|

市場調査レポート

商品コード

1849982

種子コーティング材料:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Seed Coating Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 種子コーティング材料:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月27日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

概要

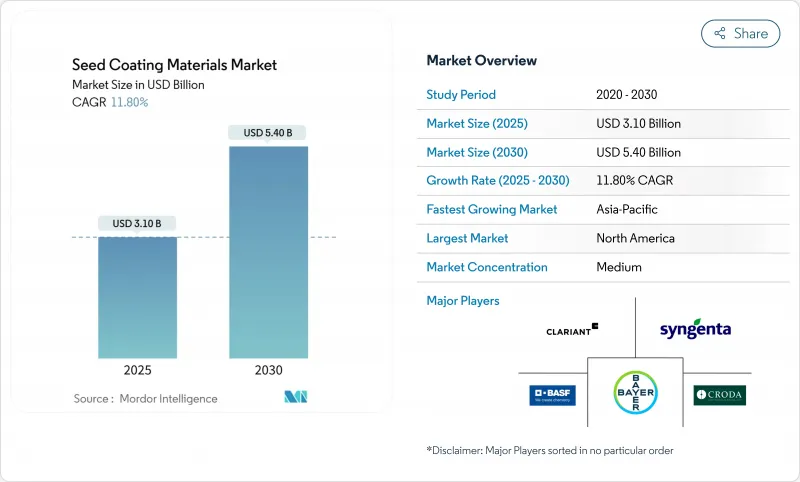

種子コーティング材市場は、2025年に31億米ドルと評価され、CAGR 11.80%で拡大し、2030年には54億米ドルに達すると予測されています。

成長の原動力は、精密農業の採用、環境規制の強化、ポリマーおよびバイオベースの化学物質における急速な技術革新です。欧州のマイクロプラスチック規制は生分解性バインダーへの軸足を加速させ、ブラジルのバイオ投入政策は植物由来および微生物由来フィルムの需要を強化しています。ナノテクノロジーと高吸水性ゲルによって、コーティング剤は遺伝子を保護し、発芽を促進し、水効率を改善する多機能プラットフォームとなりつつあります。アジア太平洋と南米は、生産者が気候変動と投入コストを管理するために近代化を進めているため、最も急速に普及が進んでいます。北米は、トウモロコシ、ダイズ、カノーラのアプリケーションにおいて、形質転換とコーティングの統合パッケージにより、規模のリーダーシップを維持しています。

世界の種子コーティング材料市場の動向と洞察

ハイブリッド種子とGM種子の拡大による高品質種子の需要

2024年後半までに、ケニアのBT綿やガーナのGMササゲを含む30カ国以上が商業的GM栽培を承認し、プレミアム種子の普及が世界的に拡大。環境保護庁は、トウモロコシ用のブレビバチルス・ラテロスポラス・タンパク質などの新しい植物組み込み型保護剤を認可し、次世代形質への道筋がよりスムーズになることを示唆しました。遺伝的価値が高まるにつれて、生産者は均一な出穂を確保し、高コストの形質を保護し、精密な植え付けを簡素化するコーティング剤を求めており、種子コーティング剤市場全体の需要を強化しています。

持続可能な農業への急速なシフト

ブラジルの生物投入物セグメントは2023~2024年シーズンに50億BRL(10億米ドル)に達し、年率15%の成長を記録し、生物投入物が規模で成功できることを証明しました。連邦法第15 070/2024号は現在、バイオ投入物専用の枠組みと資金を提供しています。欧州や米国でも同様の政策的シグナルがあり、現場での性能を犠牲にすることなく環境フットプリントを低減する植物由来のポリマー、でんぷんバインダー、微生物フィルムへの投資に舵を切っています。

石油由来のバインダーと顔料の価格変動

天然ガス価格の変動とパナマ運河とスエズ運河の貨物ボトルネックにより、化学原料コストが最大30%上昇し、合成皮膜メーカーの利幅が圧迫されています。複数の地域で供給契約を結んでいない小規模企業が最も大きなリスクに直面しており、地元産のデンプン結合剤に軸足を移しています。バイオベースの原料は現在、購入価格が高いが、そのコストプロファイルはより安定しており、種子コーティング剤市場における石油関連原料からの調達を促しています。

セグメント分析

ポリマーは、種子コーティング材市場における2024年の売上の38%を占めました。高吸水性ポリマーゲルは最も急速に成長している成分クラスで、CAGR 14.2%で急上昇しています。結合剤が29.4%で続き、添加剤は12%です。成分構成は、デンプンベースの結合剤、生分解性ポリマー、ナノ粒子添加剤へとシフトしており、価値の捕捉を高めています。酸化亜鉛とキトサンの複合体は発芽率を43%向上させ、ナノコーティングの可能性を示しています。全体として、高吸水性ゲルの種子コーティング材市場規模は、2030年までにほぼ倍増すると予想されます。

プレミアム価格は、ポリマーが接着、水分制御、栄養供給という複数の難点を一度に解決する場合に最も強くなります。デンプンやヘミセルロース結合剤のサプライヤーは、特に2028年の施行を前にマイクロプラスチック不使用の投入物を求める欧州で、早期の契約を獲得しています。アジア太平洋では、コストに敏感な生産者は依然としてポリ酢酸ビニルフィルムに頼っているが、持続可能性に関連した補助金制度によって、バイオベースの選択肢に徐々に軸足を移しつつあります。成分ポートフォリオが多様化するなか、化学企業と微生物新興企業間のライセンシング契約は、種子コーティング剤市場における次世代製剤の市場投入時期を早めています。

フィルムコーティングは、その薄く均一な層と高速プランターへの適合性により、2024年のプロセス収益の55%を占めました。ペレット化は、野菜、花卉、小粒種子の作付面積の増加に伴い、CAGR 15.5%を記録すると予測されます。包餡は24%のシェアで、穀物にとって依然として重要です。自動化、リアルタイムセンサー、低発塵製剤は性能格差を拡大し、種子コーティング材市場で企業がより高い価格を獲得するのに役立っています。

地域的な機器の嗜好がプロセス需要を形成しています。温室の多いオランダではペレット機が主流で、北米のトウモロコシ工場ではドラムフィルムコーターがリードしています。ラテンアメリカでは、輸出種子規格に対応するため、バッチコーターから連続ラインへのアップグレードが進んでおり、処理能力を25%向上させ、コーティングの過剰使用を削減しています。温度プローブ、エアフローモニタ、フィードレートアルゴリズムといった「モノのインターネット」(Internet-of-Things)レトロフィットを提供するベンダーは、ダウンタイムを削減し、サービス収益を強化しています。このような機能強化は買い手の信頼を高め、プロセス革新企業によるシードコーティング剤市場のシェア拡大を支えています。

地域分析

北米は2024年の種子コーティング剤市場シェアの35%を占め、精密植え付け、形質スタッキング、統合コーティングパッケージの普及に支えられています。サプライヤーはフィルム、微生物、潤滑剤を複数年の種子契約に組み入れ、2030年までCAGR9%で安定した採用を確保します。トウモロコシ、大豆、カノーラが処理ヘクタールの大半を占め、バイエルのアルバータ州カノーラ施設など、最近の垂直統合の動きはこの地域の価値を維持しています。気候変動に対応した農業のための官民資金援助も、作付面積を立地と水効率を向上させるプレミアム・コーティングに誘導しています。

アジア太平洋は最も急速に成長している地域で、CAGR 11.5%で成長し、種子コーティング剤の市場規模は北米に次いで2番目に大きいです。中国の種子活性化戦略とインドの2025年夏期播種量の6.5千ヘクタール増加が、ハイブリッド種子処理の需要を拡大しています。精密プランターや干ばつに強い品種に対する政府の補助金が、稲、小麦、園芸作物全体でフィルムやペレット化技術の採用を後押ししています。地元の製剤業者は多国籍の成分サプライヤーと提携し、地域の植え付け機器向けにでんぷん結合剤や着色添加剤をカスタマイズしています。

南米はCAGR 10.8%で続き、ブラジルが主導します。ブラジルは2023~2024年にバイオ投入量が15%増加し、大豆とトウモロコシの輸出用エコラベル付きコーティング剤をサポートします。欧州の厳格なマイクロプラスチック禁止令はレシピの形を変えつつあり、いち早くこれに対応するブランドを確保し、バリューチェーンのパートナーにコストプレミアムを転嫁するよう促しています。アフリカのCAGRは10.2%であるが、規制が断片的であるため市場浸透が遅れています。地域の研究機関との提携は、サプライヤーが熱帯の保管条件下で微生物コーティングを検証するのに役立ちます。これらの地域的な動きを総合すると、種子処理技術の世界的な成長見通しを維持しつつ、収益の流れを多様化することができます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- ハイブリッド種子と遺伝子組み換え種子の拡大による高品質種子の需要

- 持続可能な農業慣行への急速な移行

- ポリマーおよびバイオベースフィルム技術の継続的な革新

- マイクロプラスチックの差し迫った禁止により、環境に優しいコーティングの研究開発が加速

- 気候耐性作物栽培のための高吸水性ポリマーの採用

- 微生物コーティング種子を奨励する炭素クレジットプログラム

- 市場抑制要因

- 石油由来のバインダーと顔料の価格変動

- 多成分製剤の複雑なグローバル登録

- 種子に付着した生物活性物質の保存期間が限られている

- 今後のEU-27マイクロプラスチック規制を満たすための高価な改良

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 成分別

- バインダー

- ベントナイト

- ポリ酢酸ビニル

- ポリビニルピロリドン

- メチルセルロース

- スチレンブタジエンゴム

- アクリル

- ワックス/ワックスエマルジョン

- ポリマー

- フィルム形成ポリマー

- 高吸収性ポリマーゲル

- 添加剤

- 播種潤滑剤(シリコン、タルク、グラファイト)

- 肥料強化剤(微量栄養素分散剤、窒素阻害剤、溶剤)

- アジュバント

- 着色剤

- バインダー

- プロセス別

- フィルムコーティング

- 被覆

- ペレット化

- 機能別

- 種子保護

- 種子の強化

- 作物タイプ別

- 穀物

- 油糧種子

- 果物と野菜

- その他の作物

- コーティングの種類別

- 合成

- バイオベース

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- その他アジア太平洋地域

- 中東

- サウジアラビア

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Syngenta(Sinochem)

- BASF SE

- Bayer CropScience AG

- Clariant International(Clariant AG)

- Croda International

- Germains Seed Technology(Associated British Foods plc's)

- Precision Laboratories

- Roquette Group

- Brett Young

- Chromatech Incorporated

- Keystone Aniline Corporation(Milliken & Company)

- Lucent BioScience

- Michelman

- Nufarm Ltd.

- Ingredion Inc.