|

市場調査レポート

商品コード

1440330

セルフケア医療機器:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年)Global Self Care Medical Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| セルフケア医療機器:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 119 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

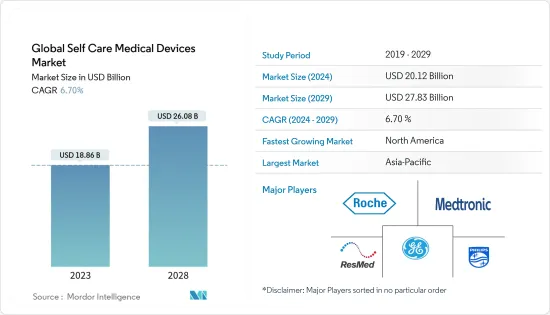

世界のセルフケア医療機器市場規模は、2024年に201億2,000万米ドルと推定され、2029年までに278億3,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に6.70%のCAGRで成長します。

世界的に、新型コロナウイルス感染症(COVID-19)のパンデミックは、人員不足で過重労働となっている病院やヘルスケアシステムに多大な圧力をかけています。 2022年 1月にヘルスケア管理フォーラムに掲載された「新型コロナウイルスのパンデミック中の在宅医療モニタリング:アルバータ州のプライマリケアにおける実現可能性研究の結果」と題された研究によると、患者は在宅ヘルスケアモニタリング技術に満足しており、60%以上が患者は追跡調査後に生活の質の改善を報告しました。患者がかかりつけ医や救急外来を受診する頻度も前年より減少しました。さらに、2020年11月にJournal of Family Medicine and Primary Careに掲載された「糖尿病と高血圧の併存疾患を抱えて暮らす人々に対する、COVID-19感染症のパンデミックにおけるセルフケアの役割」と題された研究によると、食事の予防策、服薬アドヒアランス、在宅ベースのエクササイズ、血糖値と血圧の自己測定、減塩、足の自己検査、ストレス管理はすべて、セルフケアに必要な要素として示唆されています。したがって、セルフケアを監視するために、COVID-19の期間中、セルフケアデバイスの需要が増加しました。したがって、セルフケア医療機器は、COVID-19感染症のパンデミック中にプラスの影響を受けました。

心血管疾患(CVD)や糖尿病などの慢性疾患や生活習慣病の有病率の上昇や、消費者の健康意識の高まりにより、患者の健康状態を継続的に追跡できるデバイスの需要が高まっています。世界保健機関による2021年 7月の最新情報によると、心血管疾患は世界中で主な死因となっており、これには冠状動脈性心疾患、脳血管疾患、リウマチ性心疾患、先天性心疾患などが含まれます。さらに、国際糖尿病連盟(IDF)の糖尿病アトラス第10版2021年版が発表したデータによると、2021年には約5億3,700万人の成人(20~79歳)が糖尿病を抱えて暮らしていました。同関係者は、糖尿病を抱えて生きる人の総数は2030年までに6億4,300万人、2045年までに7億8,300万人に増加すると予測していると推定しています。糖尿病の負担の増大により、より技術的に進んだセルフケア医療機器の需要が高まる可能性が高いです。

さらに、WHOによると、2030年までに地球上の6人に1人が60歳以上になるとのことです。 60歳以上の人口は、2020年の10億人から2050年までに14億人に増加すると予想されています。2050年までに、世界の60歳以上の人口は2倍の21億人に達すると予想されます。 2020年から2050年の間に、80歳以上の人口は3倍の4億2,600万人に達すると予想されています。

市場関係者は、市場収益を増やすために、製品の発売、製品開発、コラボレーション、拡張などのさまざまな戦略を採用しました。たとえば、2021年11月、世界のヘルスケア企業であるアボットは、インドの糖尿病を抱えて暮らす大人と子供(4歳以上)、および妊娠糖尿病(糖尿病)の女性が利用できる持続血糖モニタリング(CGM)技術であるFreeStyle Libreシステムを発表しました。妊娠中など、いつでもどこからでも血糖値をチェックできるため、血糖コントロールが向上します。

したがって、前述のすべての要因が予測期間中に市場を牽引すると予想されます。ただし、代替デバイスの入手可能性と製品の高コストにより、予測期間中の市場は制限されます。

セルフケア医療機器市場動向

血糖モニターセグメントは、予測期間中に市場を独占すると予想されます

血糖モニターは、他のセルフケア医療機器と比較して最大の市場シェアを獲得しました。糖尿病と診断される人の数は、座りっぱなしのライフスタイル、悪い食生活、高齢者人口の増加により着実に増加しています。さらに、技術の進歩と糖尿病管理に対する意識の高まりにより、血糖モニター市場は予測期間中に成長します。たとえば、国際糖尿病連盟の2021年 9月の報告書によると、2021年には約5億3,700万人の成人(20~79歳)が糖尿病を抱えて暮らしています。糖尿病を抱えて生きる人の総数は、2030年までに6億4,300万人、2045年までに7億8,300万人に増加すると予測されています。

この国の市場関係者は、市場収益を増やすために、製品の発売、製品開発、コラボレーション、拡大などのさまざまな戦略を採用しました。 2021年7月、テルモ株式会社は、Dexcom G6連続血糖モニタリングシステムを日本で発売しました。本製品は米国に本拠を置くDexcom, Inc.が製造し、日本ではテルモが独占販売契約を結んでいます。

同様に、2021年 11月に、POGO自動血糖モニタリングシステム(Intuity Medical)が、13歳以上の糖尿病患者を対象として食品医薬品局によって認可されました。米国では、新しいタイプの血糖値監視システムにより、ユーザーは指を突っ込んだり、測定器にテストストリップを挿入したりするのではなく、ボタンを1回押すだけで検査できるようになりました。

したがって、前述のすべての要因が予測期間中のセグメントの成長を促進すると予想されます。

北米が市場を独占しており、予測期間中も同様に成長すると予想されます。

政府当局の支援による新製品の増加に伴い、慢性疾患の負担の増大と高齢者人口の増加により、米国ではセルフケア医療の需要が高まっています。

新型コロナウイルス感染症(COVID-19)のパンデミックは、米国のヘルスケア提供の情勢を変え、セルフケアモニタリングへの新たな移行をもたらしました。 また、米国でのCOVID-19感染症のパンデミック中の2020年 4月には、米国北東部で提出された医療および歯科の請求のうち、遠隔医療の請求が20%を占めました。

疾病管理予防センター(CDC)が発行した2022年1月に更新された全国糖尿病統計報告書によると、約3,730万人(米国人口の11.3%)が糖尿病を患っています。さらに、同じ情報源によると、2021年には成人2,850万人を含む2,870万人が糖尿病と診断されたとのことです。さらに、2020年7月に発表された「高齢者と人口高齢化の統計」と題されたカナダ統計局の報告書によると、高齢者の数は2020年の65歳以上の人口は約6,835,866人です。心疾患などの慢性疾患は高齢者層での罹患率が高く、高齢者層に影響を与える可能性がより高いため、高齢者層の負担が患者監視システムの需要を高めることになります。これにより、この地域におけるセルフケア医療機器の需要が高まります。

さらに、米国の高い成長の可能性により、同国で事業を展開している企業は競合他社よりも優位に立つために新製品の承認を申請しており、これにより調査対象となっている米国の市場の予測期間の成長がさらに拡大すると予想されています。たとえば、2021年 1月にオムロンヘルスケアは、初のウェアラブル血圧計であるハートガイドの小売可能性を報告しました。大いに期待されていた腕時計型オシロメトリック血圧モニターであるHeartGuideは、医療機器として510,000のFDA認可を取得しました。

セルフケア医療機器業界の概要

セルフケア医療機器市場は適度に細分化されています。さまざまな医療機器メーカーが市場で活動しており、セルフケア医療機器の専門メーカーも数社あります。業界は競争が激しく、セルフケア医療機器の機能を自社の機器に組み込むために、業界参加者と他の医療機器メーカーとの間でパートナーシップや協定を結ぶ傾向が高まっています。主要な市場プレーヤーには、Medtronic plc.、Koninklijke Philips NV、Bayerヘルスケア LLC、General Electric Company、F. Hoffmann-La Roche AG、Johnson &Johnsonなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 高齢者人口の増加に伴う慢性疾患や生活習慣病の負担の増加

- 多忙なライフスタイルにより在宅治療への関心が高まる

- 市場抑制要因

- 代替オプションの入手可能性、およびデバイスの高コスト

- セルフケア医療機器の埋め込みに伴う副作用とリスク

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- タイプ別

- 血糖モニター

- 血圧計

- 体温モニター

- ネブライザー

- 歩数計

- 妊娠/妊孕性検査キット

- その他

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Medtronic plc.

- Koninklijke Philips NV

- Bayer HealthCare LLC

- General Electric Company

- F. Hoffmann-La Roche AG

- Johnson &Johnson

- ResMed, Inc.

- Omron Healthcare, Inc.

- OraSure Technologies, Inc.

- Abbott Inc.

- B. Braun Melsungen

第7章 市場機会と将来の動向

The Global Self Care Medical Devices Market size is estimated at USD 20.12 billion in 2024, and is expected to reach USD 27.83 billion by 2029, growing at a CAGR of 6.70% during the forecast period (2024-2029).

Globally, the COVID-19 pandemic put enormous pressure on hospitals and healthcare systems that were understaffed and overworked. According to the study titled "Home health monitoring during the COVID pandemic: Results from a feasibility study in Alberta primary care," published in the Healthcare management forum in January 2022, Patients were comfortable with the home healthcare monitoring technology, and more than 60% patients reported an improvement in their quality of life after follow-up. Patients also visited their family physician/emergency department less frequently than in the previous year. Moreover, according to the study titled "Role of self-care in COVID-19 pandemic for people living with comorbidities of diabetes and hypertension" published in the Journal of Family Medicine and Primary Care in November 2020, Dietary precautions, medication adherence, home-based exercises, self-monitoring of blood glucose and blood pressure, salt reduction, self-foot examination, and stress management are all suggested as necessary elements of self-care. Thus, to monitor self-care, the demand for self-care devices increased during COVID-19. Thus, self-care medical devices were positively impacted during the COVID-19 pandemic.

There has been an increase in demand for devices that can continuously track patients' physical well-being due to the rising prevalence of chronic and lifestyle diseases such as cardiovascular disease (CVD) and diabetes, as well as rising consumer health awareness. According to the July 2021 update by the World Health Organization, cardiovascular diseases are the leading cause of death around the world, including diseases like coronary heart disease, cerebrovascular disease, rheumatic heart disease, congenital heart disease, and others. Additionally, according to the data published by the International Diabetes Federation (IDF) Diabetes Atlas Tenth Edition 2021, in the year 2021, approximately 537 million adults (aged 20-79 years) were living with diabetes. The same source estimated that the total number of people living with diabetes is projected to rise to 643 million by 2030 and 783 million by 2045. The rising burden of diabetes is likely to increase the demand for more technically advanced self-care medical devices.

Furthermore, according to the WHO, by 2030, one out of every six people on the planet will be 60 years old or older. The number of people aged 60 and up is expected to rise from 1 billion in 2020 to 1.4 billion by 2050. By 2050, the global population of people aged 60 and above will get double to reach 2.1 billion. Between 2020 and 2050, the number of people aged 80 and above is expected to triple, reaching 426 million.

The market players adopted various strategies such as product launches, product developments, collaborations, and expansions to increase their market revenue. For instance, in November 2021, Abbott, the global healthcare launched the FreeStyle Libre system, the continuous glucose monitoring (CGM) technology available for adults and children (above the age of four) living with diabetes in India and women with gestational diabetes (diabetes during pregnancy), allowing them to check their glucose levels at any time and from any location, resulting in better glucose control.

Thus, all aforementioned factors are anticipated to drive the market over the forecast period. However, the availability of alternative devices and the high cost of the products restraint the market over the forecast period.

Self Care Medical Devices Market Trends

Blood Glucose Monitors Segment is Expected to Dominate the Market Over the Forecast Period

Blood glucose monitors had the largest market share when compared to other self-care medical devices. The number of people diagnosed with diabetes has been steadily increasing due to sedentary lifestyles, poor dietary habits, and the growing geriatric population. Furthermore, technological advancements and growing awareness about diabetes management are driving the market for blood glucose monitors to grow over the forecast period. For instance, as per the September 2021 report of the International Diabetes Federation, in 2021, approximately 537 million adults (20-79 years) were living with diabetes. The total number of people living with diabetes is projected to rise to 643 million by 2030 and 783 million by 2045.

The market players in the country adopted various strategies such as product launches, product developments, collaborations, and expansions to increase their market revenue. In July 2021, Terumo Corporation launched Dexcom G6 continuous glucose monitoring system in Japan. Dexcom, Inc., based in the United States, manufactures the product and Terumo holds the exclusive distribution agreement in Japan.

Similarly, in November 2021, The POGO Automatic Blood Glucose Monitoring System (Intuity Medical) was cleared by the Food and Drug Administration for people with diabetes aged 13 and up. In the United States, a new type of blood sugar monitoring system allows users to test with a single button press rather than finger-sticking or inserting test strips into a meter.

Thus, all aforementioned factors are anticipated to drive the segment growth over the forecast period.

North America Dominates the Market and Expected to do Same in the Forecast Period.

With the increase in product launches supported by the government authorities, the rising burden of chronic diseases and the increasing geriatric population are leading to a rise in demand for self-care medical in the United States.

The COVID-19 pandemic has changed the landscape of healthcare delivery in the United States, with a new shift toward self-care monitoring. According to a research article by Darren Roblyer published in the Journal of Biomedical Optics in October 2020, industrial and academic research projects use these devices to predict a variety of health outcomes and disease states, including surgical recovery, overall mortality, mental health, heart conditions, and other diseases states. Adding to that, in April 2020, during the COVID-19 pandemic in the United States, telehealth claims accounted for 20% of submitted medical and dental claims in the northeastern United States.

According to the National Diabetes Statistics Report updated in January 2022 published by the Centers for Disease Control and Prevention (CDC), around 37.3 million people have diabetes (11.3% of the United States population). Additionally, as per the same source, 28.7 million people, including 28.5 million adults were diagnosed with diabetes in 2021. Furthermore, according to the Statistics Canada Report titled 'Older adults and population aging statistics, published in July 2020, the number of people aged 65 years or over is about 6,835,866 in 2020. Since chronic diseases such as cardiac diseases have a high prevalence in the older population and have more chances to affect the older population, the burden of the geriatric population will drive the demand for patient monitoring systems, thereby boosting the demand for self-care medical devices in the region.

In addition, due to the high growth potential of the United States, the companies operating in the country are filing for new product approvals to have an edge over their competitors, which is further expected to augment the growth of the studied market in the country over the forecast period. For Instance, in January 2021, Omron Healthcare reported retail availability for HeartGuide, the first wearable blood pressure monitor. The highly-anticipated HeartGuide, an oscillometric blood pressure monitor in the design of a wrist watch, received 510K FDA clearance as a medical device.

Self Care Medical Devices Industry Overview

The self-care medical devices market is moderately fragmented. Various medical device manufacturers are operating in the market, along with several specialized self-care medical device manufacturers. The industry is highly competitive, and there is a growing trend of partnerships and agreements between the industry participants and other medical device manufacturers to incorporate self-care medical device functionalities into their devices. Some of the key market players include Medtronic plc., Koninklijke Philips N.V., Bayer HealthCare LLC, General Electric Company, F. Hoffmann-La Roche AG, and Johnson & Johnson.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Burden of Chronic Diseases and Lifestyle Diseases Coupled with The Geriatric Population

- 4.2.2 Growing Preference for Home- Based Treatment Due to Hectic Lifestyle

- 4.3 Market Restraints

- 4.3.1 Availability Of Alternative Options, And High Costs of Devices.

- 4.3.2 Side Effects and Risks Associated with Implantation of Self-Care Medical Devices

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Type

- 5.1.1 Blood Glucose Monitors

- 5.1.2 Blood Pressure Monitors

- 5.1.3 Body Temperature Monitors

- 5.1.4 Nebulizers

- 5.1.5 Pedometers

- 5.1.6 Pregnancy/Fertility Test Kits

- 5.1.7 Others

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Australia

- 5.2.3.5 South Korea

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 Middle-East and Africa

- 5.2.4.1 GCC

- 5.2.4.2 South Africa

- 5.2.4.3 Rest of Middle-East and Africa

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Argentina

- 5.2.5.3 Rest of South America

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Medtronic plc.

- 6.1.2 Koninklijke Philips N.V.

- 6.1.3 Bayer HealthCare LLC

- 6.1.4 General Electric Company

- 6.1.5 F. Hoffmann-La Roche AG

- 6.1.6 Johnson & Johnson

- 6.1.7 ResMed, Inc.

- 6.1.8 Omron Healthcare, Inc.

- 6.1.9 OraSure Technologies, Inc.

- 6.1.10 Abbott Inc.

- 6.1.11 B. Braun Melsungen