|

|

市場調査レポート

商品コード

1097586

次世代オンコロジーデバイス・ソリューションの世界市場 - 分析と予測:臨床応用別、エンドユーザー別、タイプ別、地域別(2022年~2031年)Next-Generation Oncology Devices and Solutions Market - A Global and Regional Analysis: Focus on Clinical Application, End User, Type, and Region - Analysis and Forecast, 2022-2031 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 次世代オンコロジーデバイス・ソリューションの世界市場 - 分析と予測:臨床応用別、エンドユーザー別、タイプ別、地域別(2022年~2031年) |

|

出版日: 2022年06月27日

発行: BIS Research

ページ情報: 英文 177 Pages

納期: 1~5営業日

|

- 全表示

- 概要

- 図表

- 目次

世界の次世代オンコロジーデバイス・ソリューションの市場規模は、2021年の32億6,820万米ドルから、2031年末までに59億7,130万米ドルに達し、2022年~2031年の予測期間中のCAGRで6.41%の成長が予測されています。

市場は、オンコロジーの普及率の増加、オンコロジー向けソフトウェアソリューションに対する需要の増加、オンコロジーの検査・治療における新技術、診断・治療における低侵襲性技術への選好の高まりなどの要因によって牽引されています。

当レポートでは、世界の次世代オンコロジーデバイス・ソリューション市場について調査分析し、市場概要、市場力学、セグメント別の市場分析、主要企業などについて、最新の情報を提供しています。

目次

第1章 市場

- 世界市場の見通し

- 製品定義

- 包含・除外基準

- 主な調査結果

- 前提条件と制限

- 世界市場のシナリオ

- 業界の見通し

- 主な動向

- 機会評価

- 特許分析

- 製品ベンチマーキング

- エンドユーザーの認識

- ケーススタディ

- 次世代オンコロジーデバイス・ソリューション市場に対するCOVID-19の影響

- オンコロジーソリューションの採用への影響

- 市場規模への影響

- 市場参入障壁と機会

- ビジネス力学

- 影響分析

- ビジネス促進要因

- ビジネス抑制要因

- ビジネス機会

第2章 世界の次世代オンコロジーデバイス・ソリューション市場(臨床応用別)

- 機会評価

- 成長シェアマトリックス

- 肺がん

- 前立腺がん

- 乳がん

- その他

第3章 世界の次世代オンコロジーデバイス・ソリューション市場(エンドユーザー別)

- 機会評価

- 成長シェアマトリックス

- 病院

- 画像診断センター

- その他(外来手術センター、がん治療センター、政府機関)

第4章 世界の次世代オンコロジーデバイス・ソリューション市場(タイプ別)

- 市場機会評価

- 成長シェアマトリックス

- デバイス

- 技術別

- アプリケーション別

- ソフトウェア

- アプリケーション別

第5章 地域

- 北米の次世代オンコロジーデバイス・ソリューション市場

- 欧州の次世代オンコロジーデバイス・ソリューション市場

- アジア太平洋の次世代オンコロジーデバイス・ソリューション市場

- その他の地域の次世代オンコロジーデバイス・ソリューション市場

第6章 市場 - 競合ベンチマーキング

- 競合情勢

- 主な戦略と発展

- 市場シェア分析

List of Figures

- Figure 1: Global Next-Generation Oncology Devices and Solutions Market, Impact Analysis

- Figure 2: Global Next-Generation Oncology Devices and Solutions Market (by Region), $Million, 2021 and 2031

- Figure 3: Global Next-Generation Oncology Devices and Solutions Market Segmentation

- Figure 4: Global Next-Generation Oncology Devices and Solutions Market Research Methodology

- Figure 5: Primary Research

- Figure 6: Secondary Research

- Figure 7: Data Triangulation

- Figure 8: Global Next-Generation Oncology Devices and Solutions Market Research Process

- Figure 9: Assumptions and Limitations

- Figure 10: Global Next-Generation Oncology Devices and Solutions Market, Potential Forecast Scenarios

- Figure 11: Global Next-Generation Oncology Devices and Solutions Market Size and Growth Potential (Realistic Scenario), $Million, 2020-2031

- Figure 12: Global Next-Generation Oncology Devices and Solutions Market Size and Growth Potential (Optimistic Scenario), $Million, 2020-2031

- Figure 13: Global Next-Generation Oncology Devices and Solutions Market Size and Growth Potential (Pessimistic/Conservative Scenario), $Million, 2020-2031

- Figure 14: Global Next-Generation Oncology Devices and Solutions Market Key Trends, Short-Term Potential

- Figure 15: Global Next-Generation Oncology Devices and Solutions Market Key Trends, Long-Term Potential

- Figure 16: Global Next-Generation Oncology Devices and Solutions Market, Patent Analysis (by Country), January 2018-April 2022

- Figure 17: Global Next-Generation Oncology Devices and Solutions Market, Patent Analysis (by Year), January 2018-April 2022

- Figure 18: Key Players' Product Offerings (by Type)

- Figure 19: Global Next-Generation Oncology Devices and Solutions Market, Pre-COVID-19 Phase, $Million, 2020-2031

- Figure 20: Global Next-Generation Oncology Devices and Solutions Market, Impact Analysis

- Figure 21: Global Number of New Cases for All Cancers, 2020-2040

- Figure 22: Global Next-Generation Oncology Devices and Solutions Market (by Clinical Application)

- Figure 23: Global Next-Generation Oncology Devices and Solutions Market Incremental Opportunity (by Clinical Application), $Million, 2021-2031

- Figure 24: Global Next-Generation Oncology Devices and Solutions Market, Growth-Share Matrix (by Clinical Application), 2021-2031

- Figure 25: Global Next-Generation Oncology Devices and Solutions Market (Lung Cancer), $Million, 2020-2031

- Figure 26: Global Next-Generation Oncology Devices and Solutions Market (Prostate Cancer), $Million, 2020-2031

- Figure 27: Global Next-Generation Oncology Devices and Solutions Market (Breast Cancer), $Million, 2020-2031

- Figure 28: Global Next-Generation Oncology Devices and Solutions Market (Others), $Million, 2020-2031

- Figure 29: Global Next-Generation Oncology Devices and Solutions Market (by End User)

- Figure 30: Global Next-Generation Oncology Devices and Solutions Market Incremental Opportunity (by End User), $Million, 2021-2031

- Figure 31: Global Next-Generation Oncology Devices and Solutions Market, Growth-Share Matrix (by End User), 2021-2031

- Figure 32: Global Next-Generation Oncology Devices and Solutions Market (Hospitals), $Million, 2020-2031

- Figure 33: Global Next-Generation Oncology Devices and Solutions Market (Diagnostic Imaging Centers), $Million, 2020-2031

- Figure 34: Global Next-Generation Oncology Devices and Solutions Market (Others), $Million, 2020-2031

- Figure 35: Global Next-Generation Oncology Devices and Solutions Market (by Type)

- Figure 36: Global Next-Generation Oncology Devices and Solutions Market Incremental Opportunity (by Type), $Million, 2021-2031

- Figure 37: Global Next-Generation Oncology Devices and Solutions Market, Growth-Share Matrix (by Type), 2021-2031

- Figure 38: Global Next-Generation Oncology Devices and Solutions Market (High-Intensity Focused Ultrasound), $Million, 2020-2031

- Figure 39: Global Next-Generation Oncology Devices and Solutions Market (Advanced Forms of Radiation Therapy), $Million, 2020-2031

- Figure 40: Global Next-Generation Oncology Devices and Solutions Market (Others), $Million, 2020-2031

- Figure 41: Global Next-Generation Oncology Devices and Solutions Market, Devices (Diagnosis), $Million, 2020-2031

- Figure 42: Global Next-Generation Oncology Devices and Solutions Market, Devices (Treatment and Monitoring), $Million, 2020-2031

- Figure 43: Global Next-Generation Oncology Devices and Solutions Market, Software (Diagnosis), $Million, 2020-2031

- Figure 44: Global Next-Generation Oncology Devices and Solutions Market, Software (Treatment and Monitoring), $Million, 2020-2031

- Figure 45: Global Next-Generation Oncology Devices and Solutions Market Share (by Region), 2021-2031

- Figure 46: North America Next-Generation Oncology Devices and Solutions Market Incremental Opportunity (by Country), $Million, 2021-2031

- Figure 47: Prevalence of Different Cancer in North America, 2010, 2015, and 2019

- Figure 48: Number of New Cases for All Cancers in North America, 2020-2040

- Figure 49: North America Next-Generation Oncology Devices and Solutions Market, $Million, 2020-2031

- Figure 50: North America Next-Generation Oncology Devices and Solutions Market (by Clinical Application), $Million, 2020-2031

- Figure 51: North America Next-Generation Oncology Devices and Solutions Market (by End User), $Million, 2020-2031

- Figure 52: North America Next-Generation Oncology Devices and Solutions Market (by Type), $Million, 2020-2031

- Figure 53: North America Next-Generation Oncology Devices and Solutions Market, Devices (by Technology), $Million, 2020-2031

- Figure 54: North America Next-Generation Oncology Devices and Solutions Market, Devices (by Application), $Million, 2020-2031

- Figure 55: North America Next-Generation Oncology Devices and Solutions Market, Software (by Application), $Million, 2020-2031

- Figure 56: North America Next-Generation Oncology Devices and Solutions Market (by Country), $Million, 2021 and 2031

- Figure 57: U.S. Next-Generation Oncology Devices and Solutions Market, $Million, 2020-2031

- Figure 58: U.S. Next-Generation Oncology Devices and Solutions Market (by Clinical Application), $Million, 2020-2031

- Figure 59: U.S. Next-Generation Oncology Devices and Solutions Market (by End User), $Million, 2020-2031

- Figure 60: Canada Next-Generation Oncology Devices and Solutions Market, $Million, 2020-2031

- Figure 61: Canada Next-Generation Oncology Devices and Solutions Market (by Clinical Application), $Million, 2020-2031

- Figure 62: Canada Next-Generation Oncology Devices and Solutions Market (by End User), $Million, 2020-2031

- Figure 63: Europe Next-Generation Oncology Devices and Solutions Market Incremental Opportunity (by Country), $Million, 2021-2031

- Figure 64: Number of New Cases for All Cancers in Europe, 2020-2040

- Figure 65: Europe Next-Generation Oncology Devices and Solutions Market, $Million, 2020-2031

- Figure 66: Europe Next-Generation Oncology Devices and Solutions Market (by Clinical Application), $Million, 2020-2031

- Figure 67: Europe Next-Generation Oncology Devices and Solutions Market (by End User), $Million, 2020-2031

- Figure 68: Europe Next-Generation Oncology Devices and Solutions Market (by Type), $Million, 2020-2031

- Figure 69: Europe Next-Generation Oncology Devices and Solutions Market, Devices (by Technology), $Million, 2020-2031

- Figure 70: Europe Next-Generation Oncology Devices and Solutions Market, Devices (by Application), $Million, 2020-2031

- Figure 71: Europe Next-Generation Oncology Devices and Solutions Market, Software (by Application), $Million, 2020-2031

- Figure 72: Europe Next-Generation Oncology Devices and Solutions Market (by Country), $Million, 2021 and 2031

- Figure 73: Germany Next-Generation Oncology Devices and Solutions Market, $Million, 2020-2031

- Figure 74: Germany Next-Generation Oncology Devices and Solutions Market (by Clinical Application), $Million, 2020-2031

- Figure 75: Germany Next-Generation Oncology Devices and Solutions Market (by End User), $Million, 2020-2031

- Figure 76: U.K. Next-Generation Oncology Devices and Solutions Market, $Million, 2020-2031

- Figure 77: U.K. Next-Generation Oncology Devices and Solutions Market (by Clinical Application), $Million, 2020-2031

- Figure 78: U.K. Next-Generation Oncology Devices and Solutions Market (by End User), $Million, 2020-2031

- Figure 79: France Next-Generation Oncology Devices and Solutions Market, $Million, 2020-2031

- Figure 80: France Next-Generation Oncology Devices and Solutions Market (by Clinical Application), $Million, 2020-2031

- Figure 81: France Next-Generation Oncology Devices and Solutions Market (by End User), $Million, 2020-2031

- Figure 82: Italy Next-Generation Oncology Devices and Solutions Market, $Million, 2020-2031

- Figure 83: Italy Next-Generation Oncology Devices and Solutions Market (by Clinical Application), $Million, 2020-2031

- Figure 84: Italy Next-Generation Oncology Devices and Solutions Market (by End User), $Million, 2020-2031

- Figure 85: Spain Next-Generation Oncology Devices and Solutions Market, $Million, 2020-2031

- Figure 86: Spain Next-Generation Oncology Devices and Solutions Market (by Clinical Application), $Million, 2020-2031

- Figure 87: Spain Next-Generation Oncology Devices and Solutions Market (by End User), $Million, 2020-2031

- Figure 88: Rest-of-Europe Next-Generation Oncology Devices and Solutions Market, $Million, 2020-2031

- Figure 89: Rest-of-Europe Next-Generation Oncology Devices and Solutions Market (by Clinical Application), $Million, 2020-2031

- Figure 90: Rest-of-Europe Next-Generation Oncology Devices and Solutions Market (by End User), $Million, 2020-2031

- Figure 91: Asia-Pacific Next-Generation Oncology Devices and Solutions Market Incremental Opportunity (by Country), $Million, 2021-2031

- Figure 92: Prevalence of Different Cancer in Asia-Pacific, 2010, 2015, and 2019

- Figure 93: Number of New Cases for All Cancers in Asia-Pacific, 2020-2040

- Figure 94: Asia-Pacific Next-Generation Oncology Devices and Solutions Market, $Million, 2020-2031

- Figure 95: Asia-Pacific Next-Generation Oncology Devices and Solutions Market (by Clinical Application), $Million, 2020-2031

- Figure 96: Asia-Pacific Next-Generation Oncology Devices and Solutions Market (by End User), $Million, 2020-2031

- Figure 97: Asia-Pacific Next-Generation Oncology Devices and Solutions Market (by Type), $Million, 2020-2031

- Figure 98: Asia-Pacific Next-Generation Oncology Devices and Solutions Market, Devices (by Technology), $Million, 2020-2031

- Figure 99: Asia-Pacific Next-Generation Oncology Devices and Solutions Market, Devices (by Application), $Million, 2020-2031

- Figure 100: Asia-Pacific Next-Generation Oncology Devices and Solutions Market, Software (by Application), $Million, 2020-2031

- Figure 101: Asia-Pacific Next-Generation Oncology Devices and Solutions Market (by Country), $Million, 2021 and 2031

- Figure 102: Japan Next-Generation Oncology Devices and Solutions Market, $Million, 2020-2031

- Figure 103: Japan Next-Generation Oncology Devices and Solutions Market (by Clinical Application), $Million, 2020-2031

- Figure 104: Japan Next-Generation Oncology Devices and Solutions Market (by End User), $Million, 2020-2031

- Figure 105: China Next-Generation Oncology Devices and Solutions Market, $Million, 2020-2031

- Figure 106: China Next-Generation Oncology Devices and Solutions Market (by Clinical Application), $Million, 2020-2031

- Figure 107: China Next-Generation Oncology Devices and Solutions Market (by End User), $Million, 2020-2031

- Figure 108: Australia Next-Generation Oncology Devices and Solutions Market, $Million, 2020-2031

- Figure 109: Australia Next-Generation Oncology Devices and Solutions Market (by Clinical Application), $Million, 2020-2031

- Figure 110: Australia Next-Generation Oncology Devices and Solutions Market (by End User), $Million, 2020-2031

- Figure 111: India Next-Generation Oncology Devices and Solutions Market, $Million, 2020-2031

- Figure 112: India Next-Generation Oncology Devices and Solutions Market (by Clinical Application), $Million, 2020-2031

- Figure 113: India Next-Generation Oncology Devices and Solutions Market (by End User), $Million, 2020-2031

- Figure 114: South Korea Next-Generation Oncology Devices and Solutions Market, $Million, 2020-2031

- Figure 115: South Korea Next-Generation Oncology Devices and Solutions Market (by Clinical Application), $Million, 2020-2031

- Figure 116: South Korea Next-Generation Oncology Devices and Solutions Market (by End User), $Million, 2020-2031

- Figure 117: Rest-of-Asia-Pacific Next-Generation Oncology Devices and Solutions Market, $Million, 2020-2031

- Figure 118: Rest-of-Asia-Pacific Next-Generation Oncology Devices and Solutions Market (by Clinical Application), $Million, 2020-2031

- Figure 119: Rest-of-Asia-Pacific Next-Generation Oncology Devices and Solutions Market (by End User), $Million, 2020-2031

- Figure 120: Rest-of-the-World Next-Generation Oncology Devices and Solutions Market Incremental Opportunity (by Country), $Million, 2021-2031

- Figure 121: Number of New Cases for All Cancers in Africa and Latin America, 2020-2040

- Figure 122: Rest-of-the-World Next-Generation Oncology Devices and Solutions Market, $Million, 2020-2031

- Figure 123: Rest-of-the-World Next-Generation Oncology Devices and Solutions Market (by Clinical Application), $Million, 2020-2031

- Figure 124: Rest-of-the-World Next-Generation Oncology Devices and Solutions Market (by End User), $Million, 2020-2031

- Figure 125: Rest-of-the-World Next-Generation Oncology Devices and Solutions Market (by Type), $Million, 2020-2031

- Figure 126: Rest-of-the-World Next-Generation Oncology Devices and Solutions Market, Devices (by Technology), $Million, 2020-2031

- Figure 127: Rest-of-the-World Next-Generation Oncology Devices and Solutions Market, Devices (by Application), $Million, 2020-2031

- Figure 128: Rest-of-the-World Next-Generation Oncology Devices and Solutions Market, Software (by Application), $Million, 2020-2031

- Figure 129: Rest-of-the-World Next-Generation Oncology Devices and Solutions Market (by Country), $Million, 2021 and 2031

- Figure 130: K.S.A. Next-Generation Oncology Devices and Solutions Market, $Million, 2020-2031

- Figure 131: K.S.A. Next-Generation Oncology Devices and Solutions Market (by Clinical Application), $Million, 2020-2031

- Figure 132: K.S.A. Next-Generation Oncology Devices and Solutions Market (by End User), $Million, 2020-2031

- Figure 133: Brazil Next-Generation Oncology Devices and Solutions Market, $Million, 2020-2031

- Figure 134: Brazil Next-Generation Oncology Devices and Solutions Market (by Clinical Application), $Million, 2020-2031

- Figure 135: Brazil Next-Generation Oncology Devices and Solutions Market (by End User), $Million, 2020-2031

- Figure 136: U.A.E. Next-Generation Oncology Devices and Solutions Market, $Million, 2020-2031

- Figure 137: U.A.E. Next-Generation Oncology Devices and Solutions Market (by Clinical Application), $Million, 2020-2031

- Figure 138: U.A.E. Next-Generation Oncology Devices and Solutions Market (by End User), $Million, 2020-2031

- Figure 139: Mexico Next-Generation Oncology Devices and Solutions Market, $Million, 2020-2031

- Figure 140: Mexico Next-Generation Oncology Devices and Solutions Market (by Clinical Application), $Million, 2020-2031

- Figure 141: Mexico Next-Generation Oncology Devices and Solutions Market (by End User), $Million, 2020-2031

- Figure 142: Rest-of-Rest-of-the-World Next-Generation Oncology Devices and Solutions Market, $Million, 2020-2031

- Figure 143: Rest-of-Rest-of-the-World Next-Generation Oncology Devices and Solutions Market (by Clinical Application), $Million, 2020-2031

- Figure 144: Rest-of-Rest-of-the-World Next-Generation Oncology Devices and Solutions Market (by End User), $Million, 2020-2031

- Figure 145: Share of Key Developments and Strategies, January 2018-April 2022

- Figure 146: Regulatory and Legal Activities (by Company), January 2018-April 2022

- Figure 147: Partnerships, Alliances, and Business Expansions (by Company), January 2018-April 2022

- Figure 148: New Offerings (by Company), January 2018-April 2022

- Figure 149: Mergers and Acquisitions (by Company), January 2018-April 2022

- Figure 150: Funding Activities (by Company), January 2018-April 2022

- Figure 151: Global Next-Generation Oncology Devices and Solutions Market, Company Revenue Share Analysis, $Million, 2021

List of Tables

- Table 1: Global Next-Generation Oncology Devices and Solutions Market, Quarterly Key Developments Analysis, January 2018-April 2022

- Table 2: Global Next-Generation Oncology Devices and Solutions Market, Key Entry Barriers and Possible Solutions

- Table 3: Key Software Solutions in Oncology

- Table 4: Key Technologies and Products in Oncology for Diagnosis and Treatment

- Table 5: Key Players Offering HIFU Devices for Cancer

- Table 6: Key Products Based on IGRT and IMRT Technology

- Table 7: Key Players Offering Next-Generation Oncology Devices for Diagnosis

- Table 8: Key Players Offering Next-Generation Oncology Devices for Treatment and Monitoring of Cancer

- Table 9: Key Players Offering Next-Generation Oncology Software for Diagnosis

- Table 10: Key Players Offering Next-Generation Oncology Software for Treatment and Monitoring

- Table 11: North America Next-Generation Oncology Devices and Solutions Market Regulatory Framework

- Table 12: U.S. Next-Generation Oncology Devices and Solutions Market, Key Players and Product Offering

- Table 13: North America Next-Generation Oncology Devices and Solutions Market Dynamics Impact Analysis

- Table 14: Key Players in France Next-Generation Oncology Devices and Software Market

- Table 15: Key Players in Rest-of-Europe Next-Generation Oncology Devices and Solutions Market

- Table 16: Europe Next-Generation Oncology Devices and Solutions Market Dynamics Impact Analysis

- Table 17: Asia-Pacific Next-Generation Oncology Devices and Solutions Market Regulatory Framework

- Table 18: Asia-Pacific Next-Generation Oncology Devices and Solutions Market Dynamics Impact Analysis

- Table 19: Rest-of-the-World Next-Generation Oncology Devices and Solutions Market Regulatory Framework

- Table 20: Rest-of-the-World Next-Generation Oncology Devices and Solutions Market Dynamics Impact Analysis

“Global Next-Generation Oncology Devices and Solutions Market to Reach $5,971.3 Million by 2031.”

Industry Overview

The global next-generation oncology devices and solutions market report highlights that the market was valued at $3,268.2 million in 2021 and is expected to reach $5,971.3 million by the end of 2031. The market is expected to grow at a CAGR of 6.41% during the forecast period from 2022 to 2031. The market is driven by factors such as the increasing prevalence of oncology, increasing demand for software solutions in oncology, emerging technologies in oncology testing and treatment, and rising preference for minimally invasive techniques of diagnosis and treatment.

Market Lifecycle Stage

The next-generation oncology devices and solutions market is still in the development phase. Increased research and development activities are underway to develop more products.

The opportunity for growth of the next-generation oncology devices and solutions market lies in the increasing demand for home-based cancer testing and the growing demand for targeted therapy.

Impact of COVID-19

The pandemic led to the deferral of cancer diagnosis by patients owing to factors such as the risk of virus transmission and higher priority given to the management of COVID-19 cases. Before the COVID-19 pandemic, cancer screening and treatment were majorly undertaken in hospitals and clinical facilities. The emphasis on home-based oncology care was still in its nascent stage. The pandemic led to a deferral of screening and treatment for various types of cancers. Owing to factors such as travel restrictions and risk of transmission of the virus, there was an increased demand for home-based care during the pandemic. While teleconsultations witnessed a drastic increase throughout the healthcare industry, there was also increased demand for home-based tests for screening and monitoring cancerous disorders. Software solutions for oncology also witnessed higher demand as a result of the pandemic.

As the recovery phase of the COVID-19 pandemic begins, cancer diagnosis and treatment procedures are expected to normalize. The shift in preference to home-based care is expected to continue even after the pandemic subsides.

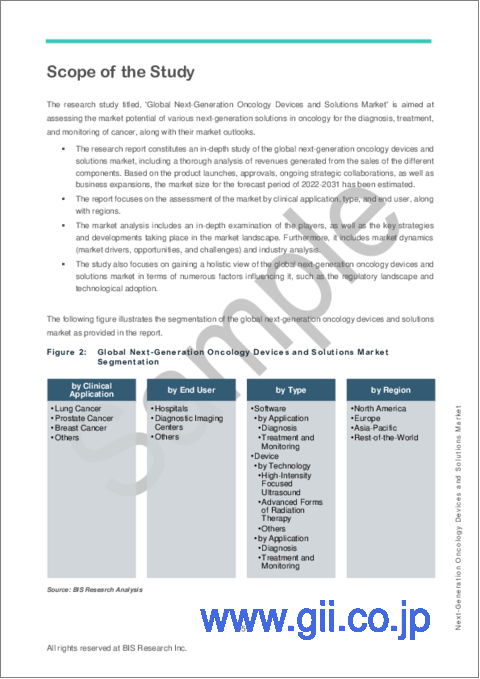

Market Segmentation:

Segmentation 1: by Clinical Application

- Lung Cancer

- Prostate Cancer

- Breast Cancer

- Others

The global next-generation oncology devices and solutions market in the clinical application segment is expected to be dominated by the breast cancer and the others segment.

Segmentation 2: by Type

- Devices

By Technology

- High-Intensity Focused Ultrasound

- Advanced Forms of Radiation Therapy

- Others

By Application

- Diagnosis

- Treatment and Monitoring

- Software

By Application

- Diagnosis

- Treatment and Monitoring

Segmentation 3: by End User

- Hospitals

- Diagnostic Imaging Centers

- Others

The global next-generation oncology devices and solutions in the end user segment is dominated by the hospital segment.

Segmentation 4: by Region

- North America - U.S., Canada

- Europe - Germany, France, U.K., Italy, Spain, Rest-of-Europe

- Asia-Pacific - Japan, China, India, Australia, South Korea, Rest-of-Asia-Pacific

- Rest-of-the-World - Kingdom of Saudi Arabia (K.S.A.), Brazil, U.A.E., Mexico, and Rest-of-Rest-of-the-World

Recent Developments in the Global Next-Generation Oncology Devices and Solutions Market

- In May 2022, Varian Medical Systems and HP partnered with Adaptiiv for supporting cancer treatment.

- In April 2022, Brainlab's patient monitoring and positioning system secured CE Mark.

- In April 2022, GE Healthcare and Elekta entered into partnership to expand the access of precision radiation therapy solutions.

- In March 2022, Paige AI Inc. launched its latest product, Paige Breast Lymph Node.

- In March 2022, Paige AI Inc. launched its pathology AI for detecting breast cancer metastases in lymph nodes.

- In February 2022, Paige and Mindpeak announced partnership to expand the access of industry - leading AI software for breast cancer.

- In January 2022, Oulu University Hospital partnered with Varian and Siemens Healthcare to build a comprehensive ecosystem addressing cancer treatment pathway.

- In December 2021, UofL Health entered into collaboration with Paige AI Inc. to deploy cancer detection software suite of Paige AI Inc.

- In November 2021, Hologic received CE mark for Genius cervical cancer software.

Demand - Drivers and Limitations

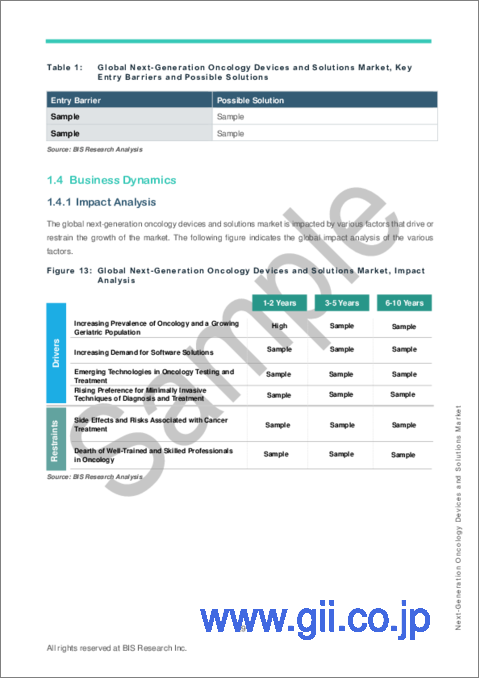

Following are the drivers for the next-generation oncology devices and solutions market:

- Increasing Prevalence of Oncology and a Growing Geriatric Population

- Increase in Demand for Software Solutions in Oncology

- Emerging Technologies in Oncology Testing and Treatment

- Rising Preference for Minimally Invasive Techniques of Diagnosis and Treatment

The market is expected to face some limitations too due to the following challenges:

- Side Effects and Risks Associated with Cancer Treatment

- Dearth of Well-Trained and Skilled Professionals in Oncology

How Can This Report Add Value to an Organization?

- Type: The 'type' segment helps the reader understand the different types of next-generation oncology devices and solutions available in the market. Moreover, the study provides the reader a detailed understanding of the different devices and solutions by clinical application (lung cancer, prostate cancer, breast cancer, and others). Furthermore, the study also covers different segments of type ((Device (Technology (High-Intensity Focused Ultrasound, Advanced Forms of Radiation Therapy, and Others), Application (Diagnosis and Treatment and Monitoring)), Software (Application (Diagnosis and Treatment and Monitoring))).

- Growth/Marketing Strategy: The global next-generation oncology devices and solutions market has seen major development by key players operating in the market, such as business expansion, partnership, collaboration, and joint venture. The favored strategy for the companies has been regulatory and legal activities, partnerships, alliances, and business expansions to strengthen their position in the market. For instance, In April 2022, Brainlab's patient monitoring and positioning system secured CE mark. In May 2022, Varian Medical Systems (a subsidiary of Siemens AG) and HP entered into a partnership with Adaptiiv to support cancer treatment.

Table of Contents

1 Markets

- 1.1 Global Market Outlook

- 1.1.1 Product Definition

- 1.1.2 Inclusion and Exclusion Criteria

- 1.1.3 Key Findings

- 1.1.4 Assumptions and Limitations

- 1.1.5 Global Market Scenario

- 1.1.5.1 Realistic Growth Scenario

- 1.1.5.2 Optimistic Growth Scenario

- 1.1.5.3 Pessimistic/Conservative Growth Scenario

- 1.2 Industry Outlook

- 1.2.1 Key Trends

- 1.2.1.1 Emerging Use of Wearables

- 1.2.1.2 Growing Demand for Point-of-Care Testing (POCT) in Oncology

- 1.2.1.3 Growing Popularity of Smartphone-Based Diagnostics

- 1.2.1.4 Growing Demand for Minimally Invasive Methods of Cancer Diagnosis

- 1.2.1.5 Rising Number of Partnerships and Regulatory Milestones

- 1.2.2 Opportunity Assessment

- 1.2.2.1 Short-Term Potential

- 1.2.2.2 Long-Term Potential

- 1.2.3 Patent Analysis

- 1.2.3.1 Awaited Technological Developments

- 1.2.3.2 Patent Filing Trend (by Country)

- 1.2.3.3 Patent Filing Trend (by Year)

- 1.2.4 Product Benchmarking

- 1.2.5 End-User Perceptions

- 1.2.6 Case Studies

- 1.2.6.1 Stereotactic Body Radiation Therapy (SBRT) using TrueBeam for Inoperable Early-Stage Non-Small Cell Lung Cancer (NSCLC)

- 1.2.6.2 Breast Cancer Treatment Using Halcyon

- 1.2.1 Key Trends

- 1.3 Impact of COVID-19 on the Next-Generation Oncology Devices and Solutions Market

- 1.3.1 Impact on Adoption of Oncology Solutions

- 1.3.2 Impact on Market Size

- 1.3.2.1 Pre-COVID-19 Phase

- 1.3.2.2 During COVID-19 Phase

- 1.3.2.3 Post-COVID-19 Phase

- 1.3.3 Market Entry Barriers and Opportunities

- 1.4 Business Dynamics

- 1.4.1 Impact Analysis

- 1.4.2 Business Drivers

- 1.4.2.1 Increasing Prevalence of Oncology and a Growing Geriatric Population

- 1.4.2.2 Increase in Demand for Software Solutions in Oncology

- 1.4.2.3 Emerging Technologies in Oncology Testing and Treatment

- 1.4.2.4 Rising Preference for Minimally Invasive Techniques of Diagnosis and Treatment

- 1.4.3 Business Restraints

- 1.4.3.1 Side Effects and Risks Associated with Cancer Treatment

- 1.4.3.2 Dearth of Well-Trained and Skilled Professionals in Oncology

- 1.4.4 Business Opportunities

- 1.4.4.1 Increasing Demand for Home-Based Cancer Testing

- 1.4.4.2 Growing Demand for Targeted Therapy

2 Global Next-Generation Oncology Devices and Solutions Market, (by Clinical Application)

- 2.1 Opportunity Assessment

- 2.2 Growth-Share Matrix

- 2.3 Lung Cancer

- 2.4 Prostate Cancer

- 2.5 Breast Cancer

- 2.6 Others

3 Global Next-Generation Oncology Devices and Solutions Market (by End User)

- 3.1 Opportunity Assessment

- 3.2 Growth-Share Matrix

- 3.3 Hospitals

- 3.4 Diagnostic Imaging Centers

- 3.5 Others (Ambulatory Surgical Centers, Cancer Care Centers, and Government Institutions)

4 Global Next-Generation Oncology Devices and Solutions Market (by Type)

- 4.1 Opportunity Assessment

- 4.2 Growth-Share Matrix

- 4.3 Devices

- 4.3.1 By Technology

- 4.3.1.1 High-Intensity Focused Ultrasound

- 4.3.1.2 Advanced Forms of Radiation Therapy

- 4.3.1.3 Others

- 4.3.2 By Application

- 4.3.2.1 Diagnosis

- 4.3.2.2 Treatment and Monitoring

- 4.3.1 By Technology

- 4.4 Software

- 4.4.1 By Application

- 4.4.1.1 Diagnosis

- 4.4.1.2 Treatment and Monitoring

- 4.4.1 By Application

5 Region

- 5.1 North America Next-Generation Oncology Devices and Solutions Market

- 5.1.1 Key Findings and Opportunity Assessment

- 5.1.2 Regulatory Framework

- 5.1.3 Key Players in North America

- 5.1.4 Market Dynamics

- 5.1.4.1 Impact Analysis

- 5.1.5 Sizing and Forecast Analysis

- 5.1.5.1 North America Next-Generation Oncology Devices and Solutions Market (by Clinical Application)

- 5.1.5.2 North America Next-Generation Oncology Devices and Solutions Market (by End User)

- 5.1.5.3 North America Next-Generation Oncology Devices and Solutions Market (by Type)

- 5.1.5.3.1 North America Next-Generation Oncology Devices and Solutions Market, Devices (by Technology)

- 5.1.5.3.2 North America Next-Generation Oncology Devices and Solutions Market, Device (by Application)

- 5.1.5.3.3 North America Next-Generation Oncology Devices and Solutions Market, Software (by Application)

- 5.1.5.4 North America Next-Generation Oncology Devices and Solutions Market (by Country)

- 5.1.5.4.1 U.S.

- 5.1.5.4.1.1 Market Dynamics

- 5.1.5.4.1.2 Sizing and Forecast Analysis

- 5.1.5.4.1.3 U.S. Next-Generation Oncology Devices and Solutions Market (by Clinical Application)

- 5.1.5.4.1.4 U.S. Next-Generation Oncology Devices and Solutions Market (by End User)

- 5.1.5.4.2 Canada

- 5.1.5.4.2.1 Market Dynamics

- 5.1.5.4.2.2 Sizing and Forecast Analysis

- 5.1.5.4.2.3 Canada Next-Generation Oncology Devices and Solutions Market (by Clinical Application)

- 5.1.5.4.2.4 Canada Next-Generation Oncology Devices and Solutions Market (by End User)

- 5.1.5.4.1 U.S.

- 5.2 Europe Next-Generation Oncology Devices and Solutions Market

- 5.2.1 Key Findings and Opportunity Assessment

- 5.2.2 Regulatory Framework

- 5.2.3 Key Players in Europe

- 5.2.4 Market Dynamics

- 5.2.4.1 Impact Analysis

- 5.2.5 Sizing and Forecast Analysis

- 5.2.5.1 Europe Next-Generation Oncology Devices and Solutions Market (by Clinical Application)

- 5.2.5.2 Europe Next-Generation Oncology Devices and Solutions Market (by End User)

- 5.2.5.3 Europe Next-Generation Oncology Devices and Solutions Market (by Type)

- 5.2.5.3.1 Europe Next-Generation Oncology Devices and Solutions Market, Devices (by Technology)

- 5.2.5.3.2 Europe Next-Generation Oncology Devices and Solutions Market, Device (by Application)

- 5.2.5.3.3 Europe Next-Generation Oncology Devices and Solutions Market, Software (by Application)

- 5.2.5.4 Europe Next-Generation Oncology Devices and Solutions Market (by Country)

- 5.2.5.4.1 Germany

- 5.2.5.4.1.1 Market Dynamics

- 5.2.5.4.1.2 Sizing and Forecast Analysis

- 5.2.5.4.1.2.1 Germany Next-Generation Oncology Devices and Solutions Market (by Clinical Application)

- 5.2.5.4.1.2.2 Germany Next-Generation Oncology Devices and Solutions Market (by End User)

- 5.2.5.4.2 U.K.

- 5.2.5.4.2.1 Market Dynamics

- 5.2.5.4.2.2 Sizing and Forecast Analysis

- 5.2.5.4.2.2.1 U.K. Next-Generation Oncology Devices and Solutions Market (by Clinical Application)

- 5.2.5.4.2.2.2 U.K. Next-Generation Oncology Devices and Solutions Market (by End User)

- 5.2.5.4.3 France

- 5.2.5.4.3.1 Market Dynamics

- 5.2.5.4.3.2 Sizing and Forecast Analysis

- 5.2.5.4.3.2.1 France Next-Generation Oncology Devices and Solutions Market (by Clinical Application)

- 5.2.5.4.3.2.2 France Next-Generation Oncology Devices and Solutions Market (by End User)

- 5.2.5.4.4 Italy

- 5.2.5.4.4.1 Market Dynamics

- 5.2.5.4.4.2 Sizing and Forecast Analysis

- 5.2.5.4.4.2.1 Italy Next-Generation Oncology Devices and Solutions Market (by Clinical Application)

- 5.2.5.4.4.2.2 Italy Next-Generation Oncology Devices and Solutions Market (by End User)

- 5.2.5.4.5 Spain

- 5.2.5.4.5.1 Market Dynamics

- 5.2.5.4.5.2 Sizing and Forecast Analysis

- 5.2.5.4.5.2.1 Spain Next-Generation Oncology Devices and Solutions Market (by Clinical Application)

- 5.2.5.4.5.2.2 Spain Next-Generation Oncology Devices and Solutions Market (by End User)

- 5.2.5.4.6 Rest-of-Europe

- 5.2.5.4.6.1 Market Dynamics

- 5.2.5.4.6.2 Sizing and Forecast Analysis

- 5.2.5.4.6.2.1 Rest-of-Europe Next-Generation Oncology Devices and Solutions Market (by Clinical Application)

- 5.2.5.4.6.2.2 Rest-of-Europe Next-Generation Oncology Devices and Solutions Market (by End User)

- 5.2.5.4.1 Germany

- 5.3 Asia-Pacific Next-Generation Oncology Devices and Solutions Market

- 5.3.1 Key Findings and Opportunity Assessment

- 5.3.2 Regulatory Framework

- 5.3.3 Key Players in Asia-Pacific

- 5.3.4 Market Dynamics

- 5.3.4.1 Impact Analysis

- 5.3.5 Sizing and Forecast Analysis

- 5.3.5.1 Asia-Pacific Next-Generation Oncology Devices and Solutions Market (by Clinical Application)

- 5.3.5.2 Asia-Pacific Next-Generation Oncology Devices and Solutions Market (by End User)

- 5.3.5.3 Asia-Pacific Next-Generation Oncology Devices and Solutions Market (by Type)

- 5.3.5.3.1 Asia-Pacific Next-Generation Oncology Devices and Solutions Market, Devices (by Technology)

- 5.3.5.3.2 Asia-Pacific Next-Generation Oncology Devices and Solutions Market, Device (by Application)

- 5.3.5.3.3 Asia-Pacific Next-Generation Oncology Devices and Solutions Market, Software (by Application)

- 5.3.5.4 Asia-Pacific Next-Generation Oncology Devices and Solutions Market (by Country)

- 5.3.5.4.1 Japan

- 5.3.5.4.1.1 Market Dynamics

- 5.3.5.4.1.2 Sizing and Forecast Analysis

- 5.3.5.4.1.2.1 Japan Next-Generation Oncology Devices and Solutions Market (by Clinical Application)

- 5.3.5.4.1.2.2 Japan Next-Generation Oncology Devices and Solutions Market (by End User)

- 5.3.5.4.2 China

- 5.3.5.4.2.1 Market Dynamics

- 5.3.5.4.2.2 Sizing and Forecast Analysis

- 5.3.5.4.2.2.1 China Next-Generation Oncology Devices and Solutions Market (by Clinical Application)

- 5.3.5.4.2.2.2 China Next-Generation Oncology Devices and Solutions Market (by End User)

- 5.3.5.4.3 Australia

- 5.3.5.4.3.1 Market Dynamics

- 5.3.5.4.3.2 Sizing and Forecast Analysis

- 5.3.5.4.3.2.1 Australia Next-Generation Oncology Devices and Solutions Market (by Clinical Application)

- 5.3.5.4.3.2.2 Australia Next-Generation Oncology Devices and Solutions Market (by End User)

- 5.3.5.4.4 India

- 5.3.5.4.4.1 Market Dynamics

- 5.3.5.4.4.2 Sizing and Forecast Analysis

- 5.3.5.4.4.2.1 India Next-Generation Oncology Devices and Solutions Market (by Clinical Application)

- 5.3.5.4.4.2.2 India Next-Generation Oncology Devices and Solutions Market (by End User)

- 5.3.5.4.5 South Korea

- 5.3.5.4.5.1 Market Dynamics

- 5.3.5.4.5.2 Sizing and Forecast Analysis

- 5.3.5.4.5.2.1 South Korea Next-Generation Oncology Devices and Solutions Market (by Clinical Application)

- 5.3.5.4.5.2.2 South Korea Next-Generation Oncology Devices and Solutions Market (by End User)

- 5.3.5.4.6 Rest-of-Asia-Pacific

- 5.3.5.4.6.1 Market Dynamics

- 5.3.5.4.6.2 Sizing and Forecast Analysis

- 5.3.5.4.6.2.1 Rest-of-Asia-Pacific Next-Generation Oncology Devices and Solutions Market (by Clinical Application)

- 5.3.5.4.6.2.2 Rest-of-Asia-Pacific Next-Generation Oncology Devices and Solutions Market (by End User)

- 5.3.5.4.1 Japan

- 5.4 Rest-of-the-World Next-Generation Oncology Devices and Solutions Market

- 5.4.1 Key Findings and Opportunity Assessment

- 5.4.2 Regulatory Framework

- 5.4.3 Key Players in Rest-of-the-World

- 5.4.4 Market Dynamics

- 5.4.4.1 Impact Analysis

- 5.4.5 Sizing and Forecast Analysis

- 5.4.5.1 Rest-of-the-World Next-Generation Oncology Devices and Solutions Market (by Clinical Application)

- 5.4.5.2 Rest-of-the-World Next-Generation Oncology Devices and Solutions Market (by End User)

- 5.4.5.3 Rest-of-the-World Next-Generation Oncology Devices and Solutions Market (by Type)

- 5.4.5.3.1 Rest-of-the-World Next-Generation Oncology Devices and Solutions Market, Devices (by Technology)

- 5.4.5.3.2 Rest-of-the-World Next-Generation Oncology Devices and Solutions Market, Device (by Application)

- 5.4.5.3.3 Rest-of-the-World Next-Generation Oncology Devices and Solutions Market, Software (by Application)

- 5.4.5.4 Rest-of-the-World Next-Generation Oncology Devices and Solutions Market (by Country)

- 5.4.5.4.1 Kingdom of Saudi Arabia (K.S.A.)

- 5.4.5.4.1.1 Market Dynamics

- 5.4.5.4.1.2 Sizing and Forecast Analysis

- 5.4.5.4.1.2.1 K.S.A. Next-Generation Oncology Devices and Solutions Market (by Clinical Application)

- 5.4.5.4.1.2.2 K.S.A. Next-Generation Oncology Devices and Solutions Market (by End User)

- 5.4.5.4.2 Brazil

- 5.4.5.4.2.1 Market Dynamics

- 5.4.5.4.2.2 Sizing and Forecast Analysis

- 5.4.5.4.2.2.1 Brazil Next-Generation Oncology Devices and Solutions Market (by Clinical Application)

- 5.4.5.4.2.2.2 Brazil Next-Generation Oncology Devices and Solutions Market (by End User)

- 5.4.5.4.3 U.A.E.

- 5.4.5.4.3.1 Market Dynamics

- 5.4.5.4.3.2 Sizing and Forecast Analysis

- 5.4.5.4.3.2.1 U.A.E. Next-Generation Oncology Devices and Solutions Market (by Clinical Application)

- 5.4.5.4.3.2.2 U.A.E. Next-Generation Oncology Devices and Solutions Market (by End User)

- 5.4.5.4.4 Mexico

- 5.4.5.4.4.1 Market Dynamics

- 5.4.5.4.4.2 Sizing and Forecast Analysis

- 5.4.5.4.4.2.1 Mexico Next-Generation Oncology Devices and Solutions Market (by Clinical Application)

- 5.4.5.4.4.2.2 Mexico Next-Generation Oncology Devices and Solutions Market (by End User)

- 5.4.5.4.5 Rest-of-Rest-of-the-World

- 5.4.5.4.5.1 Market Dynamics

- 5.4.5.4.5.2 Sizing and Forecast Analysis

- 5.4.5.4.5.2.1 Rest-of-Rest-of-the-World Next-Generation Oncology Devices and Solutions Market (by Clinical Application)

- 5.4.5.4.5.2.2 Rest-of-Rest-of-the-World Next-Generation Oncology Devices and Solutions Market (by End User)

- 5.4.5.4.1 Kingdom of Saudi Arabia (K.S.A.)

6 Markets - Competitive Benchmarking

- 6.1 Competitive Landscape

- 6.1.1 Key Strategies and Developments

- 6.1.1.1 Regulatory and Legal Activities

- 6.1.1.2 Partnerships, Alliances, and Business Expansions

- 6.1.1.3 New Offerings

- 6.1.1.4 Mergers and Acquisitions

- 6.1.1.5 Funding Activities

- 6.1.1 Key Strategies and Developments

- 6.2 Market Share Analysis