|

|

市場調査レポート

商品コード

1453085

電気中型・大型バスの世界市場:技術の展望・動向・市場分析・予測 - 推進区分・構成・用途・地域別 - 予測(~2030年)Electric Mid- and Large Bus Market Technology Landscape, Trends and Market Analysis by Propulsion, Configuration, Application and Region - Global Forecast 2030 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 電気中型・大型バスの世界市場:技術の展望・動向・市場分析・予測 - 推進区分・構成・用途・地域別 - 予測(~2030年) |

|

出版日: 2024年01月26日

発行: MarketsandMarkets

ページ情報: 英文 122 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

電気中型・大型バス (9~14m) の市場規模は、予測期間中に14.4%のCAGRで推移し、2023年の6万6,593台から、2030年には17万1,000台の規模に成長すると予測されています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2023-2030年 |

| 基準年 | 2022年 |

| 予測期間 | 2023-2030年 |

| 単位 | 数量 (台) |

| セグメント | 推進区分 (BEV・FCEV・HEV/PHEV)・構成 (小型・大型)・用途 (シティ/トランジットバス・コーチ・ミディ&スクールバス)・地域 |

| 対象地域 | アジア太平洋・欧州・北米 |

予測期間中はBEVが最大の市場になる見込み:

BEVは予測期間中の市場をリードする見通しです。自動車OEMや政府機関は、環境問題に対する世界の意識の高まりとともにカーボンフットプリントの削減に努めており、BEVはこうした願望に合致しています。いくつかの政府機関は、既存の公共車両を電気モビリティソリューションに置き換える戦略を立てています。有利なインセンティブと税制上の優遇措置が提供されるため、先進的で長距離走行が可能なピュア電気中型・大型バスの販売は大幅に急増すると予想されています。また、ICEが30~40%であるのに比べ、BEVは約90%と比較的高い運行効率を持っています。BEVの平均航続距離は150~250マイルで、LFPやNMCなどの電池タイプによって異なります。この効率的な電池容量により、バスの動力源として使用される電気はディーゼルよりも安価で、バスの運行コストはさらに下がります。BEVは可動部品が少ないため、メンテナンスコストが低くなります。ピュア電気中型・大型バスの技術が進化し続けるにつれて、さまざまな用途や市場のニーズを満たすために、各種サイズや構成の電気中型・大型バスがより幅広く提供されるようになるでしょう。

スクールバスが北米市場でかなりの成長機会を持つ見通し:

スクールバスは米国のバス区分で主要な位置付けを占めており、2030年までにこの区分では約45%の電気化が見込まれています。拡大を促進する主な要因は、Environmental Protection Agency (EPA) によるClean School Bus Rebate Programであり、9億米ドル以上の資金が投入され、389の学区で2,400台以上の電気スクールバスが購入されました。また、北米のOEMはゼロエミッションバス技術に優れ、技術革新に力を入れています。先進的な電池技術により、これらの企業は効率的な電気中型・大型バスを開発し、今後数年間でスクールバス車両全体を電気化することを計画しています。

当レポートでは、世界の電気中型・大型バスの市場を調査し、市場概要、市場影響因子の分析、市場規模の推移・予測、各種区分・地域別の詳細分析などをまとめています。

目次

- 市場の定義

- 市場の分類

- 調査手法:地域およびパワートレイン別

- 電気バス市場に影響を与える要因

- EVの普及に伴う主要地域でのバス販売数

- 中型・大型バス市場の普及:世界

- 中型・大型バス市場の普及:世界 vs 中国

- 世界の中型・大型バス市場 (中国を含む)

- 世界の中型・大型バス市場 (中国を除く)

- 欧州と北米の中型・大型バス市場

- XEVの成長率

- 世界のバッテリー式電気中型・大型バス市場、用途別

- 北米のバッテリー式電気中型・大型バス市場:用途別

- 世界の中型・大型バス市場 (地域・推進区分別)

- 市場シェア分析:世界の中型・大型バス市場

- 欧州:電気中型・大型バス市場と主要OEM

- 電気バス市場:影響を与える主要動向

- クリーンビークル指令

- 主な電気バスOEM

- 中型・大型バス市場:パワートレイン別

- バッテリー式電気中型・大型バス市場:用途別

- バス販売台数 (国別) :ディーゼル/ガソリン/NG vs 電池電気

- 電気中型・大型バス市場とそのモデル:長さ・OEM別

- 市場シェア分析- 電気バスメーカーの大きな存在感

- TIVの成長

- 北米:電気中型・大型バス市場と主要OEM

- 電気バス市場:影響を与える主要動向

- 電気バス奨励プログラム

- 主要な電気バスOEM

- 中型・大型バス市場:パワートレイン別

- バッテリー式電気中型・大型バス市場:用途別

- バス販売台数 (国別) :ディーゼル/ガソリン/NG vs 電池電気

- 電気中型・大型バス市場 (長さ・OEM・モデル・車両規模別)

- OEMモデル、技術仕様、保有台数

- 米国:標準バスガイドライン

- 中国:中型・大型バスの電気バス市場と主要OEM

- 電気バス市場:影響を与える主要動向

- 電気バス奨励プログラムと交通バスと長距離バスへの補助金

- 主要な電気バスOEM

- 中型・大型バス市場:パワートレイン別

- バッテリー式電気中型・大型バス市場:用途別

- OEMモデルと技術仕様

- 市場シェア分析- 大手および中堅バスメーカーの大きな存在感

- アジア太平洋 (中国を除く) :中型・大型バス市場と主要OEM

- 中型・大型バス市場:パワートレイン別

- バッテリー式電気中型・大型バス市場:用途別

- バス販売台数 (国別) :ディーゼル/ガソリン/NG vs 電池電気

- アジア太平洋 (中国を除く) :電気バス市場の状況

- インド:中型・大型バスの電気バス市場と主要OEM

- 電気バス市場:影響を与える主要動向

- インド:電気バス市場の概要

- 中型・大型バス市場:パワートレイン別

- 電気バス受注数:都市・バスメーカー別

- デポ充電バリューチェーン・さまざまな運用モデル・主要企業

- 市場シェア分析と製品比較

- 競合ベンチマーキング

- 今後数年で補助金要件が上昇

- 電気バス市場の拡張エコシステム

- さまざまな条件による走行距離の変化

- 国別の外形サイズ制限 (規制・現在のハードウェア条件)

- ニーズグループ:乗客定員・乗客フロー別

- 長さ・乗客数/座席数:EV/ICE、1階建て

- 長さ・座席数:EV、1階建て

- 技術ロードマップ

- バリューチェーン分析

- 総所有コスト (TCO) と部品表 (BOM)

- 顧客グループ全体の主な動向

- 財務モデル

- ビジネス指標の推定

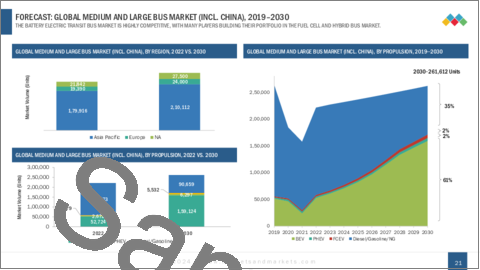

The global electric mid- and large (9-14m) bus market size is projected to grow from 66,593 units in 2023 to 171,000 units by 2030, at a CAGR of 14.4%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2030 |

| Base Year | 2022 |

| Forecast Period | 2023-2030 |

| Units Considered | Volume (Units) |

| Segments | Propulsion (BEV, FCEV, HEV/PHEV), Configuration (Light & Heavy Duty), Application (City/Transit Bus, Coach, Midi & School Bus) and Region |

| Regions covered | Asia Pacific, Europe, and North America |

The growth of the electric mid- & large bus market is primarily fueled by the impending emission regulations with stricter limits and a rising preference for sustainable transportation. Despite being in its early stages of development, the main challenge confronting this industry is the elevated cost of electric mid- & large buses in comparison to traditional diesel buses, mainly attributed to the substantial expense of batteries. The principal obstacle faced by this market revolves around safety apprehensions and the limited range associated with battery-powered buses.

Moreover, the growing focus on electrical infrastructure with supportive government efforts, as well as the development of charging stations, are some of the factors that will significantly contribute to market growth during the forecast period.

"BEV is expected to be the largest market in the forecast period."

BEV dominate the electric mid- & large bus market worldwide during the review period. Automotive OEMs and government agencies are striving to reduce the carbon footprint as worldwide awareness of environmental issues grows, and BEVs align with these aspirations. Several government agencies are strategizing to replace their existing public fleets with electric mobility solutions. With lucrative incentives and tax benefits provided, the sales of advanced and long-range pure electric mid- & large buses are anticipated to experience a significant surge. It also has relatively higher operational efficiency, about 90%, compared to ICE, which is 30-40%. The average range of BEVs is 150 to 250 miles and varies based on battery type installation such as LFP or NMC. Due to this efficient battery capacity, electricity used to power the buses is less expensive than diesel, further lowering the operational costs for buses. BEVs have fewer moving components, resulting in lower maintenance costs. As the technology for pure electric mid- & large buses continues to evolve, a broader range of electric mid- & large buses is likely to be available in different sizes and configurations to meet the needs of different applications and markets.

"School buses will have considerable growth opportunities in the North American market."

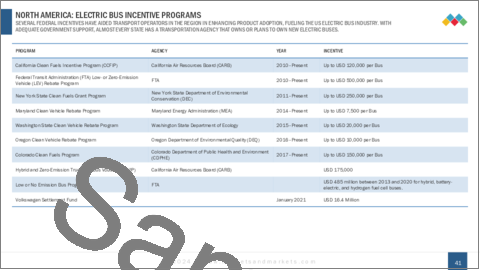

School Buses contribute a major portion of the US buses segment and around 45% electrification is expected in this segment by 2030. The predominant factor driving this expansion is the Clean School Bus Rebate Program by the LIS Environmental Protection Agency (EPA), which granted over USD 900 million for the acquisition of more than 2,400 electric school buses by 389 school districts. California continues to spearhead the adoption of electric school buses, with a commitment to over 1,800 units statewide, of which at least 35% are already delivered or in operation. This figure surpasses the next leading state, Maryland, by more than fivefold, as they have 361 commitments. Notably, New York experienced the most significant surge since September 2022, with 184 new commitments. OEMS in North America excels in zero-emission bus technology and has a strong focus on innovation. With advanced battery technology, these players are planning to develop efficient electric mid- & large buses to electrify the entire school bus fleet in the coming years.

"Europe is expected to be the second largest electric mid- and large (9-14m) bus market."

Europe offers a significant opportunity for the electric mid- & large bus market as the regulations related to the environment have become stringent in the region. These regulations drive market players to test and develop advanced vehicles, which will further boost the electric mid- & large bus market. According to the National Action Plan on Energy Efficiency, Germany aims to have at least 50% of all new buses purchased by public transport authorities and companies to be electric by 2025, with the target increasing to 100% by 2030. Europe is home to major electric mid- & large bus manufacturers and is renowned for innovations, cutting-edge R&D, and technological advancements in electric mid- & large bus. Government support through incentives and tax benefits, the presence of individual investors, and technological edge drive the European electric mid- & large bus market. European market to tend toward 100% BEV city/transit buses post 2025 and this will lead to markets such as Germany, France, and the UK having more than 3,000 BEV sales per year.

Breakdown of primaries

The study contains various industry experts' insights, from component suppliers to Tier 1 companies and OEMs. The break-up of the primaries is as follows:

By Company Type: OEMs - 80%, Tier I/Other players - 10%

By Designation: C level - 70%, Others- 30%

By Region: Asia Pacific - 70%, Europe - 20%, North America - 10%

The key players in the electric mid- & large bus market are BYD (China), Yutong (China), CAF (Solaris) (Spain), VDL Groep (Netherlands), and AB Volvo (Sweden). The key strategies adopted by major companies to sustain their position in the market are expansions, contracts and agreements, and partnerships. These companies have set up R&D facilities and offer best-in-class products to their customers.

Research Coverage:

The market study covers the electric mid- & large bus market by propulsion (BEV, HEV/PHEV, FCEV, and Diesel/Gasoline/NG), Configuration (Light Duty, Heavy Duty, Coach), Application (City/Transit Bus, Coaches, Midi Bus, and School Bus) and Region (Asia Pacific, Europe, and North America). It also covers the competitive landscape and company profiles of the major players in the electric mid- & large bus market ecosystem.

Key Benefits of the Report

The study also includes an in-depth competitive analysis of the key players in the market, along with their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall electric mid- & large bus market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (The increasing need for sustainable mass transit solutions and the need to reduce GHG emissions), restraints (Safety Concerns in EV batteries and high development costs), opportunities (Transition towards hydrogen fuel cell electric mobility, electric mid- & large bus as a service), and challenges (High cost of developing charging infrastructure) influencing the growth of the electric mid- & large bus market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the electric mid- & large bus market

- Market Development: Comprehensive information about lucrative markets - the report analyses the electric mid- & large bus market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the electric mid- & large bus market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like BYD (Build Your Dreams) (China), CRRC Electric (China), Yutong (China), and AB Volvo (Sweden), among others in the electric mid- & large bus market

TABLE OF CONTENTS

1. DEFINITIONS, RESEARCH METHODOLOGY, AND ASSUMPTIONS

- 1.1 MARKET DEFINITIONS

- 1.2 MARKET SEGMENTATION

- 1.2.1 BY CONFIGURATION AND SEATING CAPACITY

- 1.2.2 BY POWERTRAIN

- 1.3 RESEARCH METHODOLOGY, BY REGION AND POWERTRAIN

- 1.4 FACTORS INFLUENCING ELECTRIC BUS MARKET

2. EXECUTIVE SUMMARY

3. MARKET LANDSCAPE

- 3.1 BUS SALES ACROSS KEY REGIONS WITH EV PENETRATION

- 3.2 GLOBAL UPTAKE OF MEDIUM AND LARGE BUS MARKET

- 3.3 CHINA VS. GLOBAL UPTAKE OF MEDIUM AND LARGE BUS MARKET

- 3.4 GLOBAL MEDIUM AND LARGE BUS MARKET (INCL. CHINA)

- 3.5 GLOBAL MEDIUM AND LARGE BUS MARKET (EXCL. CHINA)

- 3.6 EUROPE AND NORTH AMERICA: MEDIUM AND LARGE BUS MARKET

- 3.7 GROWTH RATE OF XEVS

- 3.8 GLOBAL BATTERY ELECTRIC MEDIUM AND LARGE BUS MARKET, BY APPLICATION

- 3.9 NORTH AMERICA: BATTERY ELECTRIC MEDIUM AND LARGE BUS MARKET, BY APPLICATION

- 3.10 GLOBAL ELECTRIC MEDIUM AND LARGE BUS MARKET, BY REGION AND PROPULSION

- 3.11 MARKET SHARE ANALYSIS: GLOBAL MEDIUM AND LARGE BUS MARKET

- 3.12 EUROPE: ELECTRIC MEDIUM AND LARGE BUS MARKET AND KEY OEMS

- 3.12.1 EUROPE: ELECTRIC BUS MARKET - KEY INFLUENCING TRENDS

- 3.12.2 EUROPE: CLEAN VEHICLE DIRECTIVES

- 3.12.3 EUROPE: KEY ELECTRIC BUS OEMS

- 3.12.4 EUROPE: MEDIUM AND LARGE BUS MARKET, BY POWERTRAIN

- 3.12.5 EUROPE: BATTERY ELECTRIC MEDIUM AND LARGE BUS MARKET, BY APPLICATION

- 3.12.6 EUROPE: DIESEL/GASOLINE/NG VS. BATTERY ELECTRIC BUS SALES, BY COUNTRY

- 3.12.7 EUROPE: ELECTRIC MEDIUM AND LARGE BUS MARKET, BY LENGTH AND OEM, ALONG WITH THEIR MODELS

- 3.12.8 EUROPE: MARKET SHARE ANALYSIS - SIGNIFICANT PRESENCE OF ELECTRIC BUS MANUFACTURERS

- 3.12.9 GROWTH OF EUROPEAN TOTAL INDUSTRY VOLUME (TIV)

- 3.13 NORTH AMERICA: ELECTRIC MEDIUM AND LARGE BUS MARKET AND KEY OEMS

- 3.13.1 NORTH AMERICA: ELECTRIC BUS MARKET - KEY INFLUENCING TRENDS

- 3.13.2 NORTH AMERICA: ELECTRIC BUS INCENTIVE PROGRAMS

- 3.13.3 NORTH AMERICA: KEY ELECTRIC BUS OEMS

- 3.13.4 NORTH AMERICA: MEDIUM AND LARGE BUS MARKET, BY POWERTRAIN

- 3.13.5 NORTH AMERICA: BATTERY ELECTRIC MEDIUM AND LARGE BUS MARKET, BY APPLICATION

- 3.13.6 NORTH AMERICA: DIESEL/GASOLINE/NG VS. BATTERY ELECTRIC BUS SALES, BY COUNTRY

- 3.13.7 NORTH AMERICA: ELECTRIC MEDIUM AND LARGE BUS MARKET, BY LENGTH AND OEM, ALONG WITH THEIR MODELS AND FLEET SIZES

- 3.13.8 NORTH AMERICA: OEM MODELS, TECHNICAL SPECIFICATIONS, AND FLEET SIZES

- 3.13.9 US: STANDARD BUS GUIDELINES (HEIGHT, SEATING, AND PROCUREMENT-RELATED GUIDELINES)

- 3.14 CHINA: ELECTRIC MEDIUM AND LARGE BUS MARKET AND KEY OEMS

- 3.14.1 CHINA: ELECTRIC BUS MARKET - KEY INFLUENCING TRENDS

- 3.14.2 CHINA: ELECTRIC BUS INCENTIVE PROGRAMS AND SUBSIDIES FOR TRANSIT BUSES AND COACHES

- 3.14.3 CHINA: KEY ELECTRIC BUS OEMS

- 3.14.4 CHINA: MEDIUM AND LARGE BUS MARKET, BY POWERTRAIN

- 3.14.5 CHINA BATTERY ELECTRIC MEDIUM AND LARGE BUS MARKET, BY APPLICATION

- 3.14.6 CHINA: OEMS MODELS AND TECHNICAL SPECIFICATIONS

- 3.14.7 CHINA: MARKET SHARE ANALYSIS - SIGNIFICANT PRESENCE OF LARGE AND MEDIUM-SIZED BUS MAKERS

- 3.15 ASIA PACIFIC (EXCL. CHINA): ELECTRIC MEDIUM AND LARGE BUS MARKET AND KEY OEMS

- 3.15.1 ASIA PACIFIC (EXCL. CHINA): MEDIUM AND LARGE BUS MARKET, BY POWERTRAIN

- 3.15.2 ASIA PACIFIC (EXCL. CHINA): BATTERY ELECTRIC MEDIUM AND LARGE BUS MARKET, BY APPLICATION

- 3.15.3 ASIA PACIFIC (EXCL. CHINA): DIESEL/GASOLINE/NG VS. BATTERY ELECTRIC BUS SALES, BY COUNTRY

- 3.15.4 ASIA PACIFIC (EXCL. CHINA): ELECTRIC BUS MARKET CONDITIONS

- 3.16 INDIA: ELECTRIC MEDIUM AND LARGE BUS MARKET AND KEY OEMS

- 3.16.1 INDIA: ELECTRIC BUS MARKET - KEY INFLUENCING TRENDS

- 3.16.2 INDIA: ELECTRIC BUS MARKET OVERVIEW

- 3.16.3 INDIA: MEDIUM AND LARGE BUS MARKET, BY POWERTRAIN

- 3.16.4 INDIA: ELECTRIC BUS ORDERS RECEIVED, BY CITY AND BUS MANUFACTURER

- 3.16.5 INDIA: DEPOT CHARGING VALUE CHAIN WITH DIFFERENT OPERATION MODELS AND MAJOR COMPANIES

- 3.16.6 INDIA: MARKET SHARE ANALYSIS AND PRODUCT COMPARISON

- 3.16.7 INDIA: COMPETITIVE BENCHMARKING - 12 M ELECTRIC BUS SPECIFICATIONS FOR MAJOR PLAYERS

- 3.16.8 INDIA: SUBSIDY REQUIREMENTS TO RISE IN COMING YEARS

4. CONTENT INTRODUCTION

- 4.1 EXTENDED ELECTRIC BUS MARKET ECOSYSTEM

5. PRODUCT

- 5.1 DRIVING RANGE VARIATIONS UNDER DIFFERENT CONDITIONS

- 5.2 EXTERIOR SIZE LIMITATION, BY COUNTRY (REGULATIONS AND CURRENT HARDWARE CONDITIONS)

- 5.3 NEEDS GROUP, BY PASSENGER CAPACITY AND PASSENGER FLOW

- 5.4 LENGTH X PAX/NUMBER OF SEATS - EUR, EV/ICE, SINGLE-DECKER

- 5.5 LENGTH X NUMBER OF SEATS - EUR, EV, SINGLE-DECKER

- 5.6 TECHNOLOGY ROADMAP

- 5.6.1 ELECTRIC MOTOR TECHNOLOGY ROADMAP

- 5.6.2 FUTURE OF BATTERY CHEMISTRIES

- 5.6.3 BATTERY TECHNOLOGY ROADMAP

- 5.6.4 CHARGING STRATEGIES FOR ELECTRIC BUSES

- 5.6.5 GROWTH OF ELECTRIC BUS PLATFORMS

- 5.7 VALUE CHAIN ANALYSIS

- 5.8 TOTAL COST OF OWNERSHIP (TCO) AND BILL OF MATERIALS (BOM)

6. CUSTOMER REQUIREMENTS

- 6.1 KEY TRENDS ACROSS CUSTOMER GROUPS (OPERATORS/CITY, DRIVERS, USERS)

7. MOBILITY-AS-A-SERVICE (MAAS) BUSINESS MODEL FOR ELECTRIC BUSES

- 7.1 FINANCIAL MODELS

- 7.2 BUSINESS METRICS ESTIMATES

8. ELECTRIC BUS CASE STUDIES

9. RECOMMENDATIONS