空気力学試験およびシミュレーションの世界市場:2025年~2035年

Global Aerodynamics Testing and Simulation Market 2025-2035

- 発行日

- ページ情報

- 英文 150+ Pages

- 納期

- 3営業日

- 商品コード

- 1709978

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

- 航空宇宙/防衛関連専門 航空宇宙/防衛関連専門を専門とする市場調査会社です。

概要

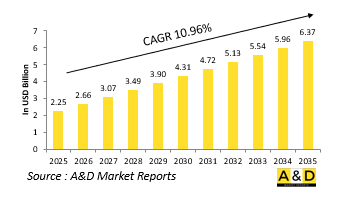

世界の空気力学試験およびシミュレーションの市場規模は、2025年に22億5,000万米ドルと予測され、2035年までにCAGR(年間平均成長率)10.96%で拡大し、63億7,000万米ドルに成長すると予測されています。

空気力学試験およびシミュレーション市場の導入:

防衛空気力学試験およびシミュレーション市場は、軍用機、ミサイル、無人航空機システムの設計、市場開拓、運用の改良において極めて重要な役割を果たしています。防衛プラットフォームが高度化するにつれて、その空気力学性能は操縦性、生存性、燃料効率、任務効果に直接影響します。試験とシミュレーションにより、これらの性能パラメータを制御された極限条件下で安全かつコスト効率よく評価することができます。風洞、数値流体力学ツール、および仮想飛行環境は、この市場の基盤を形成し、エンジニアや戦略家に複雑な機体全体の気流、熱分布、および圧力力学をモデル化する能力を提供します。これらの機能は、新規設計の検証、レガシーシステムの改善、さまざまな環境条件や戦闘条件下での最適性能の確保に不可欠です。また、空気力学シミュレーションは、ステルス最適化、兵器統合、高速飛行計画など、現代戦における重要な要素もサポートします。さらに、これらの技術は、実世界のシナリオにおける車両の挙動を正確にモデリングできるため、戦略立案にも貢献します。空中戦が敏捷性、速度、低観測性に依存するようになるにつれ、空気力学試験およびシミュレーションの重要性は高まり続けています。この市場は、研究と生産だけでなく、今日の進化する脅威環境で必要とされる継続的な適応もサポートしています。

空気力学試験およびシミュレーション市場における技術の影響:

新たな技術は、防衛空気力学試験およびシミュレーションの状況を一変させ、物理環境と仮想環境の両方において、より高い精度、拡張性、リアリズムを可能にしています。ハイパフォーマンスコンピューティングは計算流体力学に革命をもたらし、解析者は非常に複雑な流れの状態を、かつてない精度とスピードでシミュレーションできるようになりました。これらのデジタルモデルは、乱流、熱負荷、制御面や組み込み兵器システム間の相互作用など、多変数のシナリオを考慮できるようになりました。機械学習の統合により、膨大なデータセットに基づいて性能パターンを特定し、設計の反復を最適化することで、シミュレーション出力がさらに洗練されます。これと並行して、極限高度・極限速度条件をシミュレートする次世代風洞が進化し、極超音速プラットフォームや操縦可能な滑空機の開発をサポートしています。また、バーチャルリアリティや没入型インターフェースは、エンジニアやパイロットが空気力学モデルと対話する方法に影響を与え始めており、気流力学や車両の挙動に関する直感的な洞察を提供しています。さらに、クラウドベースのシミュレーションツールは、防衛関連企業、研究機関、軍需企業の間で世界なコラボレーションと安全なデータ共有を可能にしています。このような技術の融合により、開発サイクルが短縮されるだけでなく、システム検証も強化され、競合する複雑な空中環境でも運用できる、より俊敏で適応性の高い防衛プラットフォームに貢献しています。

空気力学試験およびシミュレーション市場の主な促進要因:

防衛空気力学試験およびシミュレーション市場の成長を後押ししている主な要因はいくつかあります。最も重要な要因の1つは、航空戦闘システムの複雑化であり、進化するミッションの要求を満たすために高度な空気力学プロファイルが必要となります。軍用機やミサイルは、速度、高度、大気条件の幅広い範囲にわたって確実に動作しなければならないため、厳格な試験と忠実度の高いシミュレーションが必要となります。ステルス性が現代の機体に期待されるベースラインとなるにつれ、空気力学形状は、性能と安定性を維持しながらレーダー回避をサポートするように最適化されなければなりません。極超音速技術の台頭は気流挙動に新たなフロンティアをもたらし、極端な熱・圧力条件に対応できるシミュレーションツールを要求しています。さらに、ライフサイクルコストの削減と効率的なプラットフォーム開発の推進により、コストのかかる物理試験への依存を最小限に抑える仮想試験環境の利用が推奨されています。訓練やミッションのリハーサルシステムも空気力学シミュレーションの恩恵を受けており、航空機乗組員が新しいプラットフォームや変更されたプラットフォームのハンドリング特性を理解するのに役立っています。一方、マルチロールUAVや浮遊弾への関心が高まる中、耐久性、ペイロード、および操縦性のために空気力学特性を改善する必要があります。これらの推進力は、開発だけでなく、任務の即応性と作戦上の優位性を確保する上でも、空気力学試験の役割が拡大していることを浮き彫りにしています。

空気力学試験およびシミュレーション市場の地域動向:

世界の防衛空気力学試験およびシミュレーション市場は、国家の優先事項、産業能力、および先進航空宇宙システムへの投資によって形成された明確な地域プロファイルを示しています。北米、特に米国では、市場は強固な防衛研究開発エコシステムと、風洞、シミュレーションラボ、飛行試験場などの広範なインフラによって支えられています。これらの施設は、次世代航空機プログラム、極超音速兵器開発、統合防空プラットフォームの支援において中心的な役割を果たしています。欧州は、共同研究イニシアティブと多国籍防衛プログラムを重視しており、その結果、高度なシミュレーション能力とデジタル設計ハブへの投資が共有されています。フランス、ドイツ、英国などの国々は、国内および共同での航空宇宙開発努力を支援する専用の試験施設を維持しています。アジア太平洋地域では、国産防衛航空プログラムの急速な進展により、国内のシミュレーションおよび試験能力に対する需要が高まっています。インド、中国、韓国などの国々は、外国の検証への依存を減らし、自国の航空宇宙開発スケジュールを早めるために、技術インフラを拡張しています。中東では、防衛産業化に対する関心から、国際的な航空宇宙企業との提携が進み、空気力学モデリングと検証の現地能力を開発しています。各地域の軌跡は、その戦略的目標と世界の防衛情勢における進化する役割を反映しています。

主要な空気力学試験およびシミュレーションプログラム:

将来の戦闘航空システム(FCAS)は、防衛と安全保障における主権を維持するための欧州の努力の要です。FCASの中核には次世代兵器システム(NGWS)があり、高度な「システム・オブ・システム」の基盤を形成します。この統合ネットワークは、有人新世代戦闘機が無人遠隔輸送機と連携して運用され、すべてが「コンバット・クラウド」(空、陸、海、宇宙、サイバースペースにわたる資産をつなぐ安全なデータネットワーク)を通じてシームレスに接続されることを特徴とします。これらの相互接続されたプラットフォームは、センサー、エフェクター、コマンド・アンド・コントロール・ノードとして機能し、迅速かつ柔軟な意思決定をサポートします。FCASを支えるアーキテクチャは、オープンでモジュール化されたサービス指向のもので、将来のプラットフォームや新技術の統合を可能にします。国家と同盟国の資産は、それぞれの能力を提供することでNGWSを補完し、相互運用可能なネットワーク化されたシステムの総合力によって、複数の領域にわたる真の共同戦闘環境を可能にします。

当レポートでは、世界の空気力学試験およびシミュレーション市場について調査し、10年間のセグメント別市場予測、技術動向、機会分析、企業プロファイル、国別データなどをまとめています。

目次

世界の空気力学試験およびシミュレーション市場- 目次

世界の空気力学試験およびシミュレーション市場レポートの定義

世界の空気力学試験およびシミュレーション市場セグメンテーション

- 試験方法別

- 技術別

- 最終用途別

- 地域別

今後10年間の世界の空気力学試験およびシミュレーション市場分析

この章では、10年間にわたる世界の空気力学テストおよびシミュレーション市場の分析により、世界の空気力学テストおよびシミュレーション市場の成長、変化する動向、技術採用の概要、および全体的な市場の魅力について詳細な概要が示されます。

世界の空気力学試験およびシミュレーション市場の市場技術

このセグメントでは、この市場に影響を与えると予想される上位10の技術と、これらの技術が市場全体に与える可能性のある影響について説明します。

世界の空気力学試験およびシミュレーション市場予測

この市場の10年間の世界の空気力学テストおよびシミュレーション市場予測は、上記のセグメント全体で詳細にカバーされています。

地域別世界空気力学試験およびシミュレーション市場の動向と予測

このセグメントでは、地域別の対ドローン市場の動向、促進要因、抑制要因、課題、そして政治、経済、社会、技術といった側面を網羅しています。また、地域別の市場予測とシナリオ分析も詳細に取り上げています。地域分析の最後には、主要企業のプロファイリング、サプライヤーの情勢、企業ベンチマークが含まれています。現在の市場規模は、通常のシナリオに基づいて推定されています。

- 北米

- 促進要因、抑制、課題

- PEST

市場予測とシナリオ分析

- 主要企業

- サプライヤー階層の情勢

- 企業ベンチマーク

- 欧州

- 中東

- アジア太平洋

- 南米

世界の空気力学試験およびシミュレーション市場の国別分析

この章では、この市場における主要な防衛プログラムを取り上げ、この市場で申請された最新のニュースや特許についても解説します。また、国レベルの10年間の市場予測とシナリオ分析についても解説します。

- 米国

- 防衛プログラム

- 最新ニュース

- 特許

- この市場における現在の技術成熟度

市場予測とシナリオ分析

カナダ

イタリア

フランス

ドイツ

オランダ

ベルギー

スペイン

スウェーデン

ギリシャ

オーストラリア

南アフリカ

インド

中国

ロシア

韓国

日本

マレーシア

シンガポール

ブラジル

世界の空気力学試験およびシミュレーション市場の機会マトリックス

世界の空気力学試験およびシミュレーション市場に関する専門家の意見

結論

航空・防衛市場レポートについて

図表

List of Tables

- Table 1: 10 Year Market Outlook, 2022-2032

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2022-2032

- Table 18: Scenario Analysis, Scenario 1, By Test Methods, 2022-2032

- Table 19: Scenario Analysis, Scenario 1, By Technology, 2022-2032

- Table 20: Scenario Analysis, Scenario 1, By End User, 2022-2032

- Table 21: Scenario Analysis, Scenario 2, By Region, 2022-2032

- Table 22: Scenario Analysis, Scenario 2, By Test Methods, 2022-2032

- Table 23: Scenario Analysis, Scenario 2, By Technology, 2022-2032

- Table 24: Scenario Analysis, Scenario 2, By End User, 2022-2032

List of Figures

- Figure 1: Global Aerodynamics Testing and Simulation Forecast, 2022-2032

- Figure 2: Global Aerodynamics Testing and Simulation Forecast, By Region, 2022-2032

- Figure 3: Global Aerodynamics Testing and Simulation Forecast, By Test Methods, 2022-2032

- Figure 4: Global Aerodynamics Testing and Simulation Forecast, By Technology, 2022-2032

- Figure 5: Global Aerodynamics Testing and Simulation Forecast, By End User, 2022-2032

- Figure 6: North America, Aerodynamics Testing and Simulation, Market Forecast, 2022-2032

- Figure 7: Europe, Aerodynamics Testing and Simulation, Market Forecast, 2022-2032

- Figure 8: Middle East, Aerodynamics Testing and Simulation, Market Forecast, 2022-2032

- Figure 9: APAC, Aerodynamics Testing and Simulation, Market Forecast, 2022-2032

- Figure 10: South America, Aerodynamics Testing and Simulation, Market Forecast, 2022-2032

- Figure 11: United States, Aerodynamics Testing and Simulation, Technology Maturation, 2022-2032

- Figure 12: United States, Aerodynamics Testing and Simulation, Market Forecast, 2022-2032

- Figure 13: Canada, Aerodynamics Testing and Simulation, Technology Maturation, 2022-2032

- Figure 14: Canada, Aerodynamics Testing and Simulation, Market Forecast, 2022-2032

- Figure 15: Italy, Aerodynamics Testing and Simulation, Technology Maturation, 2022-2032

- Figure 16: Italy, Aerodynamics Testing and Simulation, Market Forecast, 2022-2032

- Figure 17: France, Aerodynamics Testing and Simulation, Technology Maturation, 2022-2032

- Figure 18: France, Aerodynamics Testing and Simulation, Market Forecast, 2022-2032

- Figure 19: Germany, Aerodynamics Testing and Simulation, Technology Maturation, 2022-2032

- Figure 20: Germany, Aerodynamics Testing and Simulation, Market Forecast, 2022-2032

- Figure 21: Netherlands, Aerodynamics Testing and Simulation, Technology Maturation, 2022-2032

- Figure 22: Netherlands, Aerodynamics Testing and Simulation, Market Forecast, 2022-2032

- Figure 23: Belgium, Aerodynamics Testing and Simulation, Technology Maturation, 2022-2032

- Figure 24: Belgium, Aerodynamics Testing and Simulation, Market Forecast, 2022-2032

- Figure 25: Spain, Aerodynamics Testing and Simulation, Technology Maturation, 2022-2032

- Figure 26: Spain, Aerodynamics Testing and Simulation, Market Forecast, 2022-2032

- Figure 27: Sweden, Aerodynamics Testing and Simulation, Technology Maturation, 2022-2032

- Figure 28: Sweden, Aerodynamics Testing and Simulation, Market Forecast, 2022-2032

- Figure 29: Brazil, Aerodynamics Testing and Simulation, Technology Maturation, 2022-2032

- Figure 30: Brazil, Aerodynamics Testing and Simulation, Market Forecast, 2022-2032

- Figure 31: Australia, Aerodynamics Testing and Simulation, Technology Maturation, 2022-2032

- Figure 32: Australia, Aerodynamics Testing and Simulation, Market Forecast, 2022-2032

- Figure 33: India, Aerodynamics Testing and Simulation, Technology Maturation, 2022-2032

- Figure 34: India, Aerodynamics Testing and Simulation, Market Forecast, 2022-2032

- Figure 35: China, Aerodynamics Testing and Simulation, Technology Maturation, 2022-2032

- Figure 36: China, Aerodynamics Testing and Simulation, Market Forecast, 2022-2032

- Figure 37: Saudi Arabia, Aerodynamics Testing and Simulation, Technology Maturation, 2022-2032

- Figure 38: Saudi Arabia, Aerodynamics Testing and Simulation, Market Forecast, 2022-2032

- Figure 39: South Korea, Aerodynamics Testing and Simulation, Technology Maturation, 2022-2032

- Figure 40: South Korea, Aerodynamics Testing and Simulation, Market Forecast, 2022-2032

- Figure 41: Japan, Aerodynamics Testing and Simulation, Technology Maturation, 2022-2032

- Figure 42: Japan, Aerodynamics Testing and Simulation, Market Forecast, 2022-2032

- Figure 43: Malaysia, Aerodynamics Testing and Simulation, Technology Maturation, 2022-2032

- Figure 44: Malaysia, Aerodynamics Testing and Simulation, Market Forecast, 2022-2032

- Figure 45: Singapore, Aerodynamics Testing and Simulation, Technology Maturation, 2022-2032

- Figure 46: Singapore, Aerodynamics Testing and Simulation, Market Forecast, 2022-2032

- Figure 47: United Kingdom, Aerodynamics Testing and Simulation, Technology Maturation, 2022-2032

- Figure 48: United Kingdom, Aerodynamics Testing and Simulation, Market Forecast, 2022-2032

- Figure 49: Opportunity Analysis, Aerodynamics Testing and Simulation, By Region (Cumulative Market), 2022-2032

- Figure 50: Opportunity Analysis, Aerodynamics Testing and Simulation, By Region (CAGR), 2022-2032

- Figure 51: Opportunity Analysis, Aerodynamics Testing and Simulation, By Technology (Cumulative Market), 2022-2032

- Figure 52: Opportunity Analysis, Aerodynamics Testing and Simulation, By Technology (CAGR), 2022-2032

- Figure 53: Opportunity Analysis, Aerodynamics Testing and Simulation, By Test Methods (Cumulative Market), 2022-2032

- Figure 54: Opportunity Analysis, Aerodynamics Testing and Simulation, By Test Methods (CAGR), 2022-2032

- Figure 55: Opportunity Analysis, Aerodynamics Testing and Simulation, By End User (Cumulative Market), 2022-2032

- Figure 56: Opportunity Analysis, Aerodynamics Testing and Simulation, By End User (CAGR), 2022-2032

- Figure 57: Scenario Analysis, Aerodynamics Testing and Simulation, Cumulative Market, 2022-2032

- Figure 58: Scenario Analysis, Aerodynamics Testing and Simulation, Global Market, 2022-2032

- Figure 59: Scenario 1, Aerodynamics Testing and Simulation, Total Market, 2022-2032

- Figure 60: Scenario 1, Aerodynamics Testing and Simulation, By Region, 2022-2032

- Figure 61: Scenario 1, Aerodynamics Testing and Simulation, By Test Methods, 2022-2032

- Figure 62: Scenario 1, Aerodynamics Testing and Simulation, By Test Methods, 2022-2032

- Figure 63: Scenario 1, Aerodynamics Testing and Simulation, By End User, 2022-2032

- Figure 64: Scenario 2, Aerodynamics Testing and Simulation, Total Market, 2022-2032

- Figure 65: Scenario 2, Aerodynamics Testing and Simulation, By Region, 2022-2032

- Figure 66: Scenario 2, Aerodynamics Testing and Simulation, By Test Methods, 2022-2032

- Figure 67: Scenario 2, Aerodynamics Testing and Simulation, By Technology, 2022-2032

- Figure 68: Scenario 2, Aerodynamics Testing and Simulation, By End User, 2022-2032

- Figure 69: Company Benchmark, Aerodynamics Testing and Simulation, 2022-2032

目次

The Global Aerodynamics Testing and Simulation market is estimated at USD 2.25 billion in 2025, projected to grow to USD 6.37 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 10.96% over the forecast period 2025-2035.

Introduction to Aerodynamics Testing and Simulation Market:

The defense aerodynamics testing and simulation market plays a pivotal role in the design, development, and operational refinement of military aircraft, missiles, and unmanned aerial systems. As defense platforms become more advanced, their aerodynamic performance directly impacts maneuverability, survivability, fuel efficiency, and mission effectiveness. Testing and simulation allow for the safe and cost-effective evaluation of these performance parameters under controlled and extreme conditions. Wind tunnels, computational fluid dynamics tools, and virtual flight environments form the foundation of this market, offering engineers and strategists the ability to model airflow, heat distribution, and pressure dynamics across complex airframes. These capabilities are essential for validating new designs, improving legacy systems, and ensuring optimal performance under variable environmental and combat conditions. Aerodynamic simulation also supports stealth optimization, weapon integration, and high-speed flight planning-key elements in modern warfare. Furthermore, these technologies contribute to strategic planning by enabling accurate modeling of vehicle behavior in real-world scenarios. As aerial warfare becomes more dependent on agility, speed, and low observability, the significance of aerodynamic testing and simulation continues to grow. This market supports not only research and production but also the continuous adaptation required in today's evolving threat environments.

Technology Impact in Aerodynamics Testing and Simulation Market:

Emerging technologies are transforming the landscape of defense aerodynamics testing and simulation, enabling greater precision, scalability, and realism in both physical and virtual environments. High-performance computing has revolutionized computational fluid dynamics, allowing analysts to simulate highly complex flow conditions with unprecedented accuracy and speed. These digital models can now account for multi-variable scenarios, including turbulence, thermal loads, and interactions between control surfaces and embedded weapons systems. The integration of machine learning further refines simulation outputs by identifying performance patterns and optimizing design iterations based on vast datasets. In parallel, next-generation wind tunnels have evolved to simulate extreme altitude and velocity conditions, supporting the development of hypersonic platforms and maneuverable glide vehicles. Virtual reality and immersive interfaces are also beginning to influence how engineers and pilots interact with aerodynamic models, providing intuitive insights into airflow dynamics and vehicle behavior. Moreover, cloud-based simulation tools are enabling global collaboration and secure data sharing among defense contractors, research institutions, and military clients. This technological convergence is not only reducing development cycles but also enhancing system validation, contributing to more agile and adaptable defense platforms capable of operating in contested and complex aerial environments.

Key Drivers in Aerodynamics Testing and Simulation Market:

Several key factors are propelling growth in the defense aerodynamics testing and simulation market. One of the most significant is the increasing complexity of aerial combat systems, which require advanced aerodynamic profiles to meet evolving mission demands. Military aircraft and missiles must perform reliably across a broad spectrum of speeds, altitudes, and atmospheric conditions, which necessitates rigorous testing and high-fidelity simulation. As stealth becomes a baseline expectation in modern airframes, aerodynamic shaping must be optimized to support radar evasion while maintaining performance and stability. The rise of hypersonic technologies has introduced a new frontier in airflow behavior, demanding simulation tools that can handle extreme thermal and pressure conditions. Additionally, the push for reduced lifecycle costs and more efficient platform development encourages the use of virtual testing environments that minimize reliance on costly physical trials. Training and mission rehearsal systems also benefit from aerodynamic simulations, helping aircrews understand the handling characteristics of new or modified platforms. Meanwhile, growing interest in multi-role UAVs and loitering munitions requires aerodynamic refinement for endurance, payload, and maneuverability. These drivers highlight the expanding role of aerodynamic testing not just in development, but also in ensuring mission readiness and operational superiority.

Regional Trends in Aerodynamics Testing and Simulation Market:

The global defense aerodynamics testing and simulation market exhibits distinct regional profiles shaped by national priorities, industrial capabilities, and investment in advanced aerospace systems. In North America, particularly the United States, the market is supported by a robust defense R&D ecosystem and an extensive infrastructure of wind tunnels, simulation labs, and flight test ranges. These facilities play a central role in supporting next-generation aircraft programs, hypersonic weapons development, and integrated air defense platforms. Europe places strong emphasis on collaborative research initiatives and multinational defense programs, which has led to shared investment in advanced simulation capabilities and digital design hubs. Countries like France, Germany, and the United Kingdom maintain dedicated testing facilities that support both national and joint aerospace development efforts. In Asia-Pacific, rapid advancements in indigenous defense aviation programs are driving demand for domestic simulation and testing capabilities. Nations such as India, China, and South Korea are expanding their technical infrastructure to reduce dependency on foreign validation and accelerate their own aerospace timelines. In the Middle East, interest in defense industrialization is leading to partnerships with international aerospace firms to develop local capabilities in aerodynamic modeling and verification. Each region's trajectory reflects its strategic objectives and evolving role in the global defense landscape.

Key Aerodynamics Testing and Simulation Program:

The Future Combat Air System (FCAS) is a cornerstone of Europe's efforts to maintain sovereignty in defense and security. At the heart of FCAS lies the Next Generation Weapon System (NGWS), forming the foundation of a sophisticated "system of systems." This integrated network will feature manned New Generation Fighters operating in tandem with Unmanned Remote Carriers, all seamlessly connected through the "Combat Cloud"-a secure data network linking assets across air, land, sea, space, and cyberspace. These interconnected platforms will function as sensors, effectors, and command-and-control nodes, supporting rapid and flexible decision-making. The architecture behind FCAS is open, modular, and service-oriented, allowing for the integration of future platforms and emerging technologies. National and allied assets will complement the NGWS by contributing their distinct capabilities, enabling a truly collaborative combat environment across multiple domains through the combined strength of interoperable, networked systems.

Table of Contents

Global aerodynamics testing and simulation market- Table of Contents

Global aerodynamics testing and simulation market Report Definition

Global aerodynamics testing and simulation market Segmentation

By Test method

By Technology

By End Use

By Region

Global aerodynamics testing and simulation market Analysis for next 10 Years

The 10-year Global aerodynamics testing and simulation market analysis would give a detailed overview of Global aerodynamics testing and simulation market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Global aerodynamics testing and simulation market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global aerodynamics testing and simulation market Forecast

The 10-year Global aerodynamics testing and simulation market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Global aerodynamics testing and simulation market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Global aerodynamics testing and simulation market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Global aerodynamics testing and simulation market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Global aerodynamics testing and simulation market

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

- 発行日

- 発行

- Aviation & Defense Market Reports (A&D)

- ページ情報

- 英文 150+ Pages

- 納期

- 3営業日