|

|

市場調査レポート

商品コード

1071378

ペプチド治療薬の世界市場と治験の考察 (2028年)Global Peptide Therapeutics Market & Clinical Trials Insight 2028 |

||||||

|

|

|||||||

| ペプチド治療薬の世界市場と治験の考察 (2028年) |

|

出版日: 2022年04月01日

発行: PNS Pharma

ページ情報: 英文 1200 Pages

納期: 即日から翌営業日

|

- 全表示

- 概要

- 図表

- 目次

世界のペプチド治療薬の市場規模は、2028年までに750億米ドルに達すると見込まれています。現在、800品目以上のペプチド治療薬が治験段階にあり、200品目以上が上市されています。

適応症別に見ると、がんペプチドが世界市場の25%以上のシェアを占めています。

当レポートでは、世界のペプチド治療薬市場における治験の動向について分析し、製品の概要や市場の成長見通し、全体的な治験の概況、製品種類別の治験の進行状況 (企業別・適応症別・フェーズ別)、主要企業のプロファイルと競合情勢、といった情報を取りまとめてお届けいたします。

目次

第1章 ペプチド治療薬:概要

- ペプチド治療薬の概要

- ペプチド治療薬の歴史的展望

- 抗がんペプチドの分類

第2章 治療用ペプチドの標的

- シグナル伝達経路

- 細胞周期の調節

- 細胞死経路

- 腫瘍抑制タンパク質

- 転写因子

第3章 世界のペプチド治療薬市場:概要

第4章 世界のペプチド治療薬:治験の概要

- 企業別

- 国別

- 適応症別

- 患者セグメント別

- フェーズ別 (相別)

第5章 インスリンの臨床パイプライン:企業別・適応症別・フェーズ別

- 研究

- 前臨床

- フェーズI

- フェーズII

- フェーズII/III

- フェーズIII

- 申請済み

- 承認済み

- 上市済み

第6章 グルカゴン様ペプチドの臨床パイプライン:企業別・適応症別・フェーズ別

第7章 ペプチドの臨床パイプライン:企業別・適応症別・フェーズ別

第8章 環状ペプチドの臨床パイプライン:企業別・適応症別・フェーズ別

第9章 マルチペプチドの臨床パイプライン:企業別・適応症別・フェーズ別

第10章 糖ペプチドの臨床パイプライン:企業別・適応症別・フェーズ別

第11章 オリゴペプチドの臨床パイプライン:企業別・適応症別・フェーズ別

第12章 リポペプチドの臨床パイプライン:企業別・適応症別・フェーズ別

第13章 ジペプチドの臨床パイプライン:企業別・適応症別・フェーズ別

第14章 オピオイドペプチドの臨床パイプライン:企業別・適応症別・フェーズ別

第15章 デプシペプチドの臨床パイプライン:企業別・適応症別・フェーズ別

第16章 神経ペプチドの臨床パイプライン:企業別・適応症別・フェーズ別

第17章 ナトリウム利尿ペプチドの臨床パイプライン:企業別・適応症別・フェーズ別

第18章 二環式ペプチドの臨床パイプライン:企業別・適応症別・フェーズ別

第19章 競合情勢

- Amgen

- Amylin Pharmaceuticals

- Apitope Technology

- BioPartners

- BiondVax Pharmaceuticals Ltd

- Boehringer Ingelheim

- Circassia

- Corden Pharma (Peptisyntha)

- Eli Lily

- Galena Biopharmaceuticals

- GlaxoSmithKline

- Hyperion Therapeutics

- ImmunoCellular Therapeutics

- Ipsen

- Lonza

- Merck

- NovoNordisk

- Par Pharmaceuticals

- PeptiDream

- Roche

- Sanofi

- Tarix Pharmaceuticals

List of Figures

- Figure 1-1: Classification of Anti-Cancer Peptides

- Figure 2-1: Therapeutic Peptides Based on Their Biological Targets

- Figure 2-2: MAPK Signaling Pathways

- Figure 2-3: Cell Cycle in Eukaryotic

- Figure 2-4: Cell Death Pathways

- Figure 2-5: Features of Bcl-2 Family Proteins Including Anti-Apoptotic & Pro-Apoptotic

- Figure 3-1: Global - Peptide Therapeutic Market (US$ Billion), 2020 - 2028

- Figure 3-2: Global - Total Peptide Therapeutic Market Size vs. Cancer Peptide Therapeutic Market (US$ Billion), 2021

- Figure 3-3: Global - Cancer Peptide Market Share in Total Peptide Market (%), 2021

- Figure 3-4: Global - Cancer Peptide Drugs Market Size (US$ Billion), 2020 - 2028

- Figure 4-1: Global - Peptide Drug Clinical Pipeline by Company (Number of Drugs), 2022 till 2028

- Figure 4-2: Global - Peptide Drug Clinical Pipeline by Country (Number of Drugs), 2022 till 2028

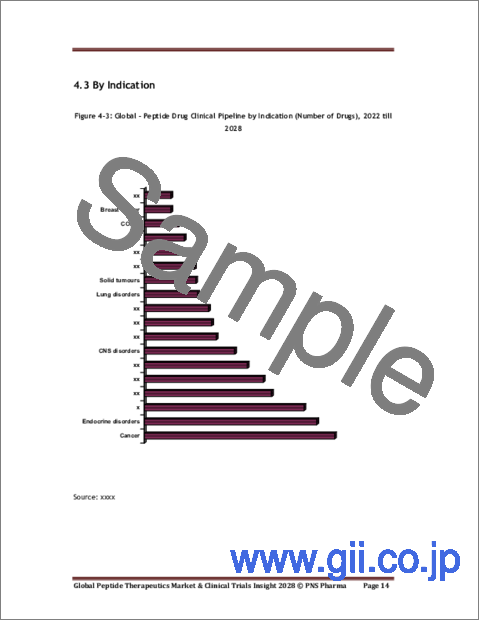

- Figure 4-3: Global - Peptide Drug Clinical Pipeline by Indication (Number of Drugs), 2022 till 2028

- Figure 4-4: Global - Peptide Drug Clinical Pipeline by Patient Segment (Number of Drugs), 2022 till 2028

- Figure 4-5: Global - Peptide Drug Clinical Pipeline by Phase (Number of Drugs), 2022 till 2028

“Global Peptide Therapeutics Market & Clinical Trials Insight 2028” Report findings:

- Global Peptide Therapeutics Market Opportunity > USD 75 billion by 2028

- Global Peptide Therapeutics Clinical Trials Insight by Company, Indication & Phase

- Peptide Therapeutics in Clinical trials: > 800 Drugs

- Peptide Therapeutics Commercially Available In Market: > 200 Drugs

- Global Peptide Therapeutics Clinical Trials Insight By Peptide Type: Glucagon-like Peptides, Cyclic Peptides, Glycopeptides, Oligopeptides, Lipopeptides, Dipeptides, Opioid, Depsipeptides, Neuropeptides, Natriuretic, Bicyclic Peptides

Peptides are naturally occurring, small biological molecules made of short chains of amino acids linked by a peptide bond, performing multiple functions within the cell. Peptide drugs have been in use for almost a century now, though initially they were only used to replicate the action of natural hormones for metabolic diseases, for example, the first of this kind that was approved for clinical usage was insulin for the management of diabetes. However, decades of research and development of peptides have resulted in the discovery of peptides that have the ability to penetrate the cell with advanced actions, all of which have shown excellent results for various therapeutic functions.

Till date, more than 200 peptide based therapeutics have gained approval from regulatory bodies. The most common indications for peptides are oncology, endocrinology, and metabolic diseases. Other target areas of peptides that have gained attention include gastroenterology, cardiovascular diseases, dermatology, bone diseases, and sexual dysfunction. The robust response of peptide therapeutics in the market has propelled the further research activities in this domain. Currently, more than 800 clinical trials are ongoing in global peptide therapeutics market which suggests promising future of peptide therapeutics in the forthcoming years.

The global peptide therapeutics market is both competitive along with being fragmented on account of the presence of several international and also domestic industry players. Such industry players have utilized an assorted innovative strategies for being at the top along with sufficing to the burgeoning requirement of the esteemed clients including geographic expansions, collaborations, joint ventures, new product launches, partnerships, contracts, and much more. For instance, Bicycle Therapeutics has entered into strategic collaboration with Genentech to discover, develop and commercialize novel Bicycle®-based immuno-oncology therapies. Further, Fusion Pharmaceuticals also enter into collaboration with Pepscan to discover, novel, peptide-based radiopharmaceuticals for the management of solid tumors.

By therapeutic indication, cancer peptide occupies more than 25% share in the global market. Several peptide based drugs including Firmagon, Eligard, Velcade, Zoladex, Cosmegen, Sandostatin, Mepact, and others have entered the market and have shown robust response rate. More recently, peptide cancer vaccine namely Riavax have also gained approval in South Korea for the treatment of locally advanced or metastatic pancreatic cancer. The promising sales of these drugs are driving this segment during the forecast period. Furthermore, surge in prevalence of cancer and unmet need of cost effective targeted drugs are also anticipated to propel the growth of cancer peptide drugs during the forecast period.

It is analyzed that the future holds an extensive place for peptides in addressing the greatest of medical challenge due to their capability of being adapted and modified to achieve the desired action. There is immense scope for the development of new peptides with protein fragmentation along with alternative routes of administration and improved oral bioavailability. They will also be used to address the currently undruggable targets in the coming years. Keeping the clinical pipeline in consideration, it is expected that the global peptide therapeutics market will surpass US$ 75 Billion by 2028. In addition to above mentioned factors, rising geriatric population and associated increase in chronic disease will also drive the growth of market.

The report provides detailed review of the overall market landscape of peptide-based therapies, including information on their current phase of development (marketed, clinical, preclinical and discovery), type of peptide, route of administration, and key therapeutic area. The report also gives insightful market assessment summary, highlighting the clinical and commercial attractiveness of pipeline molecules. This report forecasts revenue growth at global levels and provides an analysis of the latest trends and opportunities. The major companies mentioned in the report include Amgen, GlaxoSmithKline, NovoNordisk, ImmunoCellular Therapeutics, Lonza, PeptiDream and others.

Table of Contents

1. Introduction to Peptide Therapeutics

- 1.1. Overview of Peptide Therapeutics

- 1.2. Historical Perspective of Peptide Therapeutics

- 1.3. Classification Of Anti Cancer Peptides

2. Targets for Therapeutic Peptides

- 2.1. Signal Transduction Pathways

- 2.2. Cell Cycle Regulation

- 2.3. Cell Death Pathways

- 2.4. Tumor Suppressor Protein

- 2.5. Transcription Factors

3. Global Peptide Therapeutics Market Overview

4. Global Peptide Therapeutics Clinical Trials Overview

- 4.1. By Company

- 4.2. By Country

- 4.3. By Indication

- 4.4. By Patient Segment

- 4.5. By Phase

5. Insulin Clinical Pipeline By Company, Indication & Phase

- 5.1. Research

- 5.2. Preclinical

- 5.3. Phase-I

- 5.4. Phase-II

- 5.5. Phase-II/III

- 5.6. Phase-III

- 5.7. Preregistration

- 5.8. Registered

- 5.9. Marketed

6. Glucagon-like Peptides Clinical Pipeline By Company, Indication & Phase

- 6.1. Research

- 6.2. Preclinical

- 6.3. Phase-I

- 6.4. Phase-I/II

- 6.5. Phase-II

- 6.6. Phase-III

- 6.7. Preregistration

- 6.8. Marketed

7. Peptides Clinical Pipeline By Company, Indication & Phase

- 7.1. Research

- 7.2. Preclinical

- 7.3. Clinical Phase Unknown

- 7.4. Phase-I

- 7.5. Phase-I/II

- 7.6. Phase-II

- 7.7. Phase-II/III

- 7.8. Phase-III

- 7.9. Preregistration

- 7.12. Registered

- 7.11. Marketed

8. Cyclic Peptides Clinical Pipeline By Company, Indication & Phase

- 8.1. Research

- 8.2. Preclinical

- 8.3. Clinical Phase Unknown

- 8.4. Phase-I

- 8.5. Phase-II

- 8.6. Phase-III

- 8.7. Marketed

9. Multiple Peptides Clinical Pipeline By Company, Indication & Phase

- 9.1. Research

- 9.2. Preclinical

- 9.3. Phase-I

- 9.4. Phase-I/II

- 9.5. Phase-II

- 9.6. Phase-III

- 9.7. Preregistration

- 9.8. Registered

- 9.9. Marketed

10. Glycopeptides Clinical Pipeline By Company, Indication & Phase

- 10.1. Research

- 10.2. Preclinical

- 10.3. Phase-I

- 10.4. Phase-I/II

- 10.5. Preregistration

- 10.6. Marketed

11. Oligopeptides Clinical Pipeline By Company, Indication & Phase

- 11.1. Preclinical

- 11.2. Phase-I/II

- 11.3. Phase-II

- 11.4. Phase-II/III

- 11.5. Phase-III

- 11.6. Registered

- 11.7. Marketed

12. Lipopeptides Clinical Pipeline By Company, Indication & Phase

- 12.1. Research

- 12.2. Phase-II

- 12.3. Marketed

13. Dipeptides Clinical Pipeline By Company, Indication & Phase

- 13.1. Research

- 13.2. Phase-I

- 13.3. Phase-II

- 13.4. Phase-III

- 13.5. Registered

- 13.6. Marketed

14. Opioid Peptides Clinical Pipeline By Company, Indication & Phase

- 14.1. Research

- 14.2. Preclinical

- 14.3. Phase-I/II

- 14.4. Preregistration

- 14.5. Registered

- 14.6. Marketed

15. Depsipeptides Clinical Pipeline By Company, Indication & Phase

- 15.1. Preclinical

- 15.2. Phase-II

- 15.3. Registered

- 15.4. Marketed

16. Neuropeptides Clinical Pipeline By Company, Indication & Phase

- 16.1. Research

- 16.2. Preclinical

- 16.3. Phase-I/II

- 16.4. Phase-II

- 16.5. Marketed

17. Natriuretic Peptides Clinical Pipeline By Company, Indication & Phase

- 17.1. Phase-II

- 17.2. Marketed

18. Bicyclic Peptides Clinical Pipeline By Company, Indication & Phase

- 18.1. Preclinical

19. Competitive Landscape

- 19.1. Amgen

- 19.2. Amylin Pharmaceuticals

- 19.3. Apitope Technology

- 19.4. BioPartners

- 19.5. BiondVax Pharmaceuticals Ltd

- 19.6. Boehringer Ingelheim

- 19.7. Circassia

- 19.8. Corden Pharma (Peptisyntha)

- 19.9. Eli Lily

- 19.10. Galena Biopharmaceuticals

- 19.11. GlaxoSmithKline

- 19.12. Hyperion Therapeutics

- 19.13. ImmunoCellular Therapeutics

- 19.14. Ipsen

- 19.15. Lonza

- 19.16. Merck

- 19.17. NovoNordisk

- 19.18. Par Pharmaceuticals

- 19.19. PeptiDream

- 19.20. Roche

- 19.21. Sanofi

- 19.22. Tarix Pharmaceuticals