|

市場調査レポート

商品コード

1851522

組織診断薬:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Tissue Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 組織診断薬:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

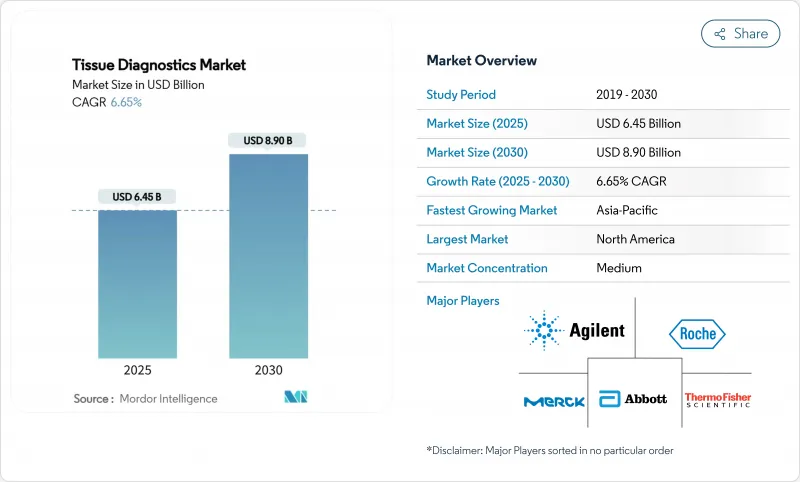

組織診断薬の市場規模は2025年に64億5,000万米ドルで、CAGR 6.65%を反映して2030年には89億米ドルに達すると予測されています。

この拡大は、世界的ながん罹患率の上昇と、検査室の急速な自動化、特に読影時間を短縮し結果を標準化するAI対応ホールスライドイメージングという2つの勢いに支えられています。試薬と消耗品は、すべての病理組織検査がシングルユースの抗体を消費するため、予測可能な需要を維持する一方、検査室がスライドの取り扱いをデジタル化し、エラーのないスループットのためにロボット工学を統合するにつれて、機器が台頭しています。米国と欧州では、デジタル診療報酬が明確化され、経済的障壁が低くなったため、小規模病院とリファレンスラボは、病理医不足を緩和する遠隔診察ワークフローを採用するようになりました。アジア太平洋地域では、各国政府が早期発見の目標を国の医療予算に組み込んでいるため、記録的な資本が集まり、グローバル・ベンダーもローカル・ベンダーも同様に新たな取引量を獲得しています。同時に、AIネイティブの新興企業は、ソフトウェア、ハードウェア、試薬をシームレスなプラットフォームにバンドルするよう既存企業に圧力をかけ、10年を通じて活発な合併やパートナーシップの舞台を整えます。

世界の組織診断薬市場の動向と洞察

がん罹患率の上昇

世界のがん罹患数は毎年2.1%ずつ増加し、2050年には3,500万人に達すると予測されているため、確定組織分析は引き続き不可欠です。乳がんは引き続き診断件数の大半を占めていますが、非小細胞肺がんは、国のスクリーニングプログラムが詳細な腫瘍プロファイリングを要求しているため、使用事例が最も急速に拡大しています。リスクは65歳を超えると急増し、すでに手狭になっている病理検査室の処理能力へのプレッシャーが強まっています。継続的な検体流入により、ベンダーは安定した収益を確保し、自動化、多重免疫組織化学、精度を維持しながら所要時間を短縮するAIアルゴリズムなど、現在進行中の研究開発を検証することができます。

病理組織検査室における自動化とAIの加速

AIを搭載したホールスライドスキャナーにより、スライドレビュー時間を40%短縮し、検査室間のコンコーダンスが向上するため、不足している病理医が複雑な症例に集中できるようになります。2024年にロシュの計算コンパニオン診断薬がFDAから画期的な指定を受けたことは、アルゴリズム支援による読影が規制当局に受け入れられ、顧客層が拡大したことを示すものです。米国では現在、退職率が後任者を2対1で上回っており、自動化がサービス継続の中心となっています。AIを導入した検査施設は、より迅速な報告、より厳格な品質指標、より高い拡張性を実現し、組織診断薬市場をソフトウェアによる標準治療へと押し上げています。

資本コストと消耗品コストが高く、償還はまちまち

ホールスライドスキャナーの価格は20万米ドルから50万米ドルであり、消耗品は検査室の運営予算の約65%を占めています。小規模病院は、民間支払機関によって払い戻しにばらつきがあるため、このような出費を回収するのに苦労しており、キャッシュリッチなプロバイダーが能力格差を広げる2層のエコシステムを作り出しています。COVID-19は、支出を急性期医療に振り向け、ハードウェアの更新サイクルを遅らせ、買い替えのバックログを拡大しています。リース・モデルや地域共有サービス・ハブは、新たな歯止めにはなっているが、手頃な価格の完全な解決にはなっていないです。

セグメント分析

機器部門は2030年までCAGR 7.23%を記録すると予測され、ラボが手作業のワークフローを見直すにつれて市場全体の成長を上回る。ホールスライドスキャナーは、米国とEUにおける償還の確実性に後押しされ、最も急成長を遂げます。ロボット化された組織プロセッサーはハンドリングエラーを減らし、AI化された染色システムは試薬の使用を節約します。バーコードによるサンプル追跡やクラウドネイティブのダッシュボードなどの進歩は、検査室の効率をさらに向上させる。逆に、試薬と消耗品からの経常収益がベンダーのマージンを支えています。このカテゴリーは2024年に68.23%のシェアを維持します。マルチプレックスアッセイキットは、複数のバイオマーカーを1回の測定に凝縮するため、1回当たりの測定コストを下げ、組織を保存できます。ルーチン試薬の安定した需要は、ベンダーに予測可能なキャッシュフローをもたらし、利益率の高い装置の研究開発の資金源となります。

第二世代のミクロトームとクライオスタットは、デジタル温度制御とブレード角度制御を組み込んでおり、切片の厚さのばらつきを最小限に抑えています。これらの機器は成熟しているが、摩耗やCAP認定要件の順守により、交換サイクルは安定しています。使い捨てのプラスチックカセット、スライドガラス、カバースリップが消耗品として使用され、小規模な地域の病理検査室でも安定した収入源となっています。機器と消耗品の共生関係は、スループットへの期待の高まりと相まって、組織診断薬市場の長期的な拡大を支えています。

デジタルパソロジーのCAGRは7.31%で、すべてのモダリティの中で最も高いです。アルゴリズムに基づくパターン認識によってピクセルデータが定量的な指標に変換され、腫瘍浸潤リンパ球や有糸分裂像の客観的な等級付けが可能になります。地方の施設では、クラウド接続を利用して都市部のサブスペシャリストを活用し、患者の移動時間と待ち時間を短縮しています。FDAが2025年にAI対応の乳がん転移検出器を認可するなどの規制上のマイルストーンは、病院の調達委員会を活気づける。一方、免疫組織化学は、その臨床的な親しみやすさと、標的治療の指針となるバイオマーカーカタログの拡大により、43.44%の市場シェアを維持しています。自動化により、染色サイクルタイムは60分未満に短縮され、人員を増やすことなく日々のスライド処理能力を高めています。

In-situ hybridizationは、特に血液悪性腫瘍において、遺伝子再配列やウイルスゲノムを検出するための関連性を維持しています。一部の検査室ではISHとmultiplex IHCを組み合わせてRNAとタンパク質の共発現を三角測量し、乏しい組織からの診断収量を高めています。新しい質量分析イメージングとラマンベースの方法は、まだニッチであるが、薬剤分布研究とリピドミクスに有望です。これらの技術アークを総合すると、組織診断薬市場の継続的な多様化が確実となります。

地域分析

北米は2024年の世界売上高の41.34%を占め、CLIA認定ラボの豊富な設置ベース、幅広い支払者カバレッジ、多くの機器・試薬本社への近接性などに支えられています。FDAの継続的な監視が世界的なベストプラクティス基準を形成し、ベンチャーキャピタルの流れがAI新興企業の形成を支えています。カナダでは、人口の少ない地域と都市部のがんセンターを結ぶ全国的な遠隔病理学ネットワークが進展し、市場範囲が広がっています。

欧州は、国境を越えたデータ交換と調達を合理化するEUデジタル単一市場戦略の恩恵を受ける。ドイツと英国はAIの検証研究を率先し、北欧諸国はアルゴリズムのトレーニングに中央病理学登録を活用しています。一部の南部および東部の加盟国では緊縮財政が成長を抑制しているもの、結束力のある規制の枠組みと安定した償還により、欧州は第2世代デジタルシステムの確実な導入国となっています。

アジア太平洋地域は最も急成長している地域であり、中国とインドが合計2,000億米ドルを診断インフラのアップグレードに投入するため、CAGRは7.62%と予測されます。日本と韓国の検査施設はすでに技術的に進んでおり、空間生物学に迅速に軸足を移す一方、東南アジア諸国は基礎的な病理組織検査能力に投資します。蘇州、深セン、ハイデラバードでは、抗体やスライドの現地製造クラスターが台頭し、供給の弾力性を高め、陸揚げコストを引き下げています。これと並行して、シンガポールやタイといった医療ツーリズムの中心地は、国際的に認定されたラボを求め、品質基準を高めています。

ラテンアメリカと中東・アフリカは新たなフロンティアです。ブラジル、サウジアラビア、アラブ首長国連邦は、民間病院の拡大と政府の近代化推進に後押しされ、それぞれの地域で支出をリードしています。とはいえ、不十分な診療報酬と熟練労働力不足により、全体の伸びは世界平均を下回っています。低所得国の診断ギャップを埋めるため、ターゲットを絞った援助プログラムやポイント・オブ・ケアのマイクロ流体工学が導入され、組織診断薬市場の対応可能ベースが徐々に拡大しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- がん罹患負担の増加

- 病理組織検査室における自動化とAIの加速

- 米国・EUにおけるデジタルパソロジー償還の拡大

- 人口の多いアジアでヘルスケアCAPEXが急増

- 空間生物学的手法によるマルチプレックスIHCの採用

- LMICs向けポイントオブケア・マイクロ流体組織プレパレーション

- 市場抑制要因

- 資本コストと消耗品コストが高いです。

- 訓練を受けた病理医の世界的不足

- プラットフォーム間のデータフォーマット相互運用性のギャップ

- 試薬・抗体サプライチェーンの変動性

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品別

- 機器

- スライド染色システム

- 組織処理システム

- ホールスライドスキャナー

- ミクロトーム&クライオスタット

- その他の機器

- 試薬と消耗品

- 抗体

- キット&アッセイ

- 試薬&プローブ

- その他の消耗品

- 機器

- 技術別

- 免疫組織化学

- インサイチュ・ハイブリダイゼーション

- デジタル病理

- その他のテクノロジー

- 用途別

- 乳がん

- 前立腺がん

- 非小細胞肺がん

- 胃がん

- リンパ腫

- その他

- エンドユーザー別

- 病院および診断研究所

- 製薬・バイオテクノロジー企業

- 調査・学術機関

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- F. Hoffmann-La Roche

- Danaher(Leica Biosystems)

- Agilent Technologies(Dako)

- Thermo Fisher Scientific

- Abbott Laboratories

- Merck KGaA

- Illumina

- QIAGEN

- PerkinElmer(Revvity)

- Sakura Finetek

- Epredia(PHC)

- 3DHISTECH

- Philips Digital & Computational Pathology

- PathAI

- OptraSCAN

- Indica Labs

- Biocare Medical

- Lunaphore Technologies

- Qritive

- Bio-Genex Laboratories

- Ventana Medical Systems(Roche)