|

市場調査レポート

商品コード

1406100

自動車用外観化学品 - 市場シェア分析、産業動向・統計、2024年~2029年成長予測Automotive Appearance Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 自動車用外観化学品 - 市場シェア分析、産業動向・統計、2024年~2029年成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

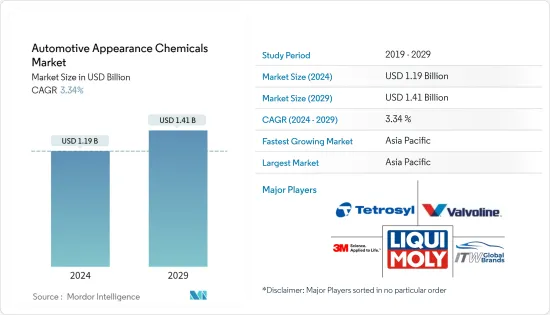

自動車用外観化学品市場規模は2024年に11億9,000万米ドルと推定・予測され、2029年には14億1,000万米ドルに達し、予測期間(2024年~2029年)のCAGRは3.34%で成長すると予測されます。

COVID-19の流行は、世界の自動車用外観化学品市場に影響を与えました。この期間に世界の自動車生産が減速したため、2020年の市場成長はわずかなものにとどまった。しかし、市場はパンデミックから回復し、大きく成長しています。

主なハイライト

- 短期的には、電気自動車(EV)の生産台数の増加と自動車のメンテナンスに対する消費者の意識が、調査対象市場の成長を促す主な要因となっています。

- しかし、ワックスやコーティング剤などの石油製品に対する政府の厳しい規制は、調査対象市場の成長を抑制する可能性が高いです。

- とはいえ、専門的な自動車ケア・サービスや専門的な用途における最新技術の採用が増加していることは、世界市場に有利な成長機会をもたらす可能性が高いです。

- アジア太平洋地域は最大の市場です。また、中国、インド、日本などの国々での消費の増加により、予測期間中に最も急成長する市場になると予想されます。

自動車用外観化学品市場の動向

電気自動車生産の増加

- 自動車用外観化学品市場は、電気自動車(EV)の需要によって成長しています。

- EV市場は、環境意識と将来のエネルギー要件に対処する必要性により、著しい成長を遂げています。持続可能な輸送を実現する必要性は、EVの需要を促進する上で重要な役割を果たしています。

- さらに、電気自動車の生産台数の増加は、調査された市場の需要を高める可能性が高いです。例えば、CleanTechnicaによると、2022年7月の国際プラグイン車登録台数は2021年7月と比較して61%増加し、77万8000台に達しました。

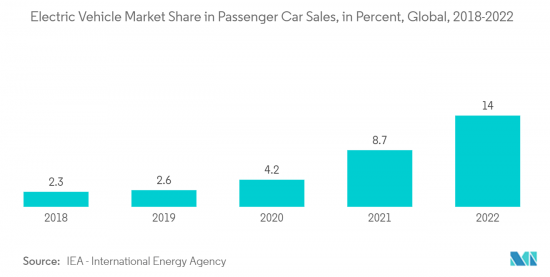

- 国際エネルギー機関(IEA)によれば、2022年の世界の乗用車販売に占める電気自動車の割合は約14%で、前年比5.3%ポイント増です。

- 世界経済フォーラム(WEF)によると、2022年上半期に世界で約430万台のバッテリー式EV(BEV)とプラグインハイブリッド車(PHEV)が新たに販売されました。さらに、BEVの販売台数は年間約75%、PHEVは37%増加しました。さらに、世界の電気自動車販売台数は2022年1~8月に570万台の大台を超え、プラグイン電気自動車の市場シェアは15%近くまで上昇しました。

- 各国政府は、電気自動車の採用や電気自動車製造インフラの拡大に向けて好意的な政策を採用しました。エネルギー・コストの上昇と、新興のエネルギー効率化技術間の競合も、市場の成長を促進すると予想されます。

- 近年、自動車メーカー各社はEVの普及に向けた計画やスケジュールを数多く発表しています。トヨタは、2025年までに売上高の半分を電気自動車で賄う計画です。同社は2021年に中国のバッテリーメーカーBYDと提携し、電気自動車を製造します。フォルクスワーゲンは、2023年までに300億米ドル以上を費やしてEVを開発すると発表しました。また、2030年までに全世界の保有車両の40%をEVにすることを目指しています。

- 現在、電動化については乗用車に注目が集まっているが、この動向はすぐに変わり、他のクラスの自動車にも広がると予想されます。

- 上記のすべての要因によって、予測期間中に自動車用外観化学品の需要が高まると予想されます。

市場を独占するアジア太平洋地域

- 予測期間中、アジア太平洋地域が自動車用外観保護剤の最大市場を占めると予想されます。

- アジア太平洋地域は、世界で最も価値のある自動車メーカーの本拠地です。中国、インド、日本、韓国などの新興諸国は、製造基盤を強化し、効率的なサプライチェーンを構築して収益性を高めるために努力しています。

- 中国汽車工業協会(CAAM)によると、中国は世界最大の自動車生産拠点であり、2022年の自動車総生産台数は2,700万台と、昨年の2,600万台から3.4%増加します。

- SIAM Indiaによると、2022年度のインドにおける自動車総生産台数は約2,290万台で、前年度より増加しています。

- さらに、インドブランド・エクイティ財団(IBEF)によると、電気自動車(EV)市場は2025年までにインドで50,000カロールインドルピー(70億9,000万米ドル)に達すると推定されています。

- 経済産業省(日本);自工会によると、2022年の日本の乗用車生産台数は約657万台で、前年の約662万台から減少しました。また、乗用車にバスやトラックなどを加えた国内総生産台数は約784万台となった。

- 従って、予測期間においては、上記の要因が市場に影響を与える可能性が高いです。

自動車用外観化学品業界の概要

自動車用外観化学品市場は細分化されています。主なプレーヤー(順不同)としては、3M、LIQUI MOLY GmbH、ITW Global Brands、Valvoline、Tetrosyl Ltd.などが挙げられます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 電気自動車(EV)の生産台数の増加

- 自動車メンテナンスに対する消費者の意識の高まり

- その他の促進要因

- 抑制要因

- ワックスやコーティング剤のような石油製品に対する政府の厳しい規制

- その他の阻害要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模)

- 製品タイプ

- ワックス

- ポリッシュ

- 保護剤

- ホイール・タイヤクリーナー

- ウィンドウォッシャー液

- レザーケア製品

- その他

- 用途

- 乗用車

- 小型商用車

- 大型商用車

- その他

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア分析(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- 3M

- SONAX GmbH

- Dow

- General Chemical Corp.

- ITW Global Brands

- Guangzhou Biaobang Car Care Industry Co. Ltd

- LIQUI MOLY GmbH

- Niteo Products, Inc.

- Nuvite Chemical Compounds

- Tetrosyl Ltd

- Turtle Wax, Inc.

- Valvoline Chemicals

第7章 市場機会と今後の動向

- プロフェッショナルオートケアサービスの採用増加

- 特殊用途における最新技術の採用増加

The Automotive Appearance Chemicals Market size is estimated at USD 1.19 billion in 2024, and is expected to reach USD 1.41 billion by 2029, growing at a CAGR of 3.34% during the forecast period (2024-2029).

The COVID-19 pandemic affected the global automotive appearance chemicals market. The slowdown in global automobile production during the period resulted in minimal market growth in 2020. However, the market recovered from the pandemic and is growing significantly.

Key Highlights

- Over the short term, the increase in the production of electric vehicles (EV) and consumer awareness toward vehicle maintenance are major factors driving the growth of the market studied.

- However, stringent government regulations on petroleum products such as waxes and coatings are likely to restrain the growth of the studied market.

- Nevertheless, the increasing adoption of professional auto care services and modern technology in specialized applications will likely create lucrative growth opportunities for the global market.

- The Asia-Pacific region represents the largest market. It is also expected to be the fastest-growing market over the forecast period, owing to the increasing consumption in countries such as China, India, and Japan.

Automotive Appearance Chemicals Market Trends

Increase in the Production of Electric Vehicles

- The automotive appearance chemical market is growing due to the demand for electric vehicles (EVs).

- The EV market witnessed significant growth due to environmental awareness and the need to address future energy requirements. The need to attain sustainable transportation plays a significant role in driving the demand for EVs.

- Furthermore, the rising production of electric vehicles will likely enhance the market demand for the studied market. For instance, according to CleanTechnica, international plug-in vehicle registrations increased by 61% in July 2022 compared to July 2021, reaching 778,000 units.

- As per the International Energy Agency (IEA), in 2022, electric vehicles accounted for around 14% of worldwide passenger car sales, a 5.3% point increase year on year.

- As per the World Economic Forum (WEF), nearly 4.3 million new battery-powered EVs (BEVs) and plug-in hybrid electric vehicles (PHEVs) were sold globally in the first half of 2022. Additionally, BEV sales grew by around 75% yearly and PHEVs by 37%. Moreover, global electric car sales crossed the 5.7 million units mark in the first eight months of 2022, and the market share of plug-in electric cars increased to nearly 15%.

- The governments of various countries adopted favorable policies toward adopting electric vehicles and expanding the manufacturing infrastructure of electric vehicles. Rising energy costs and competition among emerging energy efficiency technologies are also expected to fuel market growth.

- In recent years, automotive manufacturers announced many plans and timelines for bringing more EVs. Toyota plans to generate half of its sales from electrified vehicles by 2025. The company partnered with Chinese battery manufacturer BYD in 2021 to manufacture electric cars. Volkswagen said it will spend more than USD 30 billion developing EVs by 2023. The manufacturer also aims for EVs to make up 40% of its global fleet by 2030.

- Currently, much attention is being given to passenger vehicles for electrification, but this trend is expected to change soon and spread to other classes of vehicles.

- All the factors above are expected to enhance the demand for automotive appearance chemicals during the forecast period.

The Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to account for the largest market for automotive appearance chemicals during the forecast period.

- The Asia-Pacific region is home to some of the world's most valuable vehicle manufacturers. Developing countries such as China, India, Japan, and South Korea are working hard to strengthen the manufacturing base and develop efficient supply chains for greater profitability.

- According to the China Association of Automobile Manufacturers (CAAM), China includes the largest automotive production base in the world, with a total vehicle production of 27 million units in 2022, registering an increase of 3.4 % compared to 26 million units produced last year.

- According to SIAM India, in the financial year 2022, the total production volume of vehicles in India was around 22.9 million units, an increase from the previous year.

- Additionally, according to the Indian Brand Equity Foundation (IBEF), the electric vehicle (EV) market is estimated to reach INR 50,000 crore (USD 7.09 billion) in India by 2025.

- In 2022, according to METI (Japan); JAMA, approximately 6.57 million passenger cars were produced in Japan, down from about 6.62 million units in the previous year. The total domestic production volume reached approximately 7.84 million units, which includes buses and trucks next to passenger cars.

- Therefore, the above factors will likely impact the market in the forecasted period.

Automotive Appearance Chemicals Industry Overview

The automotive appearance market is fragmented in nature. The major players (not in any particular order) include 3M, LIQUI MOLY GmbH, ITW Global Brands, Valvoline, and Tetrosyl Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Drivers

- 4.1.1 Increase in the Production of Electric Vehicles (EV)

- 4.1.2 Increase in Consumer Awareness Toward Vehicle Maintenance

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Government Regulations on Petroleum Products like Waxes and Coatings

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Waxes

- 5.1.2 Polishes

- 5.1.3 Protectants

- 5.1.4 Wheel and Tire Cleaners

- 5.1.5 Windshield Washer Fluids

- 5.1.6 Leather Care Products

- 5.1.7 Others

- 5.2 Application

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Heavy Commercial Vehicles

- 5.2.4 Others

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis (%) **/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 SONAX GmbH

- 6.4.3 Dow

- 6.4.4 General Chemical Corp.

- 6.4.5 ITW Global Brands

- 6.4.6 Guangzhou Biaobang Car Care Industry Co. Ltd

- 6.4.7 LIQUI MOLY GmbH

- 6.4.8 Niteo Products, Inc.

- 6.4.9 Nuvite Chemical Compounds

- 6.4.10 Tetrosyl Ltd

- 6.4.11 Turtle Wax, Inc.

- 6.4.12 Valvoline Chemicals

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Adoption of Professional Auto Care Services

- 7.2 Increasing Adoption of Modern Technology in Specialized Application