|

市場調査レポート

商品コード

1443981

自動車用センサ:市場シェア分析、産業動向、成長予測(2024~2029年)Automotive Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 自動車用センサ:市場シェア分析、産業動向、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 132 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

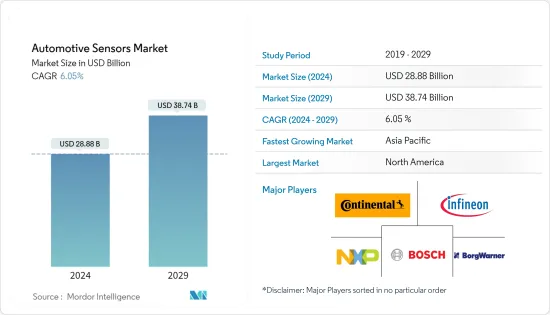

自動車用センサ市場規模は2024年に288億8,000万米ドルと推定され、2029年には387億4,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは6.05%で成長すると予測されます。

COVID-19パンデミックは、自動車用センサ市場を含む自動車産業に大きな影響を与えました。パンデミックの間、多くの自動車製造工場が閉鎖され、自動車の生産が減少し、その結果、自動車用センサの需要が減少しました。さらに、パンデミックによる世界のサプライチェーンの混乱は、原材料や部品の不足を招き、自動車用センサの生産にさらなる影響を与えました。

しかし、自動車用センサの市場は現在回復しつつあり、自動車産業の回復に伴ってセンサの需要も増加すると予想されます。パンデミックはまた、車載センサに大きく依存するADAS(先進運転支援システム)や自律走行車の採用を加速させました。長期的には、ADAS(先進運転支援システム)や自律走行車に対する需要の増加といった要因によって、自動車用センサ市場の成長が見込まれています。

自動車用センサは、車両の内部および外部環境から車両性能情報を検出、送信、分析、記録、表示するように設計された車両のコンポーネントです。車載センサの需要は、予測期間中に大幅に増加すると予想されます。これは、車両自動化の普及とコネクテッドカーに対する需要が世界中で高まっているためです。

さらに、顧客も新しい安全システムや技術に対する意識が高まっており、安全機能が向上した自動車を選択する傾向が強まっています。自動車メーカーは、乗客の安全に対する懸念が高まるにつれて、運転支援システムなどの機能を車両に装備する必要に迫られています。こうした要因がセンサの需要を押し上げています。

電動パワーステアリング(EPS)など複数の自動車用センサの使用は、 促進要因にさらなる安全上の利点を提供するのに役立っています。さらに、政府による厳しい燃費基準の採用や国際的な安全対策が、センサを多用する先進システム(EPSなど)の拡大・開発の主な促進要因となっています。

自動車産業におけるこれらの位置センサ用電子センサの需要は、技術の増大と継続的な開発およびブレークスルーの結果、拡大しています。その結果、自動車用センサ市場は予測期間を通じて大幅に増加すると予想されます。

自動車業界では最近、電動化や自律走行といった技術開発への注目が高まっており、センサの需要が高まっています。同時に、自動車メーカーが位置センサを自動車に組み込むことを選好していることから、同市場は今後も成長を続けるとみられます。

自動運転システムを搭載した自律走行車(特にレベル4とレベル5)は、一般に膨大な量のデータを処理して自動車システムにフィードバックを与え、交通標識に従って障害物を取り除いたり、旋回操作を行ったりしてスムーズに走行します。このため、この種の自動車にはより多くのセンサを組み込む必要があり、この分野の市場を牽引すると予想されます。

自動車用センサ市場の動向

政府の取り組みと、より安全な自動車システムの重視の高まりが市場を牽引

世界では毎年平均約124万人が交通事故で死亡しており、その半数は二輪車や歩行者のような交通弱者で、残りの半数は側面衝突の犠牲者です。

世界保健機関(WHO)によれば、世界で販売されている自動車の80%は、必須安全要件を満たしていないです。自動車の安全にとって最も重要な7つの規制一式は、まだ40カ国しか採用していません。

事故件数が大幅に増加しているため、エンドユーザーはより良い安全対策を採用するよう求められています。第一世界のすべての国で、道路や自動車の設計が進歩したおかげで、負傷率や死亡率は着実に減少しています。

一部の発展途上国では事故率がまだ高いため、各国政府は厳格な安全規制の施行に力を入れ、安全面を強化するセンサなどさまざまなサブシステムの自動車への採用を奨励しています。

このような要因が、自動車メーカー各社が自動車に多くの安全センサを追加する動機となっています。最新の自動車には、最先端のセキュリティや安全機能が搭載されています。消費者の安全システムや技術に対する関心が高まった結果、より優れた安全システムを搭載した自動車を選ぶようになりました。

さらに、世界の多くの国が、自動車の公害や燃費効率に関する厳しい規制を可決しています。米国のNHTSA(運輸省道路交通安全局)、欧州のICCT(国際クリーン輸送協議会)などの規制機関が、フリートレベルの要件を採用しています。これらの仕様は、自動車メーカーが従わなければならない最低排出ガスレベルを定めています。

以上の点から、対象市場は予測期間中に大きな成長が見込まれます。

アジア太平洋が市場を独占

予測期間中、アジア太平洋地域が収益面で大きな市場シェアを占めています。同地域全体での自動車販売台数の増加が、車載センサの需要を増加させると考えられます。また、同地域全体での電気自動車需要の高まりも市場成長を後押ししています。中国、インド、日本には製造業が多く存在し、市場の成長機会を生み出しています。

都市化の進展と安定した経済状況のため、新興経済諸国における自動車生産は先進経済諸国よりも急速に成長しています。新興経済諸国であるインドやASEAN諸国では、消費者の間で安全に対する関心が高まっており、自動車メーカーは低価格車により多くのセンサを搭載するようになっています。これは、当面の自動車用センサの需要を牽引すると予想されます。

世界で最も急速に経済成長している国のいくつかはAPAC地域にあり、中国とインドがその先頭を走っています。その結果、中産階級の消費者は、より多くの資金を持っているため、ADASのような先進機能を備えた自動車を購入する可能性が高くなっています。

ADAS(先進運転支援システム)や自動車用センサに依存するその他の安全機能の採用は、交通渋滞の緩和と交通安全強化のために、この地域の多くの政府が実施しているイニシアチブによって推進されています。他の地域よりも参入障壁が低いため、多くのAPAC諸国の規制環境は先進自動車技術の採用に有利です。

さらに、世界最大の電気自動車(EV)市場のいくつかはこの地域にあります。EVが電力供給を制御し、バッテリーの性能を監視するためにセンサに大きく依存しているという事実が、この地域の自動車用センサ需要を促進しています。

したがって、APAC地域は、自動車需要が高く、経済が急速に拡大し、政府の取り組みが奨励され、規制環境が良好で、電気自動車を重視する傾向が強まっているため、自動車用センサにとって最も重要な市場です。

自動車用センサ産業の概要

調査対象市場の主要企業には、Continental AG、Robert Bosch GmbH、Borgwarner Inc、Infineon Technologies、NXP Semiconductors、Denso Corporation、その他の企業が含まれます。こうした積極的な製品革新、提携などに加え、主要企業間のパートナーシップの拡大により、市場は大きな成長を遂げています。例えば

- 2023年1月、NXP Semiconductors N.V.(NXP)はCES 2023において、VinFastの新しい自動車プロジェクトの初期開発段階への参加を発表しました。VinFastはNXPのプロセッサー、半導体、センサの活用に努め、NXPは市場投入までの時間を短縮するためにトップクラスのソリューションを提供します。VinFast社は、NXP社のプロセッサー、半導体、センサを活用し、NXP社はトップクラスのソリューションを提供することで、市場投入までの時間を短縮します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ

- 温度センサ

- 圧力センサ

- 速度センサ

- レベル/位置センサ

- 磁気センサ

- ガスセンサ

- 慣性センサ

- 用途

- パワートレイン

- ボディエレクトロニクス

- 車両セキュリティシステム

- テレマティクス

- 車両タイプ

- 乗用車

- 商用車

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 欧州

- ドイツ

- 英国

- フランス

- その他欧州

- 世界のその他の地域

- ブラジル

- アラブ首長国連邦

- その他の国

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- DENSO Corporation

- Infineon Technologies AG

- Robert Bosch GmbH

- Texas Instruments Inc.

- Sensata Technologies Holding PLC

- Aptiv PLC(Delphi Automotive)

- CTS Corporation

- Maxim Integrated Products Inc.

- NXP Semiconductors NV

- Analog Devices Inc.

- Continental AG

- Littelfuse Inc.

- Hitachi Automotive Systems Americas Inc.

第7章 市場機会と今後の動向

The Automotive Sensors Market size is estimated at USD 28.88 billion in 2024, and is expected to reach USD 38.74 billion by 2029, growing at a CAGR of 6.05% during the forecast period (2024-2029).

The COVID-19 pandemic had a significant impact on the automotive industry, including the automotive sensors market. During the pandemic, many automotive manufacturing plants were shut down, which led to a reduction in the production of vehicles and consequently, a decrease in demand for automotive sensors. Additionally, the disruption in the global supply chain due to the pandemic resulted in a shortage of raw materials and components, which further affected the production of automotive sensors.

However, the market for automotive sensors is now recovering, and the demand for sensors is expected to increase as the automotive industry recovers. The pandemic has also accelerated the adoption of advanced driver assistance systems (ADAS) and autonomous vehicles, which rely heavily on automotive sensors. This is expected to drive the growth of the automotive sensors market in the coming years, as manufacturers increasingly incorporate these features into their vehicles.Over the long term, the automotive sensors market is expected to grow driven by the factors such as increasing demand for advanced driver assistance systems (ADAS) and autonomous vehicles.

Automotive sensors are components of a vehicle that are designed to detect, transmit, analyze, record, and display vehicle performance information from the vehicle's internal and external environments. The demand for automotive sensors is expected to rise significantly during the forecast period, owing to the growing popularity of vehicle automation and the growing demand for connected cars around the world.

Additionally, customers are also becoming more aware of new safety systems and technology, and they are increasingly selecting vehicles with improved safety features. Automotive manufacturers have been forced to equip their vehicles with features such as driver assistance systems, as passenger safety concerns have grown. Such factors are pushing the demand for sensors.

The use of several automobile sensors such as electric power steering (EPS) helps to provide the driver with extra safety benefits. Furthermore, the adoption of stringent fuel efficiency standards by government and international safety measures, are seen as major drivers for the expansion and development of advanced systems (such as EPS), which make extensive use of sensors.

The demand for electronic sensors for these position sensors in the automotive industry is expanding as a result of the increasing and continuous developments and breakthroughs in technology. As a result, the automotive sensor market is expected to increase significantly throughout the forecast period.

The automotive industry's recent shift in attention to technical developments such as electrification and autonomous driving has raised the demand for sensors. At the same time, the manufacturers' preference for integrating position sensors into vehicles suggests that the market will continue to grow.

Autonomous vehicles (especially level 4 and level 5) that feature self-driving systems generally process huge amounts of data to give feedback to the automotive system to drive smoothly clearing obstacles or performing turning maneuvers as per traffic signs. Due to this, it is expected that a greater number of sensors need to be incorporated into these types of vehicles, which is expected to drive the market for this segment.

Automotive Sensors Market Trends

Government Initiatives And The Growing Emphasis On Safer\sAutomotive Systems Driving The Market

Around 1.24 million people die in road accidents each year on average around the world, half of whom are vulnerable road users like motorcyclists and pedestrians, and the other half are victims of side-impact collisions.

80% of cars sold worldwide, according to the World Health Organization (WHO), do not meet the essential safety requirements. The complete set of the seven most crucial regulations for auto safety has only been adopted by 40 nations.

The number of accidents has significantly increased, which has prompted end users to adopt better safety measures. In all first-world nations, injury and death rates have steadily decreased thanks to advancements in road and vehicle design.

Governments are concentrating on enforcing strict safety regulations and encouraging the adoption of various subsystems such as sensors in vehicles that enhance the aspects of safety because accident rates are still higher in some developing countries.

These factors are motivating automakers to add a number of safety sensors to their vehicles. Modern cars can now be found with cutting-edge security and safety features. Consumers are now more interested in choosing vehicles that are outfitted with better safety systems as a result of their increased concern for safety systems and technologies.

Additionally, a number of nations around the world have passed strict regulations governing vehicle pollution and fuel efficiency. Regulatory bodies including the National Highway Traffic and Safety Administration (NHTSA) in the United States, the International Council on Clean Transportation (ICCT) in Europe, and other organizations have adopted fleet-level requirements. These specifications set a minimum emission level that automakers must follow.

Based on the aforementioned points, the target market is expected to grow at a significant rate during the forecast period.

Asia-Pacific Dominates the market

Asia-Pacific held a major market share in terms of revenue during the forecast period. A rise in vehicle sales across the region is likely to increase the demand for sensors in the vehicle. The rise in demand for electric vehicles across the region is also propelling the growth of the market. The major presence of manufacturing industries across China, India, and Japan is creating market growth opportunities.

Due to increasing urbanization and stable economic conditions, automotive production in developing economies is growing faster than in developed economies. With an increase in the safety concerns among the consumers in the developing economies of India and the ASEAN countries, automobile manufacturers are incorporating more sensors in low-cost vehicles. It is expected to drive the demand for automotive sensors in the foreseeable future.

Some of the world's fastest-growing economies are located in the APAC region, with China and India leading the way. As a result, consumers in the middle class are more likely to purchase vehicles with advanced features like ADAS because they have more money to spend.

The adoption of advanced driver assistance systems (ADAS) and other safety features that rely on automotive sensors has been driven by initiatives implemented by numerous governments in the region to reduce traffic congestion and enhance road safety. With lower entry barriers than in other regions, the regulatory environment in many APAC nations is favorable for the adoption of advanced automotive technologies.

Additionally, some of the world's largest markets for electric vehicles (EVs) are located in the region. The fact that EVs heavily rely on sensors to control power delivery and monitor battery performance is driving regional demand for automotive sensors.

Hence, APAC region is the most important market for automotive sensors because of its high demand for vehicles, rapidly expanding economy, encouraging government initiatives, favorable regulatory environment, and growing emphasis on electric vehicles.

Automotive Sensors Industry Overview

Some of the major players in the studied market include Continental AG, Robert Bosch GmbH, Borgwarner Inc, Infineon Technologies, NXP Semiconductors, Denso Corporation, and Others In addition to these active product innovations, collaborations, etc., the market is experiencing significant growth due to the growing partnership between major players. expected to give the market a good outlook over the forecast period. For instance,

- In January 2023, NXP Semiconductors N.V. (NXP) announced its participation in the early development phases of new VinFast automotive projects at CES 2023. VinFast will strive to leverage NXP's processors, semiconductors, and sensors, while NXP will provide top-tier solutions to speed time-to-market. The joint expert collaboration will focus on developing solutions for designing and producing cutting-edge EVs based on NXP's recognized reference assessment platforms and software layers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Temperature Sensors

- 5.1.2 Pressure Sensors

- 5.1.3 Speed Sensors

- 5.1.4 Level/Position Sensors

- 5.1.5 Magnetic Sensors

- 5.1.6 Gas Sensors

- 5.1.7 Inertial Sensors

- 5.2 Application

- 5.2.1 Powertrain

- 5.2.2 Body Electronics

- 5.2.3 Vehicle Security Systems

- 5.2.4 Telematics

- 5.3 Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Asia-Pacific

- 5.4.2.1 China

- 5.4.2.2 Japan

- 5.4.2.3 India

- 5.4.2.4 South Korea

- 5.4.2.5 Rest of Asia-Pacific

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Rest of Europe

- 5.4.4 Rest of the World

- 5.4.4.1 Brazil

- 5.4.4.2 United Arab Emirates

- 5.4.4.3 Other Countries

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 DENSO Corporation

- 6.2.2 Infineon Technologies AG

- 6.2.3 Robert Bosch GmbH

- 6.2.4 Texas Instruments Inc.

- 6.2.5 Sensata Technologies Holding PLC

- 6.2.6 Aptiv PLC (Delphi Automotive)

- 6.2.7 CTS Corporation

- 6.2.8 Maxim Integrated Products Inc.

- 6.2.9 NXP Semiconductors NV

- 6.2.10 Analog Devices Inc.

- 6.2.11 Continental AG

- 6.2.12 Littelfuse Inc.

- 6.2.13 Hitachi Automotive Systems Americas Inc.