillment of orders.

Additionally, the U.S. government is actively involved in shaping policies to ensure a balanced approach to robotics integration, addressing concerns related to labor displacement, privacy, and ethical considerations. Collaboration between regulatory bodies and industry stakeholders is vital to establishing standards and best practices.

Industrial Impact

The integration of robotics in the U.S. manufacturing market is profoundly reshaping the industrial landscape, heralding a new era of productivity, innovation, and competitiveness. Robotics integration fundamentally alters production processes, enabling higher throughput, precision, and consistency. Automated production lines powered by robotics minimize human error, reduce waste, and ensure optimal utilization of resources. This efficiency is critical in sectors where precision and repeatability are paramount, such as electronics, automotive, and pharmaceuticals.

Moreover, the integration of robotics in the U.S. manufacturing market is a multi-dimensional paradigm shift, influencing not just the production processes but also the economic, educational, and social fabrics of the industrial sector. This transformation, while replete with challenges, presents immense opportunities for growth, innovation, and sustainable development, asserting the pivotal role of robotics in shaping the future of U.S. manufacturing.

Market Segmentation:

Segmentation 1: by Application

- Aviation

- SpaceTech

- Automotive

- Consumer Electronics

- Semiconductor

- Renewable Energy and Power

- FoodTech

- Warehousing

- HealthTech and MedTech

Automotive Segment to Dominate the U.S. Robotics Integration for the Manufacturing Market (by Application)

The automotive segments in the U.S. robotics integration for the manufacturing market is leading the market, principally attributed to its intrinsic need for high-volume, precision manufacturing, which aligns seamlessly with the capabilities of robotic systems. In the automotive industry, the rapid evolution of connectivity and technology, propelled by advancements in artificial intelligence (AI), advanced driver assistance systems (ADAS), and expanding vehicle-to-everything (V2X) infrastructure, is steering the sector toward autonomous driving. The integration of robotics in automotive manufacturing is instrumental in this transformation, offering precision and quality in the production of sophisticated components, scalability to meet the surging demand, and adaptability to rapidly evolving technology. Robotics in manufacturing underpins the complex assembly processes required for modern vehicles, ensuring that the automotive industry can efficiently produce vehicles equipped with the latest AI, ADAS, and V2X systems, thereby shaping the future of automotive technology and mobility.

Segmentation 2: by Type

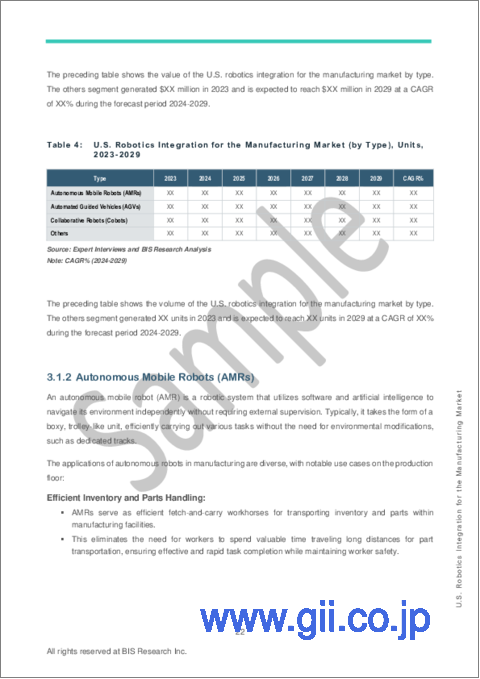

- Autonomous Mobile Robots (AMRs)

- Automated Guided Vehicles (AGVs)

- Collaborative Robots (Cobots)

- Others

Recent Developments in the U.S. Robotics Integration for the Manufacturing Market

- In January 2024, Teledyne FLIR IIS committed to revolutionizing machine vision with its latest Spinnaker 4 release, a GeniCam3 API library, which sets a new standard for machine vision developers with unparalleled performance and reliability. Tested under extreme conditions, including continuous operation with 40 GigE cameras for multiple days, it maintains flawless image capture and efficient processing even at over 90% CPU usage. This advancement underscores Teledyne FLIR IIS's dedication to delivering top-tier imaging technologies, ensuring reliability without compromising performance in challenging industrial environments.

- In July 2023, Kivnon, a global provider of autonomous mobile robots (AMRs) and automated guided vehicles (AGVs), announced a partnership with TAP, a prominent industrial solutions provider, for the distribution of Kivnon AGVs and AMRs. Kivnon specializes in designing, manufacturing, and implementing AGVs and AMRs across various industries, including automotive, food, aerospace, and retail. Its product range includes small AGVs for lab use, mouse AGV platforms for pallet handling, tractor AGVs for cart pulling, and self-driving forklifts. This collaboration with TAP aims to capitalize on the growing interest in AGVs and AMRs driven by Industry 4.0's digital transformation.

- In February 2023, ABB introduced the SWIFTI CRB 1300 industrial collaborative robot, featuring an enhanced load-handling capacity of up to 11kg. The robot is designed to address the intersection of industrial and collaborative robots, offering features such as palletizing and pick-and-place functionalities. With a reported top speed of 6.2m/s, the solution provides payload options ranging from 7kg to 11kg and reaches from 0.9 to 1.4 meters. Notably, it can handle higher payload tasks such as screwdriving. ABB's commitment to durability is evident in the robot's additional protection against dust and moisture, which achieved an IP67 rating and made it suitable for demanding applications such as machine tending.

Demand - Drivers, Challenges, and Opportunities

Market Drivers: Increase in the Role of AI and ML in Robotics Technology

The ongoing evolution of robotic technology, enhanced by artificial intelligence (AI) and machine learning (ML), is instrumental in enabling robots to tackle more intricate tasks and swiftly adapt to dynamic environments. This technological progress is a driving force behind the escalating demand for robotics integration for the manufacturing industry.

Market Challenges: Lack of Expertise in Robotics Integration

Securing competent support staff well-versed in the intricacies of industrial robots is crucial for companies aiming for excellence in robotics system integration. However, the scarcity of candidates with the requisite skills poses a significant challenge. With industrial robots evolving in complexity regarding technicalities, features, and products, companies are grappling with the dual challenge of finding and equipping their staff with the necessary capabilities to meet customer demands.

Market Opportunities: Rise of Robots-as-a-Service in Manufacturing

As manufacturers seek agile, efficient, and cost-effective solutions, robots-as-a-service emerges as a transformative opportunity in the robotics integration market. The advent of robots-as-a-service (RaaS) is poised to revolutionize the landscape of robotics integration in manufacturing, presenting a compelling opportunity for industry players. Rapid Robotics, a leading RaaS provider, exemplifies the potential benefits, offering manufacturers the promise of setting up automated systems within weeks at a fixed cost, inclusive of comprehensive service and support.

How can this report add value to an organization?

Product/Innovation Strategy: The product segment helps the reader understand the different types of products available for deployment and their potential globally. Moreover, the study provides the reader with a detailed understanding of the U.S. robotics integration for the manufacturing market by applications such as aviation, SpaceTech, automotive, consumer electronics, semiconductor, renewable energy and power, FoodTech, warehousing, and HealthTech and MedTech and on the basis of type, the market has been segmented into autonomous mobile robots (AMRs), automated guided vehicles (AGVs), collaborative robots (cobots), and others.

Growth/Marketing Strategy: The U.S. robotics integration for the manufacturing market has seen development by robot manufacturers and robot integrators operating in the market, such as business expansion, partnership, collaboration, and joint venture. The favored strategy for the companies has been the launch of new products to strengthen their position in the U.S. robotics integration for the manufacturing market. For instance, in December 2023, Brightpick, a warehouse automation solutions provider, revealed details about its advanced machine vision and AI technologies crucial for its Brightpick Autopicker robots. These technologies enable tasks such as scanning totes, creating 3D models, and determining optimal picking angles. The Brightpick Intuition software orchestrates the entire robot fleet for maximum throughput in e-commerce and e-grocery warehouses. The Autopicker, an autonomous mobile robot, uses a two-axis SCARA robotic arm with suction cups driven by AI and machine vision, ensuring picking accuracy for a diverse range of products.

Competitive Strategy: Key players in the U.S. robotics integration for the manufacturing market analyzed and profiled in the study involve robot manufacturers and robot integrators. Moreover, a detailed competitive benchmarking of the players operating in the U.S. robotics integration for the manufacturing market has been done to help the reader understand how players stack against each other, presenting a clear market landscape. Additionally, comprehensive competitive strategies such as partnerships, agreements, and collaborations will aid the reader in understanding the untapped revenue pockets in the market.\

Methodology: The research methodology design adopted for this specific study includes a mix of data collected from primary and secondary data sources. Both primary resources (key players, market leaders, and in-house experts) and secondary research (a host of paid and unpaid databases), along with analytical tools, have been employed to build the predictive and forecast models.

Data and validation have been taken into consideration from both primary sources as well as secondary sources.

Key Considerations and Assumptions in Market Engineering and Validation

- Detailed secondary research has been done to ensure maximum coverage of manufacturers/suppliers operational in a country.

- Exact revenue information, up to a certain extent, has been extracted for each company from secondary sources and databases. Revenues specific to product/application/technology were then estimated based on fact-based proxy indicators as well as primary inputs.

- Based on the classification, the average selling price (ASP) has been calculated using the weighted average method.

- The currency conversion rate has been taken from the historical exchange rate of Oanda and/or other relevant websites.

- Any economic downturn in the future has not been taken into consideration for the market estimation and forecast.

- The base currency considered for the market analysis is US$. Currencies other than the US$ have been converted to the US$ for all statistical calculations, considering the average conversion rate for that particular year.

- The term "product" in this document may refer to "service" or "technology" as and where relevant.

- The term "manufacturers/suppliers" may refer to "service providers" or "technology providers" as and where relevant.

Primary Research

The primary sources involve industry experts from the robotic industry, including robot manufacturers and robotic integration solution providers. Respondents such as CEOs, vice presidents, marketing directors, and technology and innovation directors have been interviewed to obtain and verify both qualitative and quantitative aspects of this research study.

Secondary Research

This study involves the usage of extensive secondary research, company websites, directories, and annual reports. It also makes use of databases, such as Businessweek and others, to collect effective and useful information for a market-oriented, technical, commercial, and extensive study of the global market. In addition to the data sources, the study has been undertaken with the help of other data sources and websites.

Secondary research was done to obtain critical information about the industry's value chain, the market's monetary chain, revenue models, the total pool of key players, and the current and potential use cases and applications.

Key Market Players and Competition Synopsis

The companies that are profiled have been selected based on thorough secondary research, which includes analyzing company coverage, product portfolio, market penetration, and insights gathered from primary experts.

The U.S. robotics integration for the manufacturing market comprises key players who have established themselves thoroughly and have the proper understanding of the market, accompanied by start-ups looking forward to establishing themselves in this highly competitive market. In 2022, the U.S. robotics integration for the manufacturing market was dominated by established players, accounting for 90% of the market share, whereas start-ups managed to capture 10% of the market. With the growing need for advanced diagnostic tools and quality assurance in various industries, the U.S. robotics integration for the manufacturing market is expected to see significant expansion. This growth is driven by expanding applications of robotics across sectors, including automotive, electronics, and healthcare, and the rising demand for precision, efficiency, and safety in production lines.

Some prominent names established in this market are:

- Andrews Cooper

- Steven Douglas Corp.

- Cleveland Automation Systems

- Bastian Solutions, LLC

- KC Robotics

- enVista, LLC.

- Productivity Inc.

- Remtec Automation, LLC.

- Dynamic Automation

- ACRO Automation Systems, Inc.

Table of Contents

Executive Summary

Scope of the Study

1 Market

- 1.1 Industry Outlook

- 1.1.1 Robotic Integration for the Manufacturing Market: Overview

- 1.1.1.1 Vision Systems

- 1.1.1.2 Machine Control and Integration

- 1.1.1.3 Material Handling and Motion Control

- 1.1.1.4 Platforms, Systems, and Architecture

- 1.1.2 Transition from Industry 4.0 to Industry 5.0

- 1.1.3 Trends Enabling the Robotics Industry

- 1.1.3.1 Internet of Robotic Things (IoRT)

- 1.1.3.2 5G-Enabled Smart Factory

- 1.1.3.3 Autonomous Mobile Robots

- 1.1.3.4 Collaborative Robot (Cobot) Integration with Humans

- 1.1.4 Robotic Efficiency and Accuracy Analysis

- 1.1.5 Traditional and Non-Traditional Use Cases in Key Industries

- 1.1.6 Standards and Regulations

- 1.1.7 Startups and Investment Landscape

- 1.1.1 Robotic Integration for the Manufacturing Market: Overview

- 1.2 Business Dynamics

- 1.2.1 Business Drivers

- 1.2.1.1 Increase in the Role of AI and ML in Robotics Technology

- 1.2.1.2 Increase in the Prevalence of Robotic Palletizing

- 1.2.2 Business Challenges

- 1.2.2.1 Lack of Expertise in Robotics Integration

- 1.2.3 Business Opportunities

- 1.2.3.1 Rise of Robots-as-a-Service (RaaS) in Manufacturing

- 1.2.1 Business Drivers

2 Application

- 2.1 U.S. Robotics Integration for the Manufacturing Market (by Application)

- 2.1.1 Market Overview

- 2.1.1.1 Demand Analysis of U.S. Robotics Integration for the Manufacturing Market (by Application), Value and Volume

- 2.1.2 Aviation

- 2.1.2.1 Trend Analysis

- 2.1.3 SpaceTech

- 2.1.3.1 Trend Analysis

- 2.1.4 Automotive

- 2.1.4.1 Trend Analysis

- 2.1.5 Consumer Electronics

- 2.1.5.1 Trend Analysis

- 2.1.6 Semiconductor

- 2.1.6.1 Trend Analysis

- 2.1.7 Renewable Energy and Power

- 2.1.7.1 CleanTech

- 2.1.7.2 Nuclear

- 2.1.7.3 BlueTech

- 2.1.7.4 Trend Analysis

- 2.1.8 FoodTech

- 2.1.8.1 Trend Analysis

- 2.1.9 Warehousing

- 2.1.9.1 Trend Analysis

- 2.1.10 HealthTech and MedTech

- 2.1.10.1 Trend Analysis

- 2.1.1 Market Overview

3 Product

- 3.1 U.S. Robotics Integration for the Manufacturing Market (by Type)

- 3.1.1 Market Overview

- 3.1.1.1 Demand Analysis of U.S. Robotics Integration for the Manufacturing Market (by Type), Value and Volume

- 3.1.2 Autonomous Mobile Robots (AMRs)

- 3.1.3 Automated Guided Vehicles (AGVs)

- 3.1.4 Collaborative Robots (Cobots)

- 3.1.5 Other

- 3.1.1 Market Overview

4 Market - Competitive Benchmarking & Company Profiles

- 4.1 Competitive Benchmarking

- 4.2 Company Profiles

- 4.2.1 ACRO Automation Systems, Inc.

- 4.2.1.1 Company Overview

- 4.2.1.1.1 Role of ACRO Automation Systems, Inc. in the U.S. Robotics Integration for the Manufacturing Market

- 4.2.1.2 Analyst View

- 4.2.1.1 Company Overview

- 4.2.2 Andrews Cooper

- 4.2.2.1 Company Overview

- 4.2.2.1.1 Role of Andrews Cooper in the U.S. Robotics Integration for the Manufacturing Market

- 4.2.2.2 Analyst View

- 4.2.2.1 Company Overview

- 4.2.3 Bastian Solutions, LLC

- 4.2.3.1 Company Overview

- 4.2.3.1.1 Role of Bastian Solutions, LLC in the U.S. Robotics Integration for the Manufacturing Market

- 4.2.3.1.2 Product Portfolio

- 4.2.3.2 Business Strategies

- 4.2.3.2.1 Product Developments and Fundings

- 4.2.3.3 Corporate Strategies

- 4.2.3.3.1 Partnerships, Collaborations, Contracts, and Agreements

- 4.2.3.4 Analyst View

- 4.2.3.1 Company Overview

- 4.2.4 Cleveland Automation Systems

- 4.2.4.1 Company Overview

- 4.2.4.1.1 Role of Cleveland Automation Systems in the U.S. Robotics Integration for the Manufacturing Market

- 4.2.4.2 Analyst View

- 4.2.4.1 Company Overview

- 4.2.5 Dynamic Automation

- 4.2.5.1 Company Overview

- 4.2.5.1.1 Role of Dynamic Automation in the U.S. Robotics Integration for the Manufacturing Market

- 4.2.5.2 Analyst View

- 4.2.5.1 Company Overview

- 4.2.6 enVista, LLC.

- 4.2.6.1 Company Overview

- 4.2.6.1.1 Role of enVista, LLC. in the U.S. Robotics Integration for the Manufacturing Market

- 4.2.6.2 Analyst View

- 4.2.6.1 Company Overview

- 4.2.7 KC Robotics

- 4.2.7.1 Company Overview

- 4.2.7.1.1 Role of KC Robotics in the U.S. Robotics Integration for the Manufacturing Market

- 4.2.7.2 Analyst View

- 4.2.7.1 Company Overview

- 4.2.8 Productivity Inc.

- 4.2.8.1 Company Overview

- 4.2.8.1.1 Role of Productivity Inc. in the U.S. Robotics Integration for the Manufacturing Market

- 4.2.8.1.2 Product Portfolio

- 4.2.8.2 Analyst View

- 4.2.8.1 Company Overview

- 4.2.9 Remtec Automation, LLC.

- 4.2.9.1 Company Overview

- 4.2.9.1.1 Role of Remtec Automation, LLC. in the U.S. Robotics Integration for the Manufacturing Market

- 4.2.9.2 Analyst View

- 4.2.9.1 Company Overview

- 4.2.10 Steven Douglas Corp.

- 4.2.10.1 Company Overview

- 4.2.10.1.1 Role of Steven Douglas Corp. in the U.S. Robotics Integration for the Manufacturing Market

- 4.2.10.2 Analyst View

- 4.2.10.1 Company Overview

- 4.2.11 Other Key Market Participants

- 4.2.11.1 Jabil Inc.

- 4.2.11.1.1 Company Overview

- 4.2.11.2 JR Automation

- 4.2.11.2.1 Company Overview

- 4.2.11.1 Jabil Inc.

- 4.2.1 ACRO Automation Systems, Inc.

5 Growth Opportunities and Recommendations

- 5.1 Growth Opportunities

- 5.1.1 Growth Opportunity 1: Growing Demand from Automotive Market

- 5.1.1.1 Recommendation

- 5.1.2 Growth Opportunity 2: Growing Demand for Warehouse Automation

- 5.1.2.1 Recommendation

- 5.1.1 Growth Opportunity 1: Growing Demand from Automotive Market

6 Research Methodology

- 6.1 Factors for Data Prediction and Modeling