|

市場調査レポート

商品コード

1440340

スマート生検デバイス:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年)Global Smart Biopsy Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| スマート生検デバイス:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

世界のスマート生検デバイス市場規模は、2024年に28億1,000万米ドルと推定され、2029年までに36億2,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に5.23%のCAGRで成長します。

新型コロナウイルス感染症(COVID 19)のパンデミック中、スマート生検デバイス市場は悪影響を受けました。たとえば、2021年1月に発表された「アイルランド北西部における小生検診断手順とがん切除手術に対する新型コロナウイルス感染症(COVID-19)の影響」というタイトルの調査研究では、診断と診断の両方の提供に重大な影響があると述べられています。COVID-19感染症のパンデミックによるアイルランド北西部の治療サービス。同様に、2020年11月に発表された別の調査研究「がん治療に対するCOVID-19症の影響:パンデミックが米国高齢者のがん診断と治療をどのように遅らせているのか」では、新型COVID-19感染症のパンデミックが米国のがん治療に及ぼす現在の影響について述べています。米国では、新たながんの発見と治療の提供が減少し、遅れが生じています。これらの問題が軽減されなければ、今後何年にもわたってがんの罹患率と死亡率が増加するでしょう。同様に、2021年3月に発表された「COVID-19感染症パンデミックが皮膚がん診断に及ぼす影響:集団ベースの研究」と題された別の調査研究では、新型COVID-19感染症パンデミックは前例のないものであり、緊急性のないがんの大幅な減少につながったと述べています。医療訪問。新型コロナウイルス感染症(COVID-19)症例の発症に伴い、総皮膚生検(予想の15%)、ケラチノサイトがん(KC)生検(18%)、黒色腫(27%)の急激な減少が見られました。請求による診断は、KC(99%)と黒色腫(98%)に対して高い特異性を示しましたが、感度は低かった(それぞれ61%と28%)。調整された分析では、高齢者(80歳以上)、女性、特定の地域の住民はパンデミック中に生検を受ける可能性が低かった。その後、10週間にわたって生検率が大幅に改善されました。したがって、短期的には市場は悪影響を受けましたが、パンデミック後は市場が成長する可能性があります。

がんの罹患率の増加により、市場は拡大しています。 Global Cancer Observatoryが発行したGlobocan 2020報告書では、世界 185か国における36のがんの罹患率と死亡率を推定しており、2020年に新たにがんと診断された患者数は推定19,292,789人、がんにより約9,958,133人が死亡したと推定されています。さらに、同じ情報源によると、新たながん症例数は2030年までに24,044,406人に達すると予想されており、世界中でがんの有病率が増加していることがわかります。がんの罹患率が高いと治療が必要となり、市場の成長が促進されます。同様に、GLOBOCAN 2020によれば、2020年には世界中で新たながん患者数が1,930万人に達すると推定されており、その数は2040年までに3,020万人に達すると推定されています。したがって、がんによる負担の増加が予想されることが主な要因です。生検の需要の高まりに貢献し、それによって市場の成長を促進します。

ただし、コア針生検の臨床上の問題は、今後の市場の成長を妨げるでしょう。

スマート生検デバイスの市場動向

乳がんは予測期間中にかなりの市場シェアを保持すると予想される

乳がんは女性に最も多く発生するがんであり、世界で2番目に多いがんです。世界がん調査基金国際データによると、2020年の新規感染者数は2,261,419人でした。 2020年のグロボカンの報告書によると、乳がんは最も罹患率が11.7%のがんの種類でした。同報告書によると、男女ともに5年間の有病率を見ると、アジアの罹患者数が3,218,496人(41.3%)で最も多く、次いで欧州の2,138,117人(27.4%)、北米の118万9,111人となっています。(15.3%)。このような乳がんの罹患率の高さは、診断目的で使用されるスマート生検デバイスの需要が増加すると予想される主な理由の1つです。米国では、乳がんの負担が特に高くなっています。 Breastcancer.orgによると、米国の女性では推定276,480人の新規浸潤性乳がん症例が診断されると予想され、48,530人の新たな非浸潤性乳がん症例、および2,620人の新たな浸潤性乳がん症例が予想されています。 2020年に男性で診断されました。

がん症例の増加により、治療用の斬新で先進的な生検装置を製造する市場関係者にチャンスが生まれています。さらに、USFDAが発表したデータによると、2021年10月に米国全土で実施されたマンモグラフィー処置の総数は約38,698,995件でした。したがって、マンモグラフィー検査の実施数の増加は、米国などの国々の市場の成長にプラスの影響を与える可能性があります。

製品の発売も市場成長のもう一つの要因です。たとえば、Izi Medical Productsは2021年 3月に、軟組織生検用のQuick-Core Auto Biopsy Systemを発売しました。 Quick-Core Autoは、同社の以前の半自動生検システムをベースにした軽量の全自動生検デバイスです。

したがって、前述の要因は、調査対象の市場の成長を促進するのに役立ちます。

予測期間中、北米が市場を独占すると予想される

北米は、がん症例数の増加、がん関連の研究開発への資金調達の可能性、主要な市場プレーヤーの存在、および主要な市場プレーヤーによるより大きなイニシアチブにより、予測期間を通じて市場全体を支配すると予想されます。

公的および民間組織による資金の増加は、市場の成長の重要な要因の1つです。たとえば、国立衛生研究所(NIH)の2020年の推計によると、乳がん調査に資金提供された金額は、国内のすべてのNIH研究所全体で、2019年は7億900万米ドル、2020年は768ドルでした。乳がんに対する資金の増加により、国内におけるデジタル乳がんスクリーニング法の研究開発の可能性が高まり、この分野の成長が促進されます。同様に、経済協力開発機構(OECD)によると、2019年のカナダの医療支出総額は2,082億米ドルに達しました。ヘルスケアへの投資は、多くの女性への償還と無料のマンモグラフィー検査の提供につながっています。マンモグラフィーの増加により、生検などの治療を必要とするがんと特定される患者の数が増加します。これにより市場の成長が促進される可能性があります。がん症例の増加も市場成長のもう1つの要因です。例えば、国際がん調査機関によると、2020年には29,929人の新たな乳がん症例が報告され、2040年までに最大46,315人に増加すると推定されています。カナダがん協会によると、推定27,400人の女性が乳がんと診断されています。 2020年までに国内で乳がんが増加し、2020年までに女性の新規がん患者全体の25%を占め、5,100人の女性が乳がんにより死亡します。

したがって、上記の要因により、市場は将来的に成長する可能性があります。

スマート生検デバイス業界の概要

市場シェアの点では、現在、いくつかの大手企業が市場を独占しています。現在市場を独占している企業としては、Danaher、Intuitive Surgical、CANON MEDICAL SYSTEMS CORPORATION、Boston Scientific Corporation、IMS Giotto SpAなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 低侵襲生検手順への関心の高まり

- がんの罹患率の増加

- 市場抑制要因

- コア針生検の臨床上の問題

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 用途別

- 乳がん

- 肝臓がん

- 皮膚ガン

- 前立腺がん

- その他

- エンドユーザー

- 病院

- 学術研究機関

- 診断センターと画像センター

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- ARGON MEDICAL

- B. Braun Melsungen AG

- Becton, Dickinson and Company

- Boston Scientific Corporation

- CR Bard

- CANON MEDICAL SYSTEMS CORPORATION

- Cook Medical

- Danaher

- IMS Giotto SpA

- INRAD, Inc.

- Intuitive Surgical

- PLANMED OY

第7章 市場機会と将来の動向

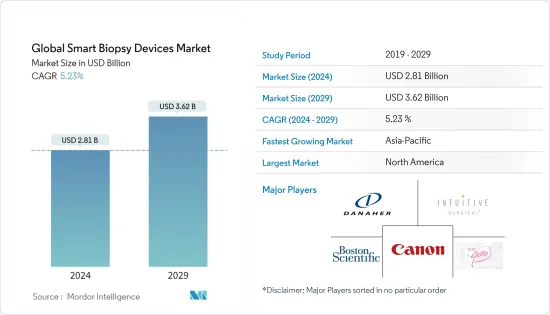

The Global Smart Biopsy Devices Market size is estimated at USD 2.81 billion in 2024, and is expected to reach USD 3.62 billion by 2029, growing at a CAGR of 5.23% during the forecast period (2024-2029).

During the COVID 19 pandemic, the smart biopsy devices market was adversely affected. For instance, in January 2021, a research study published titled "Impact of COVID-19 on small biopsy diagnostic procedures and cancer resection surgeries in the North-West of Ireland" stated that there has been a significant impact on the provision of both diagnostic and therapeutic services in North-West of Ireland due to the COVID-19 pandemic. Similarly, another research study published in November 2020, titled "Impact of COVID-19 on Cancer Care: How the Pandemic Is Delaying Cancer Diagnosis and Treatment for American Seniors" stated that the current impact of the COVID-19 pandemic on cancer care in the United States has resulted in decreases and delays in identifying new cancers and delivery of treatment. These problems, if unmitigated, will increase cancer morbidity and mortality for years to come. Similarly, another research study published in March 2021, titled "Impact of the COVID-19 pandemic on skin cancer diagnosis: A population-based study" stated that the COVID-19 pandemic has been unprecedented and has led to drastic reductions in non-urgent medical visits. A precipitous drop in total skin biopsies (15% of expected), biopsies for keratinocyte carcinoma (KC) (18%) and melanoma (27%) was seen with the onset of COVID-19 cases. Claims diagnoses were of high specificity for KC (99%), and for melanoma (98%), though sensitivity was less (61% and 28% respectively). In adjusted analysis, the elderly (80+ years), females and residents of certain regions were less likely to be biopsied during the pandemic. Subsequently, there were substantial improvements in biopsy rates over 10 weeks. Hence, in the short term the market was negatively impacted however, post pandemic the market is likely to grow.

The market is increasing due to increasing prevalence of cancer. The Globocan 2020 report published by Global Cancer Observatory, which estimated the incidence and mortality of 36 cancer in 185 countries, globally, there were an estimated 19,292,789 new cases of cancer diagnosed in 2020 and about 9,958,133 people died due to cancer, all over the world. Further, as per the same source, the number of new cancer cases are expected to reach 24,044,406 by 2030, which shows an increasing prevalence of cancer around the globe. High prevalence of cancer will require treatment and will increase the growth of the market. Similarly, as per the GLOBOCAN 2020, in 2020, there were 19.3 million estimated number of new cancer cases worldwide, and the number is estimated to reach 30.2 million by the year 2040. Thus, the anticipated increase in burden of cancer is a major factor contributing to the rising demand for biopsy, thereby boosting the market growth.

However, the clinical issues with core needle biopsy will hinder the market growth in upcoming future.

Smart Biopsy Devices Market Trends

Breast Cancer is Expected to Hold a Significant Market Share Over the Forecast Period

Breast cancer is the most commonly occurring cancer in women and the second most common cancer overall in the world. There were 2,261,419 new cases in 2020, according to World Cancer Research Fund International data. According to a Globocan report in 2020, breast cancer was the most prevalent type of cancer with a prevalence rate of 11.7%. According to the same report, the five-year prevalence rate for both the sexes showed that Asia had the highest number of people affected at 3,218,496 (41.3%), followed by Europe at 2,138,117 (27.4%) and North America with 1.189,111 people (15.3%). Such high prevalence rates of breast cancer is one of the main reasons for the demand for smart biopsy devices is expected to increase, as they will be used for diagnostic purposes. In the United States, the burden of breast cancer is particularly high. According to Breastcancer.org, an estimated 276,480 novel cases of invasive breast cancer were expected to have been diagnosed in women in the United States, along with 48,530 new cases of non-invasive breast cancer, and 2,620 new cases of invasive breast cancer were expected to have been diagnosed in men in 2020.

The increasing number of cancer cases is creating opportunities for the market players who are producing novel and advanced biopsy devices for treatment. Moreover, as per the data published by USFDA, in October 2021, the total number of mammography procedures performed across the United States was around 38,698,995. Therefore, the increasing number of mammography tests performed are likely to have a positive impact on the growth of the market in countries, like the United States.

Product launches are another factor for the growth of the market. For instance, in March 2021, Izi Medical Products launched its Quick-Core Auto Biopsy System for soft tissue biopsies. Quick-Core Auto is a lightweight, fully automatic biopsy device that builds upon the company's previous semi-automatic biopsy system. The Quick-Core Auto is a great solution for all soft tissue biopsy needs and complements Izi's women's health offering, which includes Indicator markers used during mammograms, Quick-Core, Quick-Core Auto and ColdCare Packs for biopsy sampling, and Kopans and X-Reidy localization wires used for breast localization.

Hence, the aforesaid factors help in driving the growth of the market studied.

North America is Expected to Dominate the Market Over the Forecast Period

North America is expected to dominate the overall market through the forecast period due to the increasing number of cancer cases, availability of funding for cancer-related research and development, the presence of key market players, and greater initiative by major market players.

Increasing funding by public and private organizations is one of the key factors for the growth of the market. For instance, according to the National Institute of Health (NIH) 2020 estimates, the amount funded for breast cancer research was USD 709 million for 2019, and USD 768 for 2020 across all the NIH institutes in the country. The growing funding for breast cancer increases the possibilities of research and development of digital breast cancer screening methods in the country, boosting the segment growth. Similarly, according to the Organization for Economic Co-operation and Development (OECD), in 2019, Canada's total health spending reached USD 208.2 billion in 2019. Investments in healthcare get translated into providing many women with reimbursements and free mammography exams. Increasing mammography will increase the number of patient identified with cancer who would require treatment including biopsy. This is likely to boost market growth. Increasing cancer cases is another factor for the growth of the market. For instance, according to the International Agency for Research on Cancer, 29,929 new breast cancer cases were reported for 2020, which are estimated to increase up to 46,315 by the year 2040. According to the Canadian Cancer Society, an estimated 27,400 women were diagnosed with breast cancer in the country by 2020, representing 25% of all new cancer cases in women by 2020, with 5,100 women dying from breast cancer.

Hence, due to above mentioned factors the market is likely to grow in the future.

Smart Biopsy Devices Industry Overview

In terms of market share, a few of the major players are currently dominating the market. Some of the companies which are currently dominating the market are Danaher, Intuitive Surgical, CANON MEDICAL SYSTEMS CORPORATION, Boston Scientific Corporation, and IMS Giotto S.p.A

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Preference for Minimally Invasive Biopsy Procedure

- 4.2.2 Increasing Prevalence of Cancer

- 4.3 Market Restraints

- 4.3.1 Clinical Issues With Core Needle Biopsy

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Application

- 5.1.1 Breast Cancer

- 5.1.2 Liver Cancer

- 5.1.3 Skin Cancer

- 5.1.4 Prostate Cancer

- 5.1.5 Others

- 5.2 End User

- 5.2.1 Hospitals

- 5.2.2 Academic and Research Institutes

- 5.2.3 Diagnostic and Imaging Centers

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East & Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East & Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 ARGON MEDICAL

- 6.1.2 B. Braun Melsungen AG

- 6.1.3 Becton, Dickinson and Company

- 6.1.4 Boston Scientific Corporation

- 6.1.5 C. R. Bard

- 6.1.6 CANON MEDICAL SYSTEMS CORPORATION

- 6.1.7 Cook Medical

- 6.1.8 Danaher

- 6.1.9 IMS Giotto S.p.A

- 6.1.10 INRAD, Inc.

- 6.1.11 Intuitive Surgical

- 6.1.12 PLANMED OY