|

市場調査レポート

商品コード

1714094

振動試験装置の世界市場:2025-2035年Global Vibration Test Equipment Market 2025-2035 |

||||||

|

|||||||

| 振動試験装置の世界市場:2025-2035年 |

|

出版日: 2025年04月25日

発行: Aviation & Defense Market Reports (A&D)

ページ情報: 英文 150+ Pages

納期: 3営業日

|

全表示

- 概要

- 図表

- 目次

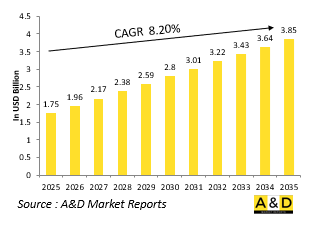

世界の振動試験装置の市場規模は、2025年の17億5,000万米ドルから、予測期間中はCAGR 8.20%で推移し、2035年には38億5,000万米ドルに成長すると予測されています。

振動試験装置市場:イントロダクション

振動試験装置は、防衛産業において極めて重要な役割を果たしています。これはミッションクリティカルなシステムが運用中のストレス条件下でも機械的な堅牢性、構造的完全性、性能の信頼性を維持できるようにするためです。航空機のアビオニクスやミサイル部品、耐環境通信システム、陸上移動車両に至るまで、防衛プラットフォームは展開中に過酷な振動環境にさらされます。防衛分野における振動試験装置市場は、機械工学とミッション保証の交差点に位置しており、現実の状況で遭遇する衝撃・衝突・持続的な振動を再現するシミュレーション機能を提供しています。防衛システムがますます複雑化・小型化し、高精度な許容範囲やマルチドメイン機能を備えるようになる中で、高度な試験インフラの必要性が増しています。振動試験装置は、試作段階での検証から最終製品の認証、運用中のアップグレードに至るまで、製品ライフサイクルのさまざまな段階で使用されます。防衛関連の請負業者、政府系研究所、航空宇宙の試験センターは、MIL-STD-810やNATO STANAGといった国際軍用規格への適合を検証するために、これらの装置に依存しています。市場には、電動振動シェーカー、油圧振動テーブル、多軸システムなど多様な技術が含まれており、これらは高精度な解析のためにデジタルデータ収集システムと統合されることが増えています。防衛分野が迅速なシステム展開やライフサイクル延長戦略へとシフトする中で、振動試験装置は開発リスクの低減や戦闘準備性の確保に不可欠な存在となりつつあります。

振動試験装置市場:技術の影響

技術の進歩は、防衛分野で使用される振動試験装置の機能と性能指標を再定義しています。最新のシステムは現在、高解像度センサ、リアルタイム制御ソフトウェア、機械学習ベースの分析機能を統合し、より正確で適応性の高い試験環境を実現しています。最も革新的なシフトの1つは、デジタルツインテクノロジーの導入です。このテクノロジーでは、部品やシステムの仮想レプリカを振動シナリオのシミュレーションにかけることで、物理的な破壊を伴わずに構造的な脆弱性を特定します。これらのデジタルシミュレーションは、高周波加速度計やひずみゲージで取得した物理的な試験データで検証され、設計を改善し、予知保全モデルを強化するフィードバックループを可能にします。さらに、多軸加振プラットフォームへの移行により、X軸、Y軸、Z軸という異なるベクトルでの同時加振が可能になったため、空中、海上、陸上を問わず、実際の戦場の動きをよりリアルにシミュレーションできるようになりました。また、冷却システムと動的負荷制御の革新により、極限の発射、飛行、輸送条件を再現できる高荷重の電磁加振器の使用も拡大しています。さらに、AIを活用したソフトウェアにより、センサーからのフィードバックに基づいて試験パラメータをリアルタイムで自動調整できるようになり、試験時間の短縮と精度の向上が実現しました。防衛研究開発がより俊敏で開発サイクルを加速する方向に向かう中、技術的に強化された振動試験システムは、ますますダイナミックになる軍事環境において、信頼性保証、構造認証、システム回復力を実現するために不可欠なものとして台頭してきています。

振動試験装置市場の主な促進要因:

いくつかの戦略的・運用的要因が、世界の防衛分野における先進的な振動試験装置の需要を促進しています。その最たるものが、現代の防衛システムの複雑化と性能要求の高まりです。その多くには、コンパクトな電子アセンブリ、高精度の誘導ユニット、モジュール式の構造要素などが含まれ、これらはすべて予測不可能な環境や機械的ストレスに耐えなければなりません。軍がより軽く、より機敏で、電子的に統合されたシステムを追求する中、これらのコンポーネントが振動下でも機能的完全性を維持できるようにすることは、オプションではなく、必須です。特に、各国がレガシー・プラットフォームを段階的に廃止し、新たな試験プロトコルを必要とする次世代車両、ミサイル、航空機に移行しているためです。さらに、極超音速兵器、再利用可能な宇宙システム、無人戦闘機(UCAV)への投資の増加により、高速通過、大気圏再突入、極端な温度変化など、繊細なサブシステムに比類ない機械的ストレスを与える条件を含む新しい振動試験パラメータが導入されています。また、政府との防衛契約では、環境試験規格への準拠がますます厳しくなっており、そのため、高性能で認証可能な振動試験ソリューションの使用が必要となっています。最後に、構造健全性監視と予知保全を通じて資産のライフサイクルを延長することに重点を置く防衛産業の高まりは、重大な故障が発生する前に動作摩耗をシミュレートし、材料疲労を評価できる試験装置に大きく依存しています。これらの要因が相まって、振動試験は日常的な検証プロセスから、防衛システムのエンジニアリングとライフサイクル管理における戦略的な機能へと変化しています。

当レポートでは、世界の振動試験装置の市場を調査し、市場の現況、技術動向、市場影響因子の分析、市場規模の推移・予測、地域別の詳細分析、競合情勢、主要企業のプロファイルなどをまとめています。

目次

世界の振動試験装置市場:目次

世界の振動試験装置市場:レポートの定義

世界の振動試験装置市場:セグメンテーション

地域別

タイプ別

機器タイプ別

用途別

今後10年間の世界の振動試験装置市場の分析

世界の振動試験装置市場:市場技術

世界の振動試験装置市場:予測

世界の振動試験装置市場の動向・予測:地域別

北米

促進要因、制約、課題

抑制要因

市場予測・シナリオ分析

主要企業

サプライヤーティアの情勢

企業ベンチマーキング

欧州

中東

アジア太平洋地域

南米

世界の振動試験装置市場:国別分析

米国

防衛プログラム

最新ニュース

特許

現在の技術成熟度

市場予測・シナリオ分析

カナダ

イタリア

フランス

ドイツ

オランダ

ベルギー

スペイン

スウェーデン

ギリシャ

オーストラリア

南アフリカ

インド

中国

ロシア

韓国

日本

マレーシア

シンガポール

ブラジル

世界の振動試験装置市場:機会マトリックス

世界の振動試験装置市場:レポートに関する専門家の意見

総論

航空・防衛市場レポートについて

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Type, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Application, 2025-2035

- Table 20: Scenario Analysis, Scenario 1, By Equipment Type, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Type, 2025-2035

- Table 23: Scenario Analysis, Scenario 2, By Application, 2025-2035

- Table 24: Scenario Analysis, Scenario 2, By Equipment Type, 2025-2035

List of Figures

- Figure 1: Global Vibration Test Equipment Market Forecast, 2025-2035

- Figure 2: Global Vibration Test Equipment Market Forecast, By Region, 2025-2035

- Figure 3: Global Vibration Test Equipment Market Forecast, By Type, 2025-2035

- Figure 4: Global Vibration Test Equipment Market Forecast, By Application, 2025-2035

- Figure 5: Global Vibration Test Equipment Market Forecast, By Equipment Type, 2025-2035

- Figure 6: North America, Vibration Test Equipment Market, Market Forecast, 2025-2035

- Figure 7: Europe, Vibration Test Equipment Market, Market Forecast, 2025-2035

- Figure 8: Middle East, Vibration Test Equipment Market, Market Forecast, 2025-2035

- Figure 9: APAC, Vibration Test Equipment Market, Market Forecast, 2025-2035

- Figure 10: South America, Vibration Test Equipment Market, Market Forecast, 2025-2035

- Figure 11: United States, Vibration Test Equipment Market, Technology Maturation, 2025-2035

- Figure 12: United States, Vibration Test Equipment Market, Market Forecast, 2025-2035

- Figure 13: Canada, Vibration Test Equipment Market, Technology Maturation, 2025-2035

- Figure 14: Canada, Vibration Test Equipment Market, Market Forecast, 2025-2035

- Figure 15: Italy, Vibration Test Equipment Market, Technology Maturation, 2025-2035

- Figure 16: Italy, Vibration Test Equipment Market, Market Forecast, 2025-2035

- Figure 17: France, Vibration Test Equipment Market, Technology Maturation, 2025-2035

- Figure 18: France, Vibration Test Equipment Market, Market Forecast, 2025-2035

- Figure 19: Germany, Vibration Test Equipment Market, Technology Maturation, 2025-2035

- Figure 20: Germany, Vibration Test Equipment Market, Market Forecast, 2025-2035

- Figure 21: Netherlands, Vibration Test Equipment Market, Technology Maturation, 2025-2035

- Figure 22: Netherlands, Vibration Test Equipment Market, Market Forecast, 2025-2035

- Figure 23: Belgium, Vibration Test Equipment Market, Technology Maturation, 2025-2035

- Figure 24: Belgium, Vibration Test Equipment Market, Market Forecast, 2025-2035

- Figure 25: Spain, Vibration Test Equipment Market, Technology Maturation, 2025-2035

- Figure 26: Spain, Vibration Test Equipment Market, Market Forecast, 2025-2035

- Figure 27: Sweden, Vibration Test Equipment Market, Technology Maturation, 2025-2035

- Figure 28: Sweden, Vibration Test Equipment Market, Market Forecast, 2025-2035

- Figure 29: Brazil, Vibration Test Equipment Market, Technology Maturation, 2025-2035

- Figure 30: Brazil, Vibration Test Equipment Market, Market Forecast, 2025-2035

- Figure 31: Australia, Vibration Test Equipment Market, Technology Maturation, 2025-2035

- Figure 32: Australia, Vibration Test Equipment Market, Market Forecast, 2025-2035

- Figure 33: India, Vibration Test Equipment Market, Technology Maturation, 2025-2035

- Figure 34: India, Vibration Test Equipment Market, Market Forecast, 2025-2035

- Figure 35: China, Vibration Test Equipment Market, Technology Maturation, 2025-2035

- Figure 36: China, Vibration Test Equipment Market, Market Forecast, 2025-2035

- Figure 37: Saudi Arabia, Vibration Test Equipment Market, Technology Maturation, 2025-2035

- Figure 38: Saudi Arabia, Vibration Test Equipment Market, Market Forecast, 2025-2035

- Figure 39: South Korea, Vibration Test Equipment Market, Technology Maturation, 2025-2035

- Figure 40: South Korea, Vibration Test Equipment Market, Market Forecast, 2025-2035

- Figure 41: Japan, Vibration Test Equipment Market, Technology Maturation, 2025-2035

- Figure 42: Japan, Vibration Test Equipment Market, Market Forecast, 2025-2035

- Figure 43: Malaysia, Vibration Test Equipment Market, Technology Maturation, 2025-2035

- Figure 44: Malaysia, Vibration Test Equipment Market, Market Forecast, 2025-2035

- Figure 45: Singapore, Vibration Test Equipment Market, Technology Maturation, 2025-2035

- Figure 46: Singapore, Vibration Test Equipment Market, Market Forecast, 2025-2035

- Figure 47: United Kingdom, Vibration Test Equipment Market, Technology Maturation, 2025-2035

- Figure 48: United Kingdom, Vibration Test Equipment Market, Market Forecast, 2025-2035

- Figure 49: Opportunity Analysis, Vibration Test Equipment Market, By Region (Cumulative Market), 2025-2035

- Figure 50: Opportunity Analysis, Vibration Test Equipment Market, By Region (CAGR), 2025-2035

- Figure 51: Opportunity Analysis, Vibration Test Equipment Market, By Type (Cumulative Market), 2025-2035

- Figure 52: Opportunity Analysis, Vibration Test Equipment Market, By Type (CAGR), 2025-2035

- Figure 53: Opportunity Analysis, Vibration Test Equipment Market, By Application (Cumulative Market), 2025-2035

- Figure 54: Opportunity Analysis, Vibration Test Equipment Market, By Application (CAGR), 2025-2035

- Figure 55: Opportunity Analysis, Vibration Test Equipment Market, By Equipment Type (Cumulative Market), 2025-2035

- Figure 56: Opportunity Analysis, Vibration Test Equipment Market, By Equipment Type (CAGR), 2025-2035

- Figure 57: Scenario Analysis, Vibration Test Equipment Market, Cumulative Market, 2025-2035

- Figure 58: Scenario Analysis, Vibration Test Equipment Market, Global Market, 2025-2035

- Figure 59: Scenario 1, Vibration Test Equipment Market, Total Market, 2025-2035

- Figure 60: Scenario 1, Vibration Test Equipment Market, By Region, 2025-2035

- Figure 61: Scenario 1, Vibration Test Equipment Market, By Type, 2025-2035

- Figure 62: Scenario 1, Vibration Test Equipment Market, By Application, 2025-2035

- Figure 63: Scenario 1, Vibration Test Equipment Market, By Equipment Type, 2025-2035

- Figure 64: Scenario 2, Vibration Test Equipment Market, Total Market, 2025-2035

- Figure 65: Scenario 2, Vibration Test Equipment Market, By Region, 2025-2035

- Figure 66: Scenario 2, Vibration Test Equipment Market, By Type, 2025-2035

- Figure 67: Scenario 2, Vibration Test Equipment Market, By Application, 2025-2035

- Figure 68: Scenario 2, Vibration Test Equipment Market, By Equipment Type, 2025-2035

- Figure 69: Company Benchmark, Vibration Test Equipment Market, 2025-2035

The Global Vibration Test Equipment market is estimated at USD 1.75 billion in 2025, projected to grow to USD 3.85 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 8.20% over the forecast period 2025-2035.

Introduction to Vibration Test Equipment Market:

Vibration test equipment plays a critical role in the defense industry by ensuring the mechanical robustness, structural integrity, and performance reliability of mission-critical systems under operational stress conditions. From aircraft avionics and missile components to ruggedized communication systems and mobile ground vehicles, defense platforms are subject to harsh vibration environments during deployment. The global defense vibration test equipment market exists at the intersection of mechanical engineering and mission assurance, providing simulation capabilities that replicate shock, impact, and sustained vibration encountered in real-world scenarios. As defense systems become increasingly complex and miniaturized, with tighter tolerances and multi-domain functionality, the need for advanced testing infrastructure has intensified. Vibration test equipment is used across multiple phases of the product lifecycle-from prototype validation to final product certification and ongoing system upgrades. Defense contractors, government laboratories, and aerospace test centers rely on these tools to verify compliance with international military standards such as MIL-STD-810 and NATO STANAG protocols. The market includes a range of technologies, including electrodynamic shakers, hydraulic vibration tables, and multi-axis systems, which are increasingly integrated with digital data acquisition systems for high-fidelity analysis. As the defense sector pivots toward rapid system deployment and lifecycle extension strategies, vibration test equipment is becoming indispensable in reducing development risk and enhancing combat-readiness assurance.

Technology Impact in Vibration Test Equipment Market:

Technological advancements are redefining the capabilities and performance metrics of vibration test equipment used in the defense sector. Modern systems now integrate high-resolution sensors, real-time control software, and machine learning-based analytics to deliver more precise and adaptable testing environments. One of the most transformative shifts has been the incorporation of digital twin technology, where virtual replicas of components or systems are subjected to simulated vibration scenarios to identify structural vulnerabilities without physical destruction. These digital simulations are then validated with physical test data captured through high-frequency accelerometers and strain gauges, enabling a feedback loop that refines design and enhances predictive maintenance models. Additionally, the transition to multi-axis vibration platforms has allowed for simultaneous excitation along different vectors-X, Y, and Z axes-thereby providing more realistic simulations of actual battlefield motion, whether it be in airborne, seaborne, or land-based conditions. Innovations in cooling systems and dynamic load control have also expanded the use of high-force electrodynamic shakers capable of replicating extreme launch, flight, or transport conditions. Furthermore, AI-driven software can now automatically adjust test parameters in real-time based on sensor feedback, reducing test time and improving accuracy. As defense R&D moves toward more agile and accelerated development cycles, technology-enhanced vibration test systems are emerging as essential enablers of reliability assurance, structural certification, and system resilience in increasingly dynamic military environments.

Key Drivers in Vibration Test Equipment Market:

Several strategic and operational factors are propelling the demand for advanced vibration test equipment within global defense sectors. Chief among them is the growing complexity and performance demands of modern defense systems, many of which include compact electronic assemblies, high-precision guidance units, and modular structural elements-all of which must endure unpredictable environmental and mechanical stressors. As militaries pursue lighter, more agile, and electronically integrated systems, ensuring these components maintain functional integrity under vibration is not optional-it is mandatory. Another significant driver is the ongoing global push for defense system modernization and platform interoperability, particularly as countries phase out legacy platforms in favor of next-generation vehicles, missiles, and aircraft that require new testing protocols. In addition, increasing investments in hypersonic weapons, reusable space systems, and unmanned combat aerial vehicles (UCAVs) have introduced new vibration test parameters involving high-speed transit, atmospheric re-entry, and extreme thermal variation-conditions that place unparalleled mechanical stress on sensitive subsystems. Government defense contracts also increasingly specify stricter compliance with environmental test standards, which necessitates the use of highly capable and certifiable vibration test solutions. Finally, the defense industry's growing emphasis on extending asset lifecycles-through structural health monitoring and predictive maintenance-relies heavily on test equipment that can simulate operational wear and assess material fatigue before critical failure occurs. Collectively, these drivers are transforming vibration testing from a routine verification process to a strategic function within defense systems engineering and lifecycle management.

Regional Trends in Vibration Test Equipment Market:

The adoption and development of vibration test equipment in the defense sector varies across global regions, reflecting distinct national priorities, defense procurement strategies, and industrial capabilities. In North America, particularly the United States, defense agencies and prime contractors maintain some of the world's most sophisticated test facilities, supporting development of aircraft like the F-35, missile systems under the Missile Defense Agency, and space programs led by the U.S. Space Force. These facilities invest in cutting-edge vibration simulation infrastructure, often paired with climate chambers and EMI/EMC labs, to deliver comprehensive qualification processes. Canada also maintains an active role, especially in testing for NATO-interoperable systems and cold-weather stress applications. In Europe, countries like Germany, France, and the UK are investing heavily in vibration testing capabilities for joint defense programs like the Future Combat Air System (FCAS) and Tempest, while also supporting dual-use technologies for both military and civil aviation. European defense firms often collaborate with academic institutions and testing consortia, creating innovation clusters that advance vibration simulation methods and standards compliance. In the Asia-Pacific region, China and India are rapidly expanding their defense manufacturing bases and associated testing infrastructure. China, in particular, is building large-scale vibration and shock testing complexes to support the development of indigenous fighter aircraft, long-range missile systems, and space assets. India, through DRDO and ISRO, is enhancing its vibration test capabilities as it pushes toward strategic autonomy in defense production. Japan and South Korea, while smaller in defense output, lead in high-precision vibration systems used for naval and aerospace component qualification. In the Middle East, especially in countries like the UAE and Saudi Arabia, there is growing investment in establishing in-country test facilities as part of defense localization efforts. These regional trends suggest that while North America and Europe maintain leadership in vibration testing technology, Asia-Pacific and the Middle East are rapidly scaling up their capabilities to meet domestic manufacturing and strategic independence goals.

Key Vibration Test Equipment Program:

The impending deployment of the U.S. Army's Long-Range Hypersonic Weapon (LRHW), officially named "Dark Eagle," signals a significant shift in the dynamics of modern warfare. Expected to enter service by the end of fiscal year 2025, Dark Eagle marks the United States' official entry into the hypersonic missile arena-an area currently led by China and Russia. This development holds far-reaching implications for both U.S. military capabilities and the broader global strategic balance and deterrence posture.

Table of Contents

Global vibration test equipment Market - Table of Contents

Global vibration test equipment Market Report Definition

Global vibration test equipment Market Segmentation

By Region

By Type

By Equipment Type

By Application

Global vibration test equipment Market Analysis for next 10 Years

The 10-year Global vibration test equipment market analysis would give a detailed overview of Global vibration test equipment market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Global vibration test equipment Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global vibration test equipment Market Forecast

The 10-year Global vibration test equipment market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Global vibration test equipment Market Trends & Forecast

The regional Global vibration test equipment market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Global vibration test equipment Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Global vibration test equipment Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Global vibration test equipment Market Report

Hear from our experts their opinion of the possible analysis for this market.