|

市場調査レポート

商品コード

1406243

軍用地上車両アクチュエータ:市場シェア分析、産業動向と統計、2024~2029年の成長予測Military Ground Vehicle Actuators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 軍用地上車両アクチュエータ:市場シェア分析、産業動向と統計、2024~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 78 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

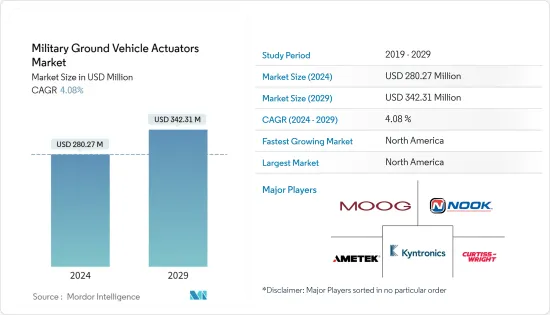

軍用地上車両アクチュエータ市場規模は、2024年に2億8,027万米ドルと推定され、2029年には3億4,231万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは4.08%で成長すると予測されます。

主なハイライト

- 米国、中国、インド、ロシアなどの国々による、テロや国境紛争などの増加による軍事費の増加は、高度な自動化機能を備えた軍用地上車両への投資を促進しています。この要因は、軍用地上車両のアクチュエータ市場の成長を大きく後押ししています。武器システムや保護システムなどを搭載した装甲車の使用が増加していることが、軍用地上車両用アクチュエータの市場成長を促進しています。

- 装甲車の軽量化が重視されるようになり、ドアの作動、窓の作動、座席の調節、ブレーキやスロットルの制御などにリニアアクチュエータや電気機械アクチュエータが使用されるようになっています。さらに、自動化が進み、自律自走式防衛車両技術の大規模な登場が予想されることも、軍用車両アクチュエータの使用を大幅に押し上げると予測されます。

- 北米や欧州などの地域では、自律戦車などの自律型地上兵器車両の研究開発に投資しています。このような進歩の重視は、軍用車両アクチュエータの使用の増加と一致しており、自律システムの効率性と人命救助能力が、将来的に高度なアクチュエータの使用によって推進されることを示唆しています。

軍用地上車両のアクチュエータ市場動向

予測期間中に最も高い成長率を示すのは電動アクチュエータ

- 軍用車両における電動化と自律化の動向の高まりが、電動アクチュエータの市場成長を後押しします。陸上車両の保有台数が増加し、アップグレードやレトロフィット活動が活発化すると、それに伴って電動アクチュエータの需要も増加します。防衛産業では、電動アクチュエータは地上戦闘車両、特に主戦闘戦車、砲兵砲敷設システム、砲・砲塔駆動アクチュエータ、トラバースアクチュエータで用途が拡大しています。

- 米国陸軍は2022年12月、EVメーカーのCanooが製造した全電気式小型軍用戦術車両であるCanoo LTV(Light Tactical Vehicle)を、分析と実証のために受領しました。全電動モーターと軽量ケブラーボディパネルを装備したLTVは、軍事用途における電動アクチュエーターの可能性を実証しています。

- 電動アクチュエータは、エネルギーロスを最小限に抑えるなどの利点があり、空気圧や油圧アクチュエータと併用することで、高い電気機械出力と堅牢な性能を発揮し、効率を高めることができます。特に、50,000N以上の負荷で動作可能な電動リニアアクチュエータは、モーションコントロール、ユーティリティ作動、サスペンション、オートヒッチ機能など、軍用車両で多様な機能を果たします。

- 自律性への注目が高まる中、圧電アクチュエータは軍用車両に搭載されるコンピュータやデバイスの作動用の先進デバイスとして台頭してきました。圧電アクチュエータはメンテナンスが容易で、組み立てコストが低く、熱安定性が高いです。さらに、高度な軽量砲システムを搭載した現代の戦闘車両は、リンクレス弾薬供給、スピード発射機構などに電気システムを利用しています。

- 電気機械アクチュエータの設計における絶え間ない技術革新は、装甲車両システムの生存性を高める。単一のデバイスで回転と直線の両方の作動を可能にする多機能性などの技術の進歩は、コスト効率、システムの重量とサイズの削減に貢献します。これらの要因が総合的に軍用地上車両アクチュエータ市場の成長を後押ししています。

予測期間中に最も高い成長率を示すのは北米

- 北米は、世界最大の軍事予算を誇る米国などの国々で構成されています。この予算の大部分は、高度に先進的で自律的な地上車両システムの開発に割り当てられています。モノのインターネット(IoT)、人工知能(AI)、ロボット工学などの技術進歩が、この地域におけるインテリジェント地上車両システムの拡大を促進しています。

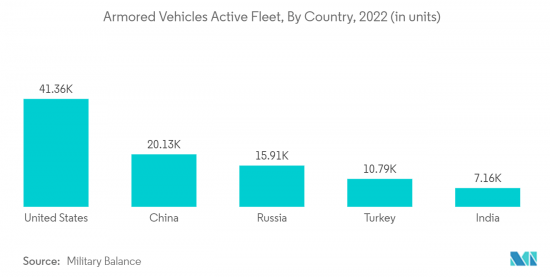

- 現在、米国はさまざまな自律走行車システム技術の開発に積極的に取り組んでいます。米国陸軍は、主力戦車、装甲兵員輸送車、歩兵戦闘車、工兵支援車、地雷防護車、原動機車およびトラック、機動砲兵、軽戦術車、軽用途車など、多様な装甲車両を保有しています。これらの車両の大きさや重量はさまざまで、70トンを超えるエイブラムス主力戦車から、重量約1トンの特殊部隊用軽量戦術全地形対応車両まです。

- さらに陸軍は、ダンプトラックやピックアップのような市販の車両を改造して運用しています。例えば、2023年6月、米国陸軍は機械化歩兵戦闘車両の新しいプロトタイプを開発する契約を発注しました。この契約では、ゼネラル・ダイナミクス・ランド・システムズ社とアメリカン・ラインメタル・ビークルズ社が、M2ブラッドレー歩兵戦闘車の後継となる車両のプロトタイプを作成します。この代替車両は、分隊の監視、保護、輸送、小火器火力を提供します。これらの契約の合計額は約16億米ドルです。

- さらに、オプション有人戦闘車(OMFV)プログラムは、米国陸軍の近代化戦略の極めて重要な要素です。次世代戦闘車両プログラムは、陸軍内で使用されるさまざまな車両や兵器プラットフォームのアップグレードを目指しています。米国陸軍は2022年7月、ミシガン州にあるリカルドの防衛事業部門と、アンチロック・ブレーキ・システム/電子安定制御(ABS/ESC)後付けキットを追加納入する1,890万米ドル超の契約を締結しました。これらのキットは、米国陸軍の高機動多目的車(HMMWV)の操作の安全性を高めることを目的としています。これらの要因や事例が、軍用地上車両アクチュエータ市場の成長を後押ししています。

軍用地上車両アクチュエータ産業の概要

軍用地上車両アクチュエータ市場は、Moog Inc.、Nook Industries Inc.、Curtiss-Wright Corporation、AMETEK Inc.、Kyntronicsが市場シェアの大半を占めています。同市場は、陸上自律戦闘車技術への投資の増加により、大きな需要を目の当たりにしています。プレイヤーは、より高い効率と軽量で堅牢なモーションコントロール要件に対する需要の高まりに大きな機会を見込んでいます。市場プレイヤーの収益創出は、設計と性能の革新、製品の費用対効果、主要な陸上戦闘システムメーカーとの提携に依存します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ

- リニア

- ロータリー

- システム

- 機械式

- 油圧式

- 電気式

- 空気圧

- 地域

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- その他の欧州

- アジア太平洋

- インド

- 中国

- 日本

- 韓国

- その他のアジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他のラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- イスラエル

- その他の中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Moog Inc.

- Curtiss-Wright Corporation

- Thomson Industries, Inc.

- CRD Devices

- Piedrafita Systems

- Semcon

- Kyntronics

- Nook Industries, Inc.

- AMETEK Inc.

- Ultra Motion

第7章 市場機会と今後の動向

The Military Ground Vehicle Actuators Market size is estimated at USD 280.27 million in 2024, and is expected to reach USD 342.31 million by 2029, growing at a CAGR of 4.08% during the forecast period (2024-2029).

Key Highlights

- The rise in military spending by nations such as the United States, China, India, Russia, etc., due to growth in terrorism, border conflicts, etc., is propelling investments in military ground vehicles with advanced automated functions. This factor significantly drives the market growth for military ground vehicle actuators. The increasing use of armored vehicles with mounted weapon systems, protection systems, etc., is driving the market growth for military ground vehicle actuators.

- The growing emphasis on reducing the weight of armored vehicles is propelling the use of linear and electromechanical actuators for door actuation, window actuation, seat adjustment, brake and throttle control, etc. Moreover, the rise in automation and the expected large-scale arrival of autonomous self-driven defense vehicle technology is also projected to significantly boost the use of actuators in military vehicles.

- Geographies such as North America and Europe are investing in research and development of autonomous ground weapon vehicles such as autonomous tanks. This emphasis on advancement aligns with the increasing use of actuators in military vehicles, suggesting that the efficiency and life-saving abilities of autonomous systems will be propelled by the use of advanced actuators in the future.

Military Ground Vehicle Actuators Market Trends

Electrical Actuators To Exhibit The Highest Growth Rate During the Forecast Period

- The increasing trend toward electrification and autonomy in military vehicles drives the market growth for electric actuators. As the fleet size of land vehicles grows and upgrade and retrofit activities increase, the demand for electric actuators rises accordingly. In the defense industry, electric actuators find increasing usage in ground combat vehicles, particularly in main battle tanks, artillery gun-laying systems, gun and turret drive actuators, and traverse actuators.

- In December 2022, the US Army received the Canoo LTV (Light Tactical Vehicle), an all-electric light-duty military tactical vehicle manufactured by EV-maker Canoo, for analysis and demonstration. Equipped with an all-electric motor and lightweight Kevlar body paneling, the LTV demonstrates the potential of electric actuators in military applications.

- Electric actuators offer advantages such as minimized energy loss, and when used alongside pneumatic and hydraulic actuators, they deliver high electromechanical power and robust performance with increased efficiency. Specifically, electrical linear actuators, capable of operating under loads of 50,000N and above, serve diverse functions in military vehicles, including motion control, utility actuation, suspension, and auto hitch functionalities.

- With a heightened focus on autonomy, piezoelectric actuators have emerged as advanced devices for actuation in computers and devices installed in military vehicles. They offer easy maintenance, low assembly costs, and high thermal stability. Furthermore, modern combat vehicles equipped with advanced lightweight gun systems utilize electrical systems for linkless ammunition feeding, speed firing mechanisms, and more.

- Continual innovation in the design of electromechanical actuators enhances the survivability of armored vehicle systems. Technological advancements, such as multi-functionality that enables both rotary and linear actuation from a single device contribute to cost efficiency, reduction in system weight, and size. These factors collectively drive the market growth of electric actuators for military ground vehicles.

North America To Exhibit The Highest Growth Rate During The Forecast Period

- North America comprises countries such as the US, which boasts the world's largest military budget. A significant portion of this budget is allocated to the development of highly advanced and autonomous ground vehicle systems. Technological advancements in the Internet of Things (IoT), artificial intelligence (AI), robotics, and others are driving the expansion of intelligent ground vehicle systems in the region.

- Currently, the United States is actively engaged in the development of various autonomous vehicle system technologies. The US Army maintains a diverse array of armored vehicles, including main battle tanks, armored personnel carriers, infantry fighting vehicles, engineering support vehicles, mine-protected vehicles, prime movers and trucks, mobile artillery, light tactical vehicles, and light utility vehicles. These vehicles vary in size and weight, ranging from the 70-plus ton Abrams main battle tank to the Special Forces' Lightweight Tactical All-Terrain Vehicle, which weighs approximately one ton.

- Additionally, the Army operates modified commercially available vehicles like dump trucks and pickups. For example, in June 2023, the US Army awarded a contract to develop a new prototype for a mechanized infantry combat vehicle. Under this contract, General Dynamics Land Systems Inc. and American Rheinmetall Vehicles LLC will create prototypes of a vehicle intended to replace the M2 Bradley Infantry Fighting Vehicle. The replacement vehicle will offer surveillance, protection, transportation, and small-arms firepower for squad elements. The combined value of these contracts is approximately USD 1.6 billion.

- Moreover, the Optionally Manned Fighting Vehicle (OMFV) program is a pivotal component of the US Army's modernization strategy. The Next Generation Combat Vehicle program seeks to upgrade various vehicles and weapons platforms used within the Army. In July 2022, the US Army signed a contract valued at over USD 18.9 million with Ricardo's Defense business unit, situated in Michigan, to deliver additional antilock brake system/electronic stability control (ABS/ESC) retrofit kits. These kits aim to enhance the safety of operation for the US Army's high mobility multipurpose wheeled vehicle (HMMWV). Collectively, these factors and instances are driving the market growth for military ground vehicle actuators.

Military Ground Vehicle Actuators Industry Overview

The military ground vehicle actuators market is consolidated with Moog Inc., Nook Industries Inc., Curtiss-Wright Corporation, AMETEK Inc., and Kyntronics, accounting for a majority of the market share. The market is witnessing a heavy demand due to increased investments in land-based autonomous combat vehicle technology. Players are witnessing huge opportunities in the growing demand for robust motion control requirements with higher efficiency and lightweight. The revenue generation of market players depends upon innovations in design and performance, the cost-effectiveness of products, and partnerships with major land-based combat system manufacturers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Linear

- 5.1.2 Rotary

- 5.2 System

- 5.2.1 Mechanical

- 5.2.2 Hydraulic

- 5.2.3 Electrical

- 5.2.4 Pneumatic

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Israel

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Moog Inc.

- 6.2.2 Curtiss-Wright Corporation

- 6.2.3 Thomson Industries, Inc.

- 6.2.4 CRD Devices

- 6.2.5 Piedrafita Systems

- 6.2.6 Semcon

- 6.2.7 Kyntronics

- 6.2.8 Nook Industries, Inc.

- 6.2.9 AMETEK Inc.

- 6.2.10 Ultra Motion