|

市場調査レポート

商品コード

1904992

防衛用オプトロニクスの世界市場(2026年~2036年)Global Defense Optronics Market 2026-2036 |

||||||

|

|||||||

| 防衛用オプトロニクスの世界市場(2026年~2036年) |

|

出版日: 2026年01月10日

発行: Aviation & Defense Market Reports (A&D)

ページ情報: 英文 150+ Pages

納期: 3営業日

|

概要

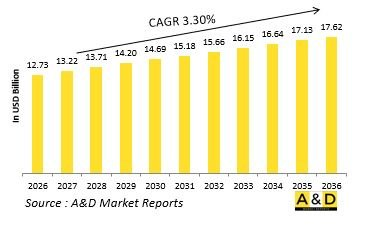

世界の防衛用オプトロニクスの市場規模は、2026年に推定127億3,000万米ドルであり、2036年までに176億2,000万米ドルに達すると予測され、2026年~2036年の予測期間にCAGRで3.30%の成長が見込まれます。

防衛用オプトロニクス市場のイントロダクション

世界の防衛用オプトロニクス市場は、監視、標的捕捉、ナビゲーション、脅威検知を目的として、人間の視覚能力を電磁スペクトル全体に拡張する電気光学的な赤外線システムを包含しています。これらのシステムは、光子を処理、表示、分析可能な電子信号に変換し、暗闇、視界不良、長距離における重要な能力を提供します。オプトロニクス部品には、サーマルイメージャー、増感器、レーザー測距儀、目標指示器、ハイパースペクトルセンサーなどが含まれ、個人用兵士照準器から衛星監視システムに至るまで、あらゆる軍事領域に展開されています。この技術により、発見されることなく視認し、精密に目標を捕捉し、視認環境が劣化した状況下でもナビゲーションすることが可能となります。戦争が24時間体制の作戦や視覚的観測が制限される環境へと拡大する中、オプトロニクスは戦術・作戦・戦略レベルにおける状況認識と交戦力学を根本的に変革する、戦力を増強する存在となっています。

防衛用オプトロニクス市場における技術の影響

オプトロニクスの技術的進歩は、センサーフュージョン、解像度向上、認知処理に焦点を当てています。より小さな画素ピッチを備えた高精細サーマルセンサーは、システムのサイズと電力要件を低減しつつ、長距離での鮮明な画像を提供します。マルチスペクトル/ハイパースペクトルイメージングは、多数のスペクトル帯域にわたる情報を統合し、カモフラージュされた物体の検出や材料の特定を可能にします。先進の画像処理アルゴリズムはAIを活用し、目標の自動検知・分類・追跡を実現すると同時に、操作者の負荷を軽減します。熱画像、低照度画像、レーザーデータを単一の統合ディスプレイに融合することで、包括的な状況把握が可能となります。量子ベースのセンシング技術は、感度と識別能力において画期的な向上をもたらすと期待されています。小型化は無人システムや個人用兵器を含む小型プラットフォームへの展開を推進し続けています。これらの革新により、オプトロニクスは単なる視覚補助ツールから、戦場の重要情報を自動的に抽出・優先順位付けするインテリジェントセンシングシステムへと変化しています。

防衛用オプトロニクス市場の主な促進要因

あらゆる環境下での24時間365日の作戦能力の必要性が、オプトロニクスの継続的強化を推進しています。夜間や悪天候が戦術的休息をもたらさなくなったためです。隠蔽・欺瞞戦術を用いる敵に対する非対称戦争が、先進の探知・識別能力への需要を高めています。プラットフォームの生存性要件は、先制的な対抗を可能にする、より長い距離での早期脅威探知を強く求めます。精密攻撃の要請により、視認条件にかかわらず高精度な標的データが必須となります。世界各国の兵士近代化プログラムでは、分隊レベルの状況認識能力と射撃精度を向上させるため、個人用オプトロニクスを優先付けています。さらに、対ドローン作戦や周辺警備作戦では、ネットワーク化されたオプトロニクスアレイを用いた広域持続監視の新たな要件が生じています。これらの促進要因が組み合わさり、防衛近代化サイクル全体を通じて、あらゆるオプトロニクスカテゴリとプラットフォームタイプへの持続的な投資が保証されています。

防衛用オプトロニクス市場の地域的な動向

各地域のオプトロニクス開発は、脅威認識、産業能力、作戦教義の違いを反映しています。北米のプログラムは、デジタル化された戦域への統合を目的とした先進の処理能力とネットワーク機能を備えたマルチスペクトルシステムを重視しています。欧州の開発は、次世代装甲車両や航空機向けの高性能サーマルイメージャーと照準システムに焦点を当てています。アジア太平洋では、特に歩兵部隊への広範な展開を目的とした非冷却式サーマル技術において、自国生産の著しい成長が見られます。中東の調達では、極端な温度差と長距離観測を要する砂漠環境向けに最適化されたシステムが優先されています。イスラエルの産業は、継続的な実戦経験を通じて洗練された革新的なオプトロニクスソリューションにおいて特に強力です。発展途上国では、大規模なプラットフォーム調達の一環として技術移転契約を通じて高性能オプトロニクスへのアクセスが増加していますが、先進のシステムの維持管理と持続性において課題に直面することが多い状況です。

当レポートでは、世界の防衛用オプトロニクス市場について調査分析し、市場に影響を与える技術、今後10年間の予測、各地域の市場動向などの情報を提供しています。

目次

防衛用オプトロニクス市場レポートの定義

防衛用オプトロニクス市場のセグメンテーション

地域別

技術別

プラットフォーム別

今後10年間の防衛用オプトロニクス市場の分析

防衛用オプトロニクス市場の技術

世界の防衛用オプトロニクス市場の予測

地域の防衛用オプトロニクス市場の動向と予測

北米

促進要因、抑制要因、課題

PEST

市場予測とシナリオ分析

主要企業

サプライヤーのTierの状況

企業ベンチマーク

欧州

中東

アジア太平洋

南米

防衛用オプトロニクス市場の国の分析

米国

防衛プログラム

最新ニュース

特許

この市場における現在の技術成熟度

市場予測とシナリオ分析

カナダ

イタリア

フランス

ドイツ

オランダ

ベルギー

スペイン

スウェーデン

ギリシャ

オーストラリア

南アフリカ

インド

中国

ロシア

韓国

日本

マレーシア

シンガポール

ブラジル