無人ヘリコプターの世界市場(2026年~2036年)

Global Unmanned Helicopter Market 2026-2036- 発行日

- ページ情報

- 英文 150+ Pages

- 納期

- 3営業日

- 商品コード

- 2009470

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

- 航空宇宙/防衛関連専門 航空宇宙/防衛関連専門を専門とする市場調査会社です。

世界の防衛用無人ヘリコプター市場

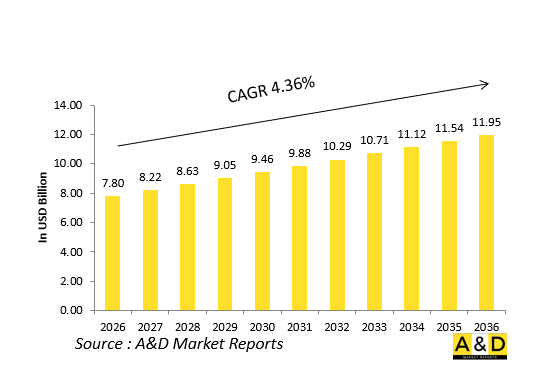

世界の防衛用無人ヘリコプターの市場規模は、2026年に推定78億米ドルであり、2036年までに119億5,000万米ドルに達すると予測され、2026年~2036年の予測期間においてCAGRで4.36%の成長が見込まれています。

イントロダクション

軍隊が作戦の柔軟性を高め、要員へのリスクを低減するために先進の航空システムの採用を進める中、世界の防衛用無人ヘリコプター市場は大きな勢いを得ています。回転翼無人航空システムとしても知られる無人ヘリコプターは、監視、偵察、後方支援、目標捕捉など、幅広い作戦を遂行するように設計されています。これらのプラットフォームは垂直離着陸が可能という利点があり、狭隘で過酷な環境での作戦に適しています。現代の戦争がより動的かつ技術主導的になるにつれて、汎用性が高く信頼性の高い無人ソリューションへの需要が高まっています。防衛機関は、状況認識能力と作戦効率を向上させるため、無人ヘリコプターを作戦体制に統合しています。人命を危険にさらすことなく危険な状況下で運用できる能力も、その採用を後押ししています。防衛の近代化が進む中、無人ヘリコプターは将来の軍事戦略における重要な構成要素として台頭しています。

防衛用無人ヘリコプター市場における技術の影響

技術の進歩は、防衛用無人ヘリコプター市場の形成において極めて重要な役割を果たしています。AIや自律飛行システムにおける革新により、これらのプラットフォームは最小限の人為的介入で複雑な作戦を遂行できるようになっています。衛星測位やセンサーフュージョンを含む先進の航法技術は、多様な環境下での飛行精度と信頼性を向上させています。高解像度イメージングシステムや監視センサーの統合により、情報収集能力も強化されています。推進システムとエネルギー効率の向上により、飛行持続時間が延長され、より長時間の作戦遂行が可能になっています。さらに、通信技術の発達により、無人ヘリコプターと指揮管制センター間のセキュアかつリアルタイムなデータ伝送が可能になっています。軽量材料とモジュール式設計により、積載能力と運用上の柔軟性が高まっています。また、潜在的な脅威からこれらのシステムを保護するため、サイバーセキュリティ対策も強化されています。こうした技術革新が、より高性能で強靭な無人ヘリコプターシステムの進化を促進しています。

防衛用無人ヘリコプター市場の主な市場促進要因

複数の要因が防衛用無人ヘリコプター市場の成長を促進しています。主因の1つは、高リスクな作戦における軍人への危険を低減する必要性の増大です。無人ヘリコプターは、人間の直接的な関与なしに作戦を遂行することで、より安全な代替手段を提供します。リアルタイムの監視・偵察に対する需要の高まりも、市場の拡大に寄与しています。防衛機関は、状況認識と意思決定を強化する効率的で柔軟なソリューションを求めています。さらに、軍事作戦における自動化と無人システムへの移行が採用を加速させています。無人ヘリコプターは従来の有人プラットフォームと比較して運用コストを削減できるため、コスト効率も要因の1つです。地政学的緊張の高まりや、変化し続ける安全保障上の課題も、先進の航空技術への投資をさらに後押ししています。研究開発の継続的な進歩がイノベーションを支え、システムの性能を向上させているため、防衛用途にとっての無人ヘリコプターの魅力はますます高まっています。

防衛用無人ヘリコプター市場の地域的な動向

防衛用無人ヘリコプター市場の地域的な動向は、技術採用の水準や防衛上の優先順位の違いを反映しています。北米は、先進の防衛技術や無人システムへの強力な投資により、依然として支配的な地域となっています。欧州も、近代化構想や共同防衛プログラムにより、着実な成長を示しています。アジア太平洋では、防衛費の増加と安全保障上の懸念の高まりが、無人ヘリコプターへの需要を後押ししています。同地域の国々は能力を強化するために、国内開発と国際パートナーシップの両方に投資しています。

当レポートでは、世界の無人ヘリコプター市場について調査分析し、市場に影響を与える技術、今後10年間の予測、各地域市場の動向などの情報を提供しています。

目次

無人ヘリコプター市場レポートの定義

無人ヘリコプター市場のセグメンテーション

エンドユーザー別

地域別

ペイロード別

今後10年間の無人ヘリコプター市場の分析

無人ヘリコプター市場の技術

世界の無人ヘリコプター市場の予測

地域の無人ヘリコプター市場の動向と予測

北米

促進要因、抑制要因、課題

PEST

市場予測とシナリオ分析

主要企業

サプライヤーのTierの状況

企業ベンチマーク

欧州

中東

アジア太平洋

南米

無人ヘリコプター市場の国の分析

米国

防衛計画

最新ニュース

特許

この市場における現在の技術成熟度

市場予測とシナリオ分析

カナダ

イタリア

フランス

ドイツ

オランダ

ベルギー

スペイン

スウェーデン

ギリシャ

オーストラリア

南アフリカ

インド

中国

ロシア

韓国

日本

マレーシア

シンガポール

ブラジル

無人ヘリコプター市場の機会マトリクス

無人ヘリコプター市場レポートに関する専門家の意見

結論

Aviation and Defense Market Reportsについて

- 発行日

- 発行

- Aviation & Defense Market Reports (A&D)

- ページ情報

- 英文 150+ Pages

- 納期

- 3営業日