|

市場調査レポート

商品コード

1273532

木材用接着剤市場- 成長、動向、予測(2023年-2028年)Wood Adhesives Market - Growth, Trends, and Forecasts (2023 - 2028) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 木材用接着剤市場- 成長、動向、予測(2023年-2028年) |

|

出版日: 2023年04月14日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

木材用接着剤市場は、予測期間中に4%以上のCAGRで推移すると予想されます。

COVID-19は、2020年の市場にマイナスの影響を与えました。しかし、現在は流行前のレベルに達していると推定され、市場は安定的に成長すると予想されます。

主なハイライト

- 建設活動の活発化により、木材用接着剤市場は予測期間中に成長すると予想されます。

- 一方、原材料価格の変動が予測期間中の市場の妨げになると予想されます。

- 環境に優しい接着剤の開拓は、今後数年間、市場に機会をもたらすと期待されています。

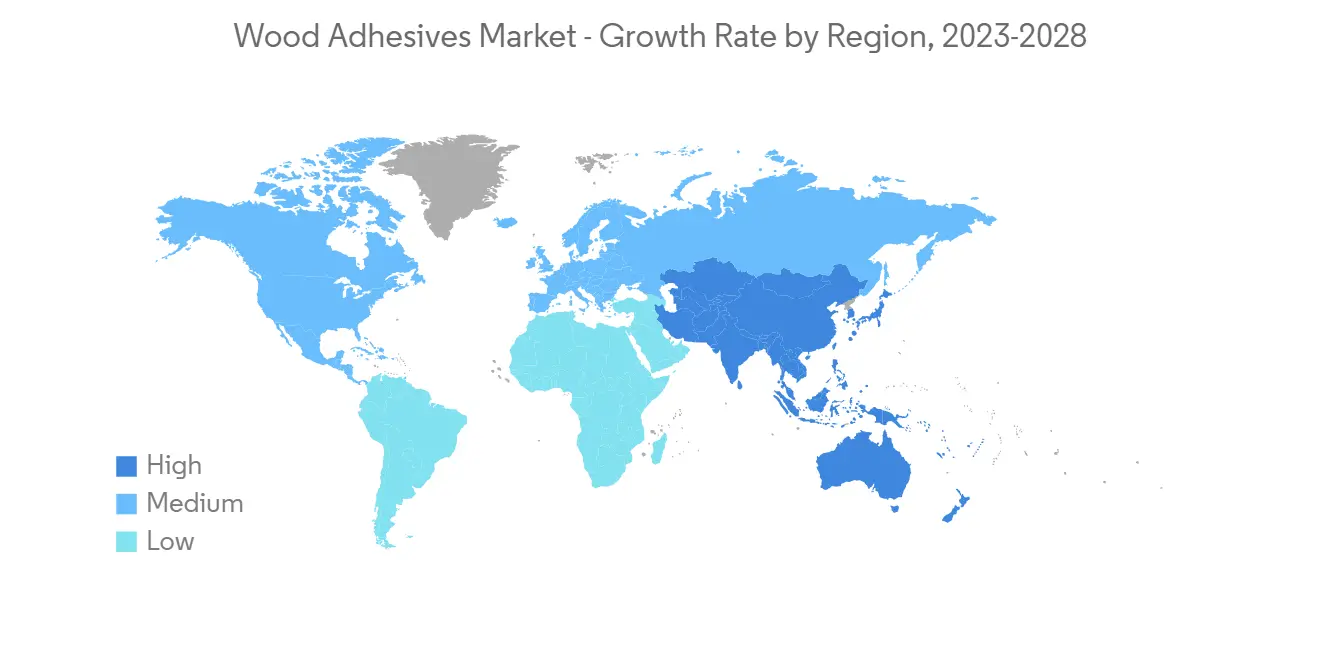

- アジア太平洋は、中国、インド、日本などの国からの消費が最も大きく、世界市場を独占しています。

木材用接着剤市場の動向

建設活動の活発化に伴う需要の増加

- 接着剤は、糊、粘液、ペーストとしても知られ、2つの物品の片面または両面に塗布され、それらを結合し、分離しないようにする非金属物質です。木材用接着剤は、木製の物質を結合するために特別に作られたものです。

- 木工用接着剤は、天然と合成の原料を使用して製造されます。天然接着剤は植物や動物の体から得られるもので、合成接着剤に比べ結合力が弱いです。

- 建設活動の活発化により、木材の用途が増え、木材用接着剤の活躍の場が広がっています。

- 中国の成長は、主に急速な住宅と商業ビルの拡大によって促進されています。世界銀行によると、中国は継続的な都市化プロセスを奨励し、それに耐えており、2030年までに70%の割合になると予測しています。

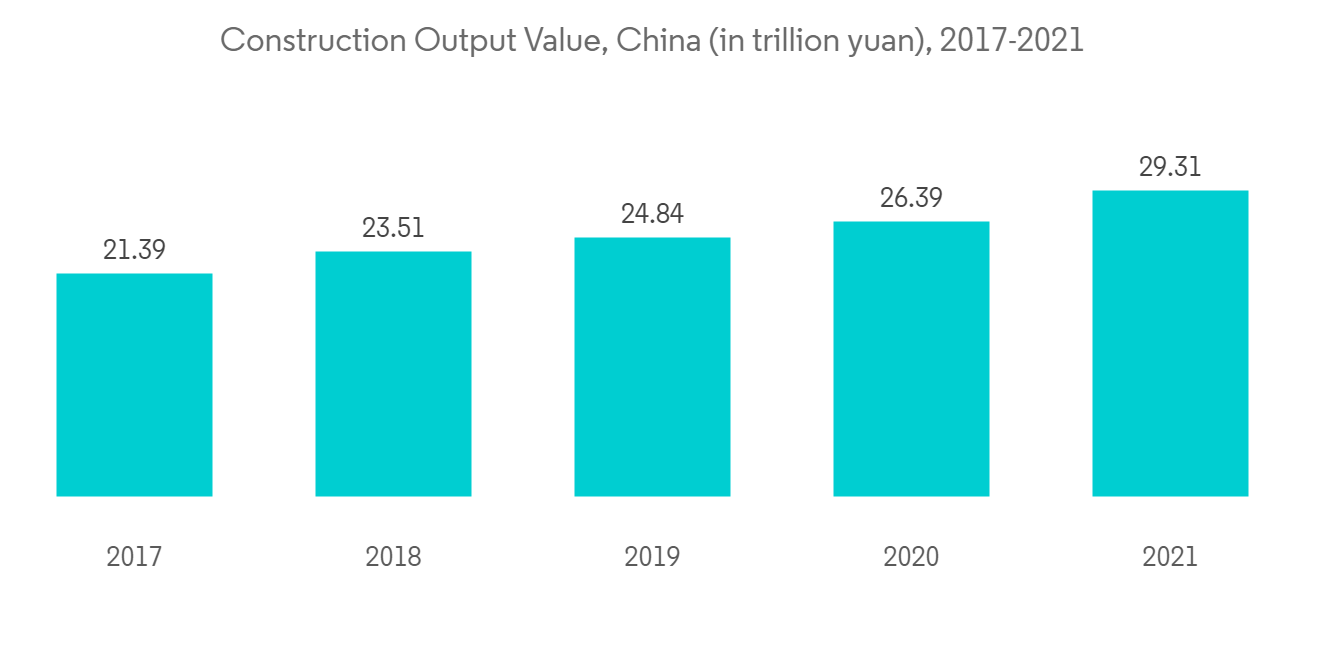

- また、中国国家統計局によると、同国の建設生産高は2021年にピークを迎え、約4兆3,000億米ドルに達しています。その結果、これらの要因によって木材用接着剤の需要が増加する傾向にあります。

- さらに、インドの不動産業界が発表した報告書によると、インドも今後7年間で約1兆3,000億米ドルを住宅に投資するようです。これにより、6,000万戸の住宅が新たに建設されると予想されています。2024年には、手頃な価格の住宅が約70%増加すると思われます。

- このように、世界の建設活動の活発化は、予測期間中、木材用接着剤の市場を牽引すると予想されます。

アジア太平洋地域が市場を独占する

- 予測期間中、アジア太平洋地域が木材用接着剤市場を独占すると予想されます。中国、インド、日本などの国々で建設部門が成長しているため、この地域では木材用接着剤の利用が増加しています。

- 木材用接着剤の最大の生産者はアジア太平洋に存在します。木材用接着剤製造の主要企業には、3M、Sika AG、Henkel AG &Co.KGaA、Pidilite Industries Ltd、Jubilant Industriesです。

- 家具以外にも、木材用接着剤はフローリング&デッキ、合板、キャビネット、パーティクルボード、窓&ドアなどの用途で使用されています。したがって、住宅建設の増加に伴い、市場は大きく成長すると予想されます。

- インドでは、プラダン・マントリ・アワス・ヨジャナ・アーバン(PMAY-U)により、2021年11月まで114.06 lakhの住宅が認可されました。そのうち、89.36 lakhの住宅が建築認可されており、2021年11月までに52.55 lakhが完成しています。

- さらに、中国国家統計局によると、2022年6月の中国における木製家具の小売売上高は23億9,000万米ドルで、期間中(2022年3月~2022年6月)に40%の増加を示しています。

- さらに、都市化、不動産開発の進展、堅調なGDP成長、経済の安定は、この地域における木製家具の成長に寄与する他の主要な要因の一部であり、したがって木材用接着剤の需要を増加させています。

- 上記の要因は、政府の支援と相まって、木材用接着剤の需要増加に寄与しており、予測期間中に成長すると予想されます。

木材用接着剤産業の概要

世界の木材用接着剤市場は、その性質上、部分的に断片化されています。市場の主要企業には、3M、Sika AG、Henkel AG &Co.KGaA、Pidilite Industries Ltd、Jubilant Industries Ltdなどです(順不同)。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 本調査の対象範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 建設ラッシュによる需要拡大

- その他の促進要因

- 抑制要因

- 原材料の価格変動

- その他の制約条件

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の度合い

第5章 市場セグメンテーション

- 樹脂の種類

- 天然

- 合成樹脂

- 技術分野

- 溶剤ベース

- 水性

- その他の技術

- 応用分野

- 家具

- 合板

- キャビネット

- ドア・窓

- その他の用途

- 地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米地域

- 中東・アフリカ地域

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋地域

第6章 競合情勢

- M&A、ジョイントベンチャー、コラボレーション、契約など

- 市場シェア(%)**/ランキング分析

- 主要企業が採用した戦略

- 企業プロファイル

- 3M

- Aica Kogyo Co.Ltd.

- Akzo Nobel N.V.

- Ashland

- Bostik(Arkema Group)

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Jubilant Industries Ltd

- Pidilite Industries Ltd

- Sika AG

第7章 市場機会および将来動向

- 環境に配慮した接着剤の開発

The wood adhesives market is expected to register a CAGR of more than 4% during the forecast period. COVID-19 negatively impacted the market in 2020. However, the market is now estimated to reach pre-pandemic levels and is expected to grow steadily.

Key Highlights

- Due to the increasing construction activity, the wood adhesives market is expected to grow during the forecast period.

- On the other hand, volatility in the price of raw materials is expected to hinder the market during the forecast period.

- Developing eco-friendly adhesives is expected to provide an opportunity for the market in the coming years.

- Asia-Pacific dominated the global market with the most significant consumption from countries such as China, India, and Japan.

Wood Adhesives Market Trends

Growing Demand due to Increasing Construction Activities

- Adhesive, also known as glue, mucilage, or paste, is any non-metallic substance applied to one or both surfaces of two items that bind them together and resists their separation. Wood adhesives are specially made to bind wooden substances.

- Wood adhesives are produced using natural and synthetic sources. Natural glues are obtained from plant or animal bodies with low binding capacity compared to synthetic adhesives.

- The growing construction activity is increasing the wood application, creating the scope for wood adhesives.

- China's growth is fueled mainly by rapid residential and commercial building expansion. According to the world bank, China is encouraging and enduring a continuous urbanization process, with a projected rate of 70% by 2030.

- Also, according to the National Bureau of Statistics of China, the country's construction output peaked in 2021 at about USD 4.3 trillion. As a result, these factors tend to increase the wood adhesive demand.

- Furthermore, according to a report released by the Indian Real Estate Industry, India is also likely to invest around USD 1.3 trillion in housing over the next seven years. It is expected to see the construction of 60 million new homes. Affordable housing availability will likely rise by around 70% in 2024.

- Thus, growing global construction activity is expected to drive the market for wood adhesives over the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to dominate the market for wood adhesives during the forecast period. With the growing construction sector in countries such as China, India, and Japan, the utilization of wood adhesives is increasing in the region.

- The largest producers of wood adhesives are present in Asia-Pacific. Some leading companies in adhesive wood production are 3M, Sika AG, Henkel AG & Co. KGaA, Pidilite Industries Ltd, and Jubilant Industries.

- Apart from furniture, wood adhesives are also used in flooring & decks, plywood, cabinet, particleboard, windows & doors, and other applications. Thus, the market is expected to grow significantly with growing housing construction.

- In India, the Pradhan Mantri Awas Yojana-Urban (PMAY-U) sanctioned 114.06 lakh houses till November 2021. Of them, 89.36 lakh houses are approved for building, with 52.55 lakhs completed by November 2021.

- Furthermore, according to the National Bureau of Statistics of China, in June 2022, the retail sales of wood furniture in China amounted to USD 2.39 billion, which shows an increase of 40% in the period (March 2022 - June 2022).

- Additionally, urbanization, rising real estate development, robust GDP growth, and economic stability are some of the other key factors contributing to the wood furniture growth in the region, thus increasing the wood adhesive demand.

- The factors above, coupled with government support, are contributing to the increasing demand for wood adhesives and are expected to grow during the forecast period.

Wood Adhesives Industry Overview

The global wood adhesives market is partially fragmented in nature. Some of the major players in the market include 3M, Sika AG, Henkel AG & Co. KGaA, Pidilite Industries Ltd, and Jubilant Industries Ltd, among others (in no particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from the Growing Construction Activity

- 4.1.2 Other Drivers

- 4.2 Restraints

- 4.2.1 Volatility in the Price of Raw Materials

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Resin Type

- 5.1.1 Natural

- 5.1.2 Synthetic

- 5.2 Technology

- 5.2.1 Solvent-based

- 5.2.2 Water-based

- 5.2.3 Other Technologies

- 5.3 Application

- 5.3.1 Furniture

- 5.3.2 Plywood

- 5.3.3 Cabinets

- 5.3.4 Doors and Windows

- 5.3.5 Other Applications

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East & Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Aica Kogyo Co.Ltd.

- 6.4.3 Akzo Nobel N.V.

- 6.4.4 Ashland

- 6.4.5 Bostik (Arkema Group)

- 6.4.6 Dow

- 6.4.7 H.B. Fuller Company

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Jubilant Industries Ltd

- 6.4.10 Pidilite Industries Ltd

- 6.4.11 Sika AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Eco-friendly Adhesives