|

市場調査レポート

商品コード

1405723

静脈(IV)注射器:市場シェア分析、産業動向と統計、2024年~2029年の成長予測Intravenous (IV) Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 静脈(IV)注射器:市場シェア分析、産業動向と統計、2024年~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 114 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

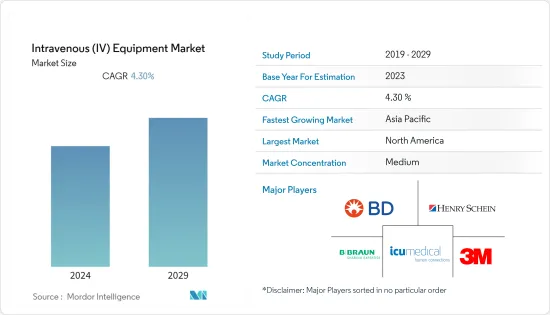

静脈(IV)注射器市場は予測期間中にCAGR 4.3%を記録する見込み

主なハイライト

- COVID-19の突然の発生は、医療インフラへの負担を減らすために延期されていた即時性のない外科手術の突然の停止により、静脈(IV)注射器産業に深刻な影響を与えました。感染の可能性を減らすため、COVID-19の治療には静脈内治療の使用が制限されました。例えば、国立衛生研究所が2023年7月に発表したガイドラインによると、COVID-19治療ガイドライン・パネルは急性COVID-19感染症の治療に免疫グロブリン静注療法の利用を推奨していることがわかった。そのため、COVID-19治療における点滴静注の使用が制限され、調査した市場にはかなりの影響があった。しかし、現在、点滴機器の需要という点では、市場はパンデミック以前の状態に達しており、今後数年間は力強い成長が期待されます。

- 主な慢性疾患には、がん、腎不全、心臓病などがあり、高血圧、糖尿病、肥満、うつ病などの生活習慣病もあります。

- このような慢性疾患の増加は、調査対象市場の成長を増大させています。例えば、2021年4月に発表された世界保健機関(WHO)のデータによると、慢性疾患により毎年4,100万人が死亡すると予想されており、これは世界全体の死亡者数の71%に相当します。また、低・中所得国の死亡率の77%は慢性疾患に起因しています。がん患者やその他の慢性疾患の増加に伴い、さまざまな外科手術の需要が高まり、これが市場の成長を促進すると考えられています。

- さらに、カナダ・アルツハイマー協会によると、2021年1月には、50万人以上のカナダ人が認知症を患っていました。2030年には、この数は912,000人に増加すると予想されています。同様に、2021年のフランス財団によると、パーキンソン病は2021年時点でフランス国内で約15万人が罹患しています。同財団はまた、この病気は老年人口により多く影響すると述べています。したがって、慢性疾患を抱える人々の数が多いことが、今後数年間の市場成長を促進すると予想されます。

- しかし、厳しい規制や製品回収につながる輸液ポンプに関連した投薬ミスが、予測期間中の市場成長を抑制すると見られています。

静脈(IV)注射器市場の動向

静脈内カテーテルが静脈(IV)注射器市場で大きなシェアを占める

- 点滴カテーテルは、患者に点滴薬、血液製剤、栄養輸液を投与するために不可欠なツールです。IVカテーテルには、末梢IVカテーテル、中心静脈カテーテル、正中線カテーテルなどの種類があります。ヘルスケアプロバイダーは、それぞれのタイプの静脈カテーテルを特定の治療目的で管理・使用します。

- 短鎖型末梢静脈カテーテルは静脈内処置時の合併症を軽減できることから需要が増加しており、静脈カテーテル・セグメントの成長を促進する可能性が高いです。さらに、閉鎖型IVカテーテルシステムは、針刺し損傷に関連するリスクから保護することができます。

- 針刺し傷害の発生率が高いことから、そのようなリスクを低減し、患者の快適性を高めるドラッグデリバリー機器を使用するようヘルスケア専門家を説得しています。米国国立衛生研究所が2022年7月に発表した研究によると、米国では毎年約38万5,000件の針刺し損傷が発生しています。このように、針刺し傷害の多さは、より安全なデバイスの使用を促進し、それによって静脈内カテーテルセグメントの成長を急増させています。さらに、2022年7月、B. Braun Medical Inc.は、1回で血液をコントロールできる新しいIntrocan Safety 2 IV Catheterを発売しました。このデバイスは自動的に制御されるため、手動のカテーテルよりも大幅に安全であると考えられています。同様に、2022年8月、日本の実用新案がセーフブレイク血管に付与されました。この装置は主に末梢静脈ラインを保護するために使用されます。この特許により、SafeBreak Vascularのメーカーであるリネウス・メディカルが日本市場に参入しました。

- このように、針刺し傷害の発生率の上昇や製品発売の増加など、前述の要因はすべて、予測期間中にセグメントを押し上げると予想されます。

北米が世界の静脈注射器市場を独占する見込み

- 慢性疾患の有病率の増加、同地域における外科手術の増加、主要市場参入企業による製品発売が、北米地域の市場成長を牽引しています。

- 2021年に発表された全米生物工学情報センターの調査によると、米国では約5,000万件の手術が行われています。心血管障害と肥満の有病率が上昇していることが、この地域の市場成長の要因となっています。アラバマ大学が2021年11月に発表した「心臓バイパス手術」の論文によると、米国では毎年35万件近くの冠動脈バイパス移植(CABG)手術が行われています。このような手術件数の多さが、同国における静脈内機器の需要を増大させ、市場成長に寄与しています。

- さらに、米国食品医薬品局からの承認や主要企業による製品発売が市場を押し上げると期待されています。例えば、2022年8月、バクスターは用量IQ安全ソフトウェアを搭載したNovum IQシリンジ輸液ポンプの米国食品医薬品局(USFDA)認可を発表しました。Novum IQ SYRは、安全機能、より優れた接続性、精度を強化して設計されています。このソフトウェアは、新生児を含む患者に個別化された治療を提供するのに役立ちます。同様に、2021年2月、United Therapeutics Corporationは米国でRemunity Pump for Remodulinを発売しました。この発売は、主に肺動脈性肺高血圧症(PAH)を患う患者に焦点を当てたものでした。したがって、このような新しい発売と国全体での承認は、市場の成長を推進しています。

静脈(IV)注射器産業の概要

静脈(IV)注射器市場は、国内企業だけでなく国際企業も存在し、競争は中程度です。強力な競合と急速な技術進歩が市場成長の主な要因です。Becton, Dickinson and Company、B. Braun, Melsungen AG、3M、Henry Schein, Inc.、ICU Medical, Inc.などの企業がこの業界で大きなシェアを占めています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 高齢者人口の増加に伴う慢性疾患の有病率の増加

- 世界の手術件数の増加

- 市場抑制要因

- 製品回収につながる輸液ポンプに関連した投薬ミス

- 厳しい規制シナリオ

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模)

- タイプ別

- 輸液カテーテル

- 輸液ポンプ

- 固定装置

- 投与セット

- 点滴室

- その他

- エンドユーザー別

- 病院

- 外来手術センター

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- 3M

- Baxter

- Becton, Dickinson and Company

- B. Braun Melsungen AG

- EuroLife Healthcare Pvt. Ltd

- Henry Schein, Inc

- ICU Medical, Inc

- Polymedicure

- Terumo Corporation

- Teleflex Incorporated

- Ascor S.A.

第7章 市場機会と今後の動向

The intravenous (IV) equipment market is expected to register a CAGR of 4.3% during the forecast period.

Key Highlights

- The sudden outbreak of COVID-19 had a severe impact on the intravenous (IV) equipment industry due to a sudden halt in surgical procedures that were non-immediate and were being postponed to decrease the burden on healthcare infrastructure. The use of intravenous therapies was restricted for the treatment of COVID-19 to reduce the chances of infection. For instance, as per the guidelines published by the National Institute of Health in July 2023, it was found that the COVID-19 Treatment Guidelines Panel recommended the utilization of IV Immunoglobulin for treating acute COVID-19 infection. Therefore, with the restricted use of IV for COVID-19 treatment, there was a considerable impact on the market studied. However, currently, the market has reached its pre-pandemic nature in terms of demand for IV equipment and is expected to witness strong growth in the coming years.

- Some of the major chronic diseases include cancer, kidney failure, and heart disease, among others, and several lifestyle disorders such as hypertension, diabetes, obesity, and depression, among others, which need critical care during their hospitalization.

- The rise in such chronic diseases is augmenting the growth of the market studied. For instance, according to the World Health Organization data published in April 2021, chronic diseases are expected to kill 41 million people each year, equivalent to 71% of all deaths globally. Also, 77% of mortality in low- and middle-income nations is attributable to chronic diseases. With the increase in the number of cancer cases and other chronic conditions, there will be a growing demand for various surgical procedures, which is believed to propel the market growth.

- Moreover, according to the Alzheimer Society of Canada, in January 2021, over 500,000 Canadians were living with dementia. By 2030, this number is expected to rise to 912,000. Similarly, according to the Fondation de France in 2021, Parkinson's disease affected around 150,000 people in France as of 2021. It also stated that the disease affects the geriatric population more. Hence, the high number of people living with chronic diseases is expected to propel the market growth in the coming years.

- However, stringent regulation and medication errors associated with infusion pumps leading to a product recall are expected to restrain the market growth over the forecast period.

Intravenous (IV) Equipment Market Trends

IV Catheters Segment Holds Significant Share in Intravenous (IV) Equipment Market

- IV catheters are the essential tools to deliver IV medications, blood products, and nutritional fluids to patients. There are different types of IV catheters, namely peripheral IV catheters, central venous catheters, and midline catheters. Healthcare providers administer and use each type of IV catheter for specific treatment purposes.

- Increasing demand for short-closed peripheral IV catheters as they are capable of reducing complications during intravenous procedures is likely to propel the IV catheter segment growth. Additionally, a closed IV catheter system offers protection against the risks associated with needle-stick injury.

- The high incidence of needle-stick injuries is persuading healthcare professionals to use drug delivery devices that reduce such a risk and increase patient comfort. As per the study published by the National Institute of Health in July 2022, approximately 385,000 needle-stick injuries occur in the United States each year. Thus, the high number of needle-stick injuries is promoting the use of safer devices, thereby surging the growth of the IV catheter segment. Moreover, in July 2022, B. Braun Medical Inc. launched its new Introcan Safety 2 IV Catheter with one-time blood control. As the device is automatically controlled, it is considered to be significantly safer than manual catheters. Similarly, in August 2022, a Japanese utility patent was granted to SafeBreak Vascular. The device is mainly used to protect the peripheral IV lines. With this patent, Lineus Medical, a manufacturer of SafeBreak Vascular, entered the Japanese market.

- Thus, all aforementioned factors, such as the rising incidence of needle-stick injuries and increasing product launches, are expected to boost the segment over the forecast period.

North America is Expected to Dominate the Global Intravenous (IV) Equipment Market

- The growing prevalence of chronic diseases, increasing surgical procedures in the region, and product launches by the major market players are driving the market growth of the North American region.

- According to a study by the National Center for Biotechnology Information published in 2021, about 50 million surgeries are performed in the United States. The rising prevalence of cardiovascular disorders and obesity rates is attributed to the market growth in this region. As per the 'Cardiac Bypass Surgeries' Article published by the University of Alabama in November 2021, nearly 350,000 Coronary Artery Bypass Graft (CABG) Surgeries are done each year in the United States. Such a high number of surgeries is augmenting the demand for intravenous equipment in the country and contributing to market growth.

- Furthermore, approvals from the United States Food and Drug Administration and product launches by key players are expected to boost the market. For instance, in August 2022, Baxter announced the United States Food and Drug Administration (USFDA) clearance of the Novum IQ Syringe infusion pump with dose IQ safety software. The Novum IQ SYR has been designed with enhanced safety features, better connectivity, and accuracy. This software is helpful in providing personalized therapy for patients, including neonates. Similarly, in February 2021, United Therapeutics Corporation launched the Remunity Pump for Remodulin in the United States. The launch was majorly focused on patients suffering from pulmonary atrial hypertension (PAH). Hence, such new launches and approvals across the country are propelling the market growth.

Intravenous (IV) Equipment Industry Overview

The intravenous (IV) equipment market is moderately competitive with the presence of local as well as international companies. Strong competition and rapid technological advancements are key factors fueling the market growth. Companies like Becton, Dickinson and Company, B. Braun, Melsungen AG, 3M, Henry Schein, Inc., and ICU Medical, Inc., among others, hold a substantial market share in the industry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Chronic Diseases Coupled with Rising Geriatric Population

- 4.2.2 Increasing Number of Surgeries Globally

- 4.3 Market Restraints

- 4.3.1 Medication Errors Associated with Infusion Pumps Leading to Product Recalls

- 4.3.2 Stringent Regulatory Scenario

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Type

- 5.1.1 IV Catheters

- 5.1.2 Infusion Pumps

- 5.1.3 Securement Devices

- 5.1.4 Administration Sets

- 5.1.5 Drip Chambers

- 5.1.6 Other Tyoes

- 5.2 By End-User

- 5.2.1 Hospitals

- 5.2.2 Ambulatory Surgical Centers

- 5.2.3 Other End-Users

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle-East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle-East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 3M

- 6.1.2 Baxter

- 6.1.3 Becton, Dickinson and Company

- 6.1.4 B. Braun Melsungen AG

- 6.1.5 EuroLife Healthcare Pvt. Ltd

- 6.1.6 Henry Schein, Inc

- 6.1.7 ICU Medical, Inc

- 6.1.8 Polymedicure

- 6.1.9 Terumo Corporation

- 6.1.10 Teleflex Incorporated

- 6.1.11 Ascor S.A.