|

|

市場調査レポート

商品コード

1437961

データ損失防止:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年)Global Data Loss Prevention - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| データ損失防止:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

世界のデータ損失防止市場規模は、2024年に27億9,000万米ドルと推定され、2029年までに76億1,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に22.29%のCAGRで成長します。

世界中の企業は、デジタル変革プロセスの一環として、より優れたセキュリティソリューションを採用することが増えており、それによって市場の成長が促進されています。

主なハイライト

- データ侵害の事例が急速に増加していることや、サービスとしてのDLP、クラウドに拡張されたDLP機能、高度な脅威保護などのその他の要因により、世界中でデータ損失保護ソリューションへの注目が大幅に高まっています。デジタル資産の需要が高まるにつれて、構造化データと非構造化データの量が大幅に増加し、データ中心の組織に戦略的に焦点を当てたデータ保護サービスの必要性が高まっています。 Fortune Global 500リストに名を連ねる複数の大企業が、10年以上にわたりDLP市場に投資してきました。現在、この市場は中堅企業にとって重要なセキュリティ戦略として浮上しつつあります。

- データ保護戦略にはデータ損失防止(DLP)ツールが必要です。 DLPソリューションはさまざまなニーズに合わせて調整でき、GDPRやカリフォルニア州消費者プライバシー法(CCPA)などの新しいデータ保護規制へのコンプライアンスへの取り組みをサポートします。これらは、組織が企業のネットワークに出入りする機密データを検索、監視、制御するのに役立ちます。

- BYODへの需要の高まりにより、主要企業の間でデータセキュリティに関する懸念が高まっています。 ForcepointのBYODセキュリティレポート 2021によると、全企業の82%が従業員に自分のデバイスを職場に持ち込むことを積極的に奨励しています。 BYODは、管理対象外のデバイスを職場に持ち込む従業員(70%)に最も関連していますが、請負業者(26%)、パートナー(21%)、顧客(18%)、サプライヤー(14%)などの他のグループにも当てはまります。ただし、情報セキュリティの問題(30%)、従業員のプライバシーの問題(15%)、サポート費用の懸念(9%)が、BYOD導入の最大の障害となっています。データの漏洩または損失は、セキュリティ上の懸念事項のリストのトップ(62%)です。同じレポートによると、ユーザーによる危険なアプリやコンテンツのインストール(54%)、デバイスの紛失または盗難(53%)、企業データやシステムへの違法アクセス(51%)はすべて重大な懸念事項です。

- アクセス権限が機密データに制限されている場合でも、印刷可能な形式でデータを閲覧できます。これらのチャネルは閉じることができず、データ交換という点ではビジネスの基盤であるため、「転送中の」データに関連するファイル共有やオンラインサービスなどのチャネルは主な課題の1つです。これらのチャネルで最適なセキュリティを保証するには、トラフィックを厳しくフィルタリングする必要があります。実装されるDLPシステムは、これらのチャネルのセキュリティと相互接続性のバランスを保つために常に機能する必要があります。

- 新型コロナウイルス感染症(COVID-19)のパンデミックの出現により、世界中で生成されるデータの総量がより急速に増加しているため、市場はさらに成長すると予想されています。COVID-19症によるロックダウンと在宅勤務の動向の結果、前例のない数の人々が主要な通信デバイスとしてモバイルデバイスを利用するようになり、それによって組織が増大するサイバー脅威から守るためのエンドポイントがさらに増えています。

データ損失防止(DLP)市場動向

市場を牽引する世界中のデータ侵害とサイバー攻撃の増加

- 複数の業界でデータ侵害の事例が増加しているため、数百万件の消費者データ記録がハッカーに漏洩し、多くの企業が数百万米ドルの損失を被っているため、新興国全体でセキュリティソリューションへの注目が高まっています。

- 世界中のビジネスが成長するにつれて、ゼロデイマルウェア、トロイの木馬、高度な持続的脅威などの新たな脅威により、重要なデータがリスクにさらされています。この傾向により、組織はDLPソリューションを導入してエンドポイントやネットワーク内のデータを潜在的な攻撃から保護することが奨励されています。

- 組織内でのBYOD動向の採用の増加により、さまざまなラップトップ、デスクトップ、スマートフォンの流入が増加し、その結果、他のエンドポイントが攻撃に対して脆弱になっています。セキュリティ対策だけでは、これらの脅威を阻止するのに十分ではありません。世界中でモバイルデバイスの導入が大幅に増加しているため、予測期間中に大きな機会が生まれると予想されます。シスコの年次インターネットレポートによると、2023年までにネットワークに接続されたデバイスは約293億台になる可能性があります。スマート製造とスマート産業は、5Gの採用増加により市場を拡大すると予想されています。

- ランサムウェアの脅威アクターは世界中のソフトウェアサプライチェーンビジネスを標的にし、クライアントを侵害したり恐喝したりします。ソフトウェアサプライチェーンに焦点を当てることで、ランサムウェアの攻撃者は1回の最初の侵入で複数の被害者にアクセスし、攻撃範囲を拡大できます。近年、技術の進歩により通信業界におけるサイバー攻撃が増加しています。したがって、通信会社にとって、ネットワーク上のすべてのオペレーティングシステムの安全性を確保するためにデータセキュリティサービスを選択することがますます重要になっています。

- エンドポイントの数は2桁の成長を遂げています。これは主に、インダストリー4.0、マシンツーマシン通信、スマートシティの出現による自動化の導入の急速な増加によるものです。データとデバイスの脆弱性を保護し、攻撃を認識して被害を最小限に抑えるためのツールを導入する必要性は非常に重要です。したがって、自動化技術の採用の増加が、予測期間中の市場の成長を促進すると予想されます。

北米が最大の市場シェアを占めると予想される

- 米国ではデータ損失の件数が増加しています。個人情報盗難リソースセンター(ITRC)によると、米国における違反の平均件数はここ数年でわずかに増加しており、2017年の1,506件の違反から2021年の1,826件の違反に増加しています。

- 2021年、国内のデータ侵害件数は増加し、約2億9,393万人に影響を及ぼしました。さまざまな業界で増加するこれらのデータ侵害は、予測期間中にデータ損失防止ソリューションの需要を促進する主な要因になると予想されます。

- 米国のヘルスケア業界でも電子記録ベースへの移行が進む中、多くのデータ侵害が発生しており、データ損失防止ソリューションが必要となっています。

- 成長戦略として、企業は市場シェアを最大化するための有利な方法として製品の発売に多大な労力を費やしています。たとえば、2022年 10月、米国に本拠を置くサイバーセキュリティおよびコンプライアンス企業であるProofpoint Inc.は、2022 Microsoft Ignite Conferenceで、脅威保護プラットフォーム全体にわたる一連のイノベーションを宣言しました。これにより、組織は次のような今日の最も高度で蔓延する脅威から防御できるようになります。サプライチェーン攻撃とビジネス電子メール侵害(BEC)。この機能強化により、電子メール詐欺の検出、サードパーティやサプライヤーの侵害に対する防御、機械学習(ML)、および行動分析に関する優れた洞察が企業に提供されます。これらはすべて、新しい導入が簡単なインラインAPIモデルを通じて利用可能になります。

- 2022年 3月、ケベック州首相兼保健大臣は、医療および社会サービス情報の管理を含むケベック州の医療システムの改革を発表しました。政府は法案19を導入しました。これは、医療ネットワークを近代化および分散化し、医療および社会サービス情報のより安全でシームレスな流れを可能にする新しい管理システムを確立することを目的としています。

データ損失防止(DLP)業界の概要

データ損失防止市場における競争企業間の敵対関係の激しさは高く、予測期間中にさらに激化すると予想されます。大手企業は研究開発や統合活動の面で市場に強い影響力を持っています。逆に、この市場は、市場への浸透度が高く、断片化レベルが増加していることを特徴としている可能性があります。

- 2022年 4月-McAfee Corp.は、主力製品であるMcAfee Total Protectionに追加される同社の最新のプライバシー機能であるPersonal Data Cleanupを米国で開始しました。 Personal Data Cleanupは、消費者に可視性、ガイダンス、継続的な監視を提供し、Webで最も危険なデータブローカーサイトからデータを削除することで、個人情報窃盗、ハッカー、スパマーから身を守ることができます。

- 2022年 4月-Broadcom Inc.は、IBMの新しいz16の「Day One」サポートを発表し、組織が同社の高度なAI、セキュリティ、ハイブリッドクラウドソリューションからより多くの価値を得る機会を拡大しました。 Broadcomの最先端のテクノロジーソリューション、サービス、革新的な「コードを超えた」ソフトウェアは、ますます困難になるビジネス環境で成功するために必要な競争上の優位性をクライアントに提供します。

- 2021年 3月-Proofpointは、データ損失保護マネージドサービスの革新者であるInteliSecure Inc.の買収を完了しました。この買収により、プルーフポイントは、多様な環境で重要なデータを保護する顧客の能力を強化することにより、クラウドベースの人間中心のセキュリティプラットフォームを強化しました。 ProofpointはInteliSecureを現金6,250万米ドルで買収しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

- COVID-19による業界への影響の評価

第5章 市場力学

- 市場促進要因

- 市場を牽引する世界中のデータ侵害とサイバー攻撃の増加

- 規制とコンプライアンス(GDPR、CCPA、PCI DSSなど)

- データの重要性と脆弱性の増大

- 市場抑制要因

- 完全なソリューションの導入に関する認識の欠如

- アクセス権、暗号化、スケーラビリティ、統合に関連する導入の課題

第6章 市場セグメンテーション

- デプロイメント別

- オンプレミス

- クラウドベース

- ソリューション別

- ネットワークDLP

- エンドポイントDLP

- データセンター/ストレージベースDLP

- エンドユーザー産業別

- IT・通信

- BFSI

- 政府

- ヘルスケア

- 製造業

- 小売および物流

- その他のエンドユーザー産業

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- その他アジア太平洋地域

- ラテンアメリカ

- 中東とアフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Broadcom Inc.(Symantec)

- Mcafee LLC

- GTB Technologies Inc.

- Cososys

- Digital Guardian Inc.

- Forcepoint LLC

- Securetrust(Vikingcloud)

- Trend Micro

- Check Point Software Technologies Ltd

- Proofpoint Inc.

- Spirion LLC

第8章 投資分析

第9章 市場の将来

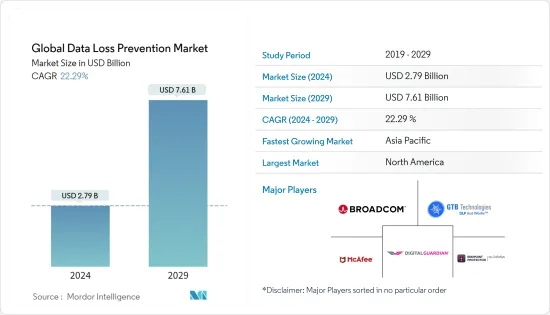

The Global Data Loss Prevention Market size is estimated at USD 2.79 billion in 2024, and is expected to reach USD 7.61 billion by 2029, growing at a CAGR of 22.29% during the forecast period (2024-2029).

Enterprises worldwide are increasingly adopting better security solutions as part of their digital transformation process, thereby augmenting the market's growth.

Key Highlights

- The rapidly increasing instances of data breaches and other factors, such as DLP-as-a-service, DLP functionalities extending into the cloud, and advanced threat protection, have significantly increased the focus on data loss protection solutions worldwide. As the demand for digital assets increased, there was a massive growth in the amount of structured and unstructured data, driving the need for data protection services with a strategic focus on data-centric organizations. Multiple large enterprises in the Fortune Global 500 list have invested in the DLP market for over a decade. Currently, the market is emerging as a critical security strategy within reach of mid-sized enterprises.

- Data loss prevention (DLP) tools are necessary for data protection strategies. DLP solutions can be tailored to various needs and support compliance efforts with the new data protection regulations, such as GDPR or the California Consumer Privacy Act (CCPA). They are helping organizations find, monitor, and control sensitive data travelling in and out of the company's network.

- The increasing demand for BYOD is raising the concern among key enterprises regarding data security. According to the BYOD Security Report 2021 by Forcepoint, 82% of all businesses actively encourage employees to bring their own devices to work. BYOD is most associated with employees bringing unmanaged devices to work (70%), but it also applies to other groups such as contractors (26%), partners (21%), customers (18%), and suppliers (14%). However, information security issues (30%), employee privacy concerns (15%), and support cost concerns (9%) are the biggest impediments to BYOD adoption. Data leakage or loss is at the top of the list of security concerns (62%). Users installing hazardous apps or content (54%), lost or stolen devices (53%), and illegal access to the company data and systems are all significant worries (51%), according to the same report.

- Data can still be viewed in a printable format even when access permission is restricted to confidential data. As these channels cannot be closed and are the foundation of business in terms of data interchange, channels like file sharing and online services related to data "in transit" have been one of the main challenges. Traffic must be heavily filtered to guarantee optimal security in these channels. The DLP system that would be implemented should constantly work to balance security and interconnectivity in these channels.

- With the emergence of the COVID-19 pandemic, the market is anticipated to grow further as the total volume of data being generated worldwide is rising much faster. As a result of the COVID-19 lockdowns and work-from-home trends, an unprecedented number of people are now making use of mobile devices as their primary communication devices, thereby creating more endpoints for the organization to secure from the rising cyber threats.

Data Loss Prevention (DLP) Market Trends

Rising Data Breaches and Cyber Attacks Worldwide to Drive the Market

- The increasing instances of data breaches across multiple industries have leaked millions of consumer data records to hackers and led to the loss of millions of dollars for numerous companies, thus increasing the focus on security solutions across emerging economies.

- As businesses worldwide grow, new threats such as zero-day malware, trojans, and advanced persistent threats have exposed critical data to risk. This trend has encouraged organizations to deploy DLP solutions to safeguard their data within endpoints and networks against potential attacks.

- The increasing adoption of BYOD trends in organizations has increased the influx of different laptops, desktops, and smartphones, thus creating other endpoints vulnerable to attacks. Security measures on their own are not enough to stop these threats. The massive growth in the adoption of mobile devices across the world is expected to create significant opportunities during the forecast period. According to the Cisco Annual Internet Report, there may be approximately 29.3 billion networked devices by 2023. Smart manufacturing and the smart industry are expected to augment the market with the increased adoption of 5G.

- Ransomware threat actors target software supply chain businesses worldwide, compromising and extorting their clients. By focusing on software supply chains, ransomware threat actors can expand the scope of their assaults by gaining access to several victims through a single initial penetration. In recent years, technological advancements have increased cyberattacks in the telecom industry. Hence, it is becoming increasingly crucial for telecom companies to choose data security services to ensure that all operating systems on their network are secure.

- There has been double-digit growth in the number of endpoints, primarily due to the rapidly increasing adoption of automation due to Industry 4.0, machine-to-machine communication, and the emergence of smart cities. The need to protect the vulnerability of data and devices and deploy tools to recognize attacks and minimize the damage is critically important. Therefore, the increasing adoption of automation technology is expected to drive the market's growth during the forecast period.

North America is Expected to Account for the Largest Market Share

- The United States is witnessing an increased number of data breaches. According to the Identity Theft Resource Center (ITRC), the average number of violations in the United States has increased marginally over the past few years, from 1,506 breaches in 2017 to 1,826 violations in 2021.

- In 2021, the country's increasing number of data breaches impacted around 293.93 million individuals. These increasing data breaches in various industries are expected to be the primary factor driving the demand for data loss prevention solutions during the forecast period.

- The US healthcare industry also witnesses many data breaches as the industry is moving to an electronic record base, thus requiring data loss prevention solutions.

- As a growth strategy, companies heavily indulge in product launches as lucrative ways to maximize their market shares. For instance, in October 2022, Proofpoint Inc., a US-based cybersecurity and compliance company, declared an array of innovations across its Threat Protection Platform at the 2022 Microsoft Ignite Conference, allowing organizations to defend against today's most advanced and pervasive threats, including supply chain assaults and business email compromise (BEC). The enhancements provide companies with outstanding insight into email fraud detection, defense against third-party and supplier compromise, machine learning (ML), and behavioral analytics, all made available through a new, easy-to-deploy inline API model.

- In March 2022, Quebec's Premier and Health Minister announced the reformation of Quebec's health system, including the management of health and social services information. The government introduced Bill 19, which aims to set up a new management system that modernizes and decentralizes the health network to enable a safer and more seamless flow of health and social services information.

Data Loss Prevention (DLP) Industry Overview

The intensity of competitive rivalry in the data loss prevention market is high and is expected to increase during the forecast period. Major companies strongly influence the market in terms of R&D and consolidation activities. Conversely, the market can be characterized by high market penetration and increasing fragmentation levels.

- April 2022 - McAfee Corp. launched Personal Data Cleanup in the United States, the company's newest privacy feature addition to its flagship product, McAfee Total Protection. Personal Data Cleanup provides consumers with visibility, guidance, and continuous monitoring to protect themselves from identity thieves, hackers, and spammers by removing their data from some of the web's riskiest data broker sites.

- April 2022 - Broadcom Inc. announced "Day One" support for IBM's new z16, expanding opportunities for organizations to gain more value from the company's advanced AI, security, and hybrid cloud solutions. Broadcom's leading technology solutions, services, and innovative "beyond code" software give clients the competitive advantage required to succeed in an increasingly challenging business environment.

- March 2021 - Proofpoint completed its acquisition of InteliSecure Inc., an innovator in data loss protection managed services. With this acquisition, Proofpoint strengthened its cloud-based people-centric security platform by enhancing customers' ability to protect critical data in diverse environments. Proofpoint acquired InteliSecure for USD 62.5 million in cash.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment Of Covid-19 Impact On The Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Data Breaches and Cyber Attacks Worldwide to Drive the Market

- 5.1.2 Regulations and Compliances (GDPR, CCPA, PCI DSS, Etc.)

- 5.1.3 Increasing Data Criticality and Vulnerability

- 5.2 Market Restraints

- 5.2.1 Lack of Awareness About Complete Solution Adoption

- 5.2.2 Deployment Challenges Related to Access Rights, Encryption, Scalability, and Integration

6 MARKET SEGMENTATION

- 6.1 By Deployment

- 6.1.1 On-premise

- 6.1.2 Cloud-based

- 6.2 By Solution

- 6.2.1 Network DLP

- 6.2.2 Endpoint DLP

- 6.2.3 Datacenter/Storage-based DLP

- 6.3 By End-user Industry

- 6.3.1 IT and Telecommunication

- 6.3.2 BFSI

- 6.3.3 Government

- 6.3.4 Healthcare

- 6.3.5 Manufacturing

- 6.3.6 Retail and Logistics

- 6.3.7 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 United Kingdom

- 6.4.2.3 France

- 6.4.2.4 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.5 Middle-East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Broadcom Inc. (Symantec)

- 7.1.2 Mcafee LLC

- 7.1.3 GTB Technologies Inc.

- 7.1.4 Cososys

- 7.1.5 Digital Guardian Inc.

- 7.1.6 Forcepoint LLC

- 7.1.7 Securetrust (Vikingcloud)

- 7.1.8 Trend Micro

- 7.1.9 Check Point Software Technologies Ltd

- 7.1.10 Proofpoint Inc.

- 7.1.11 Spirion LLC