|

市場調査レポート

商品コード

1680165

防衛ヘリコプターエンジンの世界市場:2025年~2035年Global Defense Helicopter Engine Market 2025-2035 |

||||||

|

|||||||

| 防衛ヘリコプターエンジンの世界市場:2025年~2035年 |

|

出版日: 2025年03月14日

発行: Aviation & Defense Market Reports (A&D)

ページ情報: 英文 150+ Pages

納期: 3営業日

|

全表示

- 概要

- 図表

- 目次

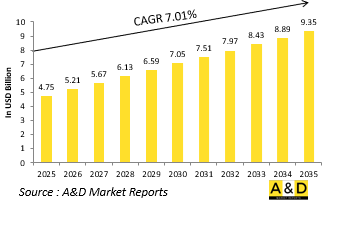

世界の防衛ヘリコプターエンジンの市場規模は、2025年に47億5,000万米ドルと予測され、2024年から2034年の予測期間中に7.01%の年間平均成長率(CAGR)で拡大し、2035年までに93億5,000万米ドルに成長すると予測されています。

世界の防衛ヘリコプターエンジン市場は、戦闘、偵察、輸送、捜索救助などの任務に使用される幅広い回転翼機を支える、軍事航空にとって極めて重要なコンポーネントです。ヘリコプターは現代の戦争において欠かすことのできない役割を担っており、攻撃と防御の両方の作戦において多用途性を提供しています。山岳地帯、密林、市街戦地帯など、厳しい環境でも活動できることから、世界中の軍隊がヘリコプターに信頼を寄せています。これらのヘリコプターを動かすエンジンは、軍事作戦の厳しい要求を満たしながら、高い性能、耐久性、効率を提供しなければなりません。国防の近代化努力の進行、地政学的緊張の高まり、マルチロール能力の重視の高まりに伴い、先進的なヘリコプターエンジンに対する需要は世界的に高まっています。大手防衛請負業者とエンジン・メーカーは、運用効果、燃料効率、メンテナンスの信頼性を高めるため、最先端の推進技術に投資しています。

技術革新は、出力重量比の改善、燃料効率、運用寿命の延長に重点を置いており、防衛ヘリコプターエンジン市場の大幅な進歩を牽引しています。最も注目すべきブレークスルーのひとつは、より効率的なターボシャフトエンジンの開発であり、全体的な重量を軽減しながら優れた出力を提供します。セラミックマトリックス複合材料(CMC)や軽量合金などの先端材料の使用により、エンジンの耐熱性と耐久性が大幅に向上し、ヘリコプターがより高い温度と高度でより高い信頼性をもって運用できるようになりました。全権デジタルエンジン制御(FADEC)を含むデジタルエンジン制御システムは、燃料消費を最適化し、パイロットの作業負担を軽減し、メンテナンス診断を改善することで、エンジン性能を向上させました。これらのスマートエンジンマネジメントシステムは、リアルタイムのモニタリングと予知保全機能を提供し、ダウンタイムを最小限に抑え、ミッションの即応性を確保します。ハイブリッド電気推進の統合も新たな動向であり、燃料消費を抑え、音響シグネチャーを低減し、ステルス運用に理想的なハイブリッド電気ヘリコプターの開発研究が進められています。アディティブ・マニュファクチャリング(3Dプリンティング)の進歩も、複雑なエンジン部品の製造を一変させ、リードタイムを短縮し、新しい設計の迅速なプロトタイピングを可能にしています。

防衛ヘリコプターエンジン市場の成長を促進する主な要因には、軍事調達プログラムの増加、フリートの近代化需要、運用能力の強化ニーズなどがあります。多くの国では、老朽化したヘリコプターを、速度、積載量、燃料効率を向上させることができる先進的なエンジンを搭載した近代的な回転翼機に置き換えようとしています。戦闘、輸送、医療避難の各ミッションをシームレスに移行できるマルチロールヘリコプターの推進により、適応性の高い高性能エンジンの需要が高まっています。さらに、紛争環境における垂直上昇能力の重要性が高まっているため、次世代ロータークラフトと推進システムへの投資が活発化しています。特に米国におけるFuture Vertical Lift(FVL)プログラムの出現は、市場を形成する主要な促進要因です。これらの構想は、優れた耐久性と生存性を提供する最先端のエンジンを搭載した高速長距離軍用ヘリコプターの開発を目的としています。米国、中国、欧州諸国を含む主要な軍事大国の国防予算の増加は、新型ヘリコプターエンジンへの投資をさらに加速させています。もう一つの重要な要因は、燃料効率と持続可能性の改善に対するニーズです。防衛軍は、長期間の展開における燃料消費に関連する物流上の課題と運用コストの削減を求めているからです。

防衛ヘリコプターエンジン市場の地域動向は、軍の優先事項、技術力、調達戦略の違いを反映しています。北米は依然として優勢で、米国が技術革新と調達の両面でリードしています。米国軍は、UH-60ブラックホーク、AH-64アパッチ、CH-47チヌーク、V-22オスプレイなどの機種を含む世界最大級のヘリコプターを運用しています。FVLイニシアチブの下での未来長距離攻撃機(FLRAA)や未来攻撃偵察機(FARA)のようなプログラムは、出力、航続距離、効率を向上させた次世代エンジンの需要を促進しています。General Electric Aviation、Honeywell、Rolls-Royce North Americなどの大手エンジンメーカーは、これらの先進的な回転翼機をサポートする新しい推進技術の開発の最前線にいます。カナダは、軍用ヘリコプターの保有機数は少ないもの、既存機の性能を高めるためにエンジンのアップグレードとメンテナンス・プログラムへの投資を続けています。

当レポートでは、世界の防衛ヘリコプターエンジン市場について調査し、10年間のセグメント別市場予測、技術動向、機会分析、企業プロファイル、国別データなどをまとめています。

目次

防衛ヘリコプターエンジン市場レポートの定義

防衛ヘリコプターエンジン市場セグメンテーション

- プラットフォーム別

- スラスト別

- 地域別

今後10年間の防衛ヘリコプターエンジン市場分析

防衛ヘリコプターエンジン市場の市場技術

世界の防衛ヘリコプターエンジン市場予測

防衛ヘリコプターエンジン市場の動向と予測、地域別

- 北米

- 促進要因、抑制要因、課題

- PEST

- 市場予測とシナリオ分析

- 主要企業

- サプライヤー階層の情勢

- 企業ベンチマーク

- 欧州

- 中東

- アジア太平洋

- 南米

防衛ヘリコプターエンジン市場の国別分析

- 米国

- 防衛プログラム

- 最新ニュース

- 特許

- この市場における現在の技術成熟度

- 市場予測とシナリオ分析

- カナダ

- イタリア

- フランス

- ドイツ

- オランダ

- ベルギー

- スペイン

- スウェーデン

- ギリシャ

- オーストラリア

- 南アフリカ

- インド

- 中国

- ロシア

- 韓国

- 日本

- マレーシア

- シンガポール

- ブラジル

防衛ヘリコプターエンジン市場の機会マトリックス

防衛ヘリコプターエンジン市場レポートに関する専門家の意見

結論

航空・防衛市場レポートについて

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Thrust, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Thrust, 2025-2035

List of Figures

- Figure 1: Global Defense Helicopter Engine Market Forecast, 2025-2035

- Figure 2: Global Defense Helicopter Engine Market Forecast, By Region, 2025-2035

- Figure 3: Global Defense Helicopter Engine Market Forecast, By Platform, 2025-2035

- Figure 4: Global Defense Helicopter Engine Market Forecast, By Thrust, 2025-2035

- Figure 5: North America, Defense Helicopter Engine Market, Market Forecast, 2025-2035

- Figure 6: Europe, Defense Helicopter Engine Market, Market Forecast, 2025-2035

- Figure 7: Middle East, Defense Helicopter Engine Market, Market Forecast, 2025-2035

- Figure 8: APAC, Defense Helicopter Engine Market, Market Forecast, 2025-2035

- Figure 9: South America, Defense Helicopter Engine Market, Market Forecast, 2025-2035

- Figure 10: United States, Defense Helicopter Engine Market, Technology Maturation, 2025-2035

- Figure 11: United States, Defense Helicopter Engine Market, Market Forecast, 2025-2035

- Figure 12: Canada, Defense Helicopter Engine Market, Technology Maturation, 2025-2035

- Figure 13: Canada, Defense Helicopter Engine Market, Market Forecast, 2025-2035

- Figure 14: Italy, Defense Helicopter Engine Market, Technology Maturation, 2025-2035

- Figure 15: Italy, Defense Helicopter Engine Market, Market Forecast, 2025-2035

- Figure 16: France, Defense Helicopter Engine Market, Technology Maturation, 2025-2035

- Figure 17: France, Defense Helicopter Engine Market, Market Forecast, 2025-2035

- Figure 18: Germany, Defense Helicopter Engine Market, Technology Maturation, 2025-2035

- Figure 19: Germany, Defense Helicopter Engine Market, Market Forecast, 2025-2035

- Figure 20: Netherlands, Defense Helicopter Engine Market, Technology Maturation, 2025-2035

- Figure 21: Netherlands, Defense Helicopter Engine Market, Market Forecast, 2025-2035

- Figure 22: Belgium, Defense Helicopter Engine Market, Technology Maturation, 2025-2035

- Figure 23: Belgium, Defense Helicopter Engine Market, Market Forecast, 2025-2035

- Figure 24: Spain, Defense Helicopter Engine Market, Technology Maturation, 2025-2035

- Figure 25: Spain, Defense Helicopter Engine Market, Market Forecast, 2025-2035

- Figure 26: Sweden, Defense Helicopter Engine Market, Technology Maturation, 2025-2035

- Figure 27: Sweden, Defense Helicopter Engine Market, Market Forecast, 2025-2035

- Figure 28: Brazil, Defense Helicopter Engine Market, Technology Maturation, 2025-2035

- Figure 29: Brazil, Defense Helicopter Engine Market, Market Forecast, 2025-2035

- Figure 30: Australia, Defense Helicopter Engine Market, Technology Maturation, 2025-2035

- Figure 31: Australia, Defense Helicopter Engine Market, Market Forecast, 2025-2035

- Figure 32: India, Defense Helicopter Engine Market, Technology Maturation, 2025-2035

- Figure 33: India, Defense Helicopter Engine Market, Market Forecast, 2025-2035

- Figure 34: China, Defense Helicopter Engine Market, Technology Maturation, 2025-2035

- Figure 35: China, Defense Helicopter Engine Market, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, Defense Helicopter Engine Market, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, Defense Helicopter Engine Market, Market Forecast, 2025-2035

- Figure 38: South Korea, Defense Helicopter Engine Market, Technology Maturation, 2025-2035

- Figure 39: South Korea, Defense Helicopter Engine Market, Market Forecast, 2025-2035

- Figure 40: Japan, Defense Helicopter Engine Market, Technology Maturation, 2025-2035

- Figure 41: Japan, Defense Helicopter Engine Market, Market Forecast, 2025-2035

- Figure 42: Malaysia, Defense Helicopter Engine Market, Technology Maturation, 2025-2035

- Figure 43: Malaysia, Defense Helicopter Engine Market, Market Forecast, 2025-2035

- Figure 44: Singapore, Defense Helicopter Engine Market, Technology Maturation, 2025-2035

- Figure 45: Singapore, Defense Helicopter Engine Market, Market Forecast, 2025-2035

- Figure 46: United Kingdom, Defense Helicopter Engine Market, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, Defense Helicopter Engine Market, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, Defense Helicopter Engine Market, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, Defense Helicopter Engine Market, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, Defense Helicopter Engine Market, By Platform (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, Defense Helicopter Engine Market, By Platform (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, Defense Helicopter Engine Market, By Thrust (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, Defense Helicopter Engine Market, By Thrust (CAGR), 2025-2035

- Figure 54: Scenario Analysis, Defense Helicopter Engine Market, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, Defense Helicopter Engine Market, Global Market, 2025-2035

- Figure 56: Scenario 1, Defense Helicopter Engine Market, Total Market, 2025-2035

- Figure 57: Scenario 1, Defense Helicopter Engine Market, By Region, 2025-2035

- Figure 58: Scenario 1, Defense Helicopter Engine Market, By Platform, 2025-2035

- Figure 59: Scenario 1, Defense Helicopter Engine Market, By Thrust, 2025-2035

- Figure 60: Scenario 2, Defense Helicopter Engine Market, Total Market, 2025-2035

- Figure 61: Scenario 2, Defense Helicopter Engine Market, By Region, 2025-2035

- Figure 62: Scenario 2, Defense Helicopter Engine Market, By Platform, 2025-2035

- Figure 63: Scenario 2, Defense Helicopter Engine Market, By Thrust, 2025-2035

- Figure 64: Company Benchmark, Defense Helicopter Engine Market, 2025-2035

The Global defense helicopter engine market is estimated at USD 4.75 billion in 2025, projected to grow to USD 9.35 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 7.01% over the forecast period 2024-2034.

Introduction to Defense Helicopter Engine Market:

The global defense helicopter engine market is a crucial component of military aviation, supporting a wide range of rotorcraft used for combat, reconnaissance, transport, and search-and-rescue missions. Helicopters play an indispensable role in modern warfare, offering versatility in both offensive and defensive operations. Military forces worldwide rely on these aircraft for their ability to operate in challenging environments, including mountainous regions, dense forests, and urban warfare zones. The engines that power these helicopters must deliver high performance, durability, and efficiency while meeting the stringent demands of military operations. With ongoing defense modernization efforts, increasing geopolitical tensions, and a growing emphasis on multi-role capabilities, demand for advanced helicopter engines is rising globally. Leading defense contractors and engine manufacturers are investing in cutting-edge propulsion technologies to enhance operational effectiveness, fuel efficiency, and maintenance reliability.

Technology Impact in Defense Helicopter Engine Market:

Technology is driving significant advancements in the defense helicopter engine market, with innovations focusing on power-to-weight ratio improvements, fuel efficiency, and extended operational lifespans. One of the most notable breakthroughs is the development of more efficient turboshaft engines, which provide superior power output while reducing overall weight. The use of advanced materials, such as ceramic matrix composites (CMCs) and lightweight alloys, has significantly improved engine heat resistance and durability, allowing helicopters to operate at higher temperatures and altitudes with greater reliability. Digital engine control systems, including Full Authority Digital Engine Control (FADEC), have enhanced engine performance by optimizing fuel consumption, reducing pilot workload, and improving maintenance diagnostics. These smart engine management systems provide real-time monitoring and predictive maintenance capabilities, minimizing downtime and ensuring mission readiness. The integration of hybrid-electric propulsion is another emerging trend, with research underway to develop hybrid-electric helicopters that offer reduced fuel consumption and lower acoustic signatures, making them ideal for stealth operations. Advances in additive manufacturing, or 3D printing, have also transformed the production of complex engine components, reducing lead times and enabling the rapid prototyping of new designs.

Key Drivers in Defense Helicopter Engine Market:

Key drivers fueling the growth of the defense helicopter engine market include increasing military procurement programs, the demand for fleet modernization, and the need for enhanced operational capabilities. Many countries are replacing aging helicopter fleets with modern rotorcraft that feature advanced engines capable of delivering greater speed, payload capacity, and fuel efficiency. The push for multi-role helicopters, which can transition seamlessly between combat, transport, and medical evacuation missions, has led to a rising demand for adaptable and high-performance engines. Additionally, the growing importance of vertical lift capabilities in contested environments has intensified investments in next-generation rotorcraft and propulsion systems. The emergence of Future Vertical Lift (FVL) programs, particularly in the United States, is a major driver shaping the market. These initiatives aim to develop high-speed, long-range military helicopters with state-of-the-art engines that offer superior endurance and survivability. Increased defense budgets across key military powers, including the U.S., China, and European nations, are further accelerating investments in new helicopter engines. Another critical factor is the need for improved fuel efficiency and sustainability, as defense forces seek to reduce logistical challenges and operational costs associated with fuel consumption in prolonged deployments.

Regional Trends in Defense Helicopter Engine Market:

Regional trends in the defense helicopter engine market reflect varying military priorities, technological capabilities, and procurement strategies. North America remains the dominant player, with the United States leading in both innovation and procurement. The U.S. military operates one of the largest helicopter fleets in the world, including models such as the UH-60 Black Hawk, AH-64 Apache, CH-47 Chinook, and the V-22 Osprey. Programs like the Future Long-Range Assault Aircraft (FLRAA) and the Future Attack Reconnaissance Aircraft (FARA) under the FVL initiative are driving demand for next-generation engines with increased power, range, and efficiency. Leading engine manufacturers, including General Electric Aviation, Honeywell, and Rolls-Royce North America, are at the forefront of developing new propulsion technologies to support these advanced rotorcraft. Canada, while operating a smaller military helicopter fleet, continues to invest in engine upgrades and maintenance programs to enhance the performance of its existing aircraft.

In Europe, the defense helicopter engine market is shaped by collaborative programs and national defense strategies. France, Germany, Italy, and the United Kingdom are key players, with companies such as Safran Helicopter Engines, Rolls-Royce, and MTU Aero Engines leading innovation in the region. European nations continue to modernize their helicopter fleets, focusing on platforms such as the NH90, Tiger attack helicopter, and AW101 Merlin. The European Defence Fund and multinational projects support research into more efficient and powerful helicopter engines, ensuring that European forces maintain cutting-edge vertical lift capabilities. The increasing focus on indigenous engine development and reduced reliance on foreign suppliers has led to joint ventures and technology-sharing agreements among European defense contractors.

Key Defense Helicopter Engine Program:

SAFHAL, a joint venture between Safran Helicopter Engines SAS and Hindustan Aeronautics Limited, is dedicated to the design, development, production, sales, and support of next-generation helicopter engines in India. This initiative marks a major milestone in the country's aerospace and defense sector, reinforcing India's commitment to Aatmanirbharta in helicopter engine technology. Under this strategic agreement, SAFHAL will collaborate with its parent companies to develop cutting-edge engine technologies, ensuring exceptional performance, reliability, and operational efficiency. The partnership will focus on advanced design, state-of-the-art manufacturing processes, and rigorous testing protocols, adhering to the highest global standards.

European engine giants MTU Aero Engines and Safran Helicopter Engines have taken a significant step forward in their efforts to develop and produce a powerplant for a future European military helicopter with the establishment of a joint venture. The companies announced the signing of a cooperation agreement to create EURA (European Military Rotorcraft Engine Alliance), a 50-50 partnership aimed at advancing military rotorcraft engine technology. EURA will be led by an MTU executive and will be based alongside Safran Helicopter Engines' headquarters in Bordes, France. This development follows an initial agreement signed a year ago to formalize the collaboration.

Table of Contents

Defense Helicopter Engines Market Report Definition

Defense Helicopter Engines Market Segmentation

By Platform

By Thrust

By Region

Defense Helicopter Engines Market Analysis for next 10 Years

The 10-year defense helicopter engines market analysis would give a detailed overview of defense helicopter engines market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Helicopter Engines Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Helicopter Engines Market Forecast

The 10-year defense helicopter engines market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Helicopter Engines Market Trends & Forecast

The regional defense helicopter engines market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Helicopter Engines Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Helicopter Engines Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Helicopter Engines Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports