|

市場調査レポート

商品コード

1406152

機関車:市場シェア分析、産業動向・統計、2024~2029年の成長予測Locomotive - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 機関車:市場シェア分析、産業動向・統計、2024~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 70 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

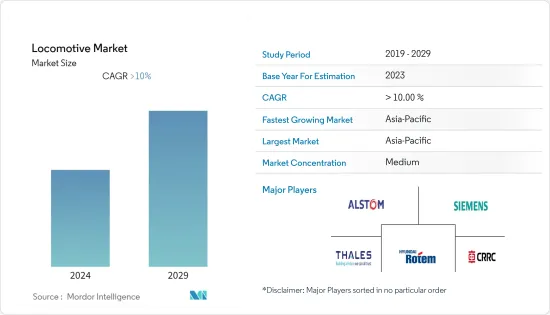

機関車市場の現在の市場規模は242億米ドルであり、今後5年間で435億8,000万米ドルに成長すると予測され、予測期間中の収益ベースのCAGRは10%と予測されています。

長期的には、都市化の進展、環境の持続可能性、広範な鉄道プロジェクト、エネルギー効率の高い車両に対する需要の増加、鉄道網のインフラ拡大などが、機関車市場を牽引する主な要因として作用すると予想されます。世界の鉄道網の拡大は、公共輸送手段としての需要を満たす電気機関車の成長をさらに後押ししています。

さらに、Sicモジュール、IGBTモジュール、補助動力装置の発売などの技術進歩が、機関車用エンジンの需要急増につながっています。この進歩により、排出ガスが削減され、燃費が向上し、総重量が減少しました。また、現在の状態に切り替える際の電力損失も減少しています。

しかし、鉄道車両の資本集約性、高いメンテナンス費用、オーバーホール費用など、特定の阻害要因が機関車市場の成長を妨げています。こうした市場の課題にもかかわらず、世界市場は今後数年で大きく成長すると予想されています。

輸送産業の発展に伴い、移動する貨物量は世界的に拡大しており、アジア太平洋と北米は予測期間中に大きな成長を遂げる可能性があります。

機関車市場の動向

電気機関車プロジェクトの増加が市場の成長を促進

機関車は、列車を牽引するために使用される動力エンジンです。機関車には積載能力があるため、低出力のエンジンとは区別されます。列車を牽引するのに必要な力は通常の車両よりもはるかに大きいため、大規模な投資は必要であり、メリットではないです。

近年、機関車の構造や設計が技術的に進歩したことで、より高い牽引力と低燃費を実現できるようになりました。鉄道部門への大規模な投資は、多くの乗客を運ぶことができる結果となっています。インドのような人口密度の高い国々には大規模な鉄道が敷設されており、この市場で事業を展開する企業にはいくつかの成長機会が生まれると思われます。大規模な企業がいくつか存在することは、市場の成長に有利に働くと思われます。

2023年にはウォークスルー方式のイントロダクションが計画されており、すでに設計寿命40年を超えた旧型車両を置き換える可能性が高いです。これらは、間もなく欧州の鉄道産業と機関車市場を押し上げる要因の一部です。

世界中の都市部で交通渋滞が増加するなか、人工知能や機械学習のような技術の進歩や交通システムとの統合と相まって、より速く、より効率的で、より信頼性の高い交通システムの開発が強く求められています。

同時に鉄道業界は、5G、ビッグデータ、モノのインターネット、自動化、人工知能、ブロックチェーンといった新たなデジタル技術に牽引され、変革の段階にあります。運転手のいない列車は、輸送能力を高め、安全性を向上させ、労働力とメンテナンス要件の削減によるコスト削減を提供できるため、交通当局や鉄道事業者にとって魅力的なソリューションとなっています。多くの地方自治体が、効率性の向上とコスト削減のため、地域全体で自律走行列車を導入しています。

- 2023年2月、デリー・メトロは初めて独自開発した列車制御・監督システム(TCSS)を稼働させました。バーラト・エレクトロニクス社(BEL)と共同で開発されたこのシステムは、列車制御と信号伝達に使われていた既存の技術に代わるものです。独自に開発されたTCSSには、自動列車運転、自動列車保護、遠隔診断などの高度な機能が組み込まれています。この技術的マイルストーンは、最先端の地下鉄鉄道システムを開発するインドの能力を示すものであり、都市交通インフラ分野におけるインドの自立に貢献するものです。

- 2022年11月、オーストラリアのシドニー市内線と南西線に初の無人運転列車が導入されました。アルストムが製造したこの列車は自律的に運行され、乗客の安全性を高め、移動効率を向上させる。この無人運転列車は、快適な通勤体験のための先進技術と広々とした車内を特徴としています。このマイルストーンは、シドニーの鉄道網を近代化し、信頼性と輸送能力を向上させるために自動運転列車を採用するための重要な一歩となります。

以上のような世界各地での開拓は、予測期間中に市場の大きな成長を示すことになりそうです。

アジア太平洋地域が機関車市場をリードする見込み

予測期間中、アジア太平洋地域が最大の市場シェアを占めると予想されます。巨大な輸送産業と、絶えず増加する鉄道旅客と鉄道旅行が、この地域市場で事業を展開する企業にいくつかの機会を生み出すと思われます。

加えて、鉄道は中国、インド、日本といったアジアの主要経済圏の利用者の間で最も好まれている交通手段です。機関車市場の主要メーカーがこの地域に本社を置いていることもあり、この3カ国は年間旅客キロ数でもトップです。

インドでは公共交通機関として地下鉄の人気が高まっており、市場も大きく成長しています。このため、鉄道網はアジア太平洋諸国の経済発展に非常に重要な役割を果たしています。例えば

- 2022年2月、杭州の地下鉄は2本の新線と1本の延伸線を開通させ、ネットワークに59路線km以上を追加しました。インドでは、大都市における通勤輸送の需要が大きいため、2023年までに地下鉄車両の設置ベースが5,458両に増加すると予想されています。2018年から2023年までの5年間で、合計3,343両が地下鉄鉄道網に追加される予定です。

日本は自律走行列車を採用している著名な国のひとつです。日本は2022年にE7系新幹線の試験を開始し、このような無人運転列車の早期運行に注力しています。JR東日本は、このような列車が人間の労力を減らし、時間とコストを節約し、安全性を向上させると期待しています。これらは、アジア太平洋の自律走行列車市場における自律走行列車の需要を押し上げる要因の一部です。

アジア太平洋地域は、シンガポール、マレーシア、インドネシア、バングラデシュなど、先進経済諸国と発展途上国諸国によって特徴づけられています。都市旅客輸送のための新たな鉄道プロジェクトや、既存車両の更新・保守が、これらの国々の市場を牽引すると期待されています。

マレーシアのハイテク産業・政府グループ(MIGHT)はボンバルディア・トランスポーテーションと覚書を締結し、今後数年間にわたり自国の鉄道産業の専門知識を発展させるための協力関係を概説しました。

マレーシア政府は、クアラルンプールの地下鉄LRT3号線向けに、シーメンス中国、CRRC株洲、マレーシアのパートナーであるTegap Dinamikのコンソーシアムに252台の無人運転車両を発注しました。政府はまた、クアラルンプールのケラナジャヤ線に使用される可能性の高いInnovia Metro 300車両108両をHartasumaとBombardierのコンソーシアムに発注しました。

以上のような要因から、この地域における機関車の配備は、予測期間中に大きな成長が見込まれます。

機関車産業の概要

機関車市場は、CRRC、Alstom SA、Siemens AG、Hyundai Rotemなどの主要企業によって支配されています。各社は、市場参入企業の買収、市場参入企業との戦略的提携、新型・先進機関車の発売などにより、存在感を高めています。例えば

2022年12月、インド鉄道省は国家鉄道計画を発表し、2030年末までに鉄道貨物輸送のシェアを27%増の45%にすると発表しました。さらに、主要な高密度路線に貨物専用通路(DFC)を開拓することは、インド鉄道の市場シェアの低下傾向に歯止めをかけるための重要な政策であり、鉄道輸送に有利なバランスに傾くと思われます。さらに、汎用貨車、特殊・大容量貨車、自動車運搬用貨車などへの民間投資を奨励するため、数多くのプログラムも開発されています。

2022年11月、アルストムはオランダのインフラ管理会社ProRailandとベルギーの鉄道貨物事業者リネアスと共同で、オランダのブレダで分列機関車の最大自動化レベルを展示しました。GoA4として知られるこの自動化レベルは、完全に自動化された始動、運転、停止、予期せぬ障害物や事故への対処を伴うもので、分列作業中に列車内の職員が直接関与することはないです。

2022年10月、シーメンス・モビリティは、コンソーシアム・パートナーのSTエンジニアリングおよびシュタートラーと共同で、高雄地下鉄のイエローラインを納入するターンキー契約を獲得しました。シーメンス・モビリティはGoA4の機能を最先端のCBTC信号システムに統合し、完全自動運転(ATO)を実現します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 世界の鉄道輸送の増加

- 市場抑制要因

- 高い資本コストとサービスコスト

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模)

- 推進力タイプ別

- ディーゼル

- 電気式

- 技術別

- IGBTモジュール

- GTOサイリスタ

- SiCモジュール

- 部品タイプ別

- 整流器

- インバーター

- トラクション・モーター

- オルタネーター

- 地域別

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他の欧州

- アジア太平洋

- インド

- 中国

- 日本

- 韓国

- その他のアジア太平洋地域

- 世界のその他の地域

- 南米

- 中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- CRRC Corporation Limited

- Alstom SA

- Turbo Power Systems

- Siemens AG

- Kawasaki Heavy Industries Ltd.

- CJSC Transmashholding

- Stadler Rail

- Toshiba Corporation

- Hyundai Rotem

- Mitsubishi Heavy Industries, Ltd.

- Thales Group

第7章 市場機会と今後の動向

The Locomotive Market was valued at USD 24.2 billion in the current year and is projected to grow to USD 43.58 billion by the next five years, registering a CAGR of 10% in terms of revenue during the forecast period.

Over the long term, an increase in urbanization, environmental sustainability, a broad spectrum of impending rail projects, growth in demand for energy-efficient rolling stock, and an expanding infrastructure of rail networks are expected to act as major factors driving the locomotives market. The extensive rail networks globally further support the growth of electric locomotives to meet the demand as a means of public transport.

In addition, technological progress, such as the launch of the Sic module, IGBT module, and auxiliary power units, has resulted in a surging demand for locomotive engines. This progress has reduced emissions, escalated fuel efficiency, and lowered overall weight. It has also reduced power loss when switching to the current state.

However, certain restraining factors are impeding the growth of the locomotives market, which include the capital intensiveness of rolling stock, high maintenance costs, and overhaul costs. Despite these market challenges, the global market is expected to grow significantly in the coming years.

With the developing transportation industry, the volume of cargo to be moved is expanding globally, while Asia-Pacific and North America may witness significant growth during the forecast period.

Locomotive Market Trends

Increasing Number of Electric Locomotive Projects to Fuel Growth of the Market

Locomotives are powered engines that are used to pull trains. The ability of a locomotive to carry a payload separates it from low-power engines. The force required to pull trains is much higher than normal vehicles; thus, large-scale investments are a necessity and not a benefit.

The recent technological advances in design, as well as structures of locomotives, have allowed applications with higher pulling capacities and lower fuel consumption. The massive investment in the railway sector is consequential to the many passengers it can carry. The extensive railways in densely populated countries such as India will create several growth opportunities for the companies operating in the market. The presence of several large-scale companies will emerge in favor of market growth.

The Inspiron walkthrough-style trains are planned for introduction in 2023, and they are likely to replace the old trains, which have already surpassed the 40-year design life. These are some of the factors that will soon boost the railway industry and the locomotive market in Europe.

With the increase in traffic congestion across urban centers around the globe, there is a strong need to develop faster, more efficient, and more reliable transportation systems coupled with the advancement in technology and its integration with transportation systems like artificial intelligence and machine learning.

At the same time, the railway industry is in the transformation stage, led by emerging digital technologies like 5G, big data, the Internet of Things, automation, artificial intelligence, and blockchain. Driverless trains can enhance capacity, improve safety, and offer cost savings through reduced labor and maintenance requirements, making them an attractive solution for transportation authorities and rail operators. Many regional governments are deploying autonomous trains across the region to increase efficiency and reduce costs. For instance,

- In February 2023, Delhi Metro launched its first-ever indigenously developed Train Control and Supervision System (TCSS). The system, developed in collaboration with Bharat Electronics Limited (BEL), replaces the existing technology used for train control and signaling. The indigenously developed TCSS incorporates advanced features like automatic train operation, automatic train protection, and remote diagnostics. This technological milestone showcases India's capability to develop state-of-the-art metro rail systems and contributes to the country's efforts in self-reliance in the field of urban transportation infrastructure.

- In November 2022, The first driverless trains were introduced on the Sydney City and Southwest Line in Australia. The trains, manufactured by Alstom, will operate autonomously, enhancing passenger safety and improving travel efficiency. The driverless trains feature advanced technologies and spacious interiors for a comfortable commuting experience. This milestone marks a significant step towards modernizing Sydney's rail network and adopting automated train operations for increased reliability and capacity.

The above-mentioned development across the globe is likely to witness major growth for the market during the forecast period.

Asia-Pacific Region is Expected to Lead the Locomotive Market

The Asia-Pacific region is anticipated to hold the largest market share during the forecast period. The massive transport industry and the constantly rising railway passengers and train travel are likely to create several opportunities for companies operating in the regional market.

In addition, the railway is the most preferred means of transport among the passengers of the major Asian economies such as China, India, and Japan. These three countries are also topping the list of passenger kilometers per year, as major manufacturers of the locomotive market are headquartered in this region.

The growing popularity of metro travel as public transportation in India is also witnessing major growth in the market. Due to this, the railway network plays a very significant role in the economic development of countries in Asia-Pacific. For instance,

- In February 2022, the Hangzhou metro opened two new lines and an extension, adding more than 59 route km to the network. The installed base of metro-rail rolling stock in India is expected to increase to 5,458 railcars by 2023, owing to the huge demand for commuter transportation in metropolitan cities. A total of 3,343 railcars are planned to be added to the metro-rail network over five years, from 2018 to 2023.

Japan is one of the prominent countries using autonomous trains. Japan started testing its E7 series Shinkansen bullet trains in 2022 with a focus on operating such driverless trains soon. The East Japan Railway Co. expects that such trains will reduce human efforts, offer time and cost savings, and improve safety. These are some of the factors that are going to boost the demand for autonomous trains in the Asia-Pacific autonomous train market.

Asia-Pacific is also characterized by developed and developing economies, such as Singapore, Malaysia, Indonesia, and Bangladesh. New rail projects for urban passenger transportation and the replacement and maintenance of the existing fleet are expected to drive the market in these countries.

The Malaysian Industry-Government Group for High Technology (MIGHT) signed a memorandum of understanding with Bombardier Transportation, outlining their collaboration on developing home-grown rail industry expertise over the coming years.

The Malaysian government ordered 252 driverless vehicles for the Kuala Lumpur metro Line LRT3 from a consortium of Siemens China, CRRC Zhuzhou, and a Malaysian partner, Tegap Dinamik. The government also ordered 108 Innovia Metro 300 vehicles from a consortium of Hartasuma and Bombardier that are likely to be used for Kuala Lumpur's Kelana Jaya Line.

Owing to the above factors, the deployment of locomotives in the region is expected to observe significant growth during the forecast period.

Locomotive Industry Overview

The locomotive market is dominated by several key players such as CRRC, Alstom SA, Siemens AG, Hyundai Rotem, and others. The companies are expanding their presence by acquiring other market participants, forming strategic alliances with other players in the market, and launching new and advanced locomotives. For instance,

In December 2022, the Ministry of Railway, India, published a National Rail Plan and announced to increase the share of rail freight traffic by 27% to 45% by the end of 2030. Further, the development of Dedicated Freight Corridors (DFCs) on key high-density routes is a crucial policy move by Indian Railways to halt the downward trend in the market share of the country's railways and would also tip the balance in favor of rail transportation. Additionally, to encourage private investment in general-purpose wagons, special-purpose/high-capacity wagons, automobile carrier wagons, etc., numerous programs have also been developed.

In November 2022, Alstom, in collaboration with Dutch infrastructure management ProRailand Belgian rail freight operator Lineas, exhibited the maximum level of automation on a shunting locomotive in Breda, the Netherlands. This level of automation, known as GoA4, entails completely automated starting, driving, halting, and dealing with unexpected obstructions or incidents without the direct involvement of any on-train personnel during shunting tasks.

In October 2022, Siemens Mobility, in collaboration with consortium partners ST Engineering and Stadler, was granted a turnkey contract to deliver the Yellow Line for the Kaohsiung Metro. Siemens Mobility will integrate GoA4 capabilities into its cutting-edge CBTC signaling system, enabling fully automated train operations (ATO).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Rise in Rail Transporation Across the Globe

- 4.2 Market Restraints

- 4.2.1 High Capital and Service Cost

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value (USD))

- 5.1 By Propulsion Type

- 5.1.1 Diesel

- 5.1.2 Electric

- 5.2 By Technology

- 5.2.1 IGBT Module

- 5.2.2 GTO Thyristor

- 5.2.3 SiC Module

- 5.3 By Component Type

- 5.3.1 Rectifier

- 5.3.2 Inverter

- 5.3.3 Traction Motor

- 5.3.4 Alternator

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.4.1 South America

- 5.4.4.2 Middle-East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 CRRC Corporation Limited

- 6.2.2 Alstom SA

- 6.2.3 Turbo Power Systems

- 6.2.4 Siemens AG

- 6.2.5 Kawasaki Heavy Industries Ltd.

- 6.2.6 CJSC Transmashholding

- 6.2.7 Stadler Rail

- 6.2.8 Toshiba Corporation

- 6.2.9 Hyundai Rotem

- 6.2.10 Mitsubishi Heavy Industries, Ltd.

- 6.2.11 Thales Group