|

市場調査レポート

商品コード

1406109

散弾銃・ライフル:市場シェア分析、産業動向・統計、成長予測、2024年~2029年Shotgun and Rifles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 散弾銃・ライフル:市場シェア分析、産業動向・統計、成長予測、2024年~2029年 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

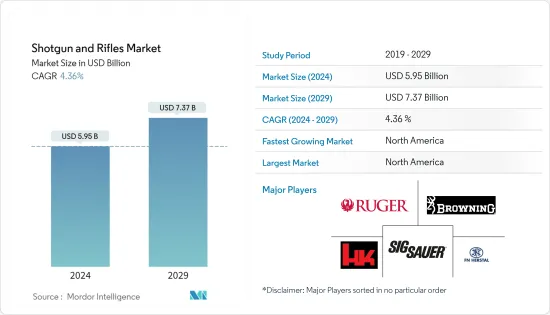

散弾銃・ライフル市場規模は2024年に59億5,000万米ドルと推定され、2029年には73億7,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは4.36%で成長する見込みです。

テロ攻撃の多発により、このような事件を効果的に防止し、人命の損失を最小限に抑えるため、法執行機関の武器の近代化が進んでいます。これが散弾銃・ライフルの需要を押し上げ、予測期間中の調達イニシアチブを強化すると予想されます。地政学的紛争の増加は、進行中の兵士近代化プログラムの一環として新しい装備の調達を促進し、主戦闘戦車(MBT)や装甲兵員輸送車(APC)などの重装甲車両の導入は、対物ライフルなどの徹甲兵器の需要を促進しています。各国の防衛予算の増加により、必要に応じてカスタマイズされた武器を調達できるようになり、市場を牽引しています。

弾丸装填の自動化、自己制御弾丸、狙撃用アクセサリーの最先端技術などの技術進歩により、将来的にはライフルの効率と精度が向上すると予想されます。しかし、各国政府による厳格な銃所持法の制定は、銃製造企業の散弾銃・ライフル市場への参入を制限します。

また、様々な政府や地域の厳しい規制の枠組みや銃刀法が、特に民間のエンドユーザーにとっては市場の成長を抑制します。こうした規制には、身元調査、待機期間、銃器所有の制限などがあり、市場へのアクセスや販売に影響を及ぼす可能性があります。こうした規制の遵守は、市場のメーカーやバイヤーにとって課題となります。

散弾銃とライフルの市場動向

半自動/自動セグメントが最も高い成長率を示す

半自動/自動の武器の利用は、洗練された武器の急速な生産と、主要途上国/先進国における防衛装備の近代化に関連した動向により増加しています。さらに、精密な兵器システムの必要性から、増加するテロ事件に対抗するための先端兵器への注目が高まっています。ハイテク、軽自動、インテリジェント兵器の導入も市場の成長を後押ししています。例えば、米国軍は、特殊作戦部隊(SOF)が敵や現地のパートナー部隊を模倣した武装を訓練で使用したり、さまざまな研究開発や試験・評価目的で使用するために、さまざまな外国製の武器の在庫を維持しています。

予測期間中、北米が優位を占める

北米は現在、散弾銃・ライフルの最大市場であり、予測期間中も同地域の優位が続くと予想されます。ライフル銃の需要のほとんどは米国軍によるものです。米国陸軍の2023会計年度予算要求では、同軍は17,164の火器管制モジュール、1,704の自動小銃、16,348の小銃を取得することになっています。米国軍は、特殊作戦部隊(SOF)が敵や現地のパートナー部隊を模した武装を訓練で使用するためや、さまざまな研究開発、試験・評価目的で外国製の武器の在庫を維持しています。

さらに米国陸軍は、M4カービンとM249分隊自動小銃の両方を兵士用に置き換えるため、新弾薬を中心に組み立てられた12万丁以上の新型軽機関銃と小銃の購入を計画しています。次世代分隊武器(NGSW)プログラムは、陸軍の歩兵、偵察兵、戦闘工兵などの近接戦闘部隊の標準的な小銃と分隊機関銃を置き換えるために設計されました。軍事調達に加え、銃乱射事件などの事件は、この地域の小銃とその弾薬の民間および国土安全保障の調達市場を推進してきました。例えば、2022年11月、米国陸軍はロシア製の5.45x39mm AK-74アサルトライフルまたは他国で製造されたコピー品の購入を計画しました。陸軍のニュージャージー州契約司令部(CCNJ)は、米国政府がAK-74タイプのカラシニコフ・アサルトライフルとサポート部品のサプライヤーに関心を寄せているとの通知を出しました。このように、国防分野への支出の増加、軍事・民間用途の銃器調達の増加が、国全体の市場成長を牽引しています。

散弾銃・ライフル産業の概要

散弾銃・ライフル市場は断片化されており、いくつかの国内および世界のプレーヤーが市場で大きなシェアを占めています。市場の主なプレーヤーとしては、Sturm, Ruger &Co., Inc.、Sig Sauer, Inc.、Heckler & Koch GmbH、FN HERSTAL、Browning International S.A.などが挙げられます。主要OEMは、新規顧客の獲得に役立つ先進的な製品の開発に注力しています。メーカー各社は、過酷な条件下でも最高の性能を発揮する素材を使用した武器のさまざまな部品を開発しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 射距離

- 短距離

- 中距離

- 長距離

- エンドユーザー

- 軍事

- 民間・法執行機関

- 装填メカニズム

- 手動

- 半自動/自動

- 地域

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- エジプト

- その他中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Remington Ammunition(Vista Outdoor Inc.)

- Sturm, Ruger & Co., Inc.

- Sig Sauer, Inc.

- Heckler & Koch GmbH

- O. F. Mossberg & Sons, Inc.

- Kalashnikov Concern JSC

- Fabbrica d'Armi Pietro Beretta S.p.A.

- CheyTac USA

- FN HERSTAL

- Barrett

- Springfield, Inc,

- Browning International S.A.

- Benelli Armi S.p.A.

第7章 市場機会と今後の動向

The Shotgun and Rifles Market size is estimated at USD 5.95 billion in 2024, and is expected to reach USD 7.37 billion by 2029, growing at a CAGR of 4.36% during the forecast period (2024-2029).

The rampant incidents of terror attacks have resulted in the modernization of the weapons of law enforcement agencies to prevent such incidences effectively and minimize loss of life. This has driven the demand for rifles and shotguns and is expected to bolster the procurement initiatives during the forecast period. The rise in geopolitical conflicts has driven the procurement of new equipment as part of ongoing soldier modernization programs, the induction of heavily armored vehicles such as main battle tanks (MBTs) and armored personnel carriers (APCs) has driven the demand for Armor-piercing weaponry, such as anti-material rifles. The rising defense budget of various countries allows them to procure customized weapons as required to drive the market.

Technological advancements in automation in bullet loading, self-steering bullets, and cutting-edge technologies in sniper accessories are all expected to make rifles more efficient and accurate in future years. However, incorporating stringent gun ownership laws by various governments will restrict gun manufacturing companies from entering the shotgun and rifle market.

Also, various governments and regions' stringent regulatory frameworks and firearm laws restrain the market's growth, especially for civilian end users. These regulations can include background checks, waiting periods, and limits on firearm ownership, which can affect market accessibility and sales. Compliance with these regulations poses challenges for manufacturers and buyers in the market.

Shotgun & Rifles Market Trends

Semi-Automatic/Automatic Segment to Have the Highest Growth Rate

The utilization of semi-automatic/automatic weapons has increased due to the rapid production of sophisticated weapons and trends linked to the modernization of defense equipment in key developing/developed countries. In addition, the need for precision weapon systems has increased the focus on advanced weapons to counter growing incidents of terrorism. Introducing high-tech, light automatic, and intelligent weapons also fuels the market growth. For instance, The US military maintains stocks of various foreign-made arms for use by special operations forces (SOF) in training exercises to arm those replicating the enemy or local partner forces and for different research and development and test and evaluation purposes.

In April 2022, SIG Sauer Inc. won a 10-year production contract from the US Army to supply two new soldier rifles: XM5 and OMC250. For soldiers involved in close-quarters combat, the XM5 will eventually replace the M4/M4A1 carbine rifle, while the XM250 will replace the M249 Squad Automatic Weapon. Both new rifles will also use the new 6.8 mm standard cartridge family of ammunition and a new fire control system. The initial delivery order on the contract is USD 20.4 million for weapons and ammunition that will undergo testing, and the contract's total value is USD 4.5 billion. Such developments will boost the segment growth during the forecast period.

North America to Dominate During the Forecast Period

North America is currently the largest market for rifles and shotguns, and the region is also expected to continue its dominance during the forecast period. Most of the demand for rifles is from the US military. The US Army's 2023 fiscal year budget request calls for the service to acquire 17,164 fire control modules, 1,704 automatic rifles, and 16,348 rifles. The US military maintains stocks of foreign-made arms for use by special operations forces (SOF) in training exercises to arm those replicating the enemy or local partner forces and also for different research and development and test and evaluation purposes.

Furthermore, the US Army plans to buy a mix of more than 120,000 new light machine guns and rifles, built around new ammunition, to replace both the M4 carbine and M249 Squad Automatic Weapon for its soldiers. The Next Generation Squad Weapon (NGSW) program was designed to replace the standard rifle and squad machine gun for close-combat units such as infantry, scouts, and combat engineers in the Army. In addition to military procurement, incidents such as mass shootings have propelled the market for civilian and homeland security procurements of rifles and their ammunition in the region. For instance, in November 2022, The US Army planned to purchase Russian-made 5.45x39mm AK-74 assault rifles or copies made in other countries. The Army Contracting Command-New Jersey (CCNJ) issued a notice for the US Government's interest in AK-74-type Kalashnikov assault rifles and support parts suppliers. Thus, growing expenditure on the defense sector and rising procurement of firearms for military and civil applications drive the market growth across the country.

Shotgun & Rifles Industry Overview

The shotgun and rifle market is fragmented, with several local and global players holding significant shares in the market. Some of the key players in the market are Sturm, Ruger & Co., Inc., Sig Sauer, Inc., Heckler & Koch GmbH, FN HERSTAL, and Browning International S.A. The key OEMs focus on developing advanced products that help them attract new customers. The manufacturers are developing different parts of the weapons with materials that will be of best use, even in hostile conditions.

For instance, in 2022, Sig Sauer and the US Government conducted numerous technical tests and a Soldier touchpoint concerning the most recent weapon configuration. This engagement aimed to obtain user acceptance, load carriage, and integration into the XM157 fire control optic developed by Vortex Optics Inc., which would be mounted on any XM7 or XM250 automatic rifle. Such contracts will help the players tap into new regional markets, thereby increasing their market presence and opportunities for growth.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Range

- 5.1.1 Short Range

- 5.1.2 Medium Range

- 5.1.3 Long Range

- 5.2 End User

- 5.2.1 Military

- 5.2.2 Civilian and Law Enforcement

- 5.3 Weapon Loading Mechanism

- 5.3.1 Manual

- 5.3.2 Semi-Automotic/Automatic

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Russia

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.4.1 Brazil

- 5.4.4.2 Mexico

- 5.4.4.3 Rest of Latin America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Egypt

- 5.4.5.4 Rest of Middle-East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Remington Ammunition (Vista Outdoor Inc.)

- 6.2.2 Sturm, Ruger & Co., Inc.

- 6.2.3 Sig Sauer, Inc.

- 6.2.4 Heckler & Koch GmbH

- 6.2.5 O. F. Mossberg & Sons, Inc.

- 6.2.6 Kalashnikov Concern JSC

- 6.2.7 Fabbrica d'Armi Pietro Beretta S.p.A.

- 6.2.8 CheyTac USA

- 6.2.9 FN HERSTAL

- 6.2.10 Barrett

- 6.2.11 Springfield, Inc,

- 6.2.12 Browning International S.A.

- 6.2.13 Benelli Armi S.p.A.