|

|

市場調査レポート

商品コード

1298136

工業塩の世界市場 - 見通しと予測(2023年~2028年)Industrial Salt Market - Global Outlook & Forecast 2023-2028 |

||||||

|

|

|||||||

|

|||||||

| 工業塩の世界市場 - 見通しと予測(2023年~2028年) |

|

出版日: 2023年06月28日

発行: Arizton Advisory & Intelligence

ページ情報: 英文 283 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

世界の工業塩の市場規模は、2022年~2028年にCAGRで4.13%の成長が予測されています。発展途上国を中心とした医薬品需要の増加が、市場の成長を促進しています。

当レポートでは、世界の工業塩市場について調査分析し、市場規模と予測、機会と動向、主要企業などの情報を提供しています。

目次

第1章 調査手法

第2章 調査の目的

第3章 調査プロセス

第4章 範囲

第5章 レポートの前提条件と注意事項

第6章 市場の概要

第7章 主要考察

- レポートの概要

- 機会と課題の分析

- セグメント分析

- 地域の分析

- 競合の分析

第8章 イントロダクション

- 概要

- 分析に基づいた用途

- 塩の生産プロセス

- 世界の塩の生産

- 政府の規制と政策

- 市場の危険因子

- COVID-19の影響の分析

- 世界経済情勢

第9章 市場の機会と動向

- 急速な工業化

- 天日塩の利用の拡大

- 岩塩鉱山とその他の生産施設の拡張

第10章 市場成長要因

- 塩生産における技術の進歩

- 化学・製薬業界における塩の多用

- 水処理システムの需要の増加

第11章 市場抑制要因

- 健康と環境の問題

- 限られた入手可能性、原材料の高い価格

- 永続する経済減速

- 氷結防止塩の販売に影響を与える冬の天候の変動

- 厳しい政府規制

第12章 市場情勢

- 市場の概要

- 市場規模と予測

- 市場:プロセス別

- 市場:製品タイプ別

- 市場:エンドユーザー別

- ファイブフォース分析

第13章 プロセス

- 市場のスナップショットと成長エンジン

- 市場の概要

- 抽出装置

- スチーマー

第14章 製品タイプ

- 市場のスナップショットと成長エンジン

- 市場の概要

- 天日塩

- 岩塩

- 塩水

- 真空塩

第15章 エンドユーザー

- 市場のスナップショットと成長エンジン

- 市場の概要

- 化学工業

- 除氷

- 水処理

- 石油・ガス産業

- その他

第16章 地域

- 市場のスナップショットと成長エンジン(収益)

- 市場のスナップショットと成長エンジン(数量)

- 地理的概要

第17章 アジア太平洋

- 市場規模と予測

- プロセス

- 製品タイプ

- エンドユーザー

- 主要国(数量)

- 中国:市場規模と予測

- インド:市場規模と予測

- オーストラリア:市場規模と予測

- 日本:市場規模と予測

- 韓国:市場規模と予測

第18章 北米

- 市場規模と予測

- プロセス

- 製品タイプ

- エンドユーザー

- 主要国(数量)

- 米国:市場規模と予測

- カナダ:市場規模と予測

第19章 欧州

- 市場規模と予測

- プロセス

- 製品タイプ

- エンドユーザー

- 主要国(数量)

- ドイツ:市場規模と予測

- 英国:市場規模と予測

- ロシア:市場規模と予測

- フランス:市場規模と予測

- ポーランド:市場規模と予測

第20章 中東・アフリカ

- 市場規模と予測

- プロセス

- 製品タイプ

- エンドユーザー

- 主要国(数量)

- イラン:市場規模と予測

- サウジアラビア:市場規模と予測

- アラブ首長国連邦:市場規模と予測

- トルコ:市場規模と予測

- エジプト:市場規模と予測

第21章 ラテンアメリカ

- 市場規模と概要

- プロセス

- 製品タイプ

- エンドユーザー

- 主要国(数量)

- ブラジル:市場規模と予測

- メキシコ:市場規模と予測

- その他のラテンアメリカ:市場規模と予測

第22章 競合情勢

- 競合の概要

第23章 主要企業プロファイル

- CARGILL

- COMPASS MINERALS AMERICA

- DOMINION SALT

- RIO TINTO

- TATA CHEMICALS

- K+S AKTIENGESELLSCHAFT

- CHINA NATIONAL SALT INDUSTRY GROUP

- INEOS GROUP

第24章 その他の著名なベンダー

- WILSON SALT

- ICL SALT

- IRISH SALT MINES

- NOBIAN

- DONALD BROWN GROUP

- DELMON

- MITSUI & CO.

- MORTON SALT

- ARCHEAN CHEMICAL INDUSTRIES

- ZOUTMAN

- SWISS SALT WORKS

- SALINS GROUP

- AMRA SALT FACTORY

- CIECH GROUP

- AMERICAN ROCK SALT

第25章 レポートの概要

- 重要事項

- 戦略的な推奨事項

第26章 量的要約

第27章 付録

The global industrial salt market is expected to grow at a CAGR of 4.13% from 2022-2028.

MARKET TRENDS & OPPORTUNITIES

Increased Use of Salt in Chemical and Pharmaceutical Industries

Salt is an essential component of the chemical and pharmaceutical industry, where it is used for chemical synthesis and manufacturing of several commodities such as rubber, glass, paper, and textiles. Chloride, commonly used for cleaning, produces various chemicals, drugs, and plastics, with over 85% of medicines, including lifesaving drugs, produced using chlorine. Caustic soda and soda ash, produced using salt, are critical components in various industrial operations, including pulp and paper, chemical processing, and detergent. The pharmaceutical industry, which is growing rapidly, is a major end-user of industrial salt, with over 50% of all drugs administered by salt. The increasing demand for pharmaceutical products, particularly in developing countries, is driving the growth of the industrial salts market.

Rising Demand for Water Treatment

Water quality is a crucial factor in various industrial sectors, such as textile and tanning, as hard water can result in adverse effects such as bleaching, uneven dyeing, and decreased lifespan of fabrics. Soft water, on the other hand, decreases the cleaning cost, increases the equipment's lifespan, and improves efficiency. In both residential and industrial settings, water softeners are widely used to mitigate the negative impacts of hard water. The global water softener market is expected to cross USD 5.7 billion in 2027, with salt-based water softeners accounting for most of the market share. The demand for portable water consumption, coupled with the rise in water-borne diseases and strict regulations related to water treatment in various sectors, is expected to drive market growth. Asia Pacific dominates the water treatment market, followed by Europe. China, Japan, South Korea, and India are the key markets in the former, and the U.K., France, Italy, and Germany in the latter.

INDUSTRY RESTRAINTS

Winter Weather Variability Affecting Salt Sales for De-icing

Industrial salt is widely used for de-icing, which accounts for approximately 20% of global consumption. Studies conducted in Wisconsin indicate that using salt for snow melting can significantly reduce road accidents by 88% and accident costs by 85%. Key markets for salt de-icing include the U.S., Canada, and Northern Europe, where a considerable amount of salt is used for de-icing roadways, sidewalks, and walkways. In the U.S., around 19 million tons of salt is used for de-icing annually, while in Canada, the number is around 5 million tons. However, the industrial salt market is significantly impacted by any fluctuations in the winter climate as it directly impacts the demand and price of salt for de-icing.

SEGMENTATION INSIGHTS

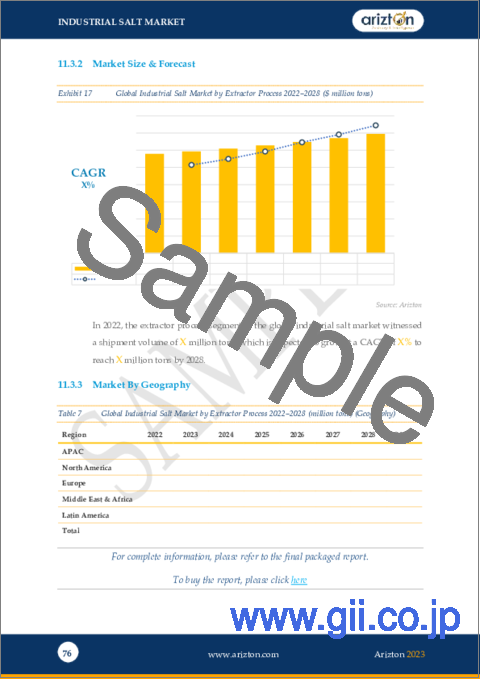

INSIGHTS BY PROCESS

The global industrial salt market by process type is divided into extractor and steamer. Industrial salt can be obtained from different sources, including steam and extraction methods. The steaming process involves the evaporation of seawater or brine under controlled conditions. There are two types of steaming methods: solar and vacuum evaporation. Solar evaporation involves using large, shallow ponds or lakes where seawater or brine evaporates naturally under the sun. This process takes some months to complete, and the resultant salt is called solar salt. The streamer process is a promising technology for the salt industry that offers more sustainable and higher-quality salt production methods. The availability of saline seawater to produce saltwater or brine has primarily driven market consumption.

Segmentation by Process

- Extractor

- Steamer

INSIGHTS BY PRODUCT TYPE

Salt is an essential natural resource that has various applications across diverse industries. The global industrial salt market by product types of segments such as solar salt, rock mining salt, salt in brine, and vacuum salt. Salt is a significant raw material used in multiple manufacturing industries. Common sectors include chemical industries, oil, and gas, de-icing, paper, pulp, etc. Trusted producers and suppliers distribute millions of tons of salt to consumers worldwide. To manage the large volume efficiently of industrial salt, various strict protocols and standards must be considered to ensure the product's quality, purity level, and efficiency level.

Segmentation by Product Type

- Solar Salt

- Rock Salt

- Salt in Brine

- Vacuum Salt

INSIGHTS BY END-USER

The global industrial salt market has various end-users across various sectors. Some key end-users of industrial salt include the chemical industry, where salt is used as a raw material for producing various chemicals such as soda ash, chlorine, and caustic soda. The chemical industry is the largest global industrial salt market end-users, accounting for approximately 51% share in 2022. The oil and gas industry uses salt in drilling operations as a component of drilling fluids.

Segmentation by End-user

- Chemical Industry

- De-icing

- Water Treatment

- Oil & Gas Industry

- Others

GEOGRAPHICAL ANALYSIS

APAC dominated the global industrial salts market, accounting for over 45% of the global consumption by volume. The Asia-Pacific region is the fastest-growing market, driven by growing industrialization, population growth, and increasing demand for processed food and chemicals. India, China, and Japan are the key markets in this region, with China being the largest producer and consumer of industrial salt globally. The growth in urbanization in East Asian countries is driving the construction market in the region. PVC and glass are the key materials of construction. Again, industrial salt is used as a primary raw material for producing PVC and glass, thus, boosting the growth of the industrial salt market in the region.

Segmentation by Geography

- APAC

- China

- India

- Australia

- Japan

- South Korea

- North America

- The U.S.

- Canada

- Europe

- Germany

- The U.K.

- Russia

- France

- Poland

- Middle East & Africa

- Iran

- Saudi Arabia

- UAE

- Turkey

- Egypt

- Latin America

- Brazil

- Mexico

- Rest of Latin America

COMPETITIVE LANDSCAPE

The global industrial salt market is favorably competitive, with several global and regional players operating. Cargill, Compass Minerals, Akzo Nobel, K+S AG, Tata Chemicals, INEOS Salt, and China National Salt Industry Corporation are key players in the global industrial salt market, with significant industry shares. These players use various strategies to maintain their competitive edge, including product innovation and development, mergers and acquisitions, and expanding production capacity. For example, some companies focus on producing low-sodium salt for the food industry. Others are investing in expanding their de-icing business in Europe or strengthening their position in the Latin American market by building a new salt plant in Chile. The industrial salt market is expected to witness intense competition in the coming years due to increasing demand and evolving customer preferences.

Key Company Profiles

- Cargill

- Compass Mineral America

- Dominion Salt

- Rio Tinto

- Tata Chemicals

- K+S Aktiengesellschaft

- China National Salt Industry Group Co. Ltd

- INEOS

Other Prominent Vendors

- Wilson Salt

- ICL Salt

- Irish Salt Mining

- Nobian

- Donald Brown Group

- Delmon

- Mitsui & Co.

- Morton Salt

- Archean Chemical Industries

- Zoutman

- Swiss Salt Works

- Salins Group

- Amra Salt Factory

- CIECH GROUP

- American Rock Salt

KEY QUESTIONS ANSWERED:

- 1. How big is the industrial salt market?

- 2. What is the growth rate of the global industrial salt market?

- 3. What are the significant trends in the industrial salt market?

- 4. Which region dominates the global industrial salt market share?

- 5. Who are the key players in the global industrial salt market?

TABLE OF CONTENTS

1 RESEARCH METHODOLOGY

2 RESEARCH OBJECTIVES

3 RESEARCH PROCESS

4 SCOPE & COVERAGE

- 4.1 MARKET DEFINITION

- 4.1.1 INCLUSIONS

- 4.1.2 EXCLUSIONS

- 4.1.3 MARKET ESTIMATION CAVEATS

- 4.2 BASE YEAR

- 4.3 SCOPE OF THE STUDY

- 4.3.1 MARKET SEGMENTATION BY GEOGRAPHY

- 4.3.2 MARKET BY PROCESS TYPE

- 4.3.3 MARKET BY PRODUCT TYPE

- 4.3.4 MARKET BY END USER

5 REPORT ASSUMPTIONS & CAVEATS

- 5.1 KEY CAVEATS

- 5.2 CURRENCY CONVERSION

- 5.3 MARKET DERIVATION

6 MARKET AT A GLANCE

7 PREMIUM INSIGHTS

- 7.1 REPORT OVERVIEW

- 7.2 ANALYSIS OF OPPORTUNITIES & CHALLENGES

- 7.3 SEGMENT ANALYSIS

- 7.4 REGIONAL ANALYSIS

- 7.5 COMPETITOR ANALYSIS

8 INTRODUCTION

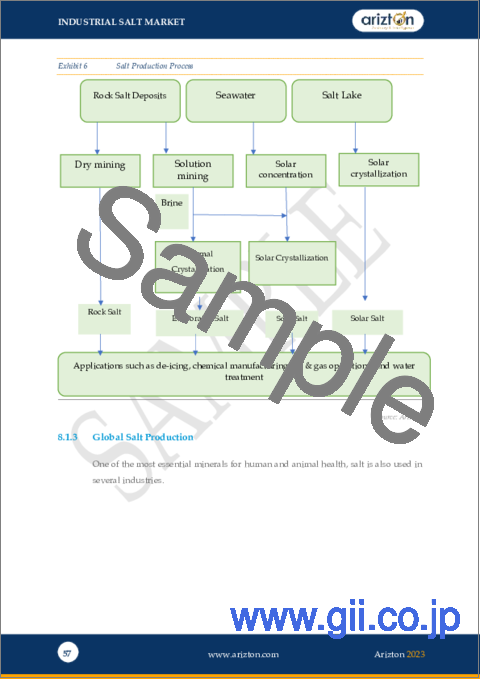

- 8.1 OVERVIEW

- 8.1.1 APPLICATION BASED ON ANALYSIS

- 8.1.2 SALT PRODUCTION PROCESS

- 8.1.3 GLOBAL SALT PRODUCTION

- 8.1.4 GOVERNMENT REGULATION AND POLICIES

- 8.1.5 RISK FACTORS FOR MARKET

- 8.1.6 COVID-19 IMPACT ANALYSIS

- 8.1.7 GLOBAL ECONOMIC CONDITION

9 MARKET OPPORTUNITIES & TRENDS

- 9.1 RAPID PACE OF INDUSTRIALIZATION

- 9.2 GROWING USE OF SOLAR SALTS

- 9.3 EXPANSION OF SALT MINES & OTHER PRODUCTION FACILITIES

10 MARKET GROWTH ENABLERS

- 10.1 TECHNOLOGICAL ADVANCES IN SALT PRODUCTION

- 10.2 HIGH USE OF SALT IN CHEMICAL & PHARMACEUTICAL INDUSTRIES

- 10.3 RISE IN DEMAND FOR WATER TREATMENT SYSTEMS

11 MARKET RESTRAINTS

- 11.1 HEALTH & ENVIRONMENTAL ISSUES

- 11.2 LIMITED AVAILABILITY & HIGH PRICES OF RAW MATERIALS

- 11.3 ENDURING ECONOMIC SLOWDOWN

- 11.4 WINTER WEATHER VARIABILITY AFFECTING SALES OF DE-ICING SALTS

- 11.5 STRINGENT GOVERNMENT REGULATIONS

12 MARKET LANDSCAPE

- 12.1 MARKET OVERVIEW

- 12.2 MARKET SIZE & FORECAST

- 12.3 MARKET BY PROCESS

- 12.4 MARKET BY PRODUCT TYPE

- 12.5 MARKET BY END USER

- 12.6 FIVE FORCES ANALYSIS

- 12.6.1 THREAT OF NEW ENTRANTS

- 12.6.2 BARGAINING POWER OF SUPPLIERS

- 12.6.3 BARGAINING POWER OF BUYERS

- 12.6.4 THREAT OF SUBSTITUTES

- 12.6.5 COMPETITIVE RIVALRY

13 PROCESS

- 13.1 MARKET SNAPSHOT & GROWTH ENGINE

- 13.2 MARKET OVERVIEW

- 13.3 EXTRACTOR

- 13.3.1 MARKET OVERVIEW

- 13.3.2 MARKET SIZE & FORECAST

- 13.3.3 MARKET BY GEOGRAPHY

- 13.4 STEAMER

- 13.4.1 MARKET OVERVIEW

- 13.4.2 MARKET SIZE & FORECAST

- 13.4.3 MARKET BY GEOGRAPHY

14 PRODUCT TYPE

- 14.1 MARKET SNAPSHOT & GROWTH ENGINE

- 14.2 MARKET OVERVIEW

- 14.3 SOLAR SALT

- 14.3.1 MARKET SIZE & FORECAST

- 14.3.2 MARKET BY GEOGRAPHY

- 14.4 ROCK SALT

- 14.4.1 MARKET SIZE & FORECAST

- 14.4.2 MARKET BY GEOGRAPHY

- 14.5 SALT IN BRINE

- 14.5.1 MARKET SIZE & FORECAST

- 14.5.2 MARKET BY GEOGRAPHY

- 14.6 VACUUM SALT

- 14.6.1 MARKET SIZE & FORECAST

- 14.6.2 MARKET BY GEOGRAPHY

15 END USER

- 15.1 MARKET SNAPSHOT & GROWTH ENGINE

- 15.2 MARKET OVERVIEW

- 15.3 CHEMICAL INDUSTRY

- 15.3.1 MARKET OVERVIEW

- 15.3.2 MARKET SIZE & FORECAST

- 15.3.3 MARKET BY GEOGRAPHY

- 15.4 DE-ICING

- 15.4.1 MARKET OVERVIEW

- 15.4.2 MARKET SIZE & FORECAST

- 15.4.3 MARKET BY GEOGRAPHY

- 15.5 WATER TREATMENT

- 15.5.1 MARKET OVERVIEW

- 15.5.2 MARKET SIZE & FORECAST

- 15.5.3 MARKET BY GEOGRAPHY

- 15.6 OIL & GAS INDUSTRY

- 15.6.1 MARKET OVERVIEW

- 15.6.2 MARKET SIZE & FORECAST

- 15.6.3 MARKET BY GEOGRAPHY

- 15.7 OTHERS

- 15.7.1 MARKET OVERVIEW

- 15.7.2 MARKET SIZE & FORECAST

- 15.7.3 MARKET BY GEOGRAPHY

16 GEOGRAPHY

- 16.1 MARKET SNAPSHOT & GROWTH ENGINE (REVENUE)

- 16.2 MARKET SNAPSHOT & GROWTH ENGINE (VOLUME)

- 16.3 GEOGRAPHIC OVERVIEW

17 APAC

- 17.1 MARKET SIZE & FORECAST

- 17.2 PROCESS

- 17.2.1 MARKET SIZE & FORECAST

- 17.3 PRODUCT TYPE

- 17.3.1 MARKET SIZE & FORECAST

- 17.4 END USER

- 17.4.1 MARKET SIZE & FORECAST

- 17.5 KEY COUNTRIES (VOLUME)

- 17.5.1 CHINA: MARKET SIZE & FORECAST

- 17.5.2 INDIA: MARKET SIZE & FORECAST

- 17.5.3 AUSTRALIA: MARKET SIZE & FORECAST

- 17.5.4 JAPAN: MARKET SIZE & FORECAST

- 17.5.5 SOUTH KOREA: MARKET SIZE & FORECAST

18 NORTH AMERICA

- 18.1 MARKET SIZE & FORECAST

- 18.2 PROCESS

- 18.2.1 MARKET SIZE & FORECAST

- 18.3 PRODUCT TYPE

- 18.3.1 MARKET SIZE & FORECAST

- 18.4 END USER

- 18.4.1 MARKET SIZE & FORECAST

- 18.5 KEY COUNTRIES (VOLUME)

- 18.5.1 US: MARKET SIZE & FORECAST

- 18.5.2 CANADA: MARKET SIZE & FORECAST

19 EUROPE

- 19.1 MARKET SIZE & FORECAST

- 19.2 PROCESS

- 19.2.1 MARKET SIZE & FORECAST

- 19.3 PRODUCT TYPE

- 19.3.1 MARKET SIZE & FORECAST

- 19.4 END USER

- 19.4.1 MARKET SIZE & FORECAST

- 19.5 KEY COUNTRIES (VOLUME)

- 19.5.1 GERMANY: MARKET SIZE & FORECAST

- 19.5.2 UK: MARKET SIZE & FORECAST

- 19.5.3 RUSSIA: MARKET SIZE & FORECAST

- 19.5.4 FRANCE: MARKET SIZE & FORECAST

- 19.5.5 POLAND: MARKET SIZE & FORECAST

20 MIDDLE EAST & AFRICA

- 20.1 MARKET SIZE & FORECAST

- 20.2 PROCESS

- 20.2.1 MARKET SIZE & FORECAST

- 20.3 PRODUCT TYPE

- 20.3.1 MARKET SIZE & FORECAST

- 20.4 END USER

- 20.4.1 MARKET SIZE & FORECAST

- 20.5 KEY COUNTRIES (VOLUME)

- 20.5.1 IRAN: MARKET SIZE & FORECAST

- 20.5.2 SAUDI ARABIA: MARKET SIZE & FORECAST

- 20.5.3 UAE: MARKET SIZE & FORECAST

- 20.5.4 TURKEY: MARKET SIZE & FORECAST

- 20.5.5 EGYPT: MARKET SIZE & FORECAST

21 LATIN AMERICA

- 21.1 MARKET SIZE & OVERVIEW

- 21.2 PROCESS

- 21.2.1 MARKET SIZE & FORECAST

- 21.3 PRODUCT TYPE

- 21.3.1 MARKET SIZE & FORECAST

- 21.4 END USER

- 21.4.1 MARKET SIZE & FORECAST

- 21.5 KEY COUNTRIES (VOLUME)

- 21.5.1 BRAZIL: MARKET SIZE & FORECAST

- 21.5.2 MEXICO: MARKET SIZE & FORECAST

- 21.5.3 REST OF LATIN AMERICA: MARKET SIZE & FORECAST

22 COMPETITIVE LANDSCAPE

- 22.1 COMPETITION OVERVIEW

23 KEY COMPANY PROFILES

- 23.1 CARGILL

- 23.1.1 BUSINESS OVERVIEW

- 23.1.2 PRODUCT OFFERINGS

- 23.1.3 KEY STRATEGIES

- 23.1.4 KEY STRENGTH

- 23.1.5 KEY OPPORTUNITIES

- 23.2 COMPASS MINERALS AMERICA

- 23.2.1 BUSINESS OVERVIEW

- 23.2.2 PRODUCT OFFERINGS

- 23.2.3 KEY STRATEGIES

- 23.2.4 KEY STRENGTH

- 23.2.5 KEY OPPORTUNITIES

- 23.3 DOMINION SALT

- 23.3.1 BUSINESS OVERVIEW

- 23.3.2 PRODUCT OFFERINGS

- 23.3.3 KEY STRATEGIES

- 23.3.4 KEY STRENGTH

- 23.3.5 KEY OPPORTUNITIES

- 23.4 RIO TINTO

- 23.4.1 BUSINESS OVERVIEW

- 23.4.2 PRODUCT OFFERINGS

- 23.4.3 KEY STRATEGIES

- 23.4.4 KEY STRENGTH

- 23.4.5 KEY OPPORTUNITIES

- 23.5 TATA CHEMICALS

- 23.5.1 BUSINESS OVERVIEW

- 23.5.2 PRODUCT OFFERINGS

- 23.5.3 KEY STRATEGIES

- 23.5.4 KEY STRENGTH

- 23.5.5 KEY OPPORTUNITIES

- 23.6 K+S AKTIENGESELLSCHAFT

- 23.6.1 BUSINESS OVERVIEW

- 23.6.2 PRODUCT OFFERINGS

- 23.6.3 KEY STRATEGIES

- 23.6.4 KEY STRENGTH

- 23.6.5 KEY OPPORTUNITIES

- 23.7 CHINA NATIONAL SALT INDUSTRY GROUP

- 23.7.1 BUSINESS OVERVIEW

- 23.7.2 PRODUCT OFFERINGS

- 23.7.3 KEY STRATEGIES

- 23.7.4 KEY STRENGTH

- 23.7.5 KEY OPPORTUNITIES

- 23.8 INEOS GROUP

- 23.8.1 BUSINESS OVERVIEW

- 23.8.2 PRODUCT OFFERINGS

- 23.8.3 KEY STRATEGIES

- 23.8.4 KEY STRENGTH

- 23.8.5 KEY OPPORTUNITIES

24 OTHER PROMINENT VENDORS

- 24.1 WILSON SALT

- 24.1.1 BUSINESS OVERVIEW

- 24.1.2 PRODUCT OFFERINGS

- 24.2 ICL SALT

- 24.2.1 BUSINESS OVERVIEW

- 24.2.2 PRODUCT OFFERINGS

- 24.3 IRISH SALT MINES

- 24.3.1 BUSINESS OVERVIEW

- 24.3.2 PRODUCT OFFERINGS

- 24.4 NOBIAN

- 24.4.1 BUSINESS OVERVIEW

- 24.4.2 PRODUCT OFFERINGS

- 24.5 DONALD BROWN GROUP

- 24.5.1 BUSINESS OVERVIEW

- 24.5.2 PRODUCT OFFERINGS

- 24.6 DELMON

- 24.6.1 BUSINESS OVERVIEW

- 24.6.2 PRODUCT OFFERINGS

- 24.7 MITSUI & CO.

- 24.7.1 BUSINESS OVERVIEW

- 24.7.2 PRODUCT OFFERINGS

- 24.8 MORTON SALT

- 24.8.1 BUSINESS OVERVIEW

- 24.8.2 PRODUCT OFFERINGS

- 24.9 ARCHEAN CHEMICAL INDUSTRIES

- 24.9.1 BUSINESS OVERVIEW

- 24.9.2 PRODUCT OFFERINGS

- 24.10 ZOUTMAN

- 24.10.1 BUSINESS OVERVIEW

- 24.10.2 PRODUCT OFFERINGS

- 24.11 SWISS SALT WORKS

- 24.11.1 BUSINESS OVERVIEW

- 24.11.2 PRODUCT OFFERINGS

- 24.12 SALINS GROUP

- 24.12.1 BUSINESS OVERVIEW

- 24.12.2 PRODUCT OFFERINGS

- 24.13 AMRA SALT FACTORY

- 24.13.1 BUSINESS OVERVIEW

- 24.13.2 PRODUCT OFFERINGS

- 24.14 CIECH GROUP

- 24.14.1 BUSINESS OVERVIEW

- 24.14.2 PRODUCT OFFERINGS

- 24.15 AMERICAN ROCK SALT

- 24.15.1 BUSINESS OVERVIEW

- 24.15.2 PRODUCT OFFERINGS

25 REPORT SUMMARY

- 25.1 KEY TAKEAWAYS

- 25.2 STRATEGIC RECOMMENDATIONS

26 QUANTITATIVE SUMMARY

- 26.1 MARKET BY GEOGRAPHY

- 26.2 MARKET BY PROCESS

- 26.3 MARKET BY PRODUCT TYPE

- 26.4 MARKET BY END USER

- 26.5 APAC

- 26.5.1 PROCESS

- 26.5.2 PRODUCT TYPE

- 26.5.3 END USER

- 26.6 NORTH AMERICA

- 26.6.1 PROCESS

- 26.6.2 PRODUCT TYPE

- 26.6.3 END USER

- 26.7 EUROPE

- 26.7.1 PROCESS

- 26.7.2 PRODUCT TYPE

- 26.7.3 END USER

- 26.8 MIDDLE EAST & AFRICA

- 26.8.1 PROCESS

- 26.8.2 PRODUCT TYPE

- 26.8.3 END USER

- 26.9 LATIN AMERICA

- 26.9.1 PROCESS

- 26.9.2 PRODUCT TYPE

- 26.9.3 END USER

27 APPENDIX

- 27.1 ABBREVIATIONS