|

|

市場調査レポート

商品コード

1189824

抗凝固剤市場- 成長、動向、予測(2023年-2028年)Anticoagulants Market - Growth, Trends, and Forecasts (2023 - 2028) |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 抗凝固剤市場- 成長、動向、予測(2023年-2028年) |

|

出版日: 2023年01月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

抗凝固剤市場は予測期間(2022-2027年)にCAGR9.41%を記録すると予想されています。

COVID-19感染は、研究のスピードが速いため、抗凝固剤業界に大きな影響を与えることが予想されます。2020年にAmerican Journal of Cardiovascular Drugsに掲載された研究によると、COVID-19患者における抗凝固剤の可能性を評価するために、現在10以上の臨床試験が行われており、重篤なCOVID-19患者に使用するためにこれらの薬の非経口投与戦略に関する研究が行われています。その結果、COVID-19のパンデミックは当該市場に直接的、間接的に影響を及ぼすと予想されます。さらに、2021年1月の世界保健機関(WHO)のUpdateによると、COVID-19の患者は、確定患者と疑い患者の両方が低用量の抗凝固剤によるフォローアップ医療を受けられる必要があるとのことです。このように、COVID-19の期間中、抗凝固剤の需要が増加しました。

これは、慢性疾患の発生率の増加と抗凝固剤製品の開発における技術的進歩に起因しています。抗凝固剤は、血栓が重要な臓器への血液の流れを妨げ、心臓発作や脳卒中を引き起こす可能性があるため、深刻な合併症を引き起こす可能性のある血管(動脈または静脈)をブロックする血栓の治療と予防に使用されます。世界保健機関(WHO)の2021年6月発表によると、世界では毎年、推定1790万人が心血管系疾患が原因で死亡しています。これは、世界の死因の35%に相当します。さらに、これらの心血管疾患による死亡の85%は、心臓発作と脳卒中によるものです。また、2020年7月にCureus Journal of Medical Scienceに掲載された論文によると、虚血性心疾患(IHD)は世界の死因の上位を占めているとのことです。虚血性心疾患は、世界で約1億2600万人(10万人あたり1655人)が罹患しており、これは世界人口の約1.72%にあたります。虚血性心疾患の世界の有病率は、2030年には10万人あたり1,845人を超えると予想されています。さらに、慢性疾患の症例数の増加、個人が採用する不健康なライフスタイル、新規経口抗凝固剤(NOAC)の採用拡大が、抗凝固剤市場の主要な促進要因となっています。

さらに、抗凝固剤製品の開発や承認における技術的進歩も、市場の成長を促進しています。For Instance, 2021年6月、米国食品医薬品局は、ベーリンガーインゲルハイムのダビガトランエテキシレート(プラザキサ)抗凝固剤経口ペレットを、静脈血栓塞栓症の3ヶ月から12歳未満の小児が注射で投与される血液希釈剤による治療を少なくとも5日間受けた後に治療するための最初の経口抗凝固剤として承認しました。

このように、前述のすべての要因が、予測期間中の抗凝固剤市場の成長を促進すると予想されます。しかし、厳しい規制や治療に伴う副作用が、予測期間中の市場成長を抑制しています。

主な市場動向

新規経口抗凝固剤(NOACs)セグメントは、抗凝固剤市場において重要な市場シェアを占めると予想される

新規経口抗凝固剤(NOACs)セグメントは、抗凝固剤市場において大きなシェアを占めており、新興諸国における新規経口抗凝固剤(NOACs)の採用拡大やワルファリンに対するNOACsの高い嗜好性から、予測期間中も同様の傾向を示すと予想されます。

新規経口抗凝固剤(NOAC)は、新しいクラスの抗凝固剤です。さらに、これらは安全性が高く(大出血の発生率が低い)、使用が便利で、食品との相互作用がなく、半減期が短いという特徴があります。NOACには、ダビガトラン、リバーロキサバン、アピキサバン、エドキサバンなどがあります。これらは、心房細動・心筋梗塞、深部静脈血栓症(DVT)、肺塞栓症の予防および治療に使用することができます。

米国疾病管理予防センター(CDC)の2022年6月の更新情報によると、米国では毎年、約90万人(人口1,000人あたり1~2人)が深部静脈血栓症に罹患する可能性があるとされています。さらに、約6万~10万人の米国人が深部静脈血栓症で死亡しています。このように、心血管障害、静脈血栓塞栓症(VTE)の発生率の増加、および新製品開発における技術の進歩が、新規経口抗凝固剤(NOACs)セグメントの主要な促進要因となっています。

さらに、製品の発売と製品承認は、予測期間中の市場成長を予想しました。例えば、2021年6月、米国食品医薬品局(FDA)は、静脈血栓塞栓症(静脈に血栓ができる状態)の3カ月から12歳未満の小児が、少なくとも5日間注射で投与される血液希釈剤で治療した後に直接プラザキサ(ダビガトランエテクシレート)の経口ペレットを治療する目的で承認しました。また、FDAは、初回の静脈血栓塞栓症の治療を終えた生後3ヶ月から12歳未満の患者さんにおける血栓の再発防止を目的として、プラダキサ経口ペレットを承認しています。

このように、上記の要因から、この市場は予測期間中に成長を見せると予想されます。

予測期間中、北米が市場の主要なシェアを占める

北米は、革新的な製品に対する高い需要と、この地域における心血管障害の有病率の増加により、世界の抗凝固剤市場において主要な市場シェアを占めると予想されます。インスタンス、2021年10月のアメリカ心臓協会調査によると、毎日約2,300人のアメリカ人が心血管疾患により死亡しており、平均すると38秒に1人の割合で死亡しています。

また、2022年2月の疾病管理予防センターによると、年間約659,000人のアメリカ人が心臓病で亡くなっています。これは、米国全体の死因のほぼ25%に相当します。このように、心血管疾患の増加は、抗凝固剤の需要が地域で増加し、それによって市場を後押しします。

さらに、治療薬の開発に携わるトップ製薬会社やバイオテクノロジー企業の存在、確立された医療インフラの存在も、地域市場全体の成長を大きく後押ししています。例えば、2021年12月、ジョンソン・エンド・ジョンソンのヤンセンファーマカンパニーズは、ザレルト(リバーロキサバン)の2つの小児適応について食品医薬品局の承認を受けました:最初の非経口(注射または点滴)抗凝固剤治療を少なくとも5日間行った後の生後から18歳未満の患者の静脈血栓塞栓症(VTE)の治療およびVTE再発リスクの軽減、ならびに血栓予防(血栓予防)です。

このように、慢性疾患の増加や主要な市場関係者による製品の上市など、前述のすべての要因が北米の抗凝固剤市場を後押ししています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査対象範囲

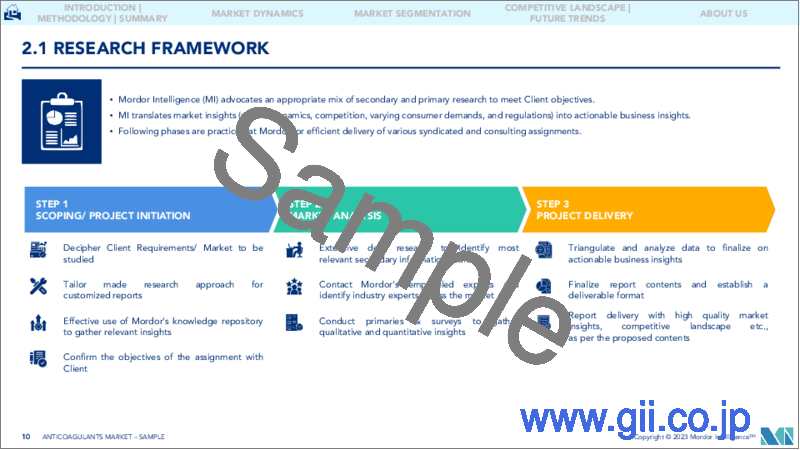

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 慢性疾患の患者数の増加

- 抗凝固剤開発における技術的進歩

- 新規経口抗凝固剤(NOACs)の採用拡大

- 市場抑制要因

- 厳しい政府規制

- 治療に伴う副作用

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション(金額ベース市場規模- 百万米ドル)

- 薬物クラス別

- 新規経口抗凝固剤(NOACs)

- ヘパリンおよび低分子ヘパリン(LMWH)

- ビタミンK拮抗薬

- アプリケーション別

- 心房細動・心筋梗塞(ハートアタック)

- 深部静脈血栓症(DVT)

- 肺塞栓症

- その他の適応症

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ地域

- GCC

- 南アフリカ共和国

- その他の中東・アフリカ地域

- 南米地域

- ブラジル

- アルゼンチン

- その他の南米地域

- 北米

第6章 競合情勢

- 企業プロファイル

- Johnson & Johnson

- Bayer AG

- Boehringer Ingelheim GmbH

- Bristol-Myers Squibb Company

- Daiichi Sankyo Company

- Abbott Laboratories

- Aspen Holdings

- Sanofi

- Pfizer, Inc

- Alexion Pharmaceuticals Inc.

- Leo Pharma AS

- Dr. Reddy's Laboratories

第7章 市場機会と今後の動向

The Anticoagulants Market is expected to register a CAGR of 9.41% during the forecast period (2022-2027).

COVID-19 infection is expected to have a substantial impact on the anticoagulant industry due to the quick pace of research. More than ten clinical trials are currently underway to assess the potential of anticoagulants in COVID-19 patients, according to a study published in the American Journal of Cardiovascular Drugs in 2020, and research on parenteral administration strategies for these drugs is being conducted for use in critically ill COVID-19 patients. As a result, the COVID-19 pandemic is expected to have both direct and indirect implications for the market in question. Furthermore, according to World Health Organization Update in January 2021, patients with COVID-19, both confirmed and suspected, should have access to follow-up care with low-dose anticoagulants, according to the World Health Organization. Thus, the demand for anticoagulants increased during COVID-19.

This is attributed to an increase in the incidence of chronic diseases and technological advances in the development of anticoagulant products. Anticoagulants are used to treat and prevent blood clots which can block blood vessels (an artery or a vein) that can lead to serious complications as the clot disrupts the flow of blood to important organs and can result in heart attack and stroke. According to the World Health Organization June 2021, an estimated 17.9 million people die due to cardiovascular diseases worldwide, each year. This represents 35% of global deaths. Additionally, 85% of these cardiovascular disease deaths are due to heart attack and stroke. In addition, according to the article published in Cureus Journal of Medical Science in July 2020, ischemic heart disease (IHD) is a leading cause of death worldwide. Ischemic heart disease affects around 126 million individuals (1,655 per 100,000) globally, which is approximately 1.72% of the world's population. The global prevalence of ischemic heart disease is expected to exceed 1,845 per 100,000 by the year 2030. Furthermore, increasing cases of chronic diseases, unhealthy lifestyles adopted by individuals, and growing adoption of novel oral anticoagulants (NOACs) are the key driving factors in the anticoagulants market.

Moreover, technological advancements in the development of anticoagulant products and approvals are also propelling the growth of the market. For Instance, In June 2021, United States Food and Drug Administration approved Boehringer Ingelheim's dabigatran etexilate (Pradaxa) anticoagulant oral pellets as the first oral anticoagulant to treat children aged 3 months to less than 12 years old with venous thromboembolism after they have received at least five days of treatment with a blood thinner given by injection.

Thus, all the aforementioned factor is expected to drive the growth of the anticoagulant market over the forecast period. However, stringent regulation and side effects associated with the treatment restrain the market growth over the forecast period.

Key Market Trends

Novel Oral Anticoagulants (NOACs) Segment is Expected to Hold Significant Market Share in the Anticoagulants Market

Novel Oral Anticoagulants (NOACs) segment holds a significant market share in the anticoagulants market and is anticipated to show a similar trend over the forecast period owing to the growing adoption of the novel oral anticoagulants (NOACs) in developing countries and the high preference of NOACs over the warfarin.

Novel oral anticoagulants (NOACs) are a new class of anticoagulant drugs. Moreover, these are safe (lower incidence of major bleeding), convenient to use, have no interactions with food, and have a shorter half-life. Some of the NOACs include dabigatran, rivaroxaban, apixaban, and edoxaban. These can be used in the prevention and treatment of atrial fibrillation/myocardial infarction, deep vein thrombosis (DVT), and pulmonary embolism.

According to the Centers for Disease Control and Prevention (CDC) update in June 2022, each year in United States, approximately 900,000 people ((1 to 2 per 1,000 population) could be affected by deep vein thrombosis. Moreover, about 60,000-100,000 Americans die of deep vein thrombosis. Thus, the increasing incidences of cardiovascular disorders, venous thromboembolism (VTE), and technological advancements in the development of novel products are the key driving factors in the novel oral anticoagulants (NOACs) segment.

Additionally, product launches and product approval anticipated market growth over the forecast period. For instance, in June 2021, United States Food and Drug Administration (FDA) approved Pradaxa (dabigatran etexilate) oral pellets to treat children 3 months to less than 12 years old with venous thromboembolism (a condition where blood clots form in the veins) directly after they have been treated with a blood thinner given by injection for at least five days. The FDA also approved Pradaxa oral pellets to prevent recurrent clots among patients 3 months to less than 12 years old who completed treatment for their first venous thromboembolism.

Thus, owing to the abovementioned factors, the market segment is expected to show growth over the forecast period.

North America Holds the Major Share in the Market Over the Forecast Period

North America is expected to hold a major market share in the global anticoagulants market due to the high demand for innovative products, and the increasing prevalence of cardiovascular disorders in this region. For Instance, According to the American Heart Association Research in October 2021, approximately 2,300 Americans die due to cardiovascular diseases each day, an average of one death every 38 seconds.

In addition, according to the Center for Disease Control and Prevention in February 2022, about 659,000 Americans die of heart disease annually. This represents almost 25% of all United States deaths. Thus increase in cardiovascular diseases the demand for anticoagulants increases in the region thereby boosting the market.

Furthermore, the presence of top pharma and biotech companies that are involved in the development of therapeutics and the presence of well-established healthcare infrastructure is also fueling the growth of the overall regional market to a large extent. For instance, in December 2021, The Janssen Pharmaceutical Companies of Johnson & Johnson received Food and Drug Administration approval for two pediatric indications for XARELTO (rivaroxaban): treatment of venous thromboembolism (VTE) and reduction in the risk of recurrent VTE in patients aged birth to less than 18 years after at least five days of initial parenteral (injected or intravenous) anticoagulant treatment; and thromboprophylaxis (blood clot prevention).

Thus all aforementioned factors such as increasing chronic diseases and product launches by key market players boost the market for anticoagulants in North America.

Competitive Landscape

The Anticoagulants Market is fragmented competitive and consists of several major players. Some of the major players operating in the market include Johnson & Johnson, Bayer AG, Boehringer Ingelheim GmbH, Bristol-Myers Squibb Company, Daiichi Sankyo Company, GlaxoSmithKline Plc, Aspen Holdings, Sanofi, Pfizer, Inc and Portola Pharmaceuticals, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Cases of Chronic Diseases

- 4.2.2 Technological Advancements in Development of Anticoagulant Products

- 4.2.3 Growing Adoption of Novel Oral Anticoagulants (NOACs)

- 4.3 Market Restraints

- 4.3.1 Stringent Government Regulations

- 4.3.2 Side Effects Associated with Treatment

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Drug Class

- 5.1.1 Novel Oral Anticoagulants (NOACs)

- 5.1.2 Heparin and Low Molecular Weight Heparin (LMWH)

- 5.1.3 Vitamin K Antagonist

- 5.2 By Application

- 5.2.1 Atrial Fibrillation/Myocardial Infarction (Heart Attack)

- 5.2.2 Deep Vein Thrombosis (DVT)

- 5.2.3 Pulmonary Embolism

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle-East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle-East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Johnson & Johnson

- 6.1.2 Bayer AG

- 6.1.3 Boehringer Ingelheim GmbH

- 6.1.4 Bristol-Myers Squibb Company

- 6.1.5 Daiichi Sankyo Company

- 6.1.6 Abbott Laboratories

- 6.1.7 Aspen Holdings

- 6.1.8 Sanofi

- 6.1.9 Pfizer, Inc

- 6.1.10 Alexion Pharmaceuticals Inc.

- 6.1.11 Leo Pharma AS

- 6.1.12 Dr. Reddy's Laboratories