|

|

市場調査レポート

商品コード

1421553

HVACメンテナンス・サービスの世界市場:展望・予測(2024年~2029年)HVAC Maintenance and Services Market - Global Outlook & Forecast 2024-2029 |

||||||

|

|||||||

|

|||||||

| HVACメンテナンス・サービスの世界市場:展望・予測(2024年~2029年) |

|

出版日: 2024年02月06日

発行: Arizton Advisory & Intelligence

ページ情報: 英文 348 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

世界のHVACメンテナンス・サービスの市場規模は、2023年~2029年にCAGRで5.79%の成長が予測されます。

市場の動向と促進要因

可処分所得の増加

世界の人々の大半の高い可処分所得は、高い識字率と就業率によるものです。そのため、市場で入手可能なプレミアムでスマートな製品に対する消費者の志向が高まっています。割高な価格設定にもかかわらず、米国などの先進国では、住宅および商業部門におけるプール建設の需要が高まっています。建設需要の急増は、HVACメンテナンス・サービスの需要を促進すると思われます。世界的にプール用ヒートポンプの需要がかなり高いのは、勤労者の可処分所得が大幅に増加しているためです。

有利な政府政策とインセンティブ

再生可能エネルギー源の使用を支援し、大気中への温室効果ガスの排出を防止する各国の有利な政府政策は、最終的にHVACメンテナンスとサービス市場を牽引しています。例えば、中国政府は全国的にヒートポンプの利用促進に努めています。特に石炭火による暖房が盛んな地域では、総単価の90%までカバーできる設置補助金を提供しています。また、同国は持続可能なアプローチも試みており、環境への有害ガスの排出を削減することをより重要視しています。China Heat Pump Alliance(CHPA)は、同国のHVAC市場の標準化団体です。

業界の抑制要因

高い設置費用と初期費用

環境への持続可能な寄与というHVACの利点にもかかわらず、高い初期費用と先行費用が普及の妨げとなっています。このような要因は、特に経済が成長し価格に敏感なアジア太平洋やラテンアメリカの市場では、コストが購入に大きな影響を与える要因となっており、HVACメンテナンス・サービス市場にとって大きな課題となり得ます。推定によると、プールの配管を伴うHVACの平均設置費用は3,600~6,500米ドルで、人件費は500~1,000米ドルです。これらの価格は、主なターゲットセグメントを形成する中間所得層の消費者にとってはかなり高額であることが多いです。従来のガスヒーターやソーラーヒーターと比較すると、HVACは長期にわたって運用コストが低いという証拠がありますが、高い設置コストが市場ベンダーにとって負担となっています。

地域の分析

2023年の世界のHVACメンテナンス・サービス市場では、アジア太平洋がもっとも大きなシェアを占めています。エネルギー効率の高いHVACシステムに対する需要の高まりと、防爆HVAC機器の使用に対する厳しい規制がアジア太平洋で拡大しています。また、業界全体でクリーンルームの採用が進み、巨大な成長機会がもたらされます。さらに、アジア太平洋では自然災害の頻度が高い状態が続くと予測されています。沿岸都市への人口移転に伴い、特定の無秩序な都市化プロセスがアジア太平洋諸国の脆弱な気候変動リスクにつながる主因となっています。したがって、気候条件の変動が、予測期間にアジア太平洋諸国におけるHVACメンテナンス・サービスの動的性質の需要を促進します。

競合情勢

Systemair Manufacturing、Johnson Controls、Zehnder、OstbergといったHVACメンテナンス・サービス市場のグローバル企業は、収益性の高いパートナーシップや合併戦略を通じて市場拡大を図っています。対照的に、HVACメンテナンス・サービス産業の国内ベンダーは、国内のニーズや欲求にもっとも適した製品ポートフォリオを活用しています。しかし、技術指向の製品であるため、エネルギー効率、COP、環境にやさしい冷媒、設置コスト、地域気候、サービス分析など、先進の機能の精巧さと展開が差別化の範囲となり、それによって競合環境から逃れることができます。エンジニアリングと技術的特徴の近年の進歩に伴い、HVAC産業の変化する力学は、一般用途向けの非常に効果的な暖房機器を要求しています。

当レポートでは、世界のHVACメンテナンス・サービス市場について調査分析し、市場規模と予測、機会と動向、主要企業などの情報を提供しています。

目次

第1章 調査対象・調査範囲

- 市場の定義

- 対象となるセグメントと定義

- 市場の導出

第2章 重要考察

- 機会ポケット

- 概要

- 促進要因

- 市場:エンドユーザー別

- 市場:機器別

- 市場:サービスモデル別

- 競合情勢

- 主要ベンダーの成長戦略

第3章 市場の概要

第4章 イントロダクション

- 概要

- コスト分析

- HVACシステムに関する重要考察

- 合併・買収と製品開発

- HVACシステムを促進する政府の規制

- 概要

- REPowerEU計画によるHVAC市場への寄与

- REPowerEU計画の利点

- 暖房機器に対するIRAの利点

- 主な競合ハイライト

- 世界経済シナリオ

- 地域経済

- ロシア・ウクライナ戦争:世界の影響

- HVACシステムとサービスの需要に関する重要考察

- 商業スペースからの需要

- コワーキングスペースにおけるHVACシステムとサービスの需要の増加

- 世界の建設部門の主なハイライト

第5章 市場の機会と動向

- 交換を支援するIoTと製品のイノベーションの到来

- 既存機器のエネルギー効率の高い機器への置き換え

- 可処分所得の増加

第6章 市場成長の実現要因

- 商業建設とプロジェクトの増加

- 政府の有利な政策と奨励金

- 暖房機器における低GWP冷媒ソリューションの需要

第7章 市場抑制要因

- 高い設置費用と初期費用

- 熟練労働者の不足

- 厳しい規制

- 激動する世界の政治、貿易関係

第8章 市場情勢

- 市場の概要

- 市場規模と予測

- ファイブフォース分析

第9章 装備

- 市場のスナップショットと成長促進要因

- 市場の概要

- 重要考察

- 暖房

- 市場の概要

- ヒートポンプ

- ボイラーユニット

- 炉

- 市場規模と予測

- 市場:地域別

- 空調

- 市場の概要

- RAC

- CAC

- チラー

- 熱交換器

- 重要事項

- 市場規模と予測

- 市場:地域別

- 換気

- 市場の概要

- 換気機器の市場力学

- エアハンドリングユニット(AHU)

- エアフィルター

- 加湿器・除湿器

- ファンコイルユニット

- 市場規模と予測

- 市場:地域別

第10章 サービスモデル

- 市場のスナップショットと成長促進要因

- 市場の概要

- HVACサービスの種類

- メンテナンス・修理

- 市場の概要

- HVACのメンテナンスと修理に関する主なハイライト

- 市場規模と予測

- 市場:地域別

- 設置

- 市場の概要

- 市場規模と予測

- 市場:地域別

- 交換

- 市場の概要

- 市場規模と予測

- 市場:地域別

- コンサルティング

- 市場の概要

- 市場規模と予測

- 市場:地域別

第11章 エンドユーザー

- 市場のスナップショットと成長促進要因

- 市場の概要

- 住宅

- 市場の概要

- 市場規模と予測

- 市場:地域別

- 商業

- 市場の概要

- ホテル、リゾート

- オフィススペース

- コワーキングスペースに関する重要考察

- 空港・公共施設

- ホスピタリティ

- 病院

- 教育機関

- 市場規模と予測

- 市場:地域別

- その他

- 市場の概要

- 市場規模と予測

- 市場:地域別

第12章 地域

- 市場のスナップショットと成長促進要因

- 地理的な概要

- 地域の分析

第13章 アジア太平洋

- 市場の概要

- 市場規模と予測

- サービスモデル

- 市場規模と予測

- 機器

- 市場規模と予測

- エンドユーザー

- 市場規模と予測

- 主要国

- 中国の市場規模と予測

- 日本の市場規模と予測

- インドの市場規模と予測

- オーストラリアの市場規模と予測

- 韓国の市場規模と予測

第14章 欧州

- 市場の概要

- 市場規模と予測

- サービスモデル

- 市場規模と予測

- 機器

- 市場規模と予測

- エンドユーザー

- 市場規模と予測

- 主要国

- ドイツの市場規模と予測

- フランスの市場規模と予測

- ロシアの市場規模と予測

- 英国の市場規模と予測

- ノルウェーの市場規模と予測

- デンマークの市場規模と予測

- イタリアの市場規模と予測

- ポーランドの市場規模と予測

- スペインの市場規模と予測

第15章 北米

- 市場の概要

- 市場規模と予測

- サービスモデル

- 市場規模と予測

- 機器

- 市場規模と予測

- エンドユーザー

- 市場規模と予測

- 主要国

- 米国の市場規模と予測

- カナダの市場規模と予測

第16章 ラテンアメリカ

- 市場の概要

- 市場規模と予測

- サービスモデル

- 市場規模と予測

- 機器

- 市場規模と予測

- エンドユーザー

- 市場規模と予測

- 主要国

- ブラジルの市場規模と予測

- メキシコの市場規模と予測

- アルゼンチンの市場規模と予測

第17章 中東・アフリカ

- 市場の概要

- 市場規模と予測

- サービスモデル

- 市場規模と予測

- 機器

- 市場規模と予測

- エンドユーザー

- 市場規模と予測

- 主要国

- サウジアラビアの市場規模と予測

- アラブ首長国連邦の市場規模と予測

- 南アフリカの市場規模と予測

第18章 競合情勢

- 競合の概要

- 主要ベンダーの成長戦略

- 主なコンピテンシー

- 世界の規範と規制の力学

第19章 主要企業プロファイル

- ALDES

- AQUACAL

- DAIKIN

- JOHNSON CONTROLS

- MITSUBISHI ELECTRIC

- OSTBERG

- PENTAIR

- ROBERT BOSCH

- RHEEM MANUFACTURING COMPANY

- SAMSUNG

- SIEMENS AG

- SYSTEMAIR

- ZEHNDER

第20章 その他の著名なベンダー

- CARRIER

- HONEYWELL INTERNATIONAL INC

- LG

- PANASONIC

- MIDEA

- REGAL

- RAYTHEON TECHNOLOGIES

- FLAKT GROUP

- SWEGON

- VTS GROUP

- NUAIRE

- NORTEK

- ALFA LAVAL

- HITACHI

- LU-VE

- VENT-AXIA

- ROSENBERG

- S & P

- WOLF

- CIAT

- AL-KO GROUP

- DYNAIR

- DANFOSS

- LENNOX

- BACKER SPRINGFIELD

- DUNHAMBUSH

- TCL

- TROX

- VAILLANT GROUP

- INGERSOLL RAND

- CAMFIL

第21章 レポートのサマリー

- 重要事項

- 戦略的な推奨事項

第22章 量的サマリー

- 市場:地域別

- サービスモデル:市場規模と予測

- 機器:市場規模と予測

- エンドユーザー:市場規模と予測

第23章 付録

List Of Exhibits

LIST OF EXHIBITS

- EXHIBIT 1 MARKET SIZE CALCULATION APPROACH 2023

- EXHIBIT 2 HVAC MAINTENANCE & SERVICE COSTS ($) (2023)

- EXHIBIT 3 TYPE OF HVAC UNIT COSTS (2023)

- EXHIBIT 4 SEVERAL ADVANTAGES OF PROPER HVAC INSTALLATIONS

- EXHIBIT 5 POLICY FRAMEWORK FOR ENERGY EFFICIENCY HVAC SYSTEMS

- EXHIBIT 6 KEY BENEFITS OF REPOWEREU PLAN

- EXHIBIT 7 GLOBAL GDP GROWTH 2019-2024 (%)

- EXHIBIT 8 MARKET EFFECTS OF RUSSIA-UKRAINE CONFLICT

- EXHIBIT 9 INSIGHTS FOR HOTEL CONSTRUCTION WORLDWIDE 2023

- EXHIBIT 10 GLOBAL GROWTH IN COWORKING SPACES 2018-2024 (THOUSAND UNITS)

- EXHIBIT 11 IMPACT OF EMERGENCE OF IOT AND PRODUCT INNOVATIONS TO AID REPLACEMENTS

- EXHIBIT 12 SOME MODERN TECHNOLOGY OF IOT FOR HVAC SYSTEMS

- EXHIBIT 13 BENEFITS OF SMART IOT SYSTEMS

- EXHIBIT 14 IMPACT OF REPLACEMENT OF EXISTING EQUIPMENT WITH ENERGY-EFFICIENT ONES

- EXHIBIT 15 ENVIRONMENTAL POLLUTION CAUSED BY TRADITIONAL HVAC SYSTEMS

- EXHIBIT 16 ADVANCED ENERGY-EFFICIENT HVAC TECHNOLOGIES

- EXHIBIT 17 IMPACT OF RISE IN DISPOSABLE INCOME

- EXHIBIT 18 HOME OWNERSHIP IN US Q4 2018-Q4 2022 (%)

- EXHIBIT 19 IMPACT OF RISE IN COMMERCIAL CONSTRUCTION AND PROJECTS

- EXHIBIT 20 UPCOMING GLOBAL RAILWAY INFRASTRUCTURE PROJECTS 2023-2024 ($ BILLION)

- EXHIBIT 21 FIVE LARGEST DATA CENTER CONSTRUCTION PROJECTS INITIATED 2022-2024 ($ MILLION)

- EXHIBIT 22 IMPACT OF FAVORABLE GOVERNMENT POLICIES AND INCENTIVES

- EXHIBIT 23 IMPACT OF DEMAND FOR LOW GWP REFRIGERANT SOLUTIONS IN HEATING EQUIPMENT

- EXHIBIT 24 IMPACT OF HIGH INSTALLATION AND UPFRONT COSTS

- EXHIBIT 25 IMPACT OF LACK OF SKILLED LABOR

- EXHIBIT 26 LABOR BENEFITS MEASURES TAKEN BY VARIOUS AGENCIES AND ORGANIZATIONS

- EXHIBIT 27 IMPACT OF STRINGENT REGULATIONS

- EXHIBIT 28 GOVERNMENT PLAN FOR ENERGY CONSUMPTION REDUCTION

- EXHIBIT 29 IMPACT OF TURBULENT GLOBAL POLITICAL AND TRADE RELATIONS

- EXHIBIT 30 GROWTH STRATEGIES FOR VENDORS IN GLOBAL HVAC MARKET

- EXHIBIT 31 WORLDWIDE ENERGY CONSUMPTION RATE OF BUILDING SECTOR, 2022

- EXHIBIT 32 FACTORS INFLUENCING PREFERENCE FOR HVAC SYSTEMS

- EXHIBIT 33 GLOBAL HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 34 FIVE FORCES ANALYSIS 2023

- EXHIBIT 35 INCREMENTAL GROWTH BY EQUIPMENT 2023 & 2029

- EXHIBIT 36 GLOBAL HEAT PUMP SALES IN 2022 (% SHARE)

- EXHIBIT 37 KEY FACTORS FAVORING DEMAND FOR HEAT PUMPS

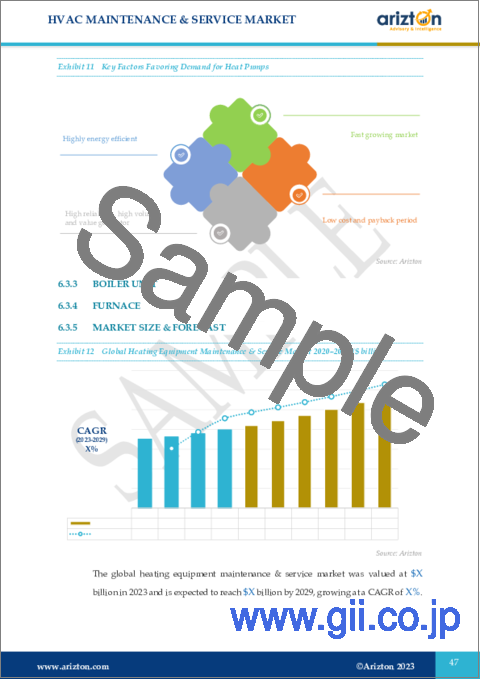

- EXHIBIT 38 GLOBAL HEATING EQUIPMENT MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 39 APPLICATION OF CHILLERS IN COMMERCIAL SECTOR

- EXHIBIT 40 VARIOUS TYPES OF HEAT EXCHANGERS

- EXHIBIT 41 FACTOR DRIVING HEAT EXCHANGER MARKET

- EXHIBIT 42 GLOBAL AIR CONDITIONING MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 43 GLOBAL VENTILATION EQUIPMENT MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 44 INCREMENTAL GROWTH BY SERVICE MODEL 2023 & 2029

- EXHIBIT 45 REVENUE AND INCREMENTAL GROWTH OF SERVICE MODEL SEGMENT

- EXHIBIT 46 THREE APPROACHES FOR HVAC PREVENTIVE MAINTENANCE

- EXHIBIT 47 ADVANTAGES OF HVAC MAINTENANCE

- EXHIBIT 48 GLOBAL HVAC MAINTENANCE & REPAIR MARKET 2020-2029 ($ BILLION)

- EXHIBIT 49 GLOBAL HVAC INSTALLATION MARKET 2020-2029 ($ BILLION)

- EXHIBIT 50 ADVANTAGES OF HVAC INSTALLATIONS

- EXHIBIT 51 AVERAGE COST FOR REPLACING AN HVAC SYSTEM

- EXHIBIT 52 GLOBAL HVAC REPLACEMENT MARKET 2020-2029 ($ BILLION)

- EXHIBIT 53 ADVANTAGES OF HVAC SYSTEM REPLACEMENT

- EXHIBIT 54 ADDITIONAL BENEFITS OF WORKING WITH HVAC CONSULTANTS

- EXHIBIT 55 GLOBAL HVAC CONSULTING MARKET 2020-2029 ($ BILLION)

- EXHIBIT 56 INCREMENTAL GROWTH BY END-USER 2023 & 2029

- EXHIBIT 57 GLOBAL RESIDENTIAL HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 58 IDEAL RECOMMENDATIONS FOR COMMERCIAL HEATING EQUIPMENT

- EXHIBIT 59 INSIGHTS FOR GLOBAL HOTEL CONSTRUCTION (2022)

- EXHIBIT 60 GLOBAL COMMERCIAL HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 61 GLOBAL OTHERS HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 62 INCREMENTAL GROWTH BY GEOGRAPHY 2023 & 2029

- EXHIBIT 63 GLOBAL HVAC MAINTENANCE & SERVICE MARKET: REVENUE AND INCREMENTAL GROWTH BY GEOGRAPHY ($ BILLION)

- EXHIBIT 64 APAC HVAC MAINTENANCE & SERVICE MARKET: REVENUE AND INCREMENTAL GROWTH 2023 ($ BILLION)

- EXHIBIT 65 ADVENT OF ENVIRONMENTAL REGULATIONS IN APAC

- EXHIBIT 66 REASONS FOR LOW ADOPTION OF COMMERCIAL HEATING EQUIPMENT IN JAPAN

- EXHIBIT 67 APAC HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 68 INCREMENTAL GROWTH IN APAC 2023 & 2029

- EXHIBIT 69 CHINA HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 70 RESIDENTIAL & NON-RESIDENTIAL CONSTRUCTION OUTPUT OF JAPAN (2020-2022) (% CHANGE YOY)

- EXHIBIT 71 ENERGY BILL SAVINGS FOR HOUSEHOLDS SWITCHING TO HEAT PUMPS FROM GAS BOILERS ($)

- EXHIBIT 72 JAPAN HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 73 LARGEST CONSTRUCTION PROJECTS INITIATED IN INDIA 2022-2026

- EXHIBIT 74 INDIA HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 75 OFFICE BUILDING CONSTRUCTION PROJECTS 2022-2025

- EXHIBIT 76 AUSTRALIA HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 77 ENERGY BILL SAVINGS FOR HOUSEHOLDS SWITCHING TO HEAT PUMPS FROM GAS BOILERS ($)

- EXHIBIT 78 SOUTH KOREA HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 79 HEAT PUMP SALES IN EUROPEAN COUNTRIES, 2021 (THOUSAND UNITS)

- EXHIBIT 80 ENERGY BILL SAVINGS FOR HOUSEHOLDS SWITCHING TO HEAT PUMPS FROM GAS BOILERS ($)

- EXHIBIT 81 EUROPE HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 82 INCREMENTAL GROWTH IN EUROPE 2023 & 2029

- EXHIBIT 83 GERMANY HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 84 FRANCE HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 85 FIVE LARGEST HIGH-RISE APARTMENT PROJECTS IN RUSSIA 2022-2024 ($ MILLION)

- EXHIBIT 86 RUSSIA HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 87 UK HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 88 NORWAY HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 89 DENMARK HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 90 ITALY HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 91 POLAND HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 92 SPAIN HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 93 FIVE LARGEST LEISURE & HOSPITALITY BUILDING CONSTRUCTION PROJECTS IN NORTH AMERICA 2022

- EXHIBIT 94 NORTH AMERICA HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 95 INCREMENTAL GROWTH IN NORTH AMERICA 2023 & 2029

- EXHIBIT 96 ENERGY BILL SAVINGS FOR HOUSEHOLDS SWITCHING TO HEAT PUMPS FROM GAS BOILERS ($)

- EXHIBIT 97 US HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 98 INVESTMENTS IN NON-RESIDENTIAL BUILDING CONSTRUCTION, JUNE 2022 ($ MILLION)

- EXHIBIT 99 NUMBER OF HVAC SYSTEM CONTRACTS ESTABLISHED IN CANADA IN 2022

- EXHIBIT 100 CANADA HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 101 VALUE OF CONSTRUCTION INDUSTRY IN LATIN AMERICA 2022 ($ BILLION)

- EXHIBIT 102 LATIN AMERICA HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 103 INCREMENTAL GROWTH IN LATIN AMERICA 2023 & 2029

- EXHIBIT 104 BRAZIL HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 105 MEXICO HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 106 ARGENTINIAN GOVERNMENT CONSTRUCTION & DEVELOPMENT PROJECTS 2022-2024

- EXHIBIT 107 ARGENTINA HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 108 MIDDLE EAST & AFRICA HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 109 INCREMENTAL GROWTH IN MIDDLE EAST & AFRICA 2023 & 2029

- EXHIBIT 110 AVIATION CONSTRUCTION PROJECTS IN SAUDI ARABIA 2022-2035

- EXHIBIT 111 SAUDI ARABIA HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 112 UAE HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 113 SOUTH AFRICA HVAC MAINTENANCE & SERVICE MARKET 2020-2029 ($ BILLION)

- EXHIBIT 114 INSIGHTS FOR MAJOR HVAC SERVICE PROVIDING COMPANY

- EXHIBIT 115 CRITERIA FOR SUCCESS IN HVAC MARKET

- EXHIBIT 116 BRAND PORTFOLIO OF JOHNSON CONTROLS

- EXHIBIT 117 KEY CAVEATS

List Of Tables

LIST OF TABLES

- TABLE 1 PRICE RANGE OF HVAC REPAIR AND MAINTENANCE SERVICES IN 2023

- TABLE 2 REBATE AMOUNTS FOR APPLIANCES UNDER HEEHRA

- TABLE 3 COMPETITIVE OVERVIEW OF GLOBAL HVAC MAINTENANCE & SERVICE MARKET

- TABLE 4 COST OF HEATING EQUIPMENT 2022

- TABLE 5 INSTALLATION COST OF HEAT PUMP TECHNOLOGY

- TABLE 6 INSTALLATION COST OF BOILER SYSTEM COST (USD)

- TABLE 7 GLOBAL HEATING EQUIPMENT MAINTENANCE & SERVICE MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 8 INSTALLATION COST OF AIR CONDITIONER TECHNOLOGY

- TABLE 9 GLOBAL AIR CONDITIONING MAINTENANCE & SERVICE MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 10 GLOBAL VENTILATION EQUIPMENT MAINTENANCE & SERVICE MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 11 BREAKDOWN OF AVERAGE COSTS FOR COMMON HVAC MAINTENANCE TASKS

- TABLE 12 REPAIR COSTS OF HVAC BREAKDOWN BY PARTS

- TABLE 13 GLOBAL HVAC MAINTENANCE & REPAIR MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 14 GLOBAL HVAC INSTALLATION MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 15 GLOBAL HVAC REPLACEMENT MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 16 GLOBAL HVAC CONSULTING MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 17 RESIDENTIAL CONSTRUCTION DATA IN US IN 2022

- TABLE 18 GLOBAL RESIDENTIAL HVAC MAINTENANCE & SERVICE MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 19 OFFICE BUILDING CONSTRUCTION PROJECTS 2022-2024 ($ MILLION)

- TABLE 20 FIVE LARGEST AIRPORT INFRASTRUCTURE CONSTRUCTION IN APAC 2021-2025 ($ MILLION)

- TABLE 21 FIVE LARGEST HOTEL CONSTRUCTION PROJECTS IN APAC 2022 ($ MILLION)

- TABLE 22 FIVE LARGEST HOSPITAL CONSTRUCTION PROJECTS 2022-2030 ($ MILLION)

- TABLE 23 GLOBAL COMMERCIAL HVAC MAINTENANCE & SERVICE MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 24 RETAIL BUILDING CONSTRUCTION PROJECTS IN EUROPE 2022

- TABLE 25 GLOBAL OTHERS HVAC MAINTENANCE & SERVICE MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 26 MULTI-FAMILY HOUSING CONSTRUCTION PROJECTS 2022-2024 ($ MILLION)

- TABLE 27 UPCOMING COMMERCIAL BUILDING CONSTRUCTION PROJECTS IN APAC, 2022-2025 ($ MILLION)

- TABLE 28 APAC HVAC MAINTENANCE & SERVICE MARKET BY SERVICE 2023-2029 ($ BILLION)

- TABLE 29 APAC HVAC MAINTENANCE & SERVICE MARKET BY EQUIPMENT 2023-2029 ($ BILLION)

- TABLE 30 APAC HVAC MAINTENANCE & SERVICE MARKET BY END-USER 2023-2029 ($ BILLION)

- TABLE 31 TOP FIVE LARGEST CONSTRUCTION PROJECTS INITIATED 2022-2024 ($ MILLION)

- TABLE 32 APARTMENT PROJECTS IN JAPAN 2022-2023

- TABLE 33 BUILDING APPROVALS IN AUSTRALIA IN 2022

- TABLE 34 NEW HOTELS CONSTRUCTION PROJECTS IN SOUTH KOREA 2021-2023

- TABLE 35 EUROPEAN RETAIL BUILDING CONSTRUCTION PROJECTS IN 2022

- TABLE 36 EUROPE HVAC MAINTENANCE & SERVICE MARKET BY SERVICE MODEL 2023-2029 ($ BILLION)

- TABLE 37 EUROPE HVAC MAINTENANCE & SERVICE MARKET BY EQUIPMENT 2023-2029 ($ BILLION)

- TABLE 38 EUROPE HVAC MAINTENANCE & SERVICE MARKET BY END-USER 2023-2029 ($ BILLION)

- TABLE 39 FIVE HEALTHCARE BUILDING CONSTRUCTION PROJECTS (2022)

- TABLE 40 COMPLETED & NEW CONSTRUCTION STATISTICS FOR POLAND 2022-2024

- TABLE 41 NORTH AMERICA HVAC MAINTENANCE & SERVICE MARKET BY SERVICE MODEL 2023-2029 ($ BILLION)

- TABLE 42 NORTH AMERICA HVAC MAINTENANCE & SERVICE MARKET BY EQUIPMENT 2023-2029 ($ BILLION)

- TABLE 43 NORTH AMERICA HVAC MAINTENANCE & SERVICE MARKET BY END-USER 2023-2029 ($ BILLION)

- TABLE 44 RISE IN PERCENTAGE OF POSITIONS FOR HVAC MECHANICS AND INSTALLERS IN US 2020-2030

- TABLE 45 NUMBER OF NEW OPENINGS FOR HVAC MECHANICS AND INSTALLERS IN US 2020-2030

- TABLE 46 HVAC INSTALLATION COSTS IN US (JULY 2022)

- TABLE 47 PRIVATE & GOVERNMENT OFFICE BUILDING CONSTRUCTION PROJECTS 2021-2024

- TABLE 48 KEY PROJECTIONS FOR HVAC CONTRACTOR INDUSTRY IN CANADA

- TABLE 49 LATIN AMERICA HVAC MAINTENANCE & SERVICE MARKET BY SERVICE MODEL 2023-2029 ($ BILLION)

- TABLE 50 LATIN AMERICA HVAC MAINTENANCE & SERVICE MARKET BY EQUIPMENT 2023-2029 ($ BILLION)

- TABLE 51 LATIN AMERICA HVAC MAINTENANCE & SERVICE MARKET BY END-USER 2023-2029 ($ BILLION)

- TABLE 52 MIDDLE EAST & AFRICA HVAC MAINTENANCE & SERVICE MARKET BY SERVICE MODEL 2023-2029 ($ BILLION)

- TABLE 53 MIDDLE EAST & AFRICA HVAC MAINTENANCE & SERVICE MARKET BY EQUIPMENT 2023-2029 ($ BILLION)

- TABLE 54 MIDDLE EAST & AFRICA HVAC MAINTENANCE & SERVICE MARKET BY END-USER 2023-2029 ($ BILLION)

- TABLE 55 UAE UPCOMING OIL AND REFINERY EXPANSION PROJECTS 2022-2027

- TABLE 56 LIQUEFIED NATURAL GAS (LNG) AND REFINERY OIL EXPANSION PROJECTS IN SOUTH AFRICA 2024-2028

- TABLE 57 ALDES: MAJOR PRODUCT OFFERINGS

- TABLE 58 AQUACAL: MAJOR PRODUCT OFFERINGS

- TABLE 59 DAIKIN: MAJOR PRODUCT OFFERINGS

- TABLE 60 ACQUISITIONS OF JOHNSON CONTROLS

- TABLE 61 BUSINESS SERVICE SOLUTIONS BY JOHNSON CONTROLS

- TABLE 62 JOHNSON CONTROLS: MAJOR PRODUCT OFFERINGS

- TABLE 63 MITSUBISHI ELECTRIC: MAJOR PRODUCT OFFERINGS

- TABLE 64 OSTBERG: MAJOR PRODUCT OFFERINGS

- TABLE 65 PENTAIR: MAJOR PRODUCT OFFERINGS

- TABLE 66 REGIONAL EMPLOYEES AND LOCATIONS OF ROBERT BOSCH

- TABLE 67 ROBERT BOSCH: MAJOR PRODUCT OFFERINGS

- TABLE 68 RHEEM MANUFACTURING COMPANY: MAJOR PRODUCT OFFERINGS

- TABLE 69 SAMSUNG: MAJOR PRODUCT OFFERINGS

- TABLE 70 SIEMENS AG: MAJOR PRODUCT OFFERINGS

- TABLE 71 SYSTEMAIR: MAJOR PRODUCT OFFERINGS

- TABLE 72 ZEHNDER: MAJOR PRODUCT OFFERINGS

- TABLE 73 CARRIER: MAJOR PRODUCT OFFERINGS

- TABLE 74 HONEYWELL INTERNATIONAL INC: MAJOR PRODUCT OFFERINGS

- TABLE 75 LG: MAJOR PRODUCT OFFERINGS

- TABLE 76 PANASONIC: MAJOR PRODUCT OFFERINGS

- TABLE 77 MIDEA: MAJOR PRODUCT OFFERINGS

- TABLE 78 REGAL: MAJOR PRODUCT OFFERINGS

- TABLE 79 RAYTHEON TECHNOLOGIES: MAJOR PRODUCT OFFERINGS

- TABLE 80 FLAKT GROUP: MAJOR PRODUCT OFFERINGS

- TABLE 81 SWEGON: MAJOR PRODUCT OFFERINGS

- TABLE 82 VTS GROUP: MAJOR PRODUCT OFFERINGS

- TABLE 83 NUAIRE: MAJOR PRODUCT OFFERINGS

- TABLE 84 NORTEK: MAJOR PRODUCT OFFERINGS

- TABLE 85 ALFA LAVAL: MAJOR PRODUCT OFFERINGS

- TABLE 86 HITACHI: MAJOR PRODUCT OFFERINGS

- TABLE 87 LU-VE: MAJOR PRODUCT OFFERINGS

- TABLE 88 VENT-AXIA: MAJOR PRODUCT OFFERINGS

- TABLE 89 ROSENBERG: MAJOR PRODUCT OFFERINGS

- TABLE 90 S & P: MAJOR PRODUCT OFFERINGS

- TABLE 91 WOLF: MAJOR PRODUCT OFFERINGS

- TABLE 92 CIAT: MAJOR PRODUCT OFFERINGS

- TABLE 93 AL-KO GROUP: MAJOR PRODUCT OFFERINGS

- TABLE 94 DYNAIR: MAJOR PRODUCT OFFERINGS

- TABLE 95 DANFOSS: MAJOR PRODUCT OFFERINGS

- TABLE 96 LENNOX: MAJOR PRODUCT OFFERINGS

- TABLE 97 BACKER SPRINGFIELD: MAJOR PRODUCT OFFERINGS

- TABLE 98 DUNHAMBUSH: MAJOR PRODUCT OFFERINGS

- TABLE 99 TCL: MAJOR PRODUCT OFFERINGS

- TABLE 100 TROX: MAJOR PRODUCT OFFERINGS

- TABLE 101 VAILLANT GROUP: MAJOR PRODUCT OFFERINGS

- TABLE 102 INGERSOLL RAND: MAJOR PRODUCT OFFERINGS

- TABLE 103 CAMFIL: MAJOR PRODUCT OFFERINGS

- TABLE 104 GLOBAL HVAC MAINTENANCE & SERVICE MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 105 GLOBAL HVAC MAINTENANCE & SERVICE MARKET BY SERVICE MODEL 2023-2029 ($ BILLION)

- TABLE 106 GLOBAL HVAC MAINTENANCE & SERVICE MARKET BY EQUIPMENT 2023-2029 ($ BILLION)

- TABLE 107 GLOBAL HVAC MAINTENANCE & SERVICE MARKET BY END-USER 2023-2029 ($ BILLION)

- TABLE 108 CURRENCY CONVERSION 2017-2023

The global HVAC maintenance and services market is expected to grow at a CAGR of 5.79% from 2023-2029.

MARKET TRENDS & DRIVERS

Rise in Disposable Income

The high disposable income of most of the population worldwide is attributable to the high literacy and employment rates. Thus, such factors contribute to an increasing consumer inclination toward premium and smart products available in the market. Despite premium pricing, the demand for the construction of swimming pools in the residential and commercial sectors is rising in developed countries such as the US. The surge in demand for construction would propel the demand for HVAC maintenance services. The considerably high demand for pool heat pumps worldwide can be attributed to the substantial disposable incomes of working individuals.

Favorable Government Policies and Incentives

The favorable government policies across the countries that support using renewable energy sources and prevent the emission of greenhouse gases into the atmosphere are eventually driving the HVAC maintenance and services market. For instance, the Chinese government strives to promote the use of heat pumps nationwide. It provides subsidies for installation that can cover up to 90% of the total unit cost, especially where heating with coal fire is popular. The country has also been trying to take a sustainable approach, making it more significant to reduce the emission of hazardous gases into the environment. The China Heat Pump Alliance (CHPA) is the standard body for the HVAC market in the country.

INDUSTRY RESTRAINTS

High Installation and Upfront Costs

Despite the benefits associated with HVAC in terms of sustainable contribution to the environment, the high initial and upfront costs are hindering their adoption. Such factors can be a significant challenge for the HVAC maintenance and services market, especially in the growing economies and price-sensitive markets of APAC and Latin America, where cost is a major influencing factor for purchase. According to estimates, the average installation costs for an HVAC with pool plumbing might range between USD 3,600 and USD 6,500, whereas the labor costs might range between USD 500 and USD 1,000. These prices are often quite high for middle-income consumers who form the major target segment. Although there is evidence of HVAC generating low operational costs over time when compared to conventional gas and solar heaters, the high installation cost is a burden for vendors in the market.

SEGMENTATION INSIGHTS

INSIGHTS BY EQUIPMENT

The HVAC maintenance and services market by equipment is segmented into heating, air conditioning, and ventilation. The heating segment dominated the global market share in 2023. The heating equipment market is characterized by many vendors producing both traditional and modern heating equipment. The market has several tools, each with a specific functional and distinct technology. Some include heating pumps, furnaces, boiler units, and other heating equipment. Heating pumps have been one of the most critical HVAC systems. They are mainly used in cold regions as their primary function is heating. The demand for heat pumps mainly results from efficiency since their output is four times the energy consumed. Heat pumps are a steady revenue generator for the industry and have witnessed high growth and constant innovation. The key factors favoring the heat pump demand include increased energy efficiency, low cost & payback period, and high reliability.

Segmentation by Equipment Type

- Heating

- Air Conditioning

- Ventilation

INSIGHTS BY SERVICE MODEL

The maintenance & repair service model segment holds the most prominent share of the HVAC maintenance and services market 2023. HVAC maintenance, such as changing belts and filters, greasing bearings, and adjusting equipment due to wear and tear, is done periodically to keep equipment running correctly and efficiently. One convincing rationale for timely HVAC preventive maintenance is the potential for substantial savings on user utility bills. When an HVAC unit operates at peak efficiency, it doesn't overexert itself, which helps to reduce energy consumption. Moreover, the U.S. Department of Energy suggests that this efficiency boost can translate into significant savings, potentially slashing end-user energy costs by as much as 30%. Embracing HVAC preventative maintenance is not only for efficiency but also helps foster healthier indoor air quality. The U.S. Environmental Protection Agency (EPA) mentioned indoor air can be two to five times more polluted than outdoor air. Proper HVAC maintenance can help remove pollutants and allergens, significantly improving indoor air quality. Such factors are projected to support the segmental growth during the forecast period.

Segmentation by Service Model

- Maintenance & Repair

- Installation

- Replacement

- Consulting

INSIGHTS BY END USERS

The global HVAC maintenance and services market by end-users is segmented into residential, commercial, and others. The residential end-user segment has emerged as the largest HVAC maintenance and services market. The rise in disposable income, growing urbanization, willingness for a sophisticated lifestyle, and expansion of distribution networks to cater to domestic aftersales services have led to the segment's dominance. With immense scope for commercial applications, the segment is booming in established markets of APAC, Europe, and the United States. Further, developing affordable and flexible HVAC that matches the complex and dynamic infrastructure and helps lower utility bills contributes to the segment's growth. Institutions such as schools, colleges, sports complexes, and water parks also use renewable technologies to signify or differentiate themselves from society by showcasing their environmental commitment by reducing their carbon footprint. Restaurants, hotels, spas, and recreation centers are the major end-users in the segment, which poses a strong growth prospect for the next five years. It is further accelerated by the growth in tourism, leisure activities, demographic factors, lifestyle modifications, and supportive incentives from the government to promote business activities.

Segmentation by End Users

- Residential

- Commercial

- Others

GEOGRAPHICAL ANALYSIS

APAC holds the most significant share of the global HVAC maintenance and services market 2023. The increasing demand for energy-efficient HVAC systems and severe regulations for using explosion-proof HVAC equipment is growing in the APAC region. Also, the adoption of cleanrooms across industries will offer enormous growth opportunities. Moreover, the frequency of natural disasters in the Asia Pacific region is expected to remain high. With population relocation to coastal cities, a specific disordered urbanization process is the primary factor leading to the vulnerable climate change risk in APAC countries. Therefore, the fluctuating climatic conditions propel the demand for the dynamic nature of HVAC maintenance & service in APAC countries in the forecast period.

Segmentation by Geography

- APAC

- China

- Japan

- India

- Australia

- South Korea

- Europe

- Germany

- France

- Russia

- The U.K.

- Norway

- Demark

- Italy

- Poland

- Spain

- North America

- The U.S.

- Canada

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

COMPETITIVE LANDSCAPE

Global players in the HVAC maintenance and services market, like Systemair Manufacturing, Johnson Controls, Zehnder, and Ostberg, are trying to expand their markets through profitable partnerships and merger strategies. In contrast, the domestic vendors in the HVAC maintenance and services industry are capitalizing on the product portfolio that best suits domestic needs and wants. However, being a technology-oriented product, the scope of differentiation lies with sophistication and deployment of advanced features like energy efficiency, COP, eco-friendly refrigerant, installation costs, geographical climate, services analysis, and much more, through which the product can stay away from the competitive environment. With the recent advancements in engineering and technological features, the changing dynamics of the HVAC industry demand highly effective heating equipment for universal applications.

Key Company Profiles

- Systemair

- Johnson Controls

- Robert Bosch

- Zehnder

- Ostberg

- Aldes

- Daikin

- Samsung

- Mitsubishi Electric

- Rheem Manufacturing Company

- AquaCal

- Pentair

Other Prominent Vendors

- LG

- Panasonic

- Carrier

- MIDEA

- Regal

- Raytheon Technologies

- Flakt Group

- Beijer Ref

- Flexit

- Grundfos

- Swegon

- VTS

- Nuaire

- Nortek

- Alfa Laval

- Hitachi

- LU-VE

- Vent-Axia

- Rosenberg

- S&P

- Wolf

- CIAT

- AL-KO GROUP

- Dynair

- Danfoss

- Lennox

- Backer Springfield

- Dunhambush

- TCL

- Trox

- Vaillant Group

- Ingersoll Rand

- Camfil

KEY QUESTIONS ANSWERED:

1. How big is the global HVAC maintenance and services market?

2. What is the growth rate of the global HVAC maintenance and services market?

3. Which region dominates the global HVAC maintenance and services market share?

4. What are the significant HVAC maintenance and services industry trends?

5. Who are the key players in the global HVAC maintenance and services market?

TABLE OF CONTENTS

1 SCOPE & COVERAGE

- 1.1. MARKET DEFINITION

- 1.1.1. INCLUSIONS

- 1.1.2. EXCLUSIONS

- 1.1.3. MARKET ESTIMATION CAVEATS

- 1.2. SEGMENT COVERED & DEFINITIONS

- 1.2.1. MARKET SEGMENTATION BY SERVICE MODEL

- 1.2.2. MARKET SEGMENTATION BY EQUIPMENT

- 1.2.3. MARKET SEGMENTATION BY END-USER

- 1.3. MARKET DERIVATION

- 1.3.1. BASE YEAR

2 PREMIUM INSIGHTS

- 2.1 OPPORTUNITY POCKETS

- 2.1.1 OVERVIEW

- 2.1.2 DRIVING FACTORS

- 2.1.3 MARKET BY END-USER

- 2.1.4 MARKET BY EQUIPMENT

- 2.1.5 MARKET BY SERVICE MODEL

- 2.1.6 COMPETITIVE LANDSCAPE

- 2.1.7 GROWTH STRATEGY OF KEY VENDORS

3 MARKET AT A GLANCE

4 INTRODUCTION

- 4.1 OVERVIEW

- 4.2 COST ANALYSIS

- 4.3 KEY INSIGHTS FOR HVAC SYSTEM

- 4.4 MERGER & ACQUISITIONS AND PRODUCT DEVELOPMENT

- 4.5 GOVERNMENT REGULATIONS PROMOTING HVAC SYSTEMS

- 4.5.1 OVERVIEW

- 4.5.2 REPOWEREU PLAN CONTRIBUTION TO HVAC MARKET

- 4.5.3 ADVANTAGES OF REPOWEREU PLAN

- 4.5.4 BENEFITS OF IRA FOR HEATING EQUIPMENT

- 4.6 KEY COMPETITIVE HIGHLIGHTS

- 4.7 GLOBAL ECONOMIC SCENARIO

- 4.7.1 REGIONAL ECONOMY

- 4.7.2 RUSSIA-UKRAINE CONFLICT: GLOBAL IMPACT

- 4.8 KEY INSIGHTS FOR DEMAND FOR HVAC SYSTEMS AND SERVICES

- 4.9 DEMAND FROM COMMERCIAL SPACES

- 4.9.1 INCREASE IN DEMAND FOR HVAC SYSTEMS AND SERVICES IN COWORKING SPACES

- 4.9.2 KEY HIGHLIGHTS FOR GLOBAL CONSTRUCTION SECTOR

5 MARKET OPPORTUNITIES & TRENDS

- 5.1 EMERGENCE OF IOT AND PRODUCT INNOVATIONS TO AID REPLACEMENTS

- 5.2 REPLACEMENT OF EXISTING EQUIPMENT WITH ENERGY-EFFICIENT ONES

- 5.3 RISE IN DISPOSABLE INCOME

6 MARKET GROWTH ENABLERS

- 6.1 RISE IN COMMERCIAL CONSTRUCTION AND PROJECTS

- 6.2 FAVORABLE GOVERNMENT POLICIES AND INCENTIVES

- 6.3 DEMAND FOR LOW GWP REFRIGERANT SOLUTIONS IN HEATING EQUIPMENT

7 MARKET RESTRAINTS

- 7.1 HIGH INSTALLATION AND UPFRONT COSTS

- 7.2 LACK OF SKILLED LABOR

- 7.3 STRINGENT REGULATIONS

- 7.4 TURBULENT GLOBAL POLITICAL AND TRADE RELATIONS

8 MARKET LANDSCAPE

- 8.1 MARKET OVERVIEW

- 8.1.1 HIGHLIGHTS

- 8.2 MARKET SIZE & FORECAST

- 8.3 FIVE FORCES ANALYSIS

- 8.3.1 THREAT OF NEW ENTRANTS

- 8.3.2 BARGAINING POWER OF SUPPLIERS

- 8.3.3 BARGAINING POWER OF BUYERS

- 8.3.4 THREAT OF SUBSTITUTES

- 8.3.5 COMPETITIVE RIVALRY

9 EQUIPMENT

- 9.1 MARKET SNAPSHOT & GROWTH ENGINE

- 9.2 MARKET OVERVIEW

- 9.2.1 KEY INSIGHTS

- 9.3 HEATING

- 9.3.1 MARKET OVERVIEW

- 9.3.2 HEAT PUMP

- 9.3.3 BOILER UNIT

- 9.3.4 FURNACE

- 9.3.5 MARKET SIZE & FORECAST

- 9.3.6 MARKET BY GEOGRAPHY

- 9.4 AIR CONDITIONING

- 9.4.1 MARKET OVERVIEW

- 9.4.2 RAC

- 9.4.3 CAC

- 9.4.4 CHILLER

- 9.4.5 HEAT EXCHANGER

- 9.4.6 KEY TAKEAWAYS

- 9.4.7 MARKET SIZE & FORECAST

- 9.4.8 MARKET BY GEOGRAPHY

- 9.5 VENTILATION

- 9.5.1 MARKET OVERVIEW

- 9.5.2 MARKET DYNAMICS OF VENTILATION EQUIPMENT

- 9.5.3 AIR HANDLING UNIT (AHU)

- 9.5.4 AIR FILTER

- 9.5.5 HUMIDIFIER & DEHUMIDIFIER

- 9.5.6 FAN COIL UNIT

- 9.5.7 MARKET SIZE & FORECAST

- 9.5.8 MARKET BY GEOGRAPHY

10 SERVICE MODEL

- 10.1 MARKET SNAPSHOT & GROWTH ENGINE

- 10.2 MARKET OVERVIEW

- 10.2.1 TYPES OF HVAC SERVICES

- 10.3 MAINTENANCE & REPAIR

- 10.3.1 MARKET OVERVIEW

- 10.3.2 KEY HIGHLIGHTS FOR HVAC MAINTENANCE AND REPAIR

- 10.3.3 MARKET SIZE & FORECAST

- 10.3.4 MARKET BY GEOGRAPHY

- 10.4 INSTALLATION

- 10.4.1 MARKET OVERVIEW

- 10.4.2 MARKET SIZE & FORECAST

- 10.4.3 MARKET BY GEOGRAPHY

- 10.5 REPLACEMENT

- 10.5.1 MARKET OVERVIEW

- 10.5.2 MARKET SIZE & FORECAST

- 10.5.3 MARKET BY GEOGRAPHY

- 10.6 CONSULTING

- 10.6.1 MARKET OVERVIEW

- 10.6.2 MARKET SIZE & FORECAST

- 10.6.3 MARKET BY GEOGRAPHY

11 END-USER

- 11.1 MARKET SNAPSHOT & GROWTH ENGINE

- 11.2 MARKET OVERVIEW

- 11.3 RESIDENTIAL

- 11.3.1 MARKET OVERVIEW

- 11.3.2 MARKET SIZE & FORECAST

- 11.3.3 MARKET BY GEOGRAPHY

- 11.4 COMMERCIAL

- 11.4.1 MARKET OVERVIEW

- 11.4.2 HOTELS AND RESORTS

- 11.4.3 OFFICE SPACES

- 11.4.4 KEY INSIGHTS FOR COWORKING SPACES

- 11.4.5 AIRPORT & PUBLIC UTILITIES

- 11.4.6 HOSPITALITY

- 11.4.7 HOSPITALS

- 11.4.8 EDUCATIONAL INSTITUTIONS

- 11.4.9 MARKET SIZE & FORECAST

- 11.4.10 MARKET BY GEOGRAPHY

- 11.5 OTHERS

- 11.5.1 MARKET OVERVIEW

- 11.5.2 MARKET SIZE & FORECAST

- 11.5.3 MARKET BY GEOGRAPHY

12 GEOGRAPHY

- 12.1 MARKET SNAPSHOT & GROWTH ENGINE

- 12.2 GEOGRAPHIC OVERVIEW

- 12.2.1 REGIONAL ANALYSIS

13 APAC

- 13.1 MARKET OVERVIEW

- 13.2 MARKET SIZE & FORECAST

- 13.3 SERVICE MODEL

- 13.3.1 MARKET SIZE & FORECAST

- 13.4 EQUIPMENT

- 13.4.1 MARKET SIZE & FORECAST

- 13.5 END-USER

- 13.5.1 MARKET SIZE & FORECAST

- 13.6 KEY COUNTRIES

- 13.7 CHINA: MARKET SIZE & FORECAST

- 13.8 JAPAN: MARKET SIZE & FORECAST

- 13.9 INDIA: MARKET SIZE & FORECAST

- 13.10 AUSTRALIA: MARKET SIZE & FORECAST

- 13.11 SOUTH KOREA: MARKET SIZE & FORECAST

14 EUROPE

- 14.1 MARKET OVERVIEW

- 14.2 MARKET SIZE & FORECAST

- 14.3 SERVICE MODEL

- 14.3.1 MARKET SIZE & FORECAST

- 14.4 EQUIPMENT

- 14.4.1 MARKET SIZE & FORECAST

- 14.5 END-USER

- 14.5.1 MARKET SIZE & FORECAST

- 14.6 KEY COUNTRIES

- 14.7 GERMANY: MARKET SIZE & FORECAST

- 14.8 FRANCE: MARKET SIZE & FORECAST

- 14.9 RUSSIA: MARKET SIZE & FORECAST

- 14.10 UK: MARKET SIZE & FORECAST

- 14.11 NORWAY: MARKET SIZE & FORECAST

- 14.12 DENMARK: MARKET SIZE & FORECAST

- 14.13 ITALY: MARKET SIZE & FORECAST

- 14.14 POLAND: MARKET SIZE & FORECAST

- 14.15 SPAIN: MARKET SIZE & FORECAST

15 NORTH AMERICA

- 15.1 MARKET OVERVIEW

- 15.2 MARKET SIZE & FORECAST

- 15.3 SERVICE MODEL

- 15.3.1 MARKET SIZE & FORECAST

- 15.4 EQUIPMENT

- 15.4.1 MARKET SIZE & FORECAST

- 15.5 END-USER

- 15.5.1 MARKET SIZE & FORECAST

- 15.6 KEY COUNTRIES

- 15.7 US: MARKET SIZE & FORECAST

- 15.7.1 COMMON ISSUE WITH SPACE HEATING AND COOLING SYSTEMS INSTALLATION AND MAINTENANCE

- 15.8 CANADA: MARKET SIZE & FORECAST

16 LATIN AMERICA

- 16.1 MARKET OVERVIEW

- 16.2 MARKET SIZE & FORECAST

- 16.3 SERVICE MODEL

- 16.3.1 MARKET SIZE & FORECAST

- 16.4 EQUIPMENT

- 16.4.1 MARKET SIZE & FORECAST

- 16.5 END-USER

- 16.5.1 MARKET SIZE & FORECAST

- 16.6 KEY COUNTRIES

- 16.7 BRAZIL: MARKET SIZE & FORECAST

- 16.8 MEXICO: MARKET SIZE & FORECAST

- 16.9 ARGENTINA: MARKET SIZE & FORECAST

17 MIDDLE EAST & AFRICA

- 17.1 MARKET OVERVIEW

- 17.2 MARKET SIZE & FORECAST

- 17.3 SERVICE MODEL

- 17.3.1 MARKET SIZE & FORECAST

- 17.4 EQUIPMENT

- 17.4.1 MARKET SIZE & FORECAST

- 17.5 END-USER

- 17.5.1 MARKET SIZE & FORECAST

- 17.6 KEY COUNTRIES

- 17.7 SAUDI ARABIA: MARKET SIZE & FORECAST

- 17.8 UAE: MARKET SIZE & FORECAST

- 17.9 SOUTH AFRICA: MARKET SIZE & FORECAST

18 COMPETITIVE LANDSCAPE

- 18.1 COMPETITION OVERVIEW

- 18.2 GROWTH STRATEGY OF KEY VENDORS

- 18.3 KEY COMPETENCIES

- 18.4 GLOBAL DYNAMICS OF NORMS AND REGULATIONS

19 KEY COMPANY PROFILES

- 19.1 ALDES

- 19.1.1 BUSINESS OVERVIEW

- 19.1.2 PRODUCT OFFERINGS

- 19.1.3 KEY STRATEGIES

- 19.1.4 KEY STRENGTHS

- 19.1.5 KEY OPPORTUNITIES

- 19.2 AQUACAL

- 19.2.1 BUSINESS OVERVIEW

- 19.2.2 PRODUCT OFFERINGS

- 19.2.3 KEY STRATEGIES

- 19.2.4 KEY STRENGTHS

- 19.2.5 KEY OPPORTUNITIES

- 19.3 DAIKIN

- 19.3.1 BUSINESS OVERVIEW

- 19.3.2 PRODUCT OFFERINGS

- 19.3.3 KEY STRATEGIES

- 19.3.4 KEY STRENGTHS

- 19.3.5 KEY OPPORTUNITIES

- 19.4 JOHNSON CONTROLS

- 19.4.1 BUSINESS OVERVIEW

- 19.4.2 PRODUCT OFFERINGS

- 19.4.3 KEY STRATEGIES

- 19.4.4 KEY STRENGTHS

- 19.4.5 KEY OPPORTUNITIES

- 19.5 MITSUBISHI ELECTRIC

- 19.5.1 BUSINESS OVERVIEW

- 19.5.2 PRODUCT OFFERINGS

- 19.5.3 KEY STRATEGIES

- 19.5.4 KEY STRENGTHS

- 19.5.5 KEY OPPORTUNITIES

- 19.6 OSTBERG

- 19.6.1 BUSINESS OVERVIEW

- 19.6.2 PRODUCT OFFERINGS

- 19.6.3 KEY STRATEGIES

- 19.6.4 KEY STRENGTHS

- 19.6.5 KEY OPPORTUNITIES

- 19.7 PENTAIR

- 19.7.1 BUSINESS OVERVIEW

- 19.7.2 PRODUCT OFFERINGS

- 19.7.3 KEY STRATEGIES

- 19.7.4 KEY STRENGTHS

- 19.7.5 KEY OPPORTUNITIES

- 19.8 ROBERT BOSCH

- 19.8.1 BUSINESS OVERVIEW

- 19.8.2 PRODUCT OFFERINGS

- 19.8.3 KEY STRATEGIES

- 19.8.4 KEY STRENGTHS

- 19.8.5 KEY OPPORTUNITIES

- 19.9 RHEEM MANUFACTURING COMPANY

- 19.9.1 BUSINESS OVERVIEW

- 19.9.2 PRODUCT OFFERINGS

- 19.9.3 KEY STRATEGIES

- 19.9.4 KEY STRENGTHS

- 19.9.5 KEY OPPORTUNITIES

- 19.10 SAMSUNG

- 19.10.1 BUSINESS OVERVIEW

- 19.10.2 PRODUCT OFFERINGS

- 19.10.3 KEY STRATEGIES

- 19.10.4 KEY STRENGTHS

- 19.10.5 KEY OPPORTUNITIES

- 19.11 SIEMENS AG

- 19.11.1 BUSINESS OVERVIEW

- 19.11.2 PRODUCT OFFERINGS

- 19.11.3 KEY STRATEGIES

- 19.11.4 KEY STRENGTHS

- 19.11.5 KEY OPPORTUNITIES

- 19.12 SYSTEMAIR

- 19.12.1 BUSINESS OVERVIEW

- 19.12.2 PRODUCT OFFERINGS

- 19.12.3 KEY STRATEGIES

- 19.12.4 KEY STRENGTHS

- 19.12.5 KEY OPPORTUNITIES

- 19.13 ZEHNDER

- 19.13.1 BUSINESS OVERVIEW

- 19.13.2 PRODUCT OFFERINGS

- 19.13.3 KEY STRATEGIES

- 19.13.4 KEY STRENGTHS

- 19.13.5 KEY OPPORTUNITIES

20 OTHER PROMINENT VENDORS

- 20.1 CARRIER

- 20.1.1 BUSINESS OVERVIEW

- 20.1.2 PRODUCT OFFERINGS

- 20.2 HONEYWELL INTERNATIONAL INC

- 20.2.1 BUSINESS OVERVIEW

- 20.2.2 PRODUCT OFFERINGS

- 20.3 LG

- 20.3.1 BUSINESS OVERVIEW

- 20.3.2 PRODUCT OFFERINGS

- 20.4 PANASONIC

- 20.4.1 BUSINESS OVERVIEW

- 20.4.2 PRODUCT OFFERINGS

- 20.5 MIDEA

- 20.5.1 BUSINESS OVERVIEW

- 20.5.2 PRODUCT OFFERINGS

- 20.6 REGAL

- 20.6.1 BUSINESS OVERVIEW

- 20.6.2 PRODUCT OFFERINGS

- 20.7 RAYTHEON TECHNOLOGIES

- 20.7.1 BUSINESS OVERVIEW

- 20.7.2 PRODUCT OFFERINGS

- 20.8 FLAKT GROUP

- 20.8.1 BUSINESS OVERVIEW

- 20.8.2 PRODUCT OFFERINGS

- 20.9 SWEGON

- 20.9.1 BUSINESS OVERVIEW

- 20.9.2 PRODUCT OFFERINGS

- 20.10 VTS GROUP

- 20.10.1 BUSINESS OVERVIEW

- 20.10.2 PRODUCT OFFERINGS

- 20.11 NUAIRE

- 20.11.1 BUSINESS OVERVIEW

- 20.11.2 PRODUCT OFFERINGS

- 20.12 NORTEK

- 20.12.1 BUSINESS OVERVIEW

- 20.12.2 PRODUCT OFFERINGS

- 20.13 ALFA LAVAL

- 20.13.1 BUSINESS OVERVIEW

- 20.13.2 PRODUCT OFFERINGS

- 20.14 HITACHI

- 20.14.1 BUSINESS OVERVIEW

- 20.14.2 PRODUCT OFFERINGS

- 20.15 LU-VE

- 20.15.1 BUSINESS OVERVIEW

- 20.15.2 PRODUCT OFFERINGS

- 20.16 VENT-AXIA

- 20.16.1 BUSINESS OVERVIEW

- 20.16.2 PRODUCT OFFERINGS

- 20.17 ROSENBERG

- 20.17.1 BUSINESS OVERVIEW

- 20.17.2 PRODUCT OFFERINGS

- 20.18 S & P

- 20.18.1 BUSINESS OVERVIEW

- 20.18.2 PRODUCT OFFERINGS

- 20.19 WOLF

- 20.19.1 BUSINESS OVERVIEW

- 20.19.2 PRODUCT OFFERINGS

- 20.20 CIAT

- 20.20.1 BUSINESS OVERVIEW

- 20.20.2 PRODUCT OFFERINGS

- 20.21 AL-KO GROUP

- 20.21.1 BUSINESS OVERVIEW

- 20.21.2 PRODUCT OFFERINGS

- 20.22 DYNAIR

- 20.22.1 BUSINESS OVERVIEW

- 20.22.2 PRODUCT OFFERINGS

- 20.23 DANFOSS

- 20.23.1 BUSINESS OVERVIEW

- 20.23.2 PRODUCT OFFERINGS

- 20.24 LENNOX

- 20.24.1 BUSINESS OVERVIEW

- 20.24.2 PRODUCT OFFERINGS

- 20.25 BACKER SPRINGFIELD

- 20.25.1 BUSINESS OVERVIEW

- 20.25.2 PRODUCT OFFERINGS

- 20.26 DUNHAMBUSH

- 20.26.1 BUSINESS OVERVIEW

- 20.26.2 PRODUCT OFFERINGS

- 20.27 TCL

- 20.27.1 BUSINESS OVERVIEW

- 20.27.2 PRODUCT OFFERINGS

- 20.28 TROX

- 20.28.1 BUSINESS OVERVIEW

- 20.28.2 PRODUCT OFFERINGS

- 20.29 VAILLANT GROUP

- 20.29.1 BUSINESS OVERVIEW

- 20.29.2 PRODUCT OFFERINGS

- 20.30 INGERSOLL RAND

- 20.30.1 BUSINESS OVERVIEW

- 20.30.2 PRODUCT OFFERINGS

- 20.31 CAMFIL

- 20.31.1 BUSINESS OVERVIEW

- 20.31.2 PRODUCT OFFERINGS

21 REPORT SUMMARY

- 21.1 KEY TAKEAWAYS

- 21.2 STRATEGIC RECOMMENDATIONS

22 QUANTITATIVE SUMMARY

- 22.1 MARKET BY GEOGRAPHY

- 22.1.1 SERVICE MODEL: MARKET SIZE & FORECAST

- 22.1.2 EQUIPMENT: MARKET SIZE & FORECAST

- 22.1.3 END-USER: MARKET SIZE & FORECAST

23 APPENDIX

- 23.1 RESEARCH METHODOLOGY

- 23.2 RESEARCH PROCESS

- 23.3 REPORT ASSUMPTIONS & CAVEATS

- 23.3.1 KEY CAVEATS

- 23.3.2 CURRENCY CONVERSION

- 23.4 ABBREVIATIONS