|

市場調査レポート

商品コード

1404420

自動車用ウルトラキャパシタ-市場シェア分析、産業動向・統計、2024~2029年成長予測Automotive Ultra-capacitor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 自動車用ウルトラキャパシタ-市場シェア分析、産業動向・統計、2024~2029年成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

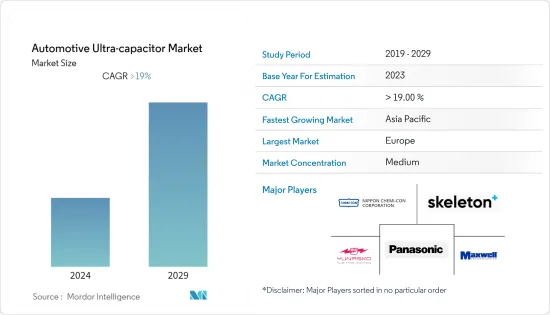

自動車用ウルトラキャパシタ市場は、現在のところ15億米ドルと評価されています。

今後5年間で42億7,000万米ドルに成長し、予測期間中の収益でCAGR 19%を記録すると予測されています。

中期的には、厳しい排出ガス規制と燃費規制が制定され、電気自動車の普及率を高めるための補助金や給付金といった政府の取り組みが増加していることから、予測期間中に大きな成長が見込まれます。

ウルトラキャパシタの使用はバッテリー負荷を拡大し、自動車メーカーが燃費効率、バッテリー寿命の延長、車両重量の軽減、CO2排出量の削減を達成することを可能にしました。ウルトラキャパシタは、世界中で厳しさを増す排ガス規制に対応するため、従来型、ハイブリッド、電気自動車など、あらゆるタイプの自動車に急速に普及する可能性が高いです。

ウルトラキャパシタは通常、自動車用バッテリーと並列に接続され、発進/停止や回生ブレーキのアプリケーションで発生する短い間隔(30秒以下)のピーク負荷需要をサポートします。ウルトラキャパシタが提供する高エネルギーの迅速な充放電能力は、自動車メーカーをスタート/ストップ・システムや回生ブレーキ・システムにウルトラキャパシタを配備させる原動力となった。自動車の内燃エンジン、燃料電池、バッテリーのような一次エネルギー源は、ピーク電力需要への対応や上記の用途におけるエネルギー奪還において非効率であることが確認されました。

自動車用ウルトラキャパシタの市場動向

厳しい排ガス規制の高まりと電気自動車需要の増加

世界各国政府は、排出量削減のための野心的な目標を設定しており、電気自動車の利用促進は、これらの目標を達成するための1つの方法と考えられています。例えば、欧州連合(EU)は2030年までに温室効果ガス排出量を55%削減することを目指しており、中国は2025年までに新車販売台数の25%を電気自動車にするという目標を掲げています。

ほとんどの電気自動車に使用されているリチウムイオン電池は、エネルギー密度、充電時間、全体的な性能の面で大きく向上しました。これにより、電気自動車はより実用的になり、消費者にとって魅力的なものとなった。

EVに対する需要の高まりは、電池化学と材料の技術的進歩につながります。安全性と性能を確保するためには、より高度で効率的な自動車用バッテリーが必要になります。多くの著名な自動車メーカーは、自動車用電池製造企業との長期的な取引関係の構築に注力しています。例えば

- 2023年6月、パナソニックホールディングスの担当者によると、日本企業はテスラと共同管理するネバダ州の工場で、電気自動車用電池の生産量を3年以内に10%増やす意向です。Panasonic Energyは、ギガファクトリー・ネバダに15番目の生産ラインを追加する計画です。Panasonic Energyは会議で、2026年3月までにネバダ工場の生産能力を10%増強する案を発表しました。

米国環境保護庁(EPA)と米国運輸省道路交通安全局(NHTSA)は、燃費の向上と二酸化炭素排出量の削減を確実にするため、環境に優しい自動車(乗用車と商用車の両方)の生産を支援する取り組みを行っています。こうした取り組みを通じて、政府は2025年までに約31億トンのCO2排出量を削減し、約60億バレルの石油を節約する計画です。

さらに、欧州連合(EU)は、乗用車と商用車のCO2排出レベルを規制する排出基準を設定しました。輸送機関の排出量は近年増加し、現在ではEU全体の温室効果ガス排出量の4分の1を占めています。

その結果、欧州委員会、欧州議会、EU加盟国は、小型車のCO2規制を2025年から2030年まで延長する準備を進めています。さらに、上記の基準を満たすために、ウルトラキャパシタの採用が増加しており、予測期間中も同様の動向が予想されます。

以上のような世界の市場開拓により、市場は予測期間中に大きな成長を遂げる可能性が高いです。

アジア太平洋と欧州が自動車用ウルトラキャパシタ市場を独占

欧州地域ではハイブリッド車や電気自動車の販売が急速に伸びており、自動車における電気エネルギーの最適利用を満たすためにウルトラキャパシタの需要が伸びると予想されます。

各地域の自動車メーカーとエコシステム利害関係者は、顧客のニーズと嗜好に基づいて変化する地域パターンに適応し始めました。自動車需要の増加と世界の生活水準の向上により、研究対象市場は拡大すると予想されます。さらに、都市化の進展と人口の増加が自動車需要を生み出しました。

アジア太平洋市場は、インフラの開拓と自動車販売の増加により、予測期間中により速いペースで成長すると予想されます。さらに、自動車に電子部品が大量に使用されている中国が収益面で市場をリードしており、日本、韓国、インドがこれに続いています。

中国は世界最大の電気自動車製造・消費国です。販売目標、有利な法律、自治体の大気質目標が国内需要を支えています。例えば、

- 中国は、電気自動車やハイブリッド車のメーカーに、新車販売台数の10%以上を占めなければならないという割り当てを課しました。また、北京市では、市民に電気自動車への乗り換えを促すため、内燃エンジン車の登録許可証を月に1万台しか発行していないです。

中国はすでにハイブリッドバスにスーパーキャパシタを使用しています。これらのバスにはストップ・スタート・エンジンが搭載されており、スーパーキャパシタによってバッテリーへの負荷が軽減されるため、バッテリーの寿命が延びる。

継続的な技術革新により、中国メーカーはスーパーキャパシタのポートフォリオを拡大しています。中国の国有鉄道車両メーカーで世界最大の鉄道建設会社であるCRRCは、より高効率でより長期間電気バスに電力を供給する可能性のあるグラフェンベースのスーパーキャパシタを開発しました。

自動車用ウルトラキャパシタ産業概要

自動車用ウルトラキャパシタ市場は、Maxwell Technologies、Skeleton Technologies、Kemet Corporation、Panasonic Corporationなど、複数の主要企業によって支配されています。製造施設の急速な拡大、自動車メーカーと部品メーカー間のパートナーシップの増加は、予測期間中に市場の大きな成長を示す可能性が高いです。例えば

- 2023年3月、Invest EstoniaとSkeleton Technologiesは、ライプチヒに建設する2番目の生産ユニットのために、ドイツ政府とザクセン州から5,374万米ドルを受け取った。このファンドを通じて、同社はウルトラキャパシタなどの製品を拡大しました。

- 2022年10月、Skeleton Technologiesはスーパーバッテリーを発表し、パートナーとしてシェルを公表しました。スーパーバッテリーは、スーパーキャパシターとバッテリーの特性を組み合わせた革新的な技術です。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 電気自動車需要の増加

- 市場抑制要因

- 製品に関連する高コスト

- 業界の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模(米ドル))

- 用途別

- 発進停止操作

- 回生ブレーキシステム

- その他の用途

- 車種別

- 乗用車

- 商用車

- 販売チャネル別

- 相手先ブランド製造(OEM)

- アフターマーケット

- 地域別

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- その他の欧州

- アジア太平洋

- インド

- 中国

- 日本

- 韓国

- その他のアジア太平洋

- その他

- 南米

- 中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Maxwell Technologies

- Skeleton Technologies

- Panasonic Corporation

- Nesscap Battery

- Nippon Chem-Con Corporation

- Hitachi AIC Inc.

- ELNA America Inc.

- LOXUS Inc.

- Yunasko Ltd

- Nichicon Corporation

- LS Mtron Ltd

第7章 市場機会と今後の動向

The automotive ultra-capacitor market is valued at USD 1.50 billion in the current year. It is anticipated to grow to USD 4.27 billion by the next five years, registering a CAGR of 19% in terms of revenue during the forecast period.

Over the medium term, the enactment of stringent emissions and fuel economy norms and increasing government initiatives, in terms of subsidies and benefits for increasing the adoption rate of electric vehicles, is expected to witness major growth during the forecast period.

The use of ultra-capacitors expanded the battery load and enabled vehicle manufacturers to achieve fuel efficiency, extended battery life, reduced vehicle weight, and reduced CO2 emissions. Ultra-capacitors are likely to penetrate at a faster rate in all vehicle types, including conventional, hybrid, and electric vehicles, to meet the growing stringent emission rules across the world.

Ultra-capacitors, typically connected in tandem with vehicle batteries, support peak load demands for short intervals (which are less than 30 seconds) encountered during start/stop and regeneration braking applications. The capacity for quick recharge and discharge of high energy offered by ultra-capacitors drove the vehicle manufacturers to deploy them in the start/stop systems and regenerative braking systems. Primary energy sources, like internal combustion engines, fuel cells, and batteries in vehicles, were identified to be inefficient in handling peak power demand or recapturing energy during the applications above.

Automotive Ultra-capacitor Market Trends

Growing Stringent Emission Regulations and Increase in demand for Electric Vehicles

Governments around the world are setting ambitious targets to reduce emissions, and promoting the use of electric vehicles is seen as one way to achieve these goals. For instance, the European Union aims to reduce its greenhouse gas emissions by 55% by 2030, and China set a target of having 25% of new cars sold by 2025 to be electric.

Lithium-ion batteries, which are used in most electric vehicles, saw a significant improvement in terms of energy density, charging time, and overall performance. It made electric vehicles more practical and appealing to consumers.

The growing demand for EVs will lead to technological advancements in battery chemistry and materials. It will require more sophisticated and efficient automotive batteries to ensure safety and performance. Many prominent automobile manufacturers are focusing on building long-term business relationships with automotive battery manufacturing companies. For instance,

- In June 2023, according to a Panasonic Holdings representative, the Japanese corporation intends to increase the output of electric vehicle batteries at a Nevada factory jointly managed with Tesla by 10% within three years. Panasonic Energy plans to add a 15th production line to the Gigafactory Nevada. At a meeting, Panasonic Energy announced a proposal to boost the Nevada factory's manufacturing capacity by 10% by March 2026.

The United States Environmental Protection Agency (EPA) and the National Highway Traffic Safety Administration (NHTSA) are taking initiatives to support the production of eco-friendly vehicles (both passenger vehicles and commercial vehicles) to ensure improved fuel economy and reduced carbon emissions. Through these initiatives, the government is planning to reduce about 3,100 million metric tons of CO2 emissions and save about 6 billion barrels of oil by 2025.

Additionally, the European Union (EU) set emission standards to regulate the CO2 emission levels of passenger cars and commercial vehicles. Transport emissions increased in recent years and now account for a quarter of the EU's total GHG emissions.

As a result, the European Commission, European Parliament, and EU member states are preparing to extend the light-duty vehicles' CO2 regulation to 2025-2030. Furthermore, to meet the standards above, the adoption of the ultra-capacitor is increasing and is expected to witness the same trend during the forecast period.

With the development mentioned above across the globe, the market is likely to witness major growth during the forecast period.

Asia-Pacific and Europe to Dominate the Automotive Ultra-capacitor Market

With the rapidly growing hybrid and electric vehicle sales in the European region, the demand for ultra-capacitors is anticipated to grow to meet the optimal utilization of electric energy in vehicles.

Automotive manufacturers and ecosystem stakeholders in each region began to adapt to the changing regional patterns based on customer needs and preferences. The market studied is expected to expand due to rising vehicle demand and rising living standards around the globe. Furthermore, increased urbanization and an increasing population created a demand for automobiles.

The Asia-Pacific market is expected to grow at a faster pace during the forecast period, owing to development in infrastructure and increased vehicle sales. Furthermore, China is leading the market in terms of revenue due to its massive use of electronic components in vehicles, followed by Japan, Korea, and India.

China is the largest manufacturer and consumer of electric vehicles in the world. Sales targets, favorable laws, and municipal air-quality targets are supporting domestic demand. For instance,

- China imposed a quota on manufacturers of electric or hybrid vehicles, which must represent at least 10% of total new sales. Also, the city of Beijing only issues 10,000 permits for the registration of combustion engine vehicles per month to encourage its inhabitants to switch to electric vehicles.

China is already using supercapacitors in hybrid buses. These buses are equipped with stop-start engines, in which supercapacitors reduce the load on the battery, which increases the lifetime of the batteries.

Due to continuous innovation, Chinese manufacturers are expanding their supercapacitor portfolio. The CRRC, the Chinese state-owned rolling stock manufacturer and the world's largest train builder developed graphene-based supercapacitors that may power electric buses with higher efficiency and for a longer period.

Automotive Ultra-capacitor Industry Overview

The automotive ultra-capacitor market is dominated by several key players, such as Maxwell Technologies, Skeleton Technologies, Kemet Corporation, and Panasonic Corporation, among others. The rapid expansion of manufacturing facilities and an increase in partnership between the vehicle manufacturer and the component manufacturer is likely to witness major growth for the market during the forecast period. For instance,

- In March 2023, Invest Estonia and Skeleton Technologies received USD 53.74 million from the German government and the state of Saxony for its second production unit to be built in Leipzig. Through this fund, the company expanded its products, including ultra-capacitor.

- In October 2022, Skeleton Technologies introduced its SuperBattery and unveiled Shell as a partner. SuperBattery is an innovative technology combining the characteristics of supercapacitors and batteries.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Rise in demand for Electric Vehicles

- 4.2 Market Restraints

- 4.2.1 High Cost Associated With Product

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value (USD))

- 5.1 By Application

- 5.1.1 Start-stop Operation

- 5.1.2 Regenerative Braking System

- 5.1.3 Other Applications

- 5.2 By Vehicle Type

- 5.2.1 Passenger Car

- 5.2.2 Commercial Vehicle

- 5.3 By Sales Channel

- 5.3.1 Original Equipment Manufacturer (OEM)

- 5.3.2 Aftermarket

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.4.1 South America

- 5.4.4.2 Middle-East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Maxwell Technologies

- 6.2.2 Skeleton Technologies

- 6.2.3 Panasonic Corporation

- 6.2.4 Nesscap Battery

- 6.2.5 Nippon Chem-Con Corporation

- 6.2.6 Hitachi AIC Inc.

- 6.2.7 ELNA America Inc.

- 6.2.8 LOXUS Inc.

- 6.2.9 Yunasko Ltd

- 6.2.10 Nichicon Corporation

- 6.2.11 LS Mtron Ltd