|

|

市場調査レポート

商品コード

1171995

原子時計市場の2028年までの予測-タイプ別、アプリケーション別の世界分析Atomic Clock Market Forecast to 2028 - COVID-19 Impact and Global Analysis By Type and Application |

||||||

|

|

|||||||

| 原子時計市場の2028年までの予測-タイプ別、アプリケーション別の世界分析 |

|

出版日: 2022年11月21日

発行: The Insight Partners

ページ情報: 英文 146 Pages

納期: 即納可能

|

- 全表示

- 概要

- 図表

- 目次

原子時計市場は、2028年には7億4579万米ドルに達すると予測されています。2022年から2028年の間にCAGR6.5%で成長すると推定されます。

セシウム原子時計市場の需要は、電波天文学の研究所や計測学における精度向上のニーズの高まりにより高まっています。また、軍事、航空宇宙、ナビゲーション衛星は、セシウム原子時計の重要な用途の一つであり、パルサーの安定性の測定、ディファレンシャルGPS(DGPS)、地理探査、世界ポジショニングシステム(GPS)、地質学、古生物学、考古学、環境調査などに使用されています。米国はセシウム原子時計の最大の生産国であり、これが地域の原子時計市場の成長を促進しています。アジア太平洋地域では、中国と日本がセシウム原子時計を生産している主要国です。また、セシウム原子時計を提供している主要企業は、Microchip社とOscilloquartz社の2社です。また、Microsemiは、世界中の国立研究所で使用されているセシウムビームチューブクロックの唯一の商用サプライヤーです。さらに、インド宇宙研究機関(ISRO)は、独自のセシウム原子時計アンサンブルを開発しました。さらにISROは、ルビジウムを使った高精度原子時計の研究にも取り組んでいます。このような要因が原子時計の市場規模を押し上げています。

通信ネットワークプロバイダーは、消費者の増加に伴い、デジタル信号を効率的に伝送するために高精度の時計を必要としています。水素メーザー原子時計と比較すると、セシウムビームはホールドオーバーが高く、水素メーザー原子時計はサイズと消費電力が効果的です。そのため、水素メーザー原子時計はセシウムビーム原子時計よりもコストが高く、原子時計市場の需要を後押ししています。さらに、その高い技術習得率のため、水素メーザー原子時計の製造は厳しいプロセスとなっています。これらのクロックの製造には、高価な希少元素と技術者の確保が主な要件となります。これが、水素メーザー原子時計メーカーを減少させた主な理由です。しかし、ハイテク生産に従事する大企業は、時間の経過と需要の増加により、水素メーザー原子時計の市場規模に参入することができます。

現在、通信、ナビゲーション、金融取引、分散型クラウド、防衛などのアプリケーションのほとんどは、原子時計や最高度の原子発振精度に基づいて時間を追跡するクロックの正確なタイミングに依存しています。5GネットワークやGPSの代替など、新しいアプリケーションや技術では、ポータブルプラットフォームでの正確な計時が必要となり、高性能小型原子時計市場の需要を促進することになるでしょう。国防高等研究計画局(DARPA)は、過去数十年にわたり原子時計市場シェアの向上と小型化に多大な投資を行い、市販のチップスケール原子時計(CSAC)を生み出し、サイズ、重量、電力(SWaP)に関して前例のないタイミング安定性を実現しています。しかし、その設計に関連する物理学が、第一世代のCSACの性能を制限しています。例えば、校正の必要性や周波数ドリフトによってタイミング誤差が発生するため、ポータブルなパッケージで最高レベルの精度と信頼性を実現することは困難です。したがって、次世代チップスケール原子時計(CSACs)/小型化は、予測期間中に原子時計市場のプレーヤーに機会を提供すると予想されます。

欧州の原子時計市場の成長は、原子時計開発に焦点を当てたプロジェクトが増加していることに起因しています。2022年5月、アキュビート(ルビジウム発振器、タイムサーバー、GPS規律原子時計の大手プロバイダ)は、宇宙ミッションや深宇宙探査プログラムが高精度原子時計に依存しているとして、欧州宇宙機関(ESA)のJUICE(Jupiter Icy Moons Explorer)ミッション用の超安定発振器(USO)を開発・製造するために選ばれたと発表しています。欧州には、Satcom Global LtdやHolkirk Communications Ltd.などの衛星通信ソリューションプロバイダーが存在します。しかし、欧州のガリレオネットワークで衛星航法信号を駆動する搭載原子時計の故障が目立ち、軌道上にある18個の衛星のうち9個の時計が作動を停止しています。このような要因が、欧州における原子時計市場関係者のビジネスの成長を妨げています。

中国はAPACの原子時計市場において最も重要な収益貢献者の1つです。中国は、2021年に37.28%のシェアでAPAC原子時計市場をリードしました。2020年7月にBeiDou Navigation Satellite System(BDS)の正式な試運転を宣言し、世界のユーザーが正式に利用できるようになったことを示しました。BDSシステムには、400以上の機関、30万人の研究者・技術者が関わっています。衛星を開発する中国宇宙技術研究院(CAST)は、全国の一流の専門家やメーカーを集め、このプロジェクトのために最先端の技術や高品質の材料・製品を統合しました。ルビジウム原子時計は、BDS衛星に時間と周波数の基準を提供し、これらの時計はシステムの位置決め、速度測定、タイミングの精度に重要な役割を果たします。西安支社は過去20年間に、70個の高精度クロックを含む100個以上のルビジウム原子時計をBDSプログラムに納入しています。さらに、APACは予測期間中、世界の原子時計市場で最も高いCAGRを記録すると予想されています。インドや中国などでは、航空、通信、放送の衛星アンテナに原子時計が使用されるケースが増えており、予測期間中にこの地域の原子時計市場の成長を後押しすると予想されています。

AccuBeat ltd., Excelitas Technologies Corp., IQD Frequency Products Ltd., Leonardo, Microchip Technology Inc., Orolia, Oscilloquartz, Stanford Research Systems, Tekron, and VREMYA-CH JSCなどは、原子時計市場調査で紹介されている主要企業の一部です。原子時計市場のレポートは、主要なプレーヤーが今後数年間の成長を戦略化するのに役立つ、詳細な市場洞察を提供します。

原子時計市場の継続的な開拓は、市場の成長を促進しています。2022年11月、中国は現在建設中の野心的な宇宙ステーションの一部として、Mengtianと呼ばれる実験モジュールを打ち上げました。Mengtianには、水素時計、ルビジウム時計、光時計からなる世界初の宇宙ベースの冷原子時計のセットが搭載される予定です。

原子時計の世界市場は、種類と用途に基づいて区分されます。タイプ別では、ルビジウム原子時計とCSAC、セシウム原子時計、水素メーザー原子時計に区分されます。用途別に見ると、宇宙・軍事・航空宇宙、科学・計測研究、通信・放送、その他に区分されます。

原子時計市場は、北米、欧州、アジア太平洋(APAC)、中東・アフリカ(MEA)、南米の5つの主要地域に区分されています。2022年には、北米が最大のシェアを占め、欧州がそれに続く。さらに、APACは2022年から2028年にかけて、市場で最も高いCAGRを記録すると予想されています。

目次

第1章 イントロダクション

- 調査範囲

- インサイトパートナーズの調査報告書ガイダンス

- 市場セグメンテーション

- 原子時計市場-タイプ別

- 原子時計市場-アプリケーション別

- 原子時計市場-地域別

第2章 重要なポイント

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 原子時計市場の情勢

- 市場概要

- PEST分析

- 北米

- 欧州

- アジア太平洋地域

- 中東&アフリカ

- 南米

- エコシステム分析

- 専門家の見解

第5章 原子時計:市場力学

- 市場促進要因

- 航空宇宙、軍事分野での高精度原子時計へのニーズの高まり

- 時間に敏感なアプリケーションのため、計測ステーションからの高い需要

- 市場抑制要因

- 原子時計に関連する高コストと複雑さ

- 市場機会

- 次世代チップスケール原子時計(CSAC)

- デジタルインフラと5G基地局の台頭

- 今後の動向

- ストロンチウム、イッテルビウム、ガドリニウム原子の光学格子に基づく原子時計

- 促進要因と抑制要因のインパクト分析

第6章 原子時計市場:世界分析

- 原子時計の世界市場概要

- 市場のポジショニング-主要5社

第7章 原子時計の市場分析:タイプ別

- 原子時計市場:タイプ別(2021年、2028年)

- ルビジウム原子時計とCSAC

- セシウム原子時計

- 水素メーザー原子時計

第8章 原子時計の市場分析:アプリケーション別

- 原子時計市場:アプリケーション別(2021年、2028年)

- 宇宙・軍事・航空宇宙

- 科学と計測研究

- 通信・放送

- その他のアプリケーション

第9章 原子時計市場:地域別分析

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- イタリア

- 英国

- ロシア

- その他欧州

- APAC

- オーストラリア

- 中国

- インド

- 日本

- 韓国

- APACのその他諸国

- MEA

- 南アフリカ

- サウジアラビア

- UAE

- MEAの残りの地域

- 南米

- ブラジル

- アルゼンチン

- その他の南米地域

第10章 原子時計市場:COVID-19の影響分析

- 北米

- 欧州

- アジア太平洋地域

- 中東とアフリカ

- 南米

第11章 業界の情勢

- 市場への取り組み

- 新製品開発

- 合併・買収

第12章 企業プロファイル

- AccuBeat Ltd

- Excelitas Technologies Corp

- IQD Frequency Products Ltd

- Leonardo SpA

- Microchip Technology Inc

- Orolia

- Oscilloquartz SA

- Stanford Research Systems Inc

- Tekron International Ltd

- VREMYA-CH JSC

第13章 付録

- インサイト・パートナーズについて

- 単語索引

List Of Tables

- Table 1. Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Table 2. North America: Atomic Clock Market, by Type - Revenue and Forecast to 2028 (US$ Million)

- Table 3. North America: Atomic Clock Market, by Application - Revenue and Forecast to 2028 (US$ Million)

- Table 4. US: Atomic Clock Market, by Type -Revenue and Forecast to 2028 (US$ Million)

- Table 5. US: Atomic Clock Market, by Application -Revenue and Forecast to 2028 (US$ Million)

- Table 6. Canada: Atomic Clock Market, by Type -Revenue and Forecast to 2028 (US$ Million)

- Table 7. Canada: Atomic Clock Market, by Application -Revenue and Forecast to 2028 (US$ Million)

- Table 8. Mexico: Atomic Clock Market, by Type -Revenue and Forecast to 2028 (US$ Million)

- Table 9. Mexico: Atomic Clock Market, by Application -Revenue and Forecast to 2028 (US$ Million)

- Table 10. Europe: Atomic Clock Market, by Type - Revenue and Forecast to 2028 (US$ Million)

- Table 11. Europe: Atomic Clock Market, by Application - Revenue and Forecast to 2028 (US$ Million)

- Table 12. Germany: Atomic Clock Market, by Application -Revenue and Forecast to 2028 (US$ Million)

- Table 13. France: Atomic Clock Market, by Type -Revenue and Forecast to 2028 (US$ Million)

- Table 14. France: Atomic Clock Market, by Application -Revenue and Forecast to 2028 (US$ Million)

- Table 15. Italy: Atomic Clock Market, by Type -Revenue and Forecast to 2028 (US$ Million)

- Table 16. Italy: Atomic Clock Market, by Application -Revenue and Forecast to 2028 (US$ Million)

- Table 17. UK: Atomic Clock Market, by Type -Revenue and Forecast to 2028 (US$ Million)

- Table 18. UK: Atomic Clock Market, by Application -Revenue and Forecast to 2028 (US$ Million)

- Table 19. Russia: Atomic Clock Market, by Type -Revenue and Forecast to 2028 (US$ Million)

- Table 20. Russia: Atomic Clock Market, by Application -Revenue and Forecast to 2028 (US$ Million)

- Table 21. Rest of Europe: Atomic Clock Market, by Type -Revenue and Forecast to 2028 (US$ Million)

- Table 22. Rest of Europe: Atomic Clock Market, by Application -Revenue and Forecast to 2028 (US$ Million)

- Table 23. APAC: Atomic Clock Market, by Type - Revenue and Forecast to 2028 (US$ Million)

- Table 24. APAC: Atomic Clock Market, by Application - Revenue and Forecast to 2028 (US$ Million)

- Table 25. Australia: Atomic Clock Market, by Type -Revenue and Forecast to 2028 (US$ Million)

- Table 26. Australia: Atomic Clock Market, by Application -Revenue and Forecast to 2028 (US$ Million)

- Table 27. China: Atomic Clock Market, by Type -Revenue and Forecast to 2028 (US$ Million)

- Table 28. China: Atomic Clock Market, by Application -Revenue and Forecast to 2028 (US$ Million)

- Table 29. India: Atomic Clock Market, by Type -Revenue and Forecast to 2028 (US$ Million)

- Table 30. India: Atomic Clock Market, by Application -Revenue and Forecast to 2028 (US$ Million)

- Table 31. Japan: Atomic Clock Market, by Type -Revenue and Forecast to 2028 (US$ Million)

- Table 32. Japan: Atomic Clock Market, by Application -Revenue and Forecast to 2028 (US$ Million)

- Table 33. South Korea: Atomic Clock Market, by Type -Revenue and Forecast to 2028 (US$ Million)

- Table 34. South Korea: Atomic Clock Market, by Application -Revenue and Forecast to 2028 (US$ Million)

- Table 35. Rest of APAC: Atomic Clock Market, by Type -Revenue and Forecast to 2028 (US$ Million)

- Table 36. Rest of APAC: Atomic Clock Market, by Application -Revenue and Forecast to 2028 (US$ Million)

- Table 37. MEA: Atomic Clock Market, by Type- Revenue and Forecast to 2028 (US$ Million)

- Table 38. MEA: Atomic Clock Market, by Application - Revenue and Forecast to 2028 (US$ Million)

- Table 39. South Africa: Atomic Clock Market, by Type -Revenue and Forecast to 2028 (US$ Million)

- Table 40. South Africa: Atomic Clock Market, by Application -Revenue and Forecast to 2028 (US$ Million)

- Table 41. Saudi Arabia: Atomic Clock Market, by Type -Revenue and Forecast to 2028 (US$ Million)

- Table 42. UAE: Atomic Clock Market, by Type -Revenue and Forecast to 2028 (US$ Million)

- Table 43. UAE: Atomic Clock Market, by Application -Revenue and Forecast to 2028 (US$ Million)

- Table 44. Rest of MEA: Atomic Clock Market, by Type -Revenue and Forecast to 2028 (US$ Million)

- Table 45. Rest of MEA: Atomic Clock Market, by Application -Revenue and Forecast to 2028 (US$ Million)

- Table 46. SAM: Atomic Clock Market, by Type - Revenue and Forecast to 2028 (US$ Million)

- Table 47. SAM: Atomic Clock Market, by Application - Revenue and Forecast to 2028 (US$ Million)

- Table 48. Brazil: Atomic Clock Market, by Type -Revenue and Forecast to 2028 (US$ Million)

- Table 49. Brazil: Atomic Clock Market, by Application -Revenue and Forecast to 2028 (US$ Million)

- Table 50. Argentina: Atomic Clock Market, by Type -Revenue and Forecast to 2028 (US$ Million)

- Table 51. Argentina: Atomic Clock Market, by Application -Revenue and Forecast to 2028 (US$ Million)

- Table 52. Rest of SAM: Atomic Clock Market, by Type-Revenue and Forecast to 2028 (US$ Million)

- Table 53. Rest of SAM: Atomic Clock Market, by Application -Revenue and Forecast to 2028 (US$ Million)

- Table 54. List of Abbreviation

List Of Figures

- Figure 1. Atomic Clock Market Segmentation

- Figure 2. Atomic Clock Market Segmentation - By Geography

- Figure 3. Global Atomic Clock Market Overview

- Figure 4. Rubidium Atomic Clock and CSAC Type Segment held the Largest Share

- Figure 5. Space and Military/Aerospace Application Segment held the Largest Share

- Figure 6. APAC to Show Great Traction During Forecast Period

- Figure 7. North America: PEST Analysis

- Figure 8. Europe: PEST Analysis

- Figure 9. Asia-Pacific: PEST Analysis

- Figure 10. MEA: PEST Analysis

- Figure 11. South America: PEST Analysis

- Figure 12. Expert Opinion

- Figure 13. Atomic Clock Market Impact Analysis of Drivers and Restraints

- Figure 14. Geographic Overview of Atomic Clock Market

- Figure 15. Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 16. Atomic Clock Market Revenue Share, by Type (2021 and 2028)

- Figure 17. Rubidium Atomic Clock and CSAC: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 18. Cesium Atomic Clock: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 19. Hydrogen Maser Atomic Clock: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 20. Atomic Clock Market Revenue Share, by Application (2021 and 2028)

- Figure 21. Space and Military/Aerospace Research: Atomic Clock Market- Revenue and Forecast to 2028 (US$ Million)

- Figure 22. Scientific and Metrology Research: Atomic Clock Market- Revenue and Forecast to 2028 (US$ Million)

- Figure 23. Telecom and Broadcasting: Atomic Clock Market- Revenue and Forecast to 2028 (US$ Million)

- Figure 24. Other Applications: Atomic Clock Market- Revenue and Forecast to 2028 (US$ Million)

- Figure 25. Atomic Clock Market Revenue Share, By Region (2021 and 2028)

- Figure 26. North America: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 27. North America: Atomic Clock Market Revenue Share, by Type (2021 and 2028)

- Figure 28. North America: Atomic Clock Market Revenue Share, by Application (2021 and 2028)

- Figure 29. North America: Atomic Clock Market Revenue Share, by Key Country (2021 and 2028)

- Figure 30. US: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 31. Canada: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 32. Mexico: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 33. Europe: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 34. Europe: Atomic Clock Market Revenue Share, By Type (2021 and 2028)

- Figure 35. Europe: Atomic Clock Market Revenue Share, By Application (2021 and 2028)

- Figure 36. Europe: Atomic Clock Market Revenue Share, By Key Country (2021 and 2028)

- Figure 37. Germany: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 38. France: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 39. Italy: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 40. UK: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 41. Russia: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 42. Rest of Europe: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 43. APAC: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 44. APAC: Atomic Clock Market Revenue Share, By Type (2021 and 2028)

- Figure 45. APAC: Atomic Clock Market Revenue Share, By Application (2021 and 2028)

- Figure 46. APAC: Atomic Clock Market Revenue Share, By Key Country (2021 and 2028)

- Figure 47. Australia: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 48. China: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 49. India: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 50. Japan: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 51. South Korea: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 52. Rest of APAC: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 53. MEA: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 54. MEA: Atomic Clock Market Revenue Share, By Type (2021 and 2028)

- Figure 55. MEA: Atomic Clock Market Revenue Share, By Application (2021 and 2028)

- Figure 56. MEA: Atomic Clock Market Revenue Share, By Key Country (2021 and 2028)

- Figure 57. South Africa: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 58. Saudi Arabia: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 59. UAE: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 60. Rest of MEA: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 61. SAM: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 62. SAM: Atomic Clock Market Revenue Share, By Type (2021 and 2028)

- Figure 63. SAM: Atomic Clock Market Revenue Share, By Application (2021 and 2028)

- Figure 64. SAM: Atomic Clock Market Revenue Share, By Key Country (2021 and 2028)

- Figure 65. Brazil: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 66. Argentina: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 67. Rest of SAM: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- Figure 68. Impact of COVID-19 Pandemic in North American Market

- Figure 69. Impact of COVID-19 Pandemic in European Market

- Figure 70. Impact of COVID-19 Pandemic in APAC Market

- Figure 71. Impact of COVID-19 Pandemic in MEA Market

- Figure 72. Impact of COVID-19 Pandemic in South American Market

The atomic clock market is expected to reach US$ 745.79 million by 2028. It is estimated to grow at a CAGR of 6.5% during 2022-2028.

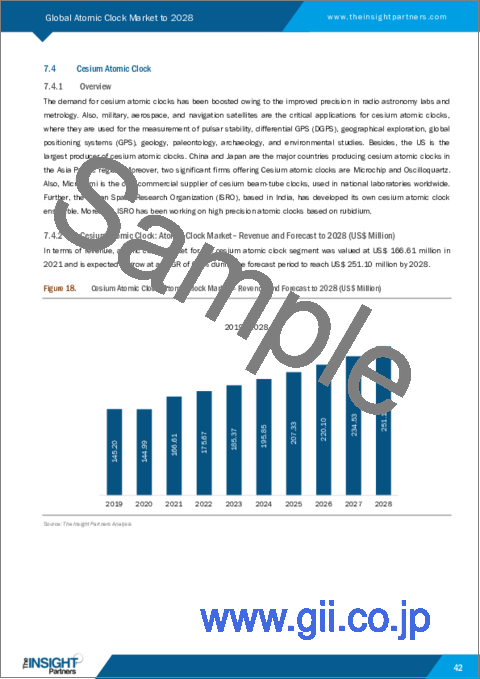

The cesium atomic clock market demand is rising due to the growing need for improved precision in radio astronomy labs and metrology. Also, military, aerospace, and navigation satellites are among the critical applications for cesium atomic clocks, where they are used for the measurement of pulsar stability, differential GPS (DGPS), geographical exploration, global positioning systems (GPS), geology, palaeontology, archaeology, and environmental studies. The US is the largest producer of cesium atomic clocks which is propelling the regional atomic clock market growth. China and Japan are major countries producing cesium atomic clocks in Asia Pacific. Moreover, two significant firms offering cesium atomic clocks are Microchip and Oscilloquartz. Also, Microsemi is the only commercial supplier of cesium beam-tube clocks, used in national laboratories across the world. Further, the Indian Space Research Organization (ISRO) has developed its own cesium atomic clock ensemble. Moreover, ISRO has been working on high precision atomic clocks based on rubidium. Such factors are bolstering the atomic clock market size.

With the increasing number of consumers, telecommunication network providers require highly precise clocks for digital signals to be transmitted effectively. Compared to hydrogen maser atomic clocks, the cesium beam has a higher holdover, while hydrogen maser atomic clocks are more effective in size and power consumption. Therefore, the cost of hydrogen maser atomic clock is higher than the cesium beams atomic clock, which fuels the demand for atomic clock market. In addition, due to its high technology learning curve, hydrogen maser atomic clock manufacturing is a stringent process. The key requirements for the manufacture of these clocks are the highly-priced rare elements and the availability of technical workers. These are the main reasons for the reduction in the number of hydrogen maser atomic clock producers. However, the larger companies engaged in high technology production can enter the hydrogen maser atomic clock market size with the passage of time and increasing demand.

At present, most of the applications for communication, navigation, financial transactions, distributed cloud, and defense rely on the accurate timing of atomic clocks or clocks that track time based on the highest degrees of atom oscillation accuracy. New applications and technologies such as 5G networks and GPS alternatives will need accurate timekeeping on portable platforms, which would propel the demand for high performance miniaturized atomic clock market. Defense Advanced Research Projects Agency (DARPA) has invested a huge amount in the advancement and miniaturization of atomic clock market share over the past few decades, generating commercially available chip-scale atomic clocks (CSACs) and offering unprecedented timing stability in regards with size, weight, and power (SWaP). However, the physics associated with their designs limit the performance of first-generation CSACs. For instance, timing errors can be created by calibration requirements and frequency drift, which makes it difficult to achieve the highest degrees of precision and reliability in a portable package. Thus, next-generation chip-scale atomic clock (CSACs)/miniaturization is anticipated to provide opportunities to the atomic clock market players during the forecast period.

The growth of the atomic clock market in Europe is attributed to the increasing number of projects focusing on atomic clock development. In May 2022, AccuBeat (a leading provider of Rubidium oscillators, Time Servers, and GPS disciplined atomic clock) announced that it was selected to develop and produce an Ultra Stable Oscillator (USO) for the European Space Agency's (ESA) JUICE (Jupiter Icy Moons Explorer) mission as Space missions and deep space exploration programs rely on high precision atomic clocks. Europe has the presence of satellite communication solutions providers such as Satcom Global Ltd and Holkirk Communications Ltd. However, the onboard atomic clocks driving satellite-navigation signals on the European Galileo network have noticeably failed, and 9 clocks have stopped working on the 18 satellites in orbit. These factors hinder the growth of the atomic clock market player's businesses in Europe.

China is one of the most significant revenue contributors to the atomic clock market in APAC. China led the APAC atomic clock market with a share of 37.28% in 2021. It declared the BeiDou Navigation Satellite System (BDS) official commissioning in July 2020, marking it formally available for global users. More than 400 agencies and 300,000 research personnel and technicians are involved in the BDS system. The China Academy of Space Technology (CAST), a satellite developer, has brought together leading experts and manufacturers across the country and integrated the most advanced technologies and high-quality materials and products for the project. Rubidium atomic clocks provide BDS satellites with time and frequency standards, and these clocks play vital role in the system's positioning, speed measurement, and timing accuracy. More than 100 rubidium atomic clocks, including 70 high-precision clocks, have been delivered to the BDS program by the Xi'an branch in the last two decades. Further, APAC is anticipated to register the highest CAGR in the global atomic clock market during the forecast period. The rise in the use of atomic clocks in satellite antennas in the aviation, telecommunications, and broadcasting applications in countries such as India and China is anticipated to boost the region's atomic clock market growth during the forecast period.

AccuBeat ltd., Excelitas Technologies Corp., IQD Frequency Products Ltd., Leonardo, Microchip Technology Inc., Orolia, Oscilloquartz, Stanford Research Systems, Tekron, and VREMYA-CH JSC are a few key players profiled in the atomic clock market study. The atomic clock market report provides detailed market insights, which will help the key players strategize growth in the coming years.

The ongoing developments in the atomic clock market are driving the market growth. In November 2022, China launched its lab module called Mengtian as a part of its ambitious space station currently under construction. Mengtian is set to carry the world's first space-based set of cold atomic clocks consisting of a hydrogen clock, a rubidium clock, and an optical clock.

The global atomic clock market is segmented on the basis of type and application. Based on type, the market is segmented into rubidium atomic clock and CSAC, cesium atomic clock, and hydrogen maser atomic clock. Based on application, the market is segmented into space and military/aerospace, scientific and metrology research, telecom/broadcasting, and others.

The atomic clock market is segmented into five major regions-North America, Europe, Asia Pacific (APAC), the Middle East & Africa (MEA), and South America. In 2022, North America is led the market with the largest share, followed by Europe. Further, APAC is expected to register the highest CAGR in the market from 2022 to 2028.

Reasons to Buy:

Save and reduce time carrying out entry-level research by identifying the growth, size, leading players and segments in the atomic clock market

Highlights key business priorities in order to assist companies to realign their business strategies

The key findings and recommendations highlight crucial progressive industry trends in the atomic clock market, thereby allowing players across the value chain to develop effective long-term strategies.

Develop/modify business expansion plans by using substantial growth offering developed and emerging markets.

Scrutinize in-depth global market trends and outlook coupled with the factors driving the market, as well as those hindering it.

Enhance the decision-making process by understanding the strategies that underpin commercial interest with respect to client products, segmentation, pricing and distribution.

Table Of Contents

1. Introduction

- 1.1 Study Scope

- 1.2 The Insight Partners Research Report Guidance

- 1.3 Market Segmentation

- 1.3.1 Atomic Clock Market - By Type

- 1.3.2 Atomic Clock Market - By Application

- 1.3.3 Atomic Clock Market- By Region

2. Key Takeaways

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. Atomic Clock Market Landscape

- 4.1 Market Overview

- 4.2 PEST Analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 South America

- 4.3 Ecosystem Analysis

- 4.4 Expert Opinion

5. Atomic Clock -Market Dynamics

- 5.1 Market Drivers

- 5.1.1 Increasing Need for a High Precision Atomic Clock in Aerospace and Military

- 5.1.2 High Demand from Metrology Station Owing to a Time-Sensitive Applications

- 5.2 Market Restraints

- 5.2.1 High Cost and Complexities Associated with Atomic Clocks

- 5.3 Market Opportunities

- 5.3.1 Next-Generation Chip-Scale Atomic Clocks (CSACs)

- 5.3.2 Emerging Digital Infrastructure and 5G Base Stations

- 5.4 Future Trends

- 5.4.1 Atomic Clocks based on Optical Lattices of Strontium, Ytterbium and Gadolinium Atoms

- 5.5 Impact Analysis of Drivers and Restraints

6. Atomic Clock Market - Global Analysis

- 6.1 Global Atomic Clock Market Overview

- 6.2 Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 6.3 Market Positioning - Five Key Players

7. Atomic Clock Market Analysis - By Type

- 7.1 Overview

- 7.2 Atomic Clock Market, By Type (2021 and 2028)

- 7.3 Rubidium Atomic Clock and CSAC

- 7.3.1 Overview

- 7.3.2 Rubidium Atomic Clock and CSAC: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 7.4 Cesium Atomic Clock

- 7.4.1 Overview

- 7.4.2 Cesium Atomic Clock: Atomic Clock Market- Revenue and Forecast to 2028 (US$ Million)

- 7.5 Hydrogen Maser Atomic Clock

- 7.5.1 Overview

- 7.5.2 Hydrogen Maser Atomic Clock: Atomic Clock Market- Revenue and Forecast to 2028 (US$ Million)

8. Atomic Clock Market Analysis - By Application

- 8.1 Overview

- 8.2 Atomic Clock Market, By Application (2021 and 2028)

- 8.3 Space and Military/Aerospace

- 8.3.1 Overview

- 8.3.2 Space and Military/Aerospace Research: Atomic Clock Market- Revenue and Forecast to 2028 (US$ Million)

- 8.4 Scientific and Metrology Research

- 8.4.1 Overview

- 8.4.2 Scientific and Metrology Research: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 8.5 Telecom and Broadcasting

- 8.5.1 Overview

- 8.5.2 Telecom and Broadcasting: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 8.6 Other Applications

- 8.6.1 Overview

- 8.6.2 Other Applications: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

9. Atomic Clock Market - Geographic Analysis

- 9.1 Overview

- 9.2 North America: Atomic Clock Market

- 9.2.1 North America: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.2.2 North America: Atomic Clock Market, by Type

- 9.2.3 North America: Atomic Clock Market, by Application

- 9.2.4 North America: Atomic Clock Market, by Key Country

- 9.2.4.1 US: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.2.4.1.1 US: Atomic Clock Market, by Type

- 9.2.4.1.2 US: Atomic Clock Market, by Application

- 9.2.4.2 Canada: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.2.4.2.1 Canada: Atomic Clock Market, by Type

- 9.2.4.2.2 Canada: Atomic Clock Market, by Application

- 9.2.4.3 Mexico: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.2.4.3.1 Mexico: Atomic Clock Market, by Type

- 9.2.4.3.2 Mexico: Atomic Clock Market, by Application

- 9.2.4.1 US: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.3 Europe: Atomic Clock Market

- 9.3.1 Europe: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.3.2 Europe: Atomic Clock Market, by Type

- 9.3.3 Europe: Atomic Clock Market, by Application

- 9.3.4 Europe: Atomic Clock Market, by Key Country

- 9.3.4.1 Germany: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.3.4.1.1 Germany: Atomic Clock Market, by Type

- 9.3.4.1.2 Germany: Atomic Clock Market, by Application

- 9.3.4.2 France: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.3.4.2.1 France: Atomic Clock Market, by Type

- 9.3.4.2.2 France: Atomic Clock Market, by Application

- 9.3.4.3 Italy: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.3.4.3.1 Italy: Atomic Clock Market, by Type

- 9.3.4.3.2 Italy: Atomic Clock Market, by Application

- 9.3.4.4 UK: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.3.4.4.1 UK: Atomic Clock Market, by Type

- 9.3.4.4.2 UK: Atomic Clock Market, by Application

- 9.3.4.5 Russia: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.3.4.5.1 Russia: Atomic Clock Market, by Type

- 9.3.4.5.2 Russia: Atomic Clock Market, by Application

- 9.3.4.6 Rest of Europe: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.3.4.6.1 Rest of Europe: Atomic Clock Market, by Type

- 9.3.4.6.2 Rest of Europe: Atomic Clock Market, by Application

- 9.3.4.1 Germany: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.4 APAC: Atomic Clock Market

- 9.4.1 APAC: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.4.2 APAC: Atomic Clock Market, by Type

- 9.4.3 APAC: Atomic Clock Market, by Application

- 9.4.4 APAC: Atomic Clock Market, by Key Country

- 9.4.4.1 Australia: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.4.4.1.1 Australia: Atomic Clock Market, by Type

- 9.4.4.1.2 Australia: Atomic Clock Market, by Application

- 9.4.4.2 China: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.4.4.2.1 China: Atomic Clock Market, by Type

- 9.4.4.2.2 China: Atomic Clock Market, by Application

- 9.4.4.3 India: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.4.4.3.1 India: Atomic Clock Market, by Type

- 9.4.4.3.2 India: Atomic Clock Market, by Application

- 9.4.4.4 Japan: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.4.4.4.1 Japan: Atomic Clock Market, by Type

- 9.4.4.4.2 Japan: Atomic Clock Market, by Application

- 9.4.4.5 South Korea: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.4.4.5.1 South Korea: Atomic Clock Market, by Type

- 9.4.4.5.2 South Korea: Atomic Clock Market, by Application

- 9.4.4.6 Rest of APAC: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.4.4.6.1 Rest of APAC: Atomic Clock Market, by Type

- 9.4.4.6.2 Rest of APAC: Atomic Clock Market, by Application

- 9.4.4.1 Australia: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.5 MEA: Atomic Clock Market

- 9.5.1 MEA: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.5.2 MEA: Atomic Clock Market, by Type

- 9.5.3 MEA: Atomic Clock Market, by Application

- 9.5.4 MEA: Atomic Clock Market, by Key Country

- 9.5.4.1 South Africa: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.5.4.1.1 South Africa: Atomic Clock Market, by Type

- 9.5.4.1.2 South Africa: Atomic Clock Market, by Application

- 9.5.4.2 Saudi Arabia: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.5.4.2.1 Saudi Arabia: Atomic Clock Market, by Type

- 9.5.4.2.2 Saudi Arabia: Atomic Clock Market, by Application

- 9.5.4.3 UAE: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.5.4.3.1 UAE: Atomic Clock Market, by Type

- 9.5.4.3.2 UAE: Atomic Clock Market, by Application

- 9.5.4.4 Rest of MEA: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.5.4.4.1 Rest of MEA: Atomic Clock Market, by Type

- 9.5.4.4.2 Rest of MEA: Atomic Clock Market, by Application

- 9.5.4.1 South Africa: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.6 SAM: Atomic Clock Market

- 9.6.1 SAM: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.6.2 SAM: Atomic Clock Market, by Type

- 9.6.3 SAM: Atomic Clock Market, by Application

- 9.6.4 SAM: Atomic Clock Market, by Key Country

- 9.6.4.1 Brazil: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.6.4.1.1 Brazil: Atomic Clock Market, by Type

- 9.6.4.1.2 Brazil: Atomic Clock Market, by Application

- 9.6.4.2 Argentina: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.6.4.2.1 Argentina: Atomic Clock Market, by Type

- 9.6.4.2.2 Argentina: Atomic Clock Market, by Application

- 9.6.4.3 Rest of SAM: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

- 9.6.4.3.1 Rest of SAM: Atomic Clock Market, by Type

- 9.6.4.3.2 Rest of SAM: Atomic Clock Market, by Application

- 9.6.4.1 Brazil: Atomic Clock Market - Revenue and Forecast to 2028 (US$ Million)

10. Atomic Clock Market- COVID-19 Impact Analysis

- 10.1 Overview

- 10.2 North America

- 10.3 Europe

- 10.4 Asia Pacific

- 10.5 Middle East and Africa

- 10.6 South America

11. Industry Landscape

- 11.1 Overview

- 11.2 Market Initiative

- 11.3 New Product Development

- 11.1 Merger and Acquisition

12. Company Profiles

- 12.1 AccuBeat Ltd

- 12.1.1 Key Facts

- 12.1.2 Business Description

- 12.1.3 Products and Services

- 12.1.4 Financial Overview

- 12.1.5 SWOT Analysis

- 12.1.6 Key Developments

- 12.2 Excelitas Technologies Corp

- 12.2.1 Key Facts

- 12.2.2 Business Description

- 12.2.3 Products and Services

- 12.2.4 Financial Overview

- 12.2.5 SWOT Analysis

- 12.2.6 Key Developments

- 12.3 IQD Frequency Products Ltd

- 12.3.1 Key Facts

- 12.3.2 Business Description

- 12.3.3 Products and Services

- 12.3.4 Financial Overview

- 12.3.5 SWOT Analysis

- 12.3.6 Key Developments

- 12.4 Leonardo SpA

- 12.4.1 Key Facts

- 12.4.2 Business Description

- 12.4.3 Products and Services

- 12.4.4 Financial Overview

- 12.4.5 SWOT Analysis

- 12.4.6 Key Developments

- 12.5 Microchip Technology Inc

- 12.5.1 Key Facts

- 12.5.2 Business Description

- 12.5.3 Products and Services

- 12.5.4 Financial Overview

- 12.5.5 SWOT Analysis

- 12.5.6 Key Developments

- 12.6 Orolia

- 12.6.1 Key Facts

- 12.6.2 Business Description

- 12.6.3 Products and Services

- 12.6.4 Financial Overview

- 12.6.5 SWOT Analysis

- 12.6.6 Key Developments

- 12.7 Oscilloquartz SA

- 12.7.1 Key Facts

- 12.7.2 Business Description

- 12.7.3 Products and Services

- 12.7.4 Financial Overview

- 12.7.5 SWOT Analysis

- 12.7.6 Key Developments

- 12.8 Stanford Research Systems Inc

- 12.8.1 Key Facts

- 12.8.2 Business Description

- 12.8.3 Products and Services

- 12.8.4 Financial Overview

- 12.8.5 SWOT Analysis

- 12.8.6 Key Developments

- 12.9 Tekron International Ltd

- 12.9.1 Key Facts

- 12.9.2 Business Description

- 12.9.3 Products and Services

- 12.9.4 Financial Overview

- 12.9.5 SWOT Analysis

- 12.9.6 Key Developments

- 12.10 VREMYA-CH JSC

- 12.10.1 Key Facts

- 12.10.2 Business Description

- 12.10.3 Products and Services

- 12.10.4 Financial Overview

- 12.10.5 SWOT Analysis

- 12.10.6 Key Developments

13. Appendix

- 13.1 About The Insight Partners

- 13.2 Word Index