|

市場調査レポート

商品コード

1822607

カーセキュリティシステムの市場機会、成長促進要因、産業動向分析と2025年~2034年予測Car Security System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| カーセキュリティシステムの市場機会、成長促進要因、産業動向分析と2025年~2034年予測 |

|

出版日: 2025年08月25日

発行: Global Market Insights Inc.

ページ情報: 英文 240 Pages

納期: 2~3営業日

|

概要

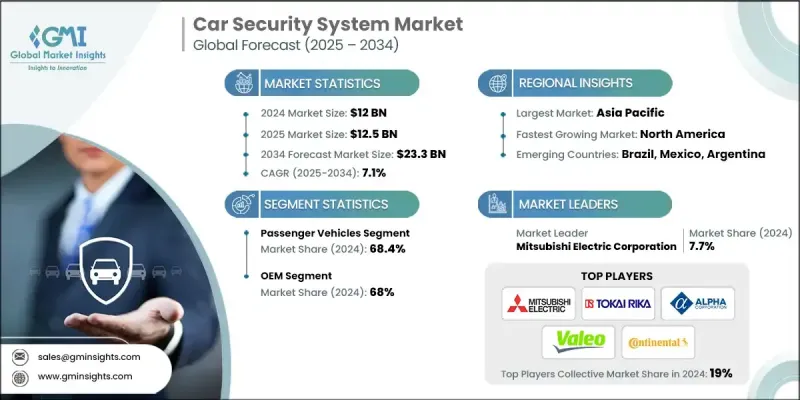

カーセキュリティシステムの世界市場規模は、2024年に120億米ドルとなり、CAGR 7.1%で成長し、2034年には233億米ドルに達すると予測されています。

世界中で車両盗難が増加していることが、高度なカーセキュリティシステムの需要増加の主な要因となっています。盗難の手口が巧妙になるにつれ、従来のロック機構では不正アクセスを抑止・防止することができなくなっています。このため、消費者も自動車メーカーも、GPSベースの追跡システム、エンジンイモビライザー、暗号化キーレス・エントリー、リアルタイムの警告通知など、強固なセキュリティ技術を優先するようになっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 120億米ドル |

| 予測金額 | 233億米ドル |

| CAGR | 7.1% |

乗用車での採用増加

強化された安全性と盗難防止ソリューションに対する消費者需要の高まりにより、乗用車セグメントは2024年に大きなシェアを占めました。都市化の進展と自動車所有率の上昇に伴い、乗用車の所有者は資産を保護するためにキーレス・エントリー、イモビライザー、GPS追跡などの高度なセキュリティ技術に多額の投資を行っています。このセグメントの成長を支えているのは、利便性と保護の両立を求める消費者の嗜好であり、メーカー各社は絶え間ない技術革新に取り組んでいます。

牽引役となるOEM

OEM分野は、新車に高度なセキュリティ機能を直接組み込むことを背景に、2024年に注目すべきシェアを獲得しました。OEMは、生体認証、暗号化キーフォブ、コネクテッド・ビークル・セキュリティ・ソリューションなどのシステムを製造中に組み込むために、テクノロジー・プロバイダーとの協力関係をますます強めています。この統合は、車両の安全性を高めるだけでなく、シームレスなユーザー体験を提供し、自動車メーカーに競争上の優位性をもたらします。

地域別洞察

有利な地域として台頭するアジア太平洋地域

アジア太平洋地域のカーセキュリティシステム市場は、急速な都市化、自動車販売の増加、人口密集都市における犯罪率の上昇に支えられ、2024年には大きなシェアを占める。中国、インド、東南アジアなどの市場では、自動車の安全性に対する消費者の意識が高まっており、高度なセキュリティ・ソリューションの採用が増加しています。さらに、スマートシティ構想や自動車技術への投資の高まりが、コネクテッド・カー・セキュリティ・システムやインテリジェント・カー・セキュリティ・システムに対する需要を促進しています。

カーセキュリティシステム市場の主要企業は、Tesla、東海理化、三菱電機、Qualcomm Technologies、ZF Friedrichshafen、ALPHA Corporation、Thales Group、Continental、Stoneridge、Valeo S.A.です。

市場ポジションを強化するため、カーセキュリティシステム業界の企業はイノベーションと戦略的パートナーシップを優先しています。AIを活用した侵入検知、スマートフォンとの連携、生体認証入退室管理などの最先端技術を開発するため、研究開発に多額の投資を行っています。自動車メーカーとの協業は、OEMのシームレスな統合を可能にし、システムの信頼性と顧客の信頼を高めています。さらに、企業は新たな顧客基盤を開拓するため、買収や新興市場への参入を通じて事業領域を拡大しています。保守や遠隔監視を含む包括的なアフターサービスを提供することで、企業は長期的な関係を築き、競合情勢の中で差別化を図ることもできます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 車両盗難とサイバー犯罪の増加

- コネクテッドカーと自動運転車の成長

- 自動車のサイバーセキュリティに対する規制の推進

- スマート機能に対する消費者の需要

- 業界の潜在的リスク&課題

- 高い導入コスト

- 技術の複雑さと信頼性の問題

- 市場機会

- 生体認証セキュリティの導入

- スマートモビリティとIoTとの統合

- アフターマーケットの成長可能性

- ブロックチェーンベースの鍵管理

- 促進要因

- 成長可能性分析

- 特許分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- サプライチェーンの脆弱性評価

- Tier-1、Tier-2、Tier-3サプライヤーのリスク分析

- サイバーセキュリティサプライチェーンの要件

- コンポーネントの認証と検証

- サプライチェーンの混乱の影響分析

- リスク軽減戦略とベストプラクティス

- サプライヤー認証およびコンプライアンス要件

- 技術の採用と成熟度分析

- 製品カテゴリー別の技術成熟度レベル(TRL)評価

- 地域別・車種別採用曲線分析

- テクノロジー統合の複雑さマトリックス

- 相互運用性と標準化のタイムライン

- イノベーションパイプラインとR&D投資分析

- 特許情勢と知的財産戦略分析

- 技術陳腐化リスク評価

- 費用便益とROI分析フレームワーク

- 総所有コスト(TCO)モデル

- OEMとアフターマーケットのROI分析

- 保険料への影響の定量化

- 盗難防止の費用便益分析

- メンテナンスとライフサイクルコストの内訳

- テクノロジーのアップグレードと移行コスト

- 消費者の支払い意思分析

- 規制コンプライアンスと標準分析

- UNECE R155/R156準拠コスト分析

- ISO/SAE 21434実装要件

- 地域規制状況の比較

- サイバーセキュリティ管理システム(CSMS)のコスト

- ソフトウェア更新管理システム(SUMS)の要件

- 認証および監査プロセス分析

- コンプライアンスタイムラインと罰則評価

- 将来の規制動向と影響

- 消費者行動と市場採用分析

- 消費者のセキュリティ意識と認識に関する調査

- 購入決定要因と価格感度

- 人口統計セグメントによる技術の受容

- 地域による消費者の嗜好の違い

- 導入障壁と抵抗要因

- ブランドの信頼とセキュリティ認識分析

- 消費者教育および啓発プログラム

- エンドユーザー体験と満足度分析

- 保険業界の統合とパートナーシップ分析

- 保険料削減モデル

- テレマティクスと利用ベースの保険の統合

- リスク評価と保険数理上の影響

- 保険会社の提携戦略

- クレーム削減と損失防止分析

- データ共有契約とプライバシーに関する考慮事項

- 保険統合に関する規制要件

- 将来の保険業界の連携モデル

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

- ユースケース

- 最良のシナリオ

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:車両別、2021-2034

- 主要動向

- 乗用車

- 商用車

- 電気自動車とハイブリッド車

第6章 市場推計・予測:製品別、2021-2034

- 主要動向

- イモビライザー

- リモートキーレスエントリー

- 集中ロックシステム

- 車の警報

- その他

第7章 市場推計・予測:技術別、2021-2034

- 主要動向

- 基本的なセキュリティ

- 中程度のセキュリティ

- 高度なセキュリティ

- 統合セキュリティエコシステム

第8章 市場推計・予測:販売チャネル別、2021-2034

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- グローバルプレーヤー

- Continental AG

- Delphi Technologies(BorgWarner)

- Denso Corporation

- Johnson Controls International

- Lear Corporation

- Magna International

- Robert Bosch

- Valeo

- 地域プレーヤー

- Alps Electric

- Mitsubishi Electric

- STRATTEC Security

- Tokai Rika

- TRW Automotive(ZF Friedrichshafen)

- Viper(VOXX International)

- 新興プレーヤー

- NXP Semiconductors N.V.

- Qualcomm Technologies

- Tesla

- Thales Group

- Upstream Security

- VicOne(Trend Micro)